RHHBY - Genmab: High-Quality Biotech Darling But Lacks Meaningful Catalysts In The Near Term

Summary

- Genmab (GMAB) is a Danish commercial biopharma company with a leading technology and track record in innovative antibody-based therapeutics.

- Darzalex royalty revenue is the key driver of the stock price and the bedrock of Genmab's strong performance during 2021-2022.

- We expect a slowing down in Darzalex royalty revenue during 2023 and the momentum in stock price to slow down. Also, the lack of short-term catalysts doesn't bode well for the stock.

- We initiate Genmab with a neutral rating.

Background

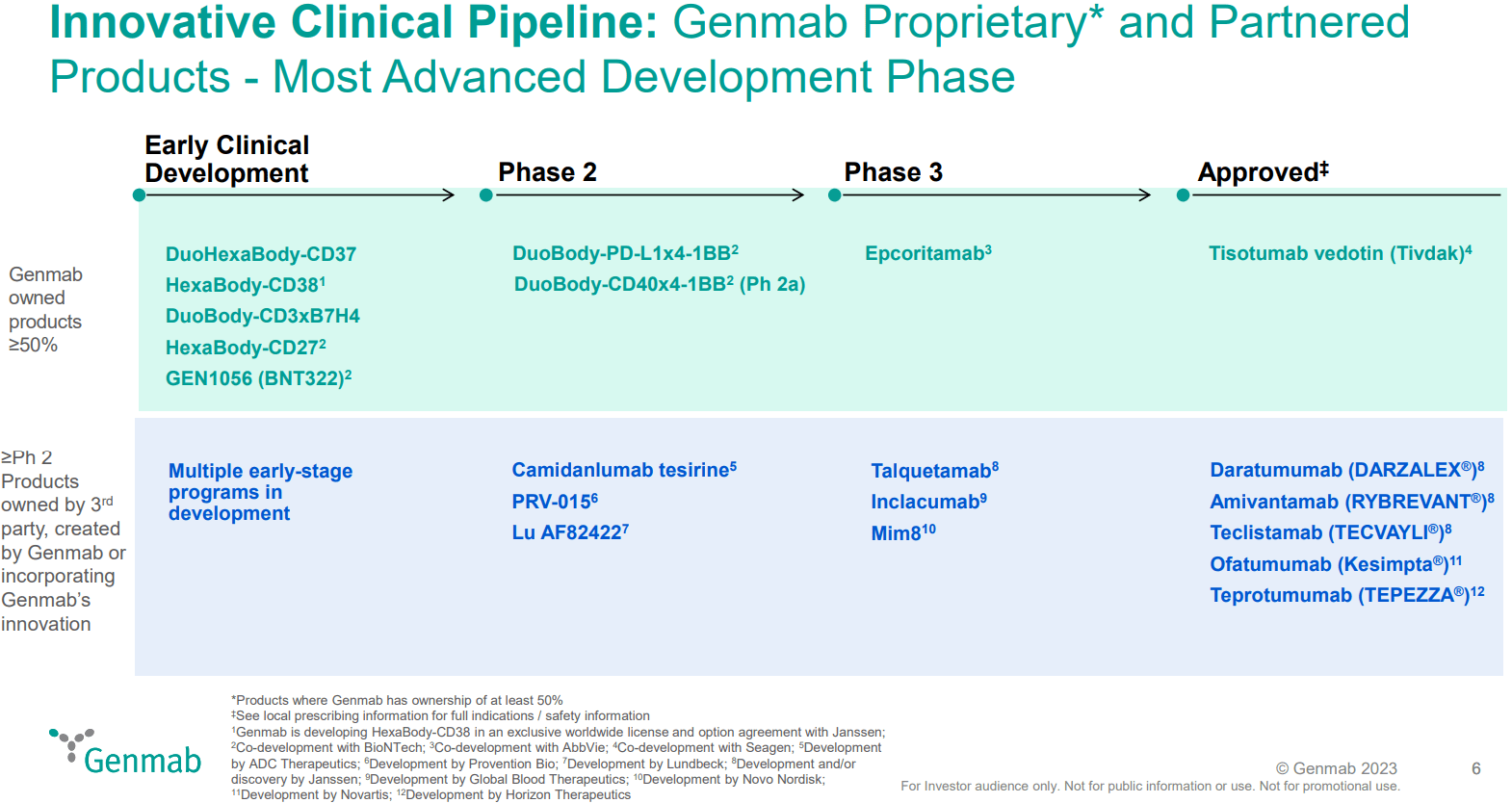

Genmab ( GMAB ) is a Danish commercial biopharma company with a leading technology and track record in innovative antibody-based therapeutics. Genmab's next-generation antibody pipeline focuses on utilizing an immune system to treat various oncology indications. Currently, the company has 6 approved therapeutics, a) Darzalex, Darzalex Faspro, and Rybrevant (marketed by J&J), b) Tepezza (marketed by Horizon), c) Kesimpta (marketed by Novartis), and d) Tivdak (marketed by Seagen). We like Genmab's strategy focusing on R&D and drug development and out-licensing the product to big pharma that can leverage their existing commercial infrastructure, which eliminates the potential commercial risk for Genmab. The company's long-term focus is on expanding its cutting-edge technology platform into numerous additional oncology indications.

Genmab Pipeline Overview (JPM presentation)

{kind=link}

We believe the biggest driver of Genmab's valuation is in the Darzalex franchise, which has consistently generated a +20% CAGR growth in royalty income, which drove the steady EPS and revenue growth for Genmab.

Genmab has several interesting pipelines in next-generation HexaBody and DuoBody & DuoHexaBody bispecific under development. However, we do not expect any meaningful catalyst from those within a 1-2 year timeframe.

Our reasoning for a neutral rating

