DAVA - Genpact: AI And Cloud Likely To Drive Transformational Demand

2024-01-03 22:21:35 ET

Summary

- Genpact’s revenue has grown at an average rate of 8%, driven by strong demand for digital consulting services, as the corporate environment increasingly embraces technology to improve its financial performance.

- Genpact provides end-to-end solutions across a range of transformational segments, including AI and Cloud computing, while having a tailored approach (and expertise within) specific industries.

- Genpact’s margins have fluctuated within a small window, but the restrictions of the industry imply material improvement is unlikely, unless significant innovation around delivery can be achieved.

- Genpact performs well compared to its peers, but we expect more. Its revenue growth in particular is disappointing, suggesting a weakness in its go-to-market strategy.

- Genpact’s valuation has significantly declined in 2023, with a NTM FCF yield of ~8%. We consider this a good entry point.

Investment thesis

Our current investment thesis is that from an internal perspective, we believe Genpact ( G ) is a good business and positioned perfectly to enjoy healthy growth in the coming years. It has deep expertise that have developed over a number of decades, a global footprint with a large workforce, and a suite of services across the transformational spectrum.

Further, the industry appears to have the legs to continue its strong growth, as AI, Cloud, and Data Analytics drive corporate improvement. Although Genpact has shown some weakness relative to its peers, we believe its core competencies are sufficient to maintain its current trajectory.

Underpinning the quality of the business and acting to alleviate any commercial concerns is its valuation, with a noticeable discount and attractive FCF yield.

Company description

Genpact is a global professional services firm headquartered in New York City, USA, with a strong presence in India. Founded in 1997 as a subsidiary of General Electric, Genpact has evolved into a standalone company providing digital transformation and business process management services to clients across various industries, including banking, financial services, insurance, healthcare, manufacturing, and more.

With operations in multiple countries, Genpact is a leader in applying technology, analytics, and process optimization to improve the way businesses operate.

Share price

Genpact's share price performance has been respectable, returning over 100% to shareholders. Similar to the wider market, it has struggled since the start of 2022, although has not seen clear evidence of an upward trajectory toward its 2022 level. Its upward trajectory is a reflection of the company's healthy growth.

