GEL - Genesis Energy: LT Outlook Remains Strong Despite Lowered Guidance Following Q2 Results

2023-09-11 09:00:00 ET

Summary

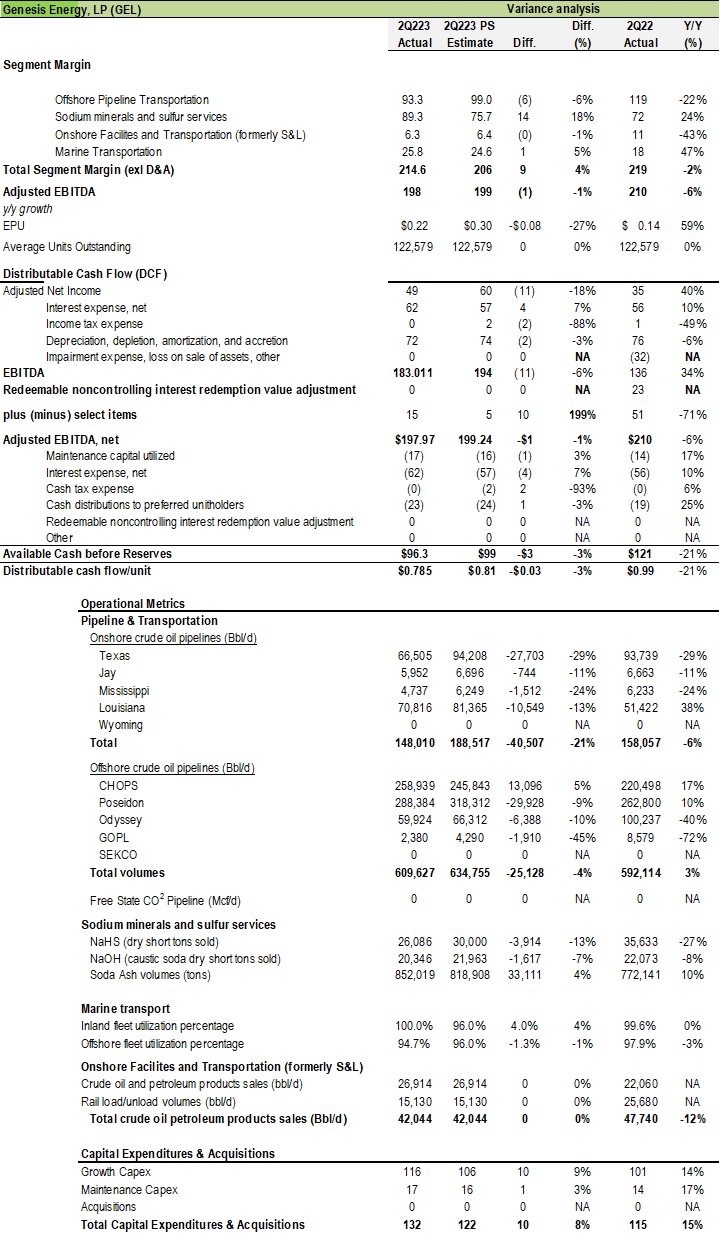

- Genesis Energy 2Q23 EBITDA beat: Adjusted EBITDA came in at $198M vs $188M/$199M consensus/our estimate. Segment margin beat at $215M vs $206M as Minerals beat while Offshore Pipeline was light.

