SAFRY - General Electric: A Long-Term Aerospace Powerhouse Buy

2023-04-27 13:39:12 ET

Summary

- General Electric results exceed expectations but energy segments are pressuring aerospace strength.

- General Electric plans to spin off the energy and power division in 2024 leaving the company as an aerospace powerhouse.

- Stock leaves little upside for this year, but significantly more for 2024.

General Electric ( GE ) reported earnings on the 25 th of April. In the past, I have owned shares of General Electric based on the prospects of its aerospace business. However, back then the company was more diversified which did not make the aerospace segment strength stand out and I sold my shares. Today General Electric is a vastly more simplified company with GE Aerospace focusing on commercial aerospace and defense and GE Vernova focusing on renewable energy and power. With an aerospace background and interest in aerospace investments, both the aerospace and energy segments are very interesting and better allow me to analyze the business which I will do in this report.

I previously covered General Electric’s joint venture with Safran ( SAFRF ) winning the bulk of the engine selections for the Air India order. In this report, I will be discussing the Q1 2023 results, the updated guidance and provide a stock price target for General Electric.

General Electric Aerospace Leads The Way

{kind=link}

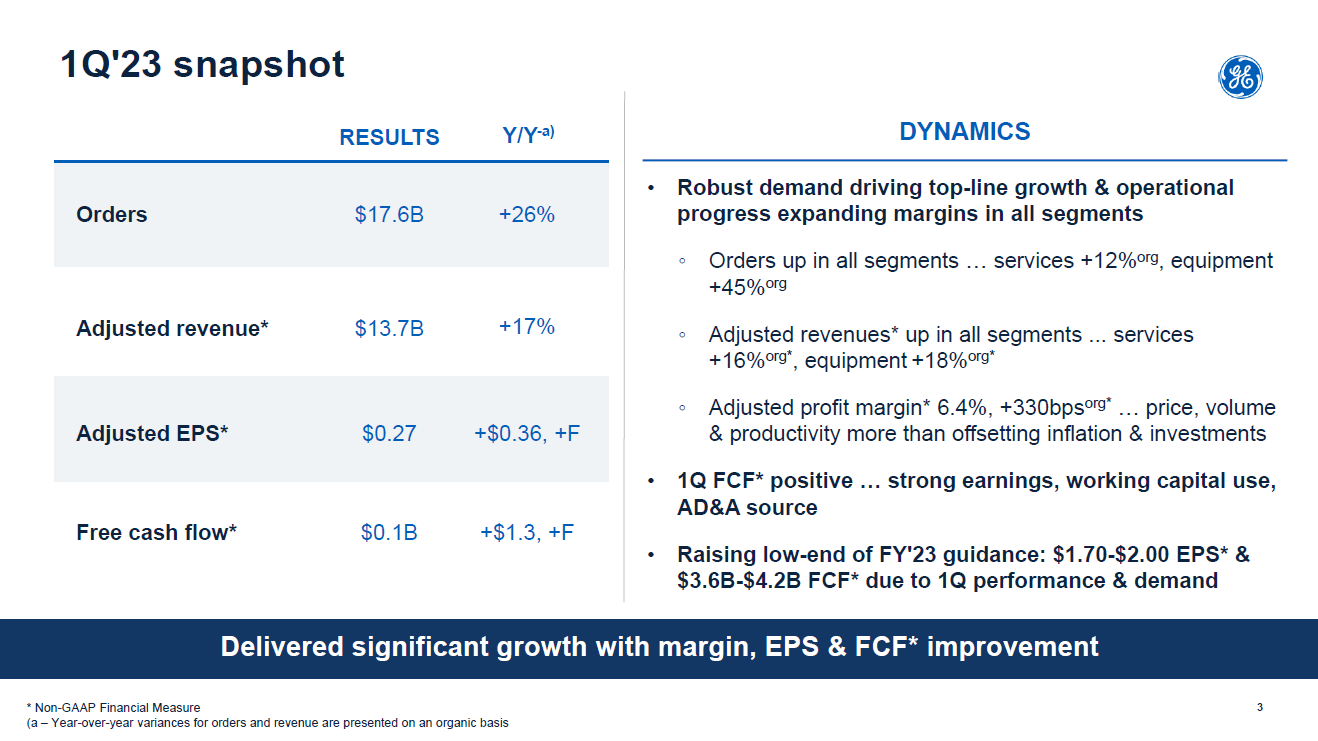

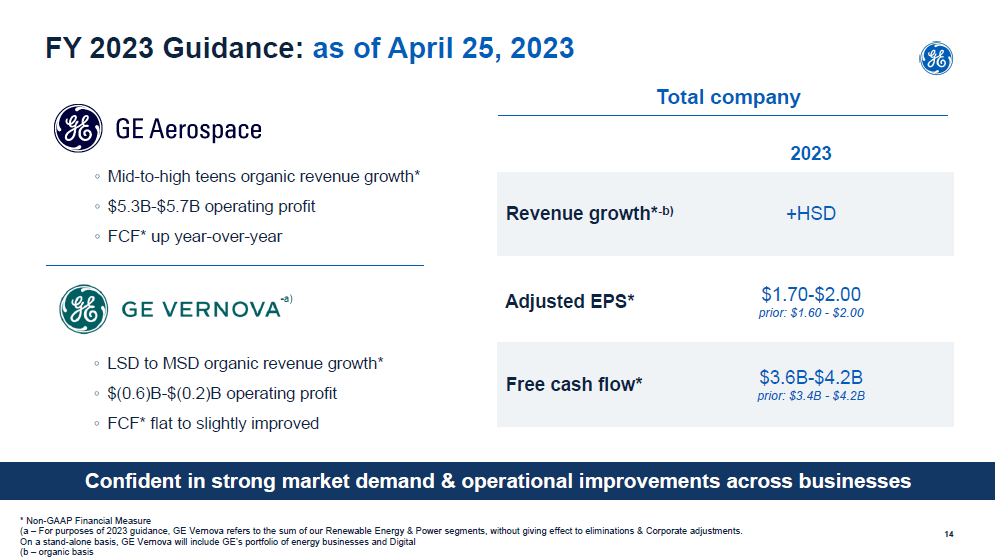

For the first quarter, analysts had expected revenues of $13.46 billion and core earnings per share of $0.14. General Electric beat those expectations by $1.03 billion posting 17% growth in adjusted revenues and earnings per share of $0.27 beating the consensus by $0.13. So, General Electric had a good quarter. Order intake grew 26%, revenues grew 17% and for the first time since 2015, the company had positive free cash flow.

{kind=link}

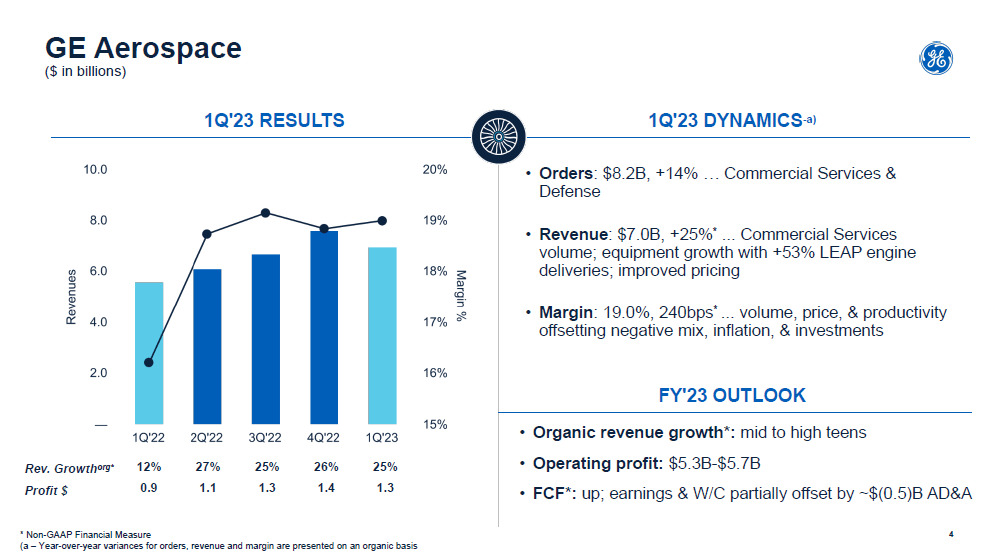

Revenues were strong at $7 billion providing 25% year-over-year growth. This was driven by 19% higher equipment revenues and 27% higher service revenues. As flight activity increases and OEMs are looking to push airplane production higher, the significantly higher revenues fit the expectations. Especially on the services side, it should be noted that Q1 2022 was before air travel demand started booming and so year-over-year we see a big jump in services revenues along with a jump in margins driven by the high-margin nature of services and better pricing. What should also be noted is that the margins strongly expanded even though CFM LEAP engine deliveries increased by 53%. This is important to highlight since those deliveries are loss-making from delivery as well as service perspective. So, being able to expand the margin despite the LEAP pressure really displayed strength.