Financial analysis

{kind=link}

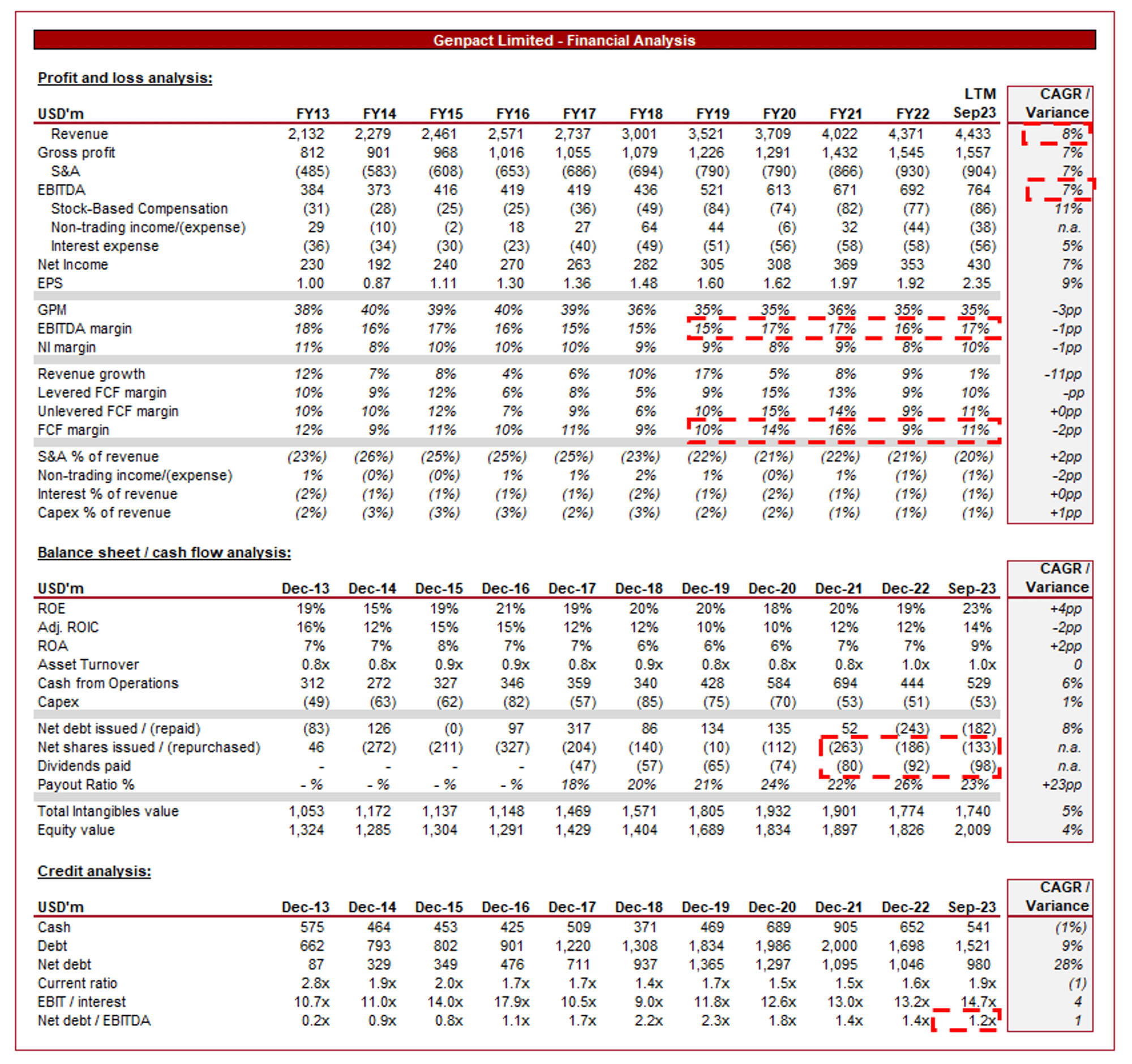

Presented above are Genpact's financial results.

Revenue & Commercial Factors

Genpact's revenue has grown at a CAGR of 8% during the last decade, with a comparable rate for EBITDA. This growth has been impressively consistent, with all but 3 fiscal periods between 6-12%.