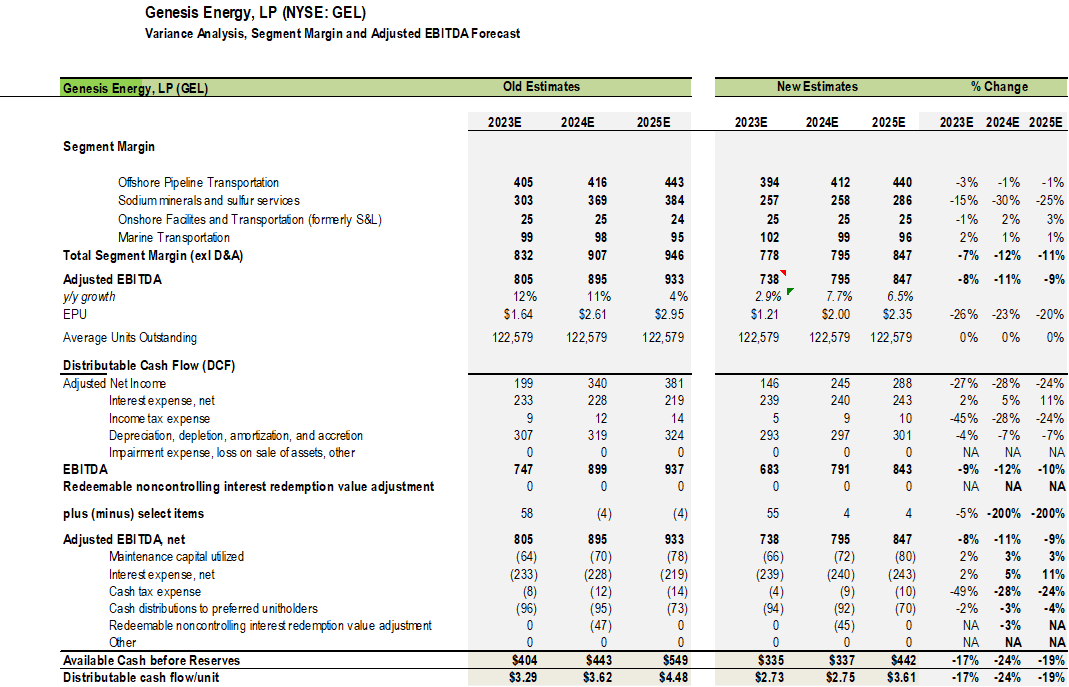

- Guidance Lowered: Adjusted EBITDA reduced to $725-$745M from $780-$810M EBITDA, mainly on weaker than expected Soda Ash pricing for the remainder of 2023.

- Longer Term above average return opportunity remains: Assuming 1.5 standard deviations below the five-year average still suggests ~70% upside by the end of 2024.

- Units repurchase announcement suggests GEL management believes GEL units are undervalued and likely to be able to generate sufficient cash flow to create additional demand for its own units.

Genesis Energy (GEL) 2Q adjusted EBITDA beat at $198M vs $188M consensus, in line with our $199M estimate. Segment margin was ahead of our estimate as Minerals delivered $89M vs $76M estimated while offshore was light at $93.3M vs $99.0M estimated. Onshore and Marine Transportation were essentially in line.

Source: Company filings, author estimates.

{kind=link}

Management lowered FY 2023 adjusted EBITDA guidance to $725-$745M from $780-$810M mainly on lower soda ash pricing. Management pre-emptively cut soda ash pricing to keep production running close to capacity. In addition, volumetric disruption at client refineries in the NaHS business is reducing the contribution by some ~$20M below its typical contribution.

In response to the lower 2023 guidance and management commentary on pricing, we have lowered our 2023-2025 adjusted EBITDA forecast by 8%/11%/9% to $738M/$795M/$847M from $805M/$895M/$933M. The Street is at $733M/$759M/$844M.

{kind=link}

The main change in my forecast was lower pricing on soda ash and lowering the contribution from NaHS. We slightly trimmed our outlook on offshore pipelines based on the result below forecast for 2Q.

