SIRE - Genesis Energy: Thesis Getting Stronger

2023-04-04 04:48:52 ET

Summary

- Genesis Energy's results continue to exceed expectations with another "beat and raise" quarter.

- By 2025, Genesis Energy should have enough free cash flow to pay a $2/unit distribution and retire $300 million a year in debt or preferred equity.

- Soda Ash's performance has the potential to significantly exceed expectations as pricing remains high and some operating costs (namely natural gas) decrease.

- My belief that the units offer a total return triple from my $9 original recommendation has only gotten stronger in 2023.

Genesis Energy ( GEL ) is my top pick for 2023 based on a combination of upside potential and ability to weather a difficult macroeconomic situation for the next few years. For background, please first read that original article, as this article will serve as an update to it.

Since then, I believe the compelling thesis for these units to be back above $20+ in the next 18 months has only strengthened.

2023 EBITDA Guidance strengthened with further upside possible

In my last article, I noted that Genesis had given an early 2023 EBITDA guide in the "mid $700 million" range. This was updated to range of $780-$810 million and to exit 2023 with guidance for a leverage ratio at or below 4.0 times. This was yet another significant "beat and raise" quarter.

Regarding this guidance, CEO Grant Sims noted on the earnings call:

We believe this range takes into account the potential negative effects on our financial results if a significant worldwide recession were to unfold as we move through the year. To the extent such recession scenario does not come to fruition or either it is milder and modeled or in fact, the tailwinds from the green transition offset all or a part of the headwinds from a potential reduction in global industrial activity, there could, in fact, be biased to the upside of even the top end of our adjusted EBITDA guidance range.

The largest variable component of GEL's cash flows for 2023 are from Soda Ash pricing, and 85% of 2023 volumes (including from the additional capacity at Grainger) are already priced. The other smaller variable for this year comes from when BP's ( BP ) Mad Dog 2/Argos production starts.

Leverage

Genesis took advantage of favorable market conditions in mid-January to issue $500 million in 8.875% Senior Notes due 2030. It used this cash to tender the $341 million in 5.625% notes due 2024. By doing this, the next maturity is not due until late 2025, providing lots of runway for the business.

Genesis Energy Debt (Genesis Energy Investor Presentation)

While issuing 8.875% debt to retire 5.625% isn't ideal, there was no choice. To term it out further than the large 2027 and 2028 maturities, it was going to have to carry a higher interest rate.

Capital Expenditures in 2023 and 2024

Genesis Management gave an detailed update on two remaining large capital projects for 2023 and 2024.

- Granger Soda Ash Expansion

$275 million spent to date, $75-$100 million remaining (all 2023)

2023 incremental EBITDA from additional 6-700,000 tons (Author's estimate, already in guidance): $30 million

2024 incremental EBITDA from full 1.2 million tons (Author's estimate, assumes stable pricing): $70 million

- SYNC lateral and CHOPS expansion projects in the Gulf of Mexico $150 million spent in 2022, $400 million remaining between 2023 and 1H 2024.Incremental EBITDA starting in 2025: $100-125 million

2023 Cash Flow before growth CapEx should be in the $350 million range.

2024 Cash Flow before growth CapEx should be in the $450 million range.

This ~$800 million in cash flow (after interest, maintenance CapEx, and preferred distributions) generated in 2023+2024 should fully cover the remaining growth CapEx ($500 million) and common unit distributions ($75 million/year over 2 years = $150 million) with ease.

2025 Free Cash Flow

Using the low end of guidance of $780 million, adding $100 million for the Sync Lateral and CHOPS expansion, plus $60 million for the Granger expansion, plus another $50 million for full run rate of BP Argos/Mad Dog 2 gets us to around $1 billion of EBITDA in 2025.

Subtracting $240 million in interest expense, $96 million in preferred distributions, and $100 million in maintenance capital, leaves $550 million for common unitholders.

At the current common unit equity valuation of ~$1.4 billion, this is a 40% cash flow yield.

Note that I'm trying to be conservative and using the low end of all estimates (albeit with a reasonable price for Soda Ash baking into the estimates.) This also assumes no additional tie-backs or other infill projects are announced, which I find unlikely, as recent Gulf of Mexico drilling rights auctions have been robust.

Uses for Free Cash Flow - increased common distributions and preferred repurchases

Around the middle of 2024, roughly 5 quarters from now, GEL will wrap up the bulk of its growth CapEx spending and start generating a significant amount of free cash flow, nearly $150 million a quarter. What will they do with it?