Business Model

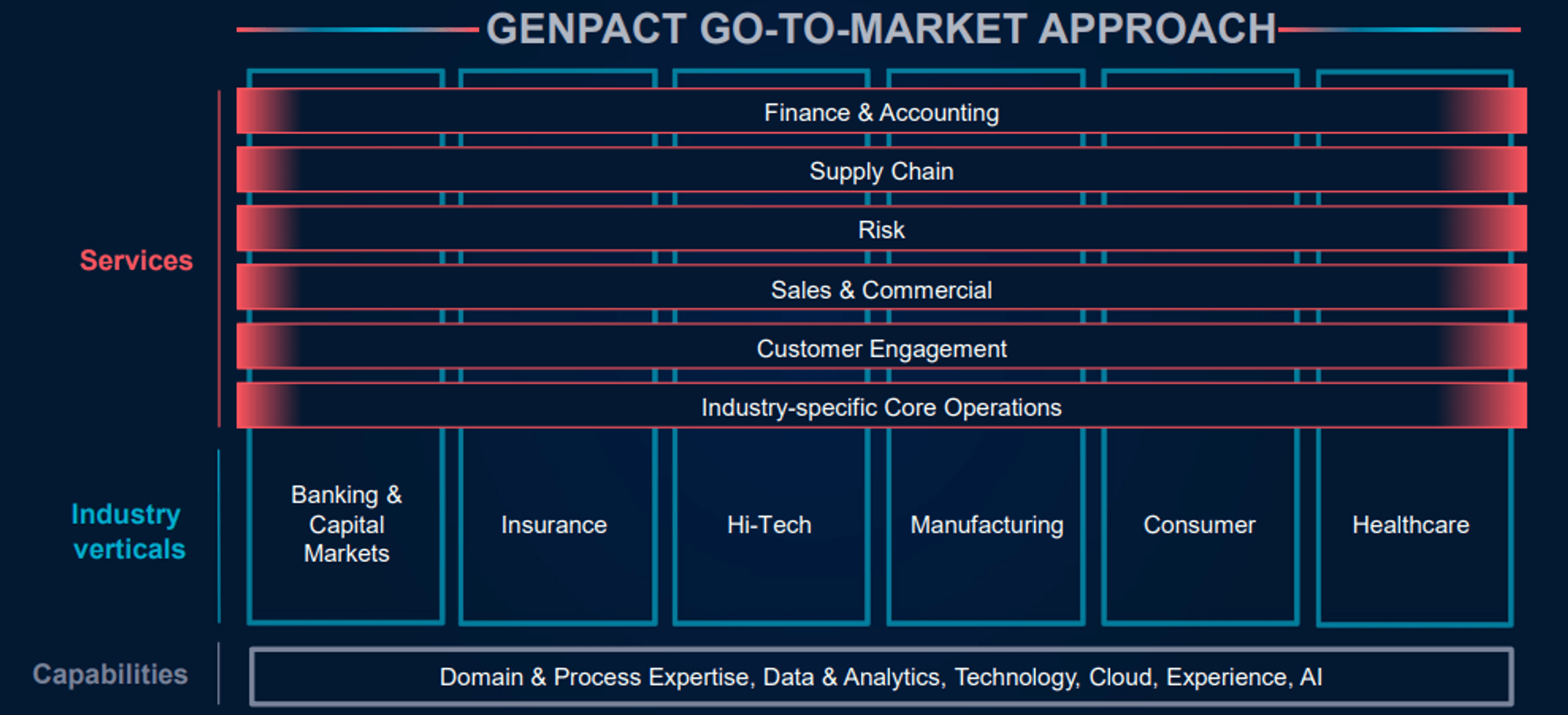

Genpact assists businesses in embracing digital technologies and processes to optimize operations, reduce costs, and gain a competitive advantage. This includes services related to automation, artificial intelligence ((AI)), data analytics, and cloud computing. The company's objective is to develop a relationship with its clients, supporting them throughout a technology-enabled journey over numerous years.

Genpact offers end-to-end business process management solutions that encompass various industries, including finance, healthcare, insurance, supply chain, and more. Further, Genpact leverages data analytics and predictive modeling to provide clients with actionable insights for better decision-making and improved performance. These solutions aim to streamline workflows, increase productivity, and ensure compliance. The industry focus has been increasingly important in the last decade, as corporate complexity has contributed to businesses seeking specialized firms as they perceive the quality to be higher.

{kind=link}

Genpact operates a global network of delivery centers, providing services to clients around the world. Similar to the above, developments in the way companies operate, namely internationally, means a global network is required to service larger businesses successfully.

The consulting industry has aggressively utilized global "delivery centres", with Genpact being no different. These are teams of employees in low-cost countries such as India, providing the "grunt work" while the front-line team focuses on the actual work required.

