GMAB - Genmab: Epkinly's Approval Not Big Enough Needle-Mover (Neutral)

2023-06-29 10:05:50 ET

Summary

- Genmab's stock has seen negative price action despite the FDA approval of its drug, Epcoritamab, for relapsed/refractory diffuse large B-cell lymphoma (DLBCL).

- The market has already priced in the approval, and the drug faces a competitive landscape with rivals Roche and Regeneron expected to file for their own bispecifics in r/r DLBCL in 2023.

- Genmab's mid-stage assets offer limited short-term catalysts to drive investor interest.

- The growth in its beachhead product, Darzalex, is already priced into the valuation, and its mid-stage assets may not have a significant enough impact to move the needle.

- We maintain a neutral rating due to these factors, despite its unique pipeline and base technology and expected success in Darzalex.

Update: Epkinly's approval

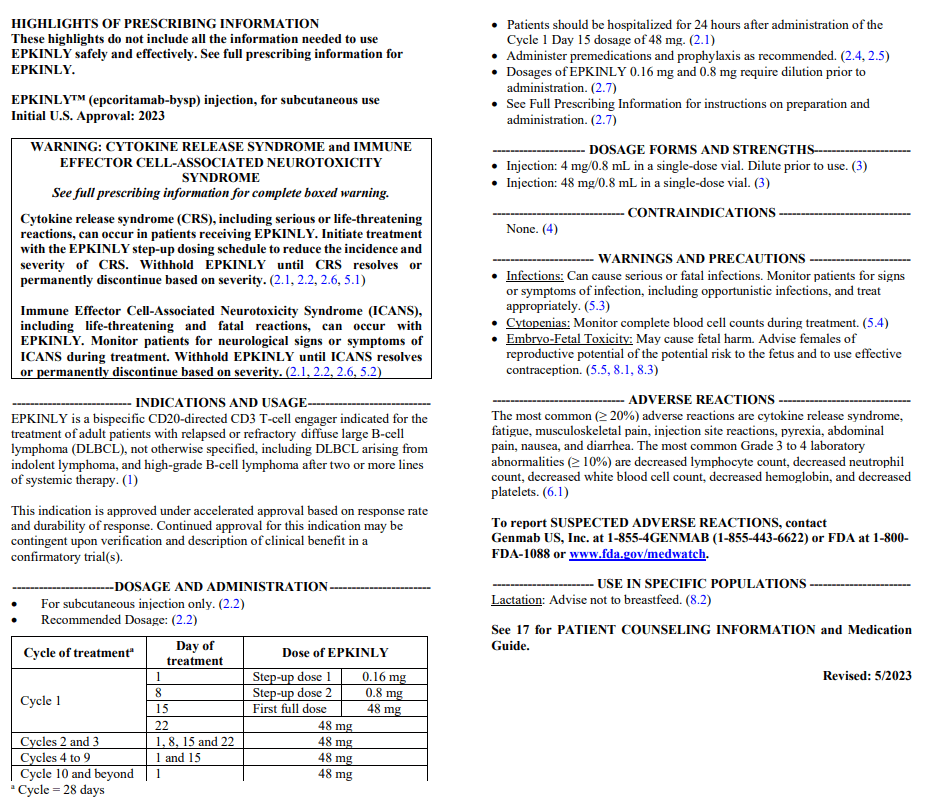

Since our previous article , Genmab's price action has been fairly negative even with Epkinly's approval, as we expected previously. We were fairly optimistic about Epkinly's approval, and we are not surprised by the recent FDA decision and the label that it has received. We remind readers that Epkinly is a CD20xCD3 bispecific that is partnered with AbbVie (ABBV) and has received approval in the relapsed/refractory (r/r) diffuse large B-cell lymphoma (DLBCL) on May 19, 2023. Moving forward, the company is planning to file in relapsed/refractory indolent NHL indication around 2023, and a phase 3 study in 1L aggressive NHL is expected by post- 2025 timeframe. We see Epcoritamab as Genmab's most prominent pipeline drug that has driven Genmab's return during the last 3 years, where at this point, we believe the market has already fully priced in its approval based on the recent price action post-approval. We see the DLBCL market to be highly competitive with multiple novel modalities that showed strong results, albeit, Epcoritamab is one of the front-runners, and like similar oncology indications, a winner-takes-all type of dynamic is expected. So far, the street consensus seems to be above $ 1.74bn (peak sales), which could be highly achievable considering the data they showed and the attractive pricing dynamics of oncology indications. The label published by the FDA seems clean and expected based on its pivotal trials.

