ARZGF - Generali: Stability And High Dividend But Wait For A Better Entry Point

Summary

- The company is a great pick for dividend-oriented investors.

- There are some hidden risks mainly related to geographical diversification.

- Despite solid financial results, the company may still have some downsides in the next quarters.

- Generali is slightly undervalued, but does not have a large safety margin.

Assicurazioni Generali S.p.A. ( ARZGF ) is the first Italian insurance company , and it is one of the largest insurance groups in Europe, with also a strong presence in Asia and Latin America. Despite some hidden risks, Generali is definitely a buy-and-hold company to keep for the long term, especially thanks to its dividend well above the market average, and its reliability proven in the past years. However, I think this is not a good time to enter a position as, given the recessionary and inflationary environment in Europe, the stock will probably underperform over the next 6-12 months. To sum up, I gave the company a hold rating.

Dividend

Almost certainly, one of the most interesting things about Generali is its dividend. With a Trailing Annual Dividend Rate of €1.07 per share and a Dividend Yield of 6.23%, it far outperforms the dividend of most Italian and European companies. Another very interesting thing for dividend-oriented investors, is that the share coupon currently exceeds the Italian bond yield by more than 2% (IT10Y yield is around 4.00%/4.20%) and it also has a higher rating (A3 stable, while the Italian 10Y bond is Baa3 negative). Therefore, compared to the "risk free" investment, Generali is not only more profitable, but also financially safer on paper.