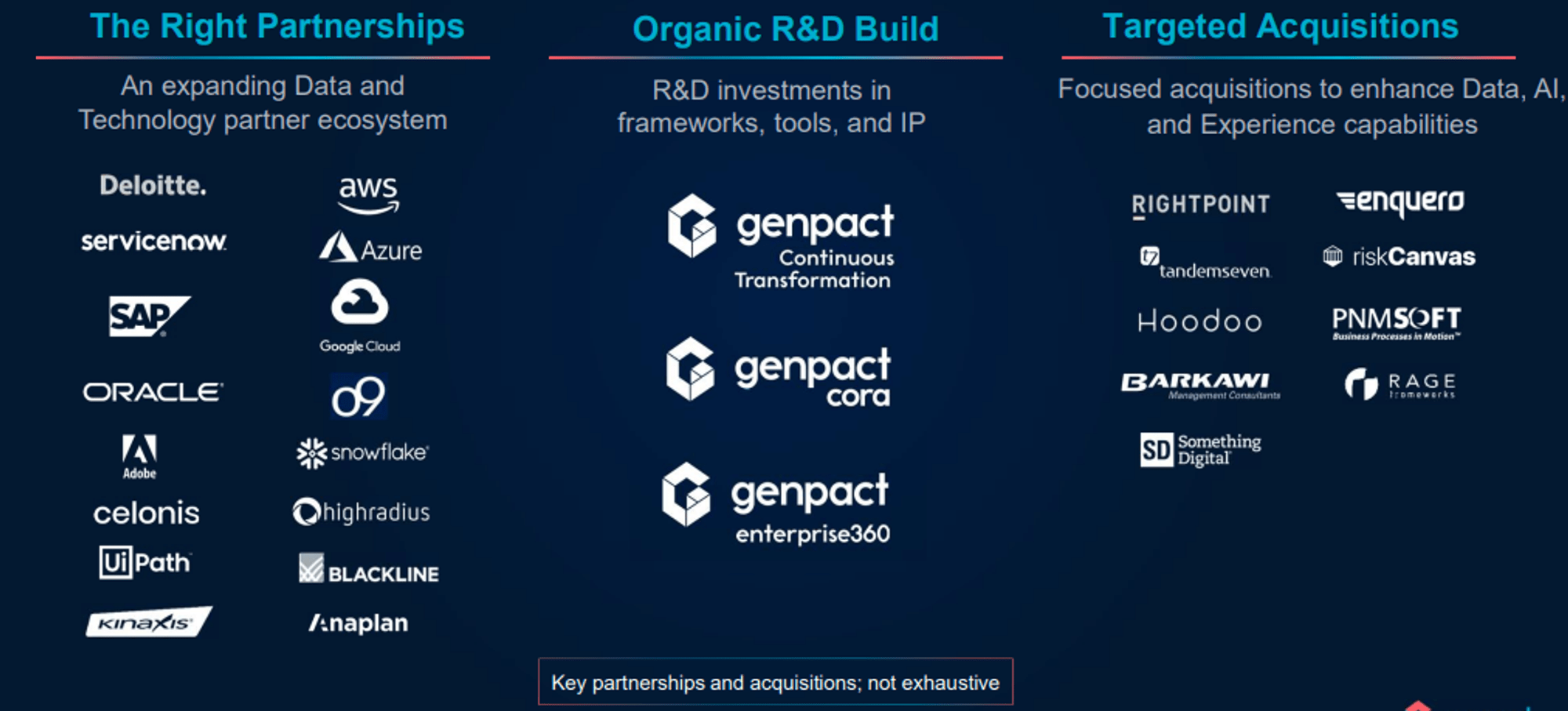

Genpact's competitive advantage centers on two primary factors. Firstly, from an internal perspective, the company has deep expertise within the industry, developed on several decades of high-quality services and market-leading recruitment and training. Externally, the business has developed strong relationships within the industry, contributing to brand development, a positive reputation, and a strong track record. From a commercial perspective, this has been enhanced by Partnerships with leading firms, as well as acquisitions to tweak the positioning of its overall portfolio.

{kind=link}

Digital Transformation Consulting

The Global Digital Transformation segment has experienced strong growth in the last decade, as numerous technological developments, such as Cloud computing, have contributed to an upward swing in the value proposition. In the case of Cloud computing, costs declined sufficiently to be utilized at scale.

Genpact competes with several global players in the professional services and BPO industry, including Accenture ( ACN ), Cognizant ( CTSH ), Infosys ( INFY ), and IBM Global Business Services ( IBM ).

MarketReports estimate that the industry will grow at a CAGR of 13% into the end of the decade, driven by continued technological development and increased R&D spending. We consider the following specific trends to be the key factors within this:

- Digital Transformation Demand - Global corporates have "had a taste" of what technological integration can provide, with significant value achieved across industries that only several years ago saw few use cases. This trend will remain strong, as we see a continued modernization of operations, as well as further development in line with new technology.

- Cost Efficiency - Inflationary pressures globally, alongside increased competition through various industry revolutions, are pressuring businesses to achieve maximal cost efficiencies as a means of being as competitive as possible. Genpact's BPM solutions and automation technologies are positioned perfectly to help clients reduce operational costs.