Balance Sheet Forecast Update

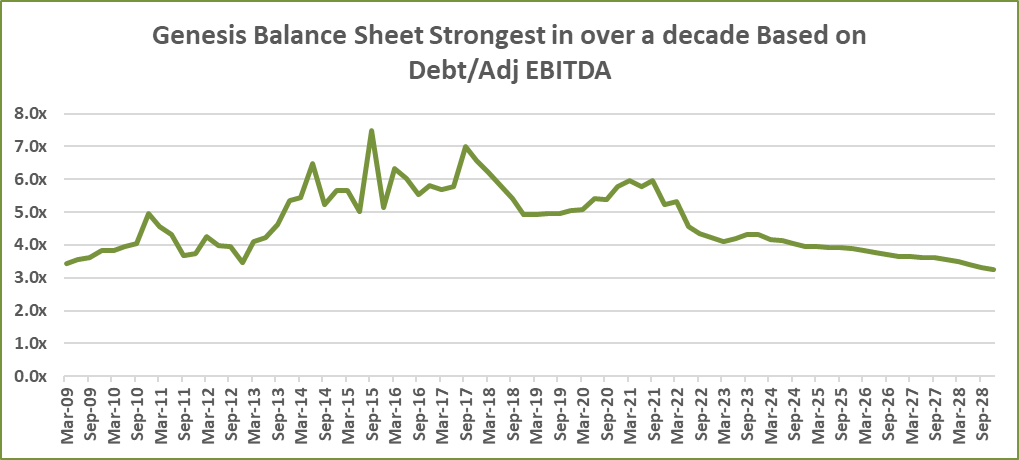

As a result of taking a more conservative growth trajectory, we are forecasting leverage to be relatively flat through the end of 2024 and then to drop by 0.1x in 2025, 0.2x in 2026 before reaching the low 3x's by the end of 2028. Embedded in the forecast is that offshore volumes rise by 80,000 bbl/d from SYNC by the 4Q 2025 from 4Q2024 compared to the 160,000 bbl/d capacity and by the end of 2026 the volume is up 123k from 4Q24. The volume outlook also does not assume any additional volumes despite discussions with producers that could result in an extra 150k-200k in volume by sometime in 2026.

We have also assumed softer soda ash margin going forward that is more consistent with levels seen in 2019 despite the much greater demand for soda ash demand emanating from the solar energy industry for solar panels.

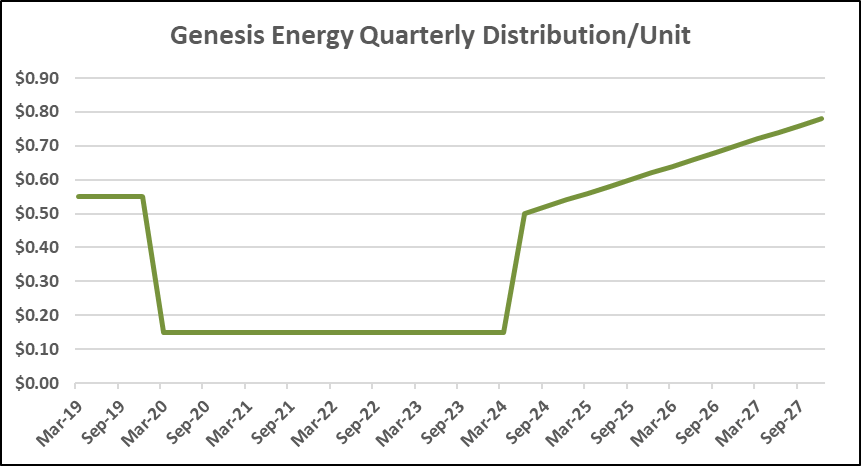

We are not modeling repurchase of the common units (despite GEL management announcing authorization to repurchase common units) into our forecast but continue to believe that management is likely to begin repurchasing the preferred units beginning 2H2024 at a rate of $50M/Q in 2024, $60M/Q in 2025, and $70M/Q after that until they are completely retired at the end of 2027. We also assume that GEL will raise the distributions on common units to $0.50/unit/Q beginning with 2Q24 declaration (payable in 3Q24) with a healthy double-digit growth rate after that with a CAGR of ~10% over the ensuing five years and maintaining distribution coverage above 1.5x.

Distribution/unit forecast (Source: Author estimates.) Balance Sheet history and forecast (Source: Company filings, author estimates.)

{kind=link}

{kind=link}

Valuation

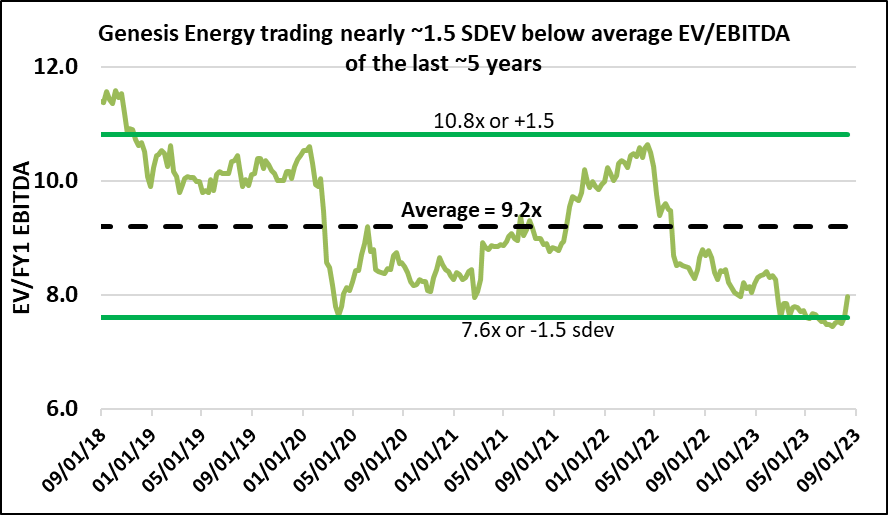

The valuation outlook changes modestly. My last update presented a valuation outlook based on nearly 3 turns below the five-year average of EV/EBITDA. Such an outlook was to emphasize that GEL units are trading at levels we believe to be significantly undervalued. Management apparently agrees with the announcement to authorize the repurchase of up to 10% of GEL's units.