On Jan 24, JNJ reported around $2.08B in global Q4 sales of Darzalex, which represents a +2% quarter-over-quarter increase and fell slightly below consensus and the company's guidance (2022 guidance: $8.0B to $8.2B in Darzalex sales and DKK 10.0B to 10.3B in royalties). We believe this may indicate the momentum in Darzalex to slow down, at least temporarily. Furthermore, we expect a negative impact from the declining dollar can impact 2023's sales, albeit it is hard to speculate on the currency move.

Besides Darzalex, we believe epcoritamab (CD3xCD20 bispecific) is the key driver of sentiment in the short term. We like epcoritamab's general clinical profile, best-in-class efficacy, and superior convenience due to subcutaneous administration vs. Roche's glofitamab targeting LBCL and mosunetuzumab targeting FL and Regeneron's odronextamab. However, we are neutral on the market opportunity of epcoritamab in the earlier line of DLBCL due to high competition from existing R-CHOP and Polivy from Roche, which means epcoritamab's core positioning would revolve around third-line DLBCL & FL, which we estimate to be <$500-1Bn market . Of note, last year, FDA accepted a priority review of Epcoritamab, and we believe the chance of approval is high based on the robust clinical data and clear convenience advantage shown to date.

Risks

There are multiple ongoing clinical trials; therefore, any clinical trial failure or regulatory headwinds can impact the stock price. Furthermore, there could be some currency and drug pricing-related headwinds. Also, Genmab is going through litigation with J&J, which can be a potential overhang.

Conclusion

We initiate with a neutral rating due to a) sign of slowing down of Darzalex sales and headwind from declining USD, b) the absence of meaningful short-term catalysts other than Darzalex sales that can have a meaningful impact on the stock price, and c) rich valuation of USD ~26Bn. Although we find epcoritamab to be a potentially best-in-class agent for third-line DLBCL, with the FDA accepting priority review in November 2022, we believe the approval of epcoritamab is fully baked into the current valuation.

For further details see:

Genmab: High-Quality Biotech Darling, But Lacks Meaningful Catalysts In The Near Term