- Data Generation - We are currently living in a data generation, as businesses have discovered a number of ways to convert consumer information into lucrative returns. Genpact's data analytics capabilities enable clients to begin the journey of harnessing the power of data for informed decision-making, predictive analytics, and improved customer experiences.

- AI and Cloud - Cloud has been the biggest trend in the last decade, contributing to a significant reduction in costs and the ability to scale data capabilities. We consider this a trend that has legs to continue, owing to the scope for further penetration. AI has the potential to be a game changer, particularly with Gen AI. With many businesses operating with significant tech capabilities, AI is the "brain" that can make this replicate the agility and learning that comes with human capital at the helm. Genpact's end-to-end solution, especially this early into its mainstream development, will be highly attractive in the market.

- Vertical Expansion - Exploring opportunities in emerging industries or expanding services within existing verticals can drive growth. Strategic acquisitions have the potential to allow this in a flexible and rapid way. The consulting industry has broadly consolidated during this last decade, as larger firms acquire expertise from boutiques. We believe Genpact has missed a trick here by not accelerating activity, even on a smaller scale (acquiring teams).

The level of competition within the industry will restrict growth running away, however, as has been the case thus far, the market is large enough for all to win. We see HSD/LDD growth being possible in the years to come given the factors discussed above.

Margins

{kind=link}

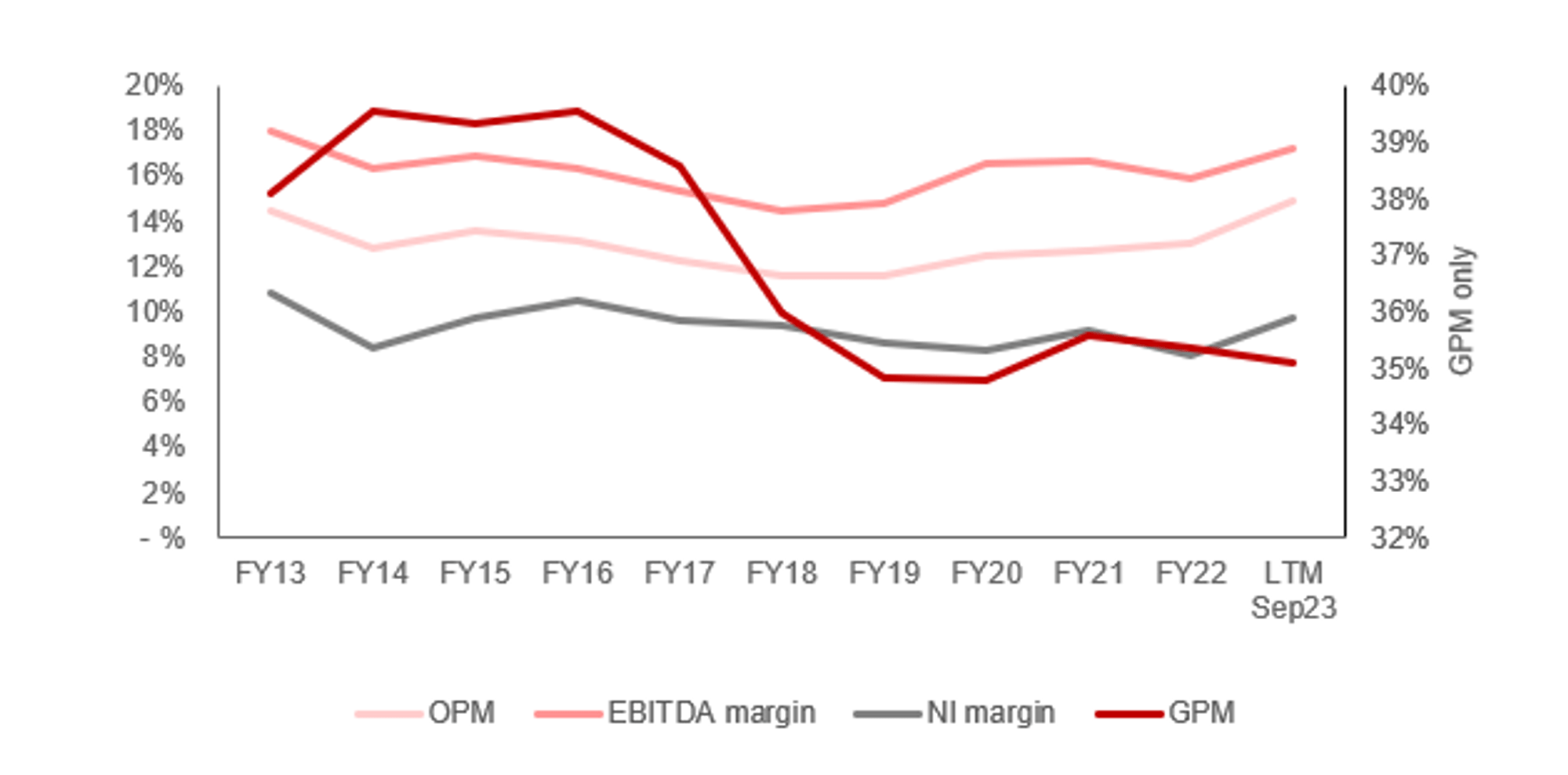

Genpact's margins have traded sideways during the last decade, with a decline in GPM offset by a decline in S&A spending. These margins are reflective of a professional services business, as the nature of human capital businesses means rate increases must be proportionately passed on to staff. The risk otherwise is higher than anticipated turnover, which can be challenging in highly skilled roles such as technology consulting. We consider this a key obstacle to improvement over time unless new delivery methods can be discovered (less labor-intensive).

Quarterly results