First, I think they'll increase the distribution. This may happen in increments. I could see them moving from 15 cents quarterly to 25 cents toward the end of this year, and then to 40 or 50 cents sometime in 2024. At 50 cents/quarter or $2/year, which would be a 17% yield at today's price, the distribution will cost them $250 million/year. After paying a 17% yield, they'll have $300 million leftover to deleverage with.

Based on the commentary in the Q4 earnings press release, I believe the next thing GEL does is redeem their preferred shares.

For background, on September 29th, 2022, the holders of the ~$854 million Class A Convertible Preferred shares exercised a one-time rate reset election, which increased the annual distribution rate from 8.75% to 11.24%. With this reset, the preferred shares became redeemable by Genesis, at 110% of liquidation value prior to September 1, 2024, and at 105% afterwards.

{kind=link}

In the Q4 Earnings release, we also learned about an upsized and more flexible revolver:

On February 17, just last week, we successfully syndicated and closed on an extension and upsizing of our existing revolving credit facility with $850 million in commitments from both existing and new lenders. Notably, our new credit facility will have expanded general and permitted investment baskets, which will give us increased flexibility to potentially purchase existing private or public securities across our capital structure, that we bought at any given point perceived to be mispriced and a high value use of our capital.

Later, in the conference:

CEO Grant Sims:

As we then start to harvest the incremental cash flow from these growth projects, along with the continued strong performance of our base businesses, we believe we're in very good shape to begin simplifying our capital structure and perhaps even start looking at ways to return capital to our bond and common equity holders in one form or another, all while maintaining a leverage ratio at or below 4x.

A follow up question:

Torrey Schultz:

Then with the expanded investment baskets and the revolver, how are you thinking about that flexibility? You talked about simplifying the capital structure, just what's the plan with the preferreds? Or where in the capital structure do you consider purchasing securities as debt leverage moves sub-4x?

CEO Grant Sims:

We will look at simplifying the capital structure and taking out expensive pieces of capital and made all the time managing the debt as calculated by our banks to at or below 4x.

I believe that Genesis will start redeeming these after September 2024 when the premium drops to 105%. How fast it will redeem them will likely depend on several factors, including prevailing interest rates/credit markets, as well Soda Ash pricing.

How Valuable is the Soda Ash business, anyways?

Since 2021, pureplay comp Sisecam Resources ( SIRE ) has doubled, and would likely be higher if it were not for the GP taking out the units it doesn't already own with a lowball offer at $25.

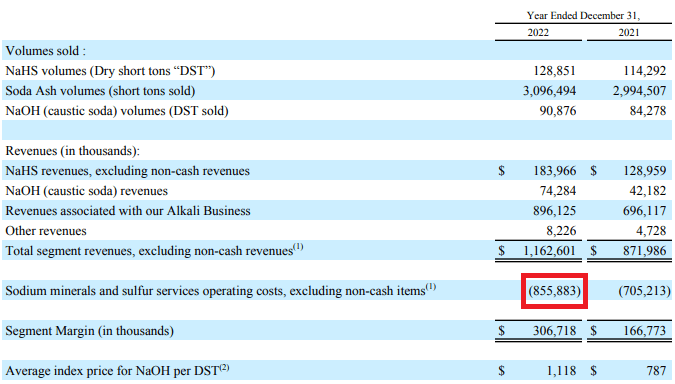

At Genesis, this segment's revenue doubled year over year while producing about the same volume. 2023 and especially 2024 will benefit from the additional volumes at Granger.

2022 Genesis Energy Sodium and Sulfur Segment Results (Genesis 2022 10-K)

{kind=link}

But I don't believe this is the full story on this business - not only did they double segment margin last year, but they did it while facing substantially higher energy costs.

{kind=link}

Unfortunately, Genesis provides very little color in their financials as to sensitivities to natural gas prices (and really, just about anything) related to this business.