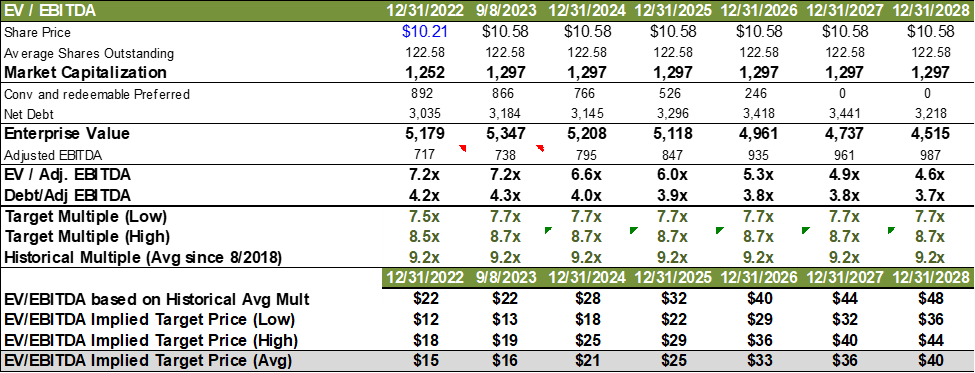

Based on a valuation of 1.5 standard deviations below the five-year historical average EV/EBITDA multiple, GEL units would trade at $13 by the end of 2023 (based on 2023 EBITDA), $18 by the end of 2024 (based on 2024E EBITDA) and $22/unit by the end of 2025 (based on 2025E EBITDA). All these target valuation figures are very conservative since most stocks trade based on forward estimates. At the five-year average historical multiple GEL units could trade at $32 by the end of 2025, nearly triple where they are trading today and if we assumed they started trading based on the forward multiple of the historical average the valuation would imply $40 or nearly 4x where they trade today.

Valuation forecast (Source: Author estimates.) EV/EBITDA history, average, std dev (Source: FactSet, author estimates.)

{kind=link}

{kind=link}

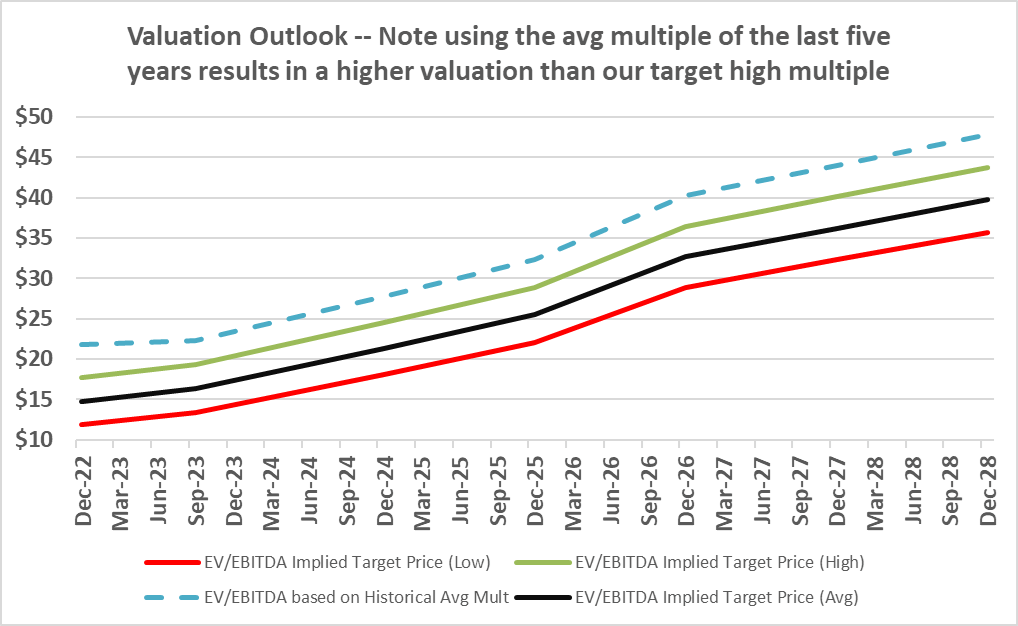

As shown below, using the low multiple of 1.5 standard deviations below the average of the last five years would still result in shares more than doubling based on forecast EBITDA for 2025 and tripling if the average multiple of the last five years were to be realized.