Genpact's recent performance has slowed relative to the post-pandemic period, with its top-line growth in the last 4 quarters being +9.4%, +2.8%, +2.0%, and +1.5%, clearly illustrating a step-down. Although disappointing, margins have remained robust, with EBITDA-M only falling below 15.8% for a single quarter. This suggests Genpact is still able to recover well on its existing projects, although is likely struggling with new work generation. This is likely an impact of macro headwinds, with softening demand and inflationary cost pressures contributing to reduced spending at the corporate level.

The key takeaways from the company's most recent quarter are:

- Revenue growth from Data-Tech-AI services was up 2% (45% of revenue) while revenue growth from Digital Operations services was up 1% (55% of revenue), implying the slowdown is being felt universally by the business, with minimal diversification benefits.

- Management believes demand for cost reduction and digital transformation services at a corporate level remains strong, with an increasing number of clients seeking value through AI-augmented services.

- Bookings remain strong despite the weakness in revenue, with Management expecting the full-year bookings growth to land at 25-30%, driven in particular by large deals. The pipeline is inherently good, owing to the hype around AI and the potential to provide end-to-end solutions at an early stage in the AI journey.

Overall, this has been a disappointing quarter, again. There are signs of positivity, however, we expect the business to continue to underwhelm in the near term.

Balance sheet & Cash Flows

Genpact's balance sheet is broadly clean. The company has utilized limited debt, while its profitability translates well to FCF, allowing the company to fund M&A, reinvestment in growth, and shareholder distributions through cash. The balance between these three has shifted in recent years, with M&A activity and reinvestment slowing, while debt servicing and distributions have a heavier weighting.

Management's preference is to distribute via buybacks, although began balancing this with dividends in 2017. Distributions have been underwhelming, with inconsistent growth. This is potentially a reason for investor sentiment changing, as Genpact has seemingly switched from investing heavily in growth and being conservative with distributions to delivering for no immediate reason and reducing its top-line growth potential. We struggle to understand the overarching capital allocation strategy here.