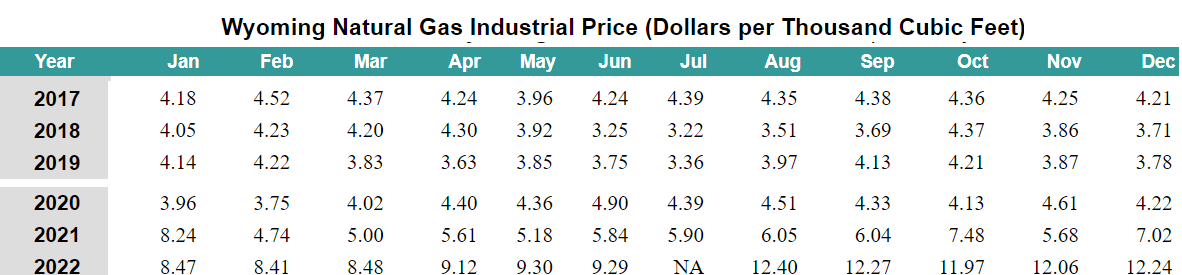

We get some information from Sisecam's 10-Q filings :

{kind=link}

For Q1 (aka, winter) West Coast natural gas and electric prices remained stubbornly high on a combination of colder weather and pipeline disruptions, but this is rapidly fixing itself with Spring coming and natural gas supply remaining extremely strong. The Opal Hub Spot Price has been in the $3-6 range for most of March, significantly down from the past year. I believe it will settle into the $3 range once warmer west coast weather arrives.

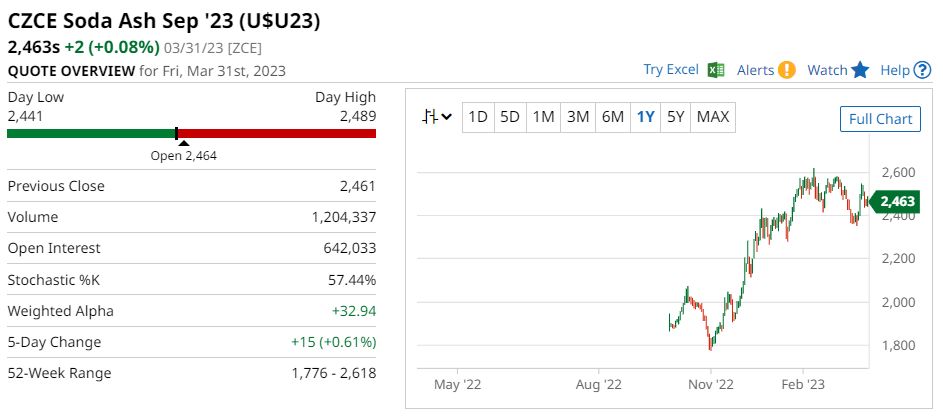

At the same time, Chinese Soda Ash prices remain well supported, with the actively traded September contract near highs.

{kind=link}

Genesis is already forecasting a strong year for the Soda Ash business with significantly global weakness in the current estimate. At least as of now, this weakness has not showed up.

I believe the performance of this business could vastly exceed expectations in 2023, removing significant risk to the bridge to free cash flow in late 2024/early 2025.

Conclusion

I think it's pretty crazy that GEL is still available at the same unit price it was way back in July 2021, when the major growth projects in the Gulf were several years from coming online, refinery utilization was still down, and soda ash prices were far lower.

The business has positively inflected since, but the unit price has gone nowhere. Maybe it won't until the distribution gets increased, like what happened with the former Altus Midstream, now Kinetik ( KNTK ).

For those unfamiliar with the Altus Midstream story, the company owns operated assets in Alpine High, a Texas oil and gas field that was a focus for Apache ( APA ). It also owned large, non-operated stakes in several Permian pipelines operated by Kinder Morgan ( KMI ), Enterprise ( EPD ) and others. In early 2020, Apache decided to stop development in Alpine High after finding it produced more natural gas than oil. Altus likely had a bunch of stranded assets along with significant debt, expensive preferred equity, and a few hundred million in CapEx spend left. Predictably, its unit price plunged.

But even valuing its operated assets at zero, its minority stakes in the Permian projects were still valuable. These JV projects were coming online and cash flow was starting to come in. In September 2020, a contributor on SA called it out as a One Year Out Cash-Flow machine . Many (including myself) liked the story and saw value in the units after they fell 90%+. But I thought the units wouldn't move much and Altus would pay back debt for the foreseeable future. I held off purchasing, which was a disaster of a mistake.

Just two months later, Altus surprised everyone (both with timing and magnitude) and declared a $1.50 quarterly dividend , giving it a 60% yield. Units tripled overnight, and then doubled again in 9 months.

Remember above when I said Genesis was 18 months away from having a 40% free cash flow yield?

For further details see:

Genesis Energy: Thesis Getting Stronger