What should be kept in mind is that as flight activity and deliveries ramped up throughout the year in 2022, we will not be seeing 25% revenue growth for the year, but this will be more moderate in the mid to high teens due to a better comparable period last year for the remainder of this year. Nevertheless, with a profit outlook of $5.3 billion to $5.7 billion, the year-over-year profit outlook signals quarterly profit above Q1 2023 levels and 12% to 22% year-over-year growth in profits.

{kind=link}

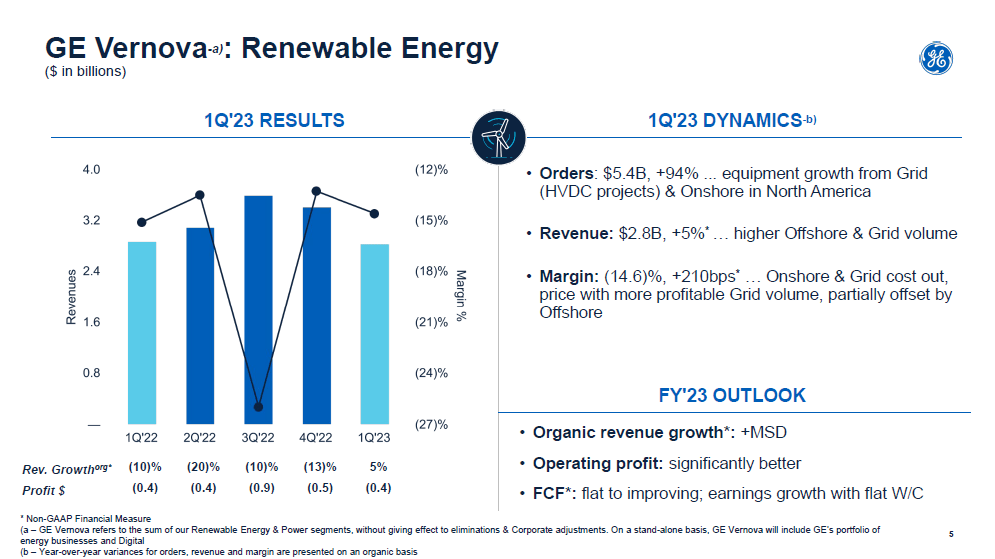

Energy transition and electrification of transport means is a hot topic at the moment, but the reality is that being in that part of the business doesn’t necessarily make you rich. Order intake was up 94% and revenues were up 5%. The Grid business is profitable which helped the margins, but the business was as profitable as it was last year and the second quarter of the year will be as loss-making with an improvement in year-over-year numbers in the second half of the year but perhaps that is not a big surprise with the Q3 2022 profitability being a negative outlier and that gives a better comp for the second half of the year which on losses of $0.4 billion throughout every remaining quarter of the year would indicate a 37.5% improvement in losses. The inflection point for Renewable Energy should be in 2024 as demand increases and better pricing and cost eliminations kick in.

{kind=link}

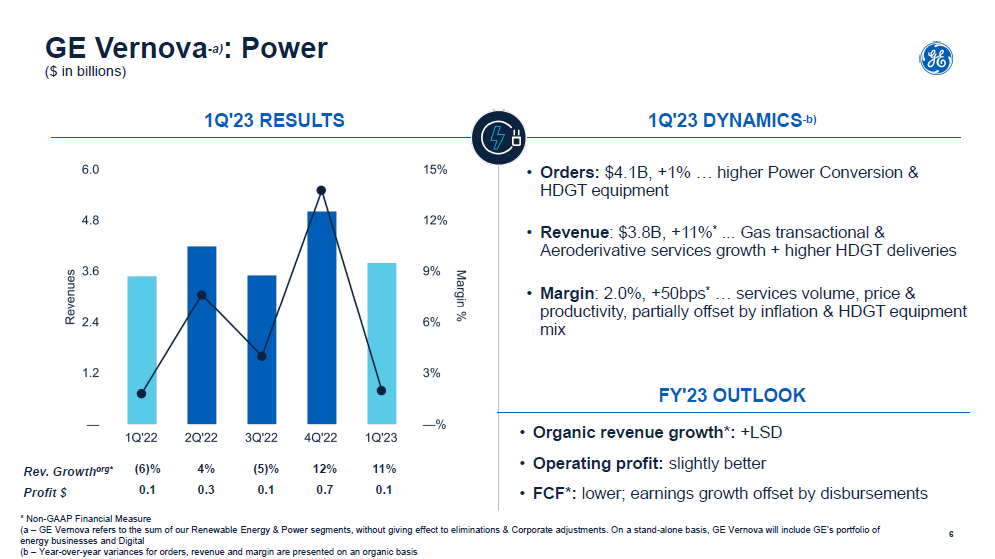

The power business also is not a great business in the short term. The revenues fluctuate and so do the margins. That is driven by mix with heavy duty gas turbines being a positive to topline but a headwind to margins. The Power segment is expected to be a long-term value segment for GE Vernova, but as of right now, it is a profitable business with fluctuating margins and revenues.

{kind=link}

If you look at the results, what can be seen rather quickly is that GE Aerospace is doing quite well, but its renewable energy business eats into the profits. However, the first quarter results were better than expected leading to revision of the 2023 guidance. Adjusted EPS has been increased at the lower bound by $0.10 and free cash flow has been increased at the lower bound by $0.2 billion. The second quarter will be break-even from cash flow perspective which really positions the company for an extremely strong second half of the year with cash generation of at least $3.5 billion. What is also helping the business from a fundamental point of view is the wind down in the company’s stake in AerCap (AER), the complete exit of the Baker Hughes ( BKR ) stake and the spin-off of GE HealthCare (GEHC) in which GE has a 19.9% share. As the value of the stake fluctuates, so will the corporate results but overall the stakes are to be monetized over time providing additional liquidity next to the GE core businesses. GE stock has dropped following the results announcement, but I would argue that this is not driven by the results of the GE core businesses but by the GE Healthcare business in which GE still has a stake.

Capitalizing On Aerospace Strength From 2024

When I was invested in General Electric, the big issue was that its aerospace gem was covered by businesses with weaker prospects and in some way with GE Vernova we are seeing the same as near-term aerospace strength is offset by the energy segment. The plan is to spin off GE Vernova in 2024, which from operational point of view would make GE a full aerospace play with exposure to the leasing, healthcare and energy through the stakes it owns. Exiting those stakes will take time but GE is also positioning Vernova for the long-term which will allow the company to efficiently monetize that stake in due time while investors will be having the ability to invest in a pure aerospace name.

Is General Electric Stock A Buy, Sell or Hold?

| Valuation General Electric |

| Market Capitalization [$ bn] |

| $ 104.90 |

| Preferred stock [$ bn] |

| $ 3.00 |

| Total debt [$ bn] |

| $ 22.42 |

| Cash and equivalents [$ bn] |

| $ 24.82 |

| Minority and controlling interests [$ bn] |

| $ 1.17 |

| Total Enterprise Value [$ bn] |

| $ 106.68 |

| EBITDA 2023 [$ bn] |

| $ 7.19 |

| EV/EBITDA |

| 14.8x |

| Current price |

| $ 96.21 |

| Median |

| Current |

| Industry |

| EV/EBITDA |

| 14.14 |

| 15.29 |

| 15.42 |

| Price target |

| $ 91.70 |

| $ 99.16 |

| $ 100.01 |

| Upside |

| -5% |

| 3% |

| 4% |

One thing that General Electric has going for itself is a big pile of cash and cash equivalents due to the stakes it holds for sale in various companies bringing it in a net cash position, which is a plus. Parsing the numbers, we see that the upside based on 2023 earnings is not huge at 3 to 4 percent and even negative when using the median. However, with General Electric being a significantly different business compared to prior years that median in my view not reflective for forward analysis and valuation.

We’re currently working on development of enterprise valuation tools for subscribers of The Aerospace Forum and when parsing the numbers using that more advanced tool, we see that while for this year the upside is rather limited, the upside based on 2024 earnings is in the range of 20 to 35 percent.

Conclusion: General Electric Provides Little Upside For 2023, Significantly More Attractive With 2024 In Mind

General Electric is in the final stages of refocusing its business, which will leave the company as a pure aerospace company with exposure via stakes in other industries. With the growth prospect ahead for aerospace and the big presence General Electric has with its turbofans in the entire airplane market arena, I do believe that the company is positioned well for long-term value generation and stock price appreciation.

For further details see:

General Electric: A Long-Term Aerospace Powerhouse Buy