Epcoritamab FDA monograph (FDA)

{kind=link}

Furthermore, the recent addition to the NCCN guideline for B-cell lymphomas (Version 4. 2023) should be a net positive for the uptake during 2023-2024 (as prescribers would be more comfortable prescribing it with the backing of guidelines and payers will be reimbursed it with less friction). Still, Epcortitamab's positive ramp seems to be fully baked into the current valuation, and further unforeseen competitive risk remains. For example, although epcoritamab was the first CD20xCD3 bispecific to make a loud entry into the US oncology market, Roche's glofitamab and Regeneron's odronextamab are expected to file a BLA for their own bispecifics in r/r DLBCL in 2023, further complicating the competitive dynamic.

Genmab Epcoritamab (Company source)

Limited short-term catalyst from the company's mid-stage asset

However, the biggest concern for the stock moving forward would be the fact that there are limited early-stage assets to drive specialist investors' interest, and it is difficult to predict its near-term success due to limited data. One key asset that can plug the gap from Darzalex royalty erosion would be GEN3014, which can be considered as a Darzalex 2.0, which Janssen can opt-in if the data from phase 2a is positive (currently being studied against Darzalex and data expected by 2024). Furthermore, we note that there are bispecifics such as GEN1046 and GEN1042 that are being studied with BioNTech (BNTX) and will release data in 2H 2023; the possibility of success of it is unclear due to limited data and high valuation of Genmab at this stage. The recent collaboration with Argenx is refreshing but hard to believe there will be a short-term impact on the stock in 2023.

Risks

-

Competitive Landscape Risk : While Epcoritamab has established a strong position as the first CD20xCD3 bispecific to make a significant entry into the US oncology market, impending competition from Roche's glofitamab and Regeneron's odronextamab, with expected BLA filings for their own bispecifics in r/r DLBCL in 2023, adds a layer of complexity to the competitive landscape. This potentially erodes Genmab's market share and, thus, revenues if these rivals can offer better results or pricing.

-

Dependence on Epcoritamab : Given that the market has already fully priced in Epcoritamab's approval and expected performance, any negative surprises, such as slower-than-expected uptake or unforeseen safety concerns, could significantly impact the stock. Genmab is heavily reliant on this drug, and any unexpected issues could be detrimental to the company's future growth trajectory.

-

Uncertainty in Mid-stage Assets : The lack of short-term catalysts from the company's mid-stage assets could be a risk for Genmab's stock. The company's potential 'gap-filler' from Darzalex royalty erosion, GEN3014, is still in early development, and its success is far from certain. In addition, bispecifics like GEN1046 and GEN1042, currently under investigation with BioNTech, offer unclear prospects due to limited available data. If these assets fail to meet expectations, Genmab's valuation could face significant pressure.

-

Limited Impact of Rybrevant Trial : The upcoming trial results of Rybrevant vs. Tagrisso, expected in 2023, may not have a significant impact on Genmab's bottom line, given that Rybrevant's royalties only constitute a minor portion of the company's revenue. If investors were expecting a significant impact from this trial and it does not materialize, it could lead to disappointment and potential downward pressure on the stock price.

Conclusion

We maintain a neutral rating due to limited short-term catalyst, although we are a big fan of the company's unique pipeline and base technology. Genmab is a high-quality European pharma with 7 marketed drugs from its unique proprietary antibody platform, and the beachhead product Darzalex is expected to become a $10Bn+ drug in myeloma (looking at the current trajectory). However, the growth in Darzalex is fully priced into the valuation, as we have seen with recent post-earnings price action. Now, the key value driver revolves around the company's mid-stage asset, which may not be a big enough impact to move the needle at the current valuation considering the early stage of the development. Another interesting trial, Rybrevant vs. Tagrisso, is currently being studied as a first-line indication for lung cancer and is expected to read out in 2023, but Rybrevant's royalty only represents a small portion of Gemanb's bottom line; as such, it is unclear what the investor's reaction there would be.

For further details see:

Genmab: Epkinly's Approval Not Big Enough Needle-Mover (Neutral)