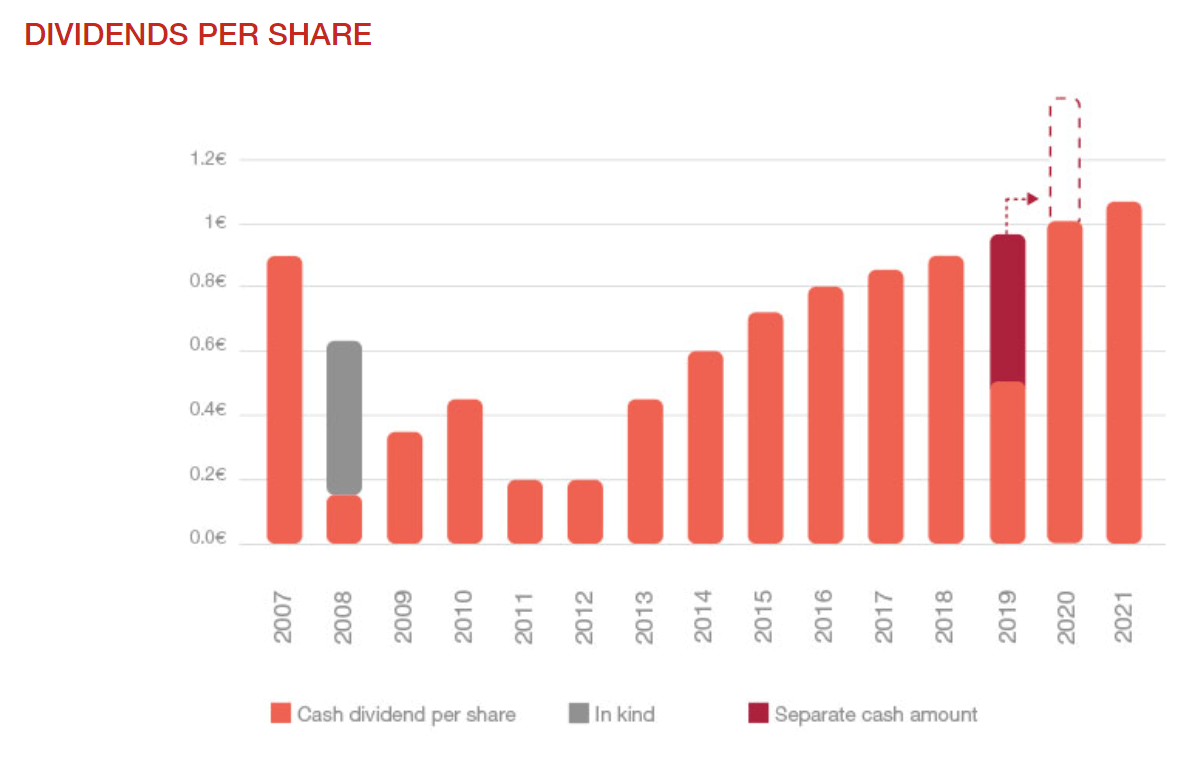

Furthermore, as can be seen from the graph below, Generali has continued to raise its dividend since 2012 with a CAGR of nearly 27% and the company has announced its intention to continue this trend.

Dividend per Share (Generali's Official Website)

{kind=link}

Indeed, management has indicated a total dividend distribution of €5,200 - €5,600 million between 2022 and 2024, against €4,500 million in the three-year period 2019-2021. Therefore, the Forward Annual Dividend Rate is estimated to be €1.53 per share, with a Dividend Yield of 8.80%. In summary a good deal, although the payout ratio may exceed 100% from the current 90%.

On the other hand, as I explain below, the risk is that Generali could shrink and reach new bottoms in the current markets, thus making the investment a double-edged sword if not seen in a long term perspective.

The business is very solid, but…

Generali is undoubtedly a very solid and reliable company with a business model in continuous, albeit slow, growth. Moreover, it has a really capable management and, in recent years, there have been no major twists or sensational losses capable of undermining the company’s stability. There are two main points to underline these aspects: the first regards financial solidity. Generali has an “A positive” rating according to Fitch, an “A3 stable” rating according to Moody's and an “A stable” rating according to AM Best, moreover it has a Solvency Ratio of 223% (according to data as of September 2022) which is a truly outstanding result. The second point regards the strategic acquisitions carried out in the last few years. The acquisition of Cattolica is an example, since it allows Generali to consolidate its presence on the Italian market and significantly improves its profitability (analysts foresee a normalized net income of Cattolica's core activities of at least €145 million in 2024 and €171-€178 million in 2025).

On the other hand, there are some aspects that do not convince me.

First of all, while Generali may appear to be very diversified, there is a clear exposure to European markets, with France, Italy and Germany alone accounting for 75% of Gross Written Premiums. This makes the company very vulnerable to just one geographical area: in a nutshell, if Europe goes badly, Generali follows. Furthermore, in the International segment, there is a significant exposure to the South America and Chinese markets where there is a huge economic and political risk respectively.

Finally, there is an almost total lack of strong presence in the US and UK markets, which have always been safer and more active.

An example of this "risky" geographical diversification can be found in the latest Generali report where we read:

Net result was stable at € 2,233 million (-0.8%). Excluding impacts from Russian investments, the net result would have grown to € 2,374 million (+5.5%)

This is a difference of €141 million!