Valuation outlook assuming target range and historical EV/EBITDA average (Source: Author estimates.)

{kind=link}

Risks

Weather: With offshore pipelines that deliver services to offshore oil and gas production platforms, volumes are subject to disruption in the event of severe weather such as hurricanes. While the average hurricane season sees ~6 days of downtime and guidance has assumed a conservative 10 days of downtime, days of disruption is highly variable. Over the last decade, the number of days of disruption has varied from 0 to 30. We estimate that 30 days of disruption could negatively impact segment margin by ~$20-$30MM while 0 days of disruption could positively impact segment margin by ~$10MM relative to guidance and our estimate.

Economy: Guidance assumes a worldwide recession in 2023. There are a number of economic indicators signaling a coming recession such as prolonged yield curve inversion, CPI reaching over 5% (latest read was 3.2%), manufacturing PMI in contraction eight consecutive months, Conference Board LEI index <-4%. GDP growth and earnings on the S&P500 usually trough 24 months after interest rates peak (which would suggest such trough would hit 1H2025) but the timing is the subject of debate. Recent economic reports for 2023 have been stronger than expected. With the full impact of higher interest rate changes usually taking ~24 months to fully impact the economy, such impact should begin to fully hit over the next two years. The offset is that the labor market remains tight and federal government spending on infrastructure programs of nearly $1Trillion (Infrastructure Investment and Jobs Act, Inflation Reduction Act, Chips Act) is also beginning to flow to the states and blunting the actions of the Fed to some extent. That being said, management has indicated that the soda ash market has softened from what they were seeing at the beginning of the year, following the release of 1Q results and lowered guidance for 2023 with the release of 2Q results as the softening market deepened.

Inland Freight Market Prices: As we mentioned earlier, the inland marine shipping market is very tight with leader Kirby indicating that capacity utilization is running in the 90s% range. GEL management has seen the utilization of its vessels as at or close to 100% and prices not seen since 2014. There is very little new marine capacity being built and according to Kirby (KEX), they are expecting fewer vessel additions than retirements, putting upward pressure on marine transport pricing. For example, barge utilization rates were in the low 90s% range and spot market prices were up mid-single digits Q/Q and mid to high 20% range Y/Y. Should there be any kind of surge in capacity and/or weakened demand for transport services, there could be a downside in the margin contribution from GEL's marine transport business.

Pipeline in-service delay : We have been conservative in our assumptions regarding the volume ramp rate from the Argos and King Quay platforms. We have assumed a ~136,000 b/d increase between the end of 2022 and the end of 2024 compared to the ~220,000 b/d contracted. King Quay is already delivering 30,000 b/d above the 85,000 b/d expected. None-the-less, there is a risk that the total volumes could arrive slower than expected or end up disappointing. Similarly, 160,000 b/d is ultimately expected from the SYNC lateral and is expected to begin flowing late in 2024 or early 2025. While we only model a 129,000 b/d increase by the end of 2026, delays to the timing and/or volumes could result in lower EBITDA than what we forecast in our model.

Valuation: While applying a valuation multiple 1.5 standard deviations below the average of the last five years suggests that GEL units could more than triple from current levels over the next five years, nonetheless, depressed valuations could continue or even get worse than they are now given the somewhat negative sentiment toward the fossil fuel industry including infrastructure. Both higher expected distributions and/or unit buybacks could mitigate depressed valuations to a large extent, other factors and or market conditions could make implementing such an approach difficult or impossible.

Conclusion

While 2Q23 results were in line and the guidance was reduced from the 1Q report, the outlook remains very strong. Genesis struggled for a number of years but has turned the corner.

We continue to believe that an investment in Genesis Energy units remains compelling and has a high probability of delivering returns to investors that outperform the broader market averages, all while delivering attractive income.

For further details see:

Genesis Energy: LT Outlook Remains Strong Despite Lowered Guidance Following Q2 Results