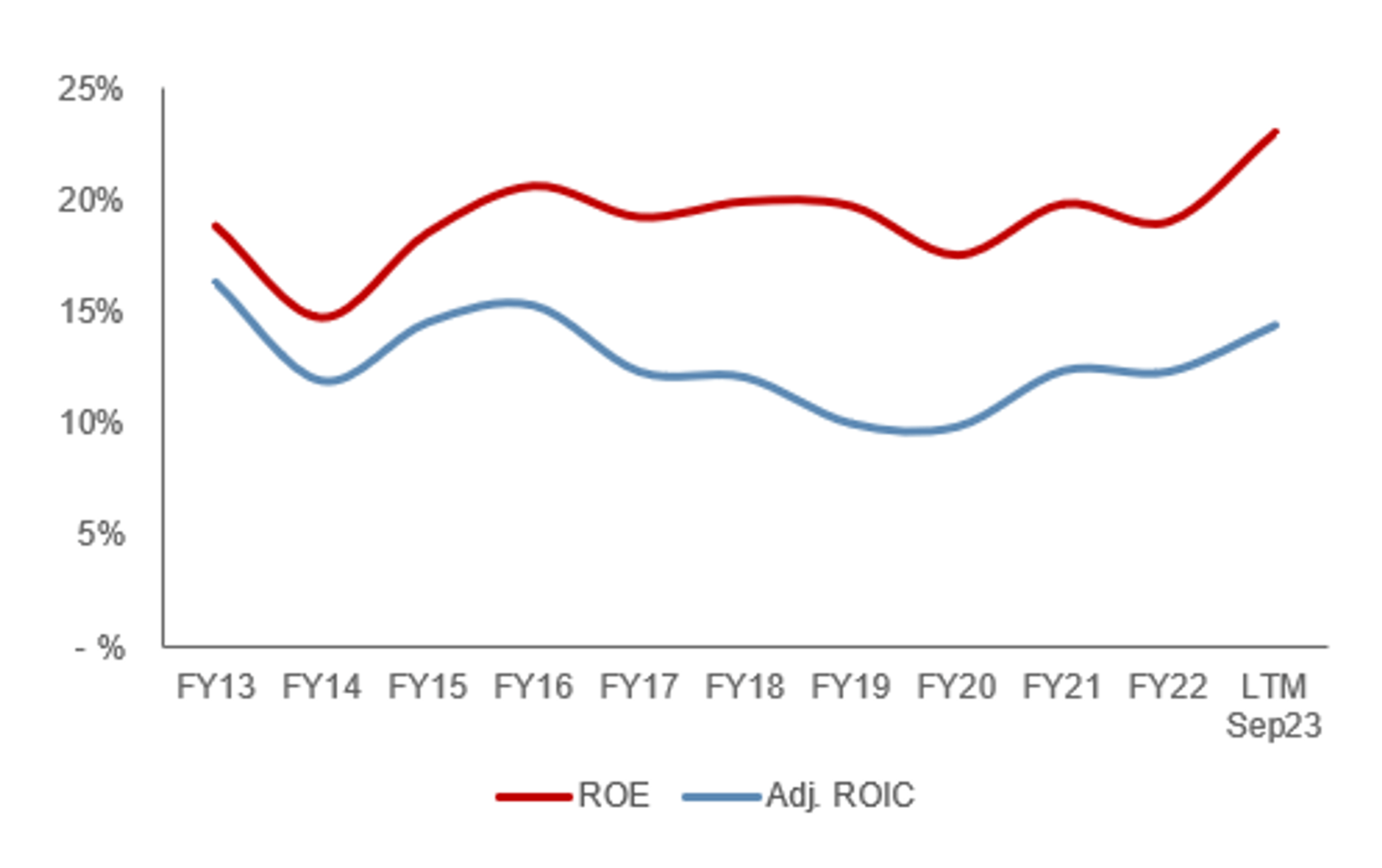

This said, the inherent returns of the business are respectable. As the following illustrates, both ROE and ROIC have been consistently attractive, with minimal variability and a broad improvement during the last decade.

{kind=link}

Outlook

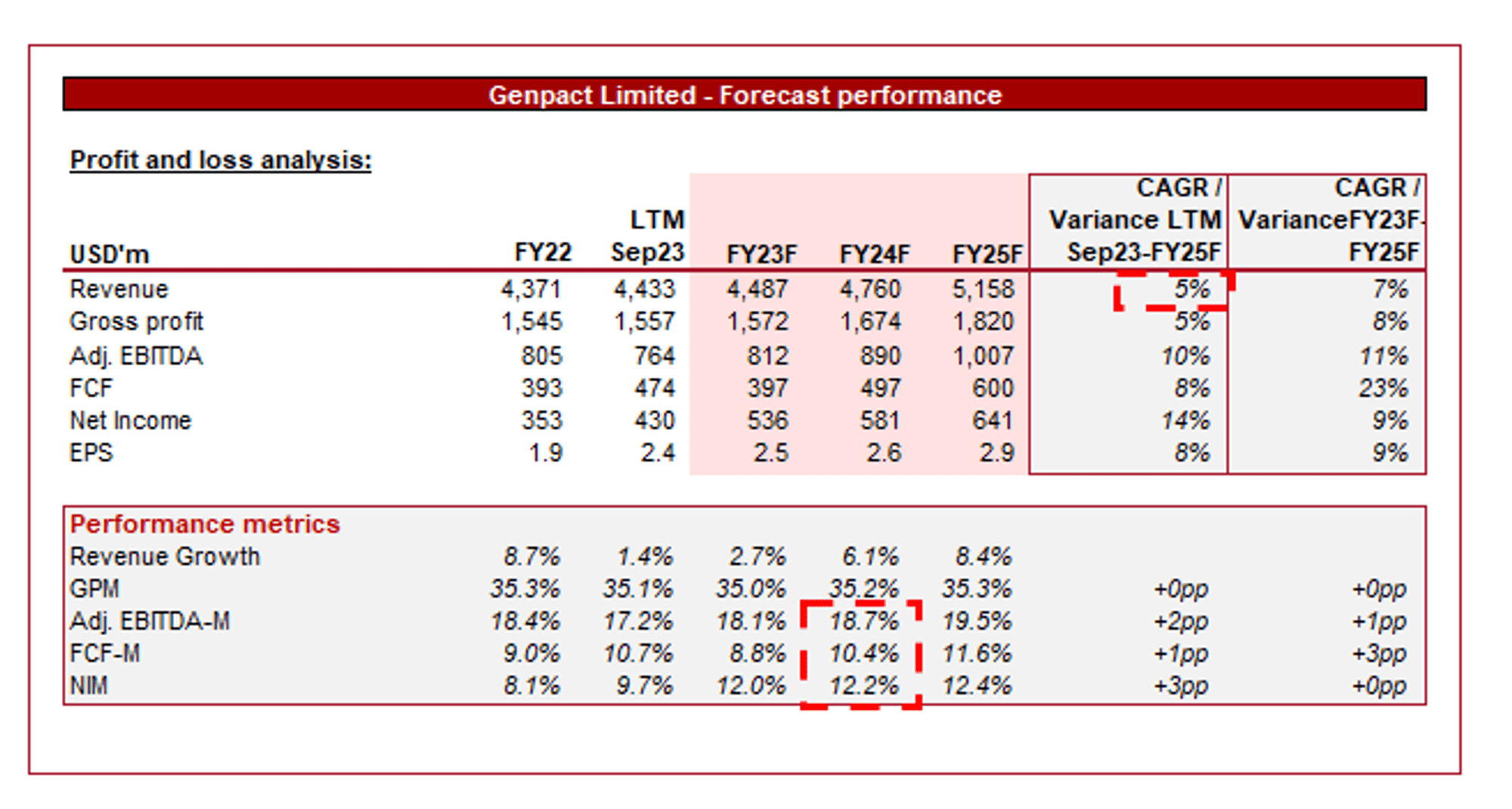

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a continuation of the company's current trajectory, with a growth rate of 5% into FY25F. In conjunction with this, margins are expected to sequentially step up, with EBITDA-M reaching 19.5% by FY25F.

The revenue forecast appears reasonable in our view, primarily due to Genpact's strong commercial position and industry tailwinds. AI and Cloud implementation, alongside Data analytics, are key value drivers that will contribute significantly to the industry's growth story.

We are less certain about margin improvement to the degree forecast, given the lack of historical improvement achieved and the competition within the market. Specific services, such as AI implementation, have the potential to garner increased margins, but competition will likely drive this down before a material level of revenue is generated.

Industry analysis