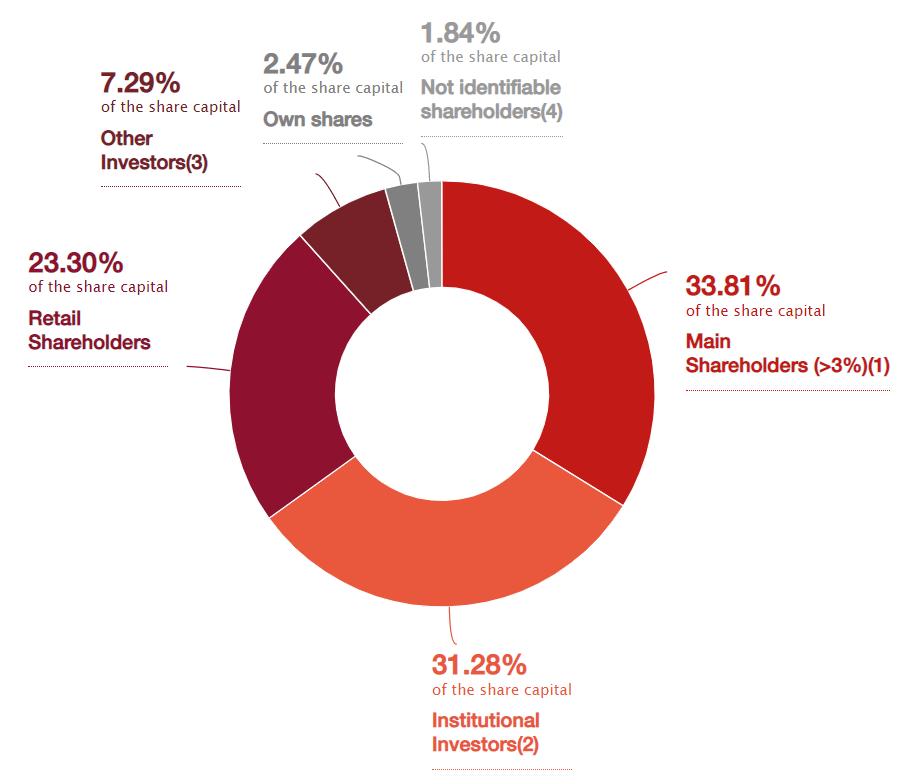

Another aspect to take into consideration is Share Ownership which is very fragmented, as the main shareholders with more than 3% of the ownership of the company represent almost 34% of the total. Therefore, the risk is given by a lack of unity in the strategic choices for the improvement of the company.

Share Ownership (Generali's Official Website)

{kind=link}

Valuation

To value the company I used a DDM (Dividend Discount Model) since I wanted a more flexible alternative to the DCF (Discounted Cash Flow Model) I usually use.

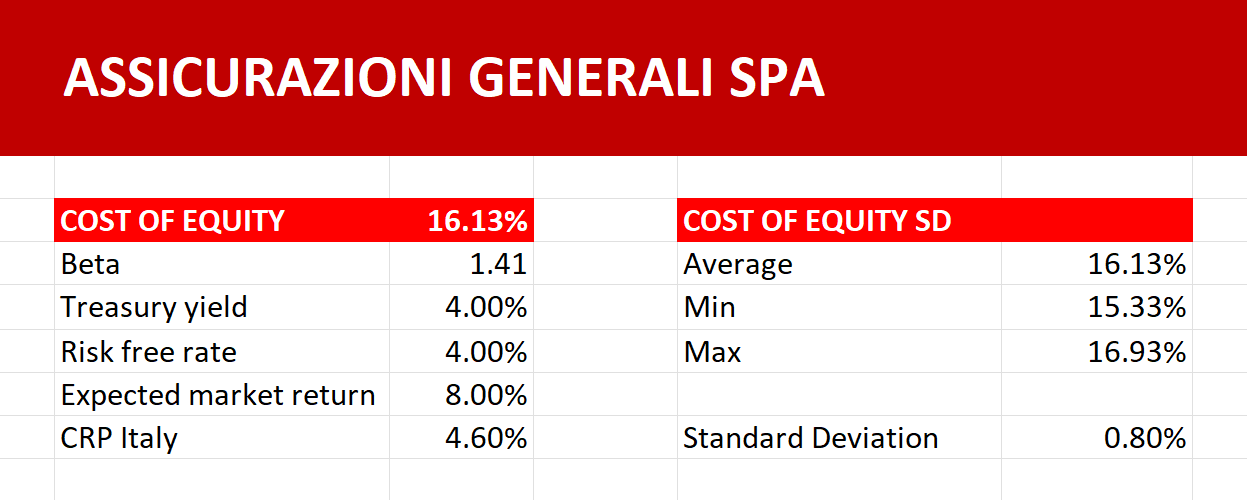

First of all, I used the company's last 10 years financial data to project the Dividend Growth. Then I estimated the Cost of Equity, assuming a Risk Free Rate of 4.00% (I used the 10Y yield of Italian bond as a reference) and a country risk premium of 4.60%. Since the DDM model is extremely sensitive to inputs, I took a wider range of Cost of Equity values, ??as the Beta and the Risk Free Rate vary, in order to then use them in the DDM table also considering errors.

Cost of Equity Calculations (Personal Excel Model)

{kind=link}

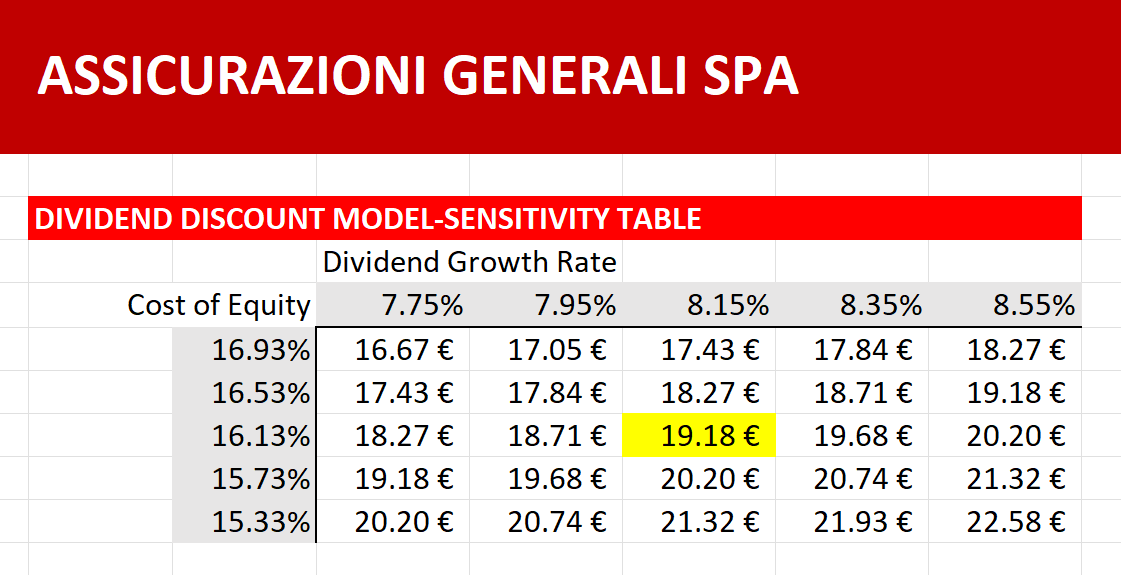

In the final table I calculated the fair value of the company by varying the parameters between the minimum and maximum found in the previous calculations. Assuming a dividend of €1.53 in 2023, an average Dividend Growth of 8.15%, and an average Cost of Equity of 16.13%, the fair value of Generali turned out to be €19.18, meaning there is a possible upside of 11.60%.

DDM Model (Personal Excel Model)

{kind=link}

Please note that all calculations are in euros.

Despite the undervaluation the company could reach new lows

One of the biggest risks associated with Generali is its possible negative performance in the coming quarters. Indeed, although the management is very optimistic about the results achieved and the possible performance of the company in the coming months, I have a more conservative view.

In the current economic environment there is high inflation combined with low growth and historically financial companies have always performed poorly in this type of market. Indeed, people's income is lower during recessions, businesses invest less and people buy less, which leads to less credit volume. This does not only apply to banks, but also to other companies in the financial sector. So it is reasonable to expect new lows in the next 6-12 months, with a recovery once inflation subsides.

Conclusion

Although I was very picky about the company's risks, it is undeniable that Generali is a great company for the long term, because of its financial solidity, its reliable management, and its well above average dividend. In my opinion, Generali is a good “sleep well at night” choice for investors who avoid to trade in and out of stocks or make direction bets on the economy. However, it is not the best option for a 6-12 months' outperformance.

For further details see:

Generali: Stability And High Dividend, But Wait For A Better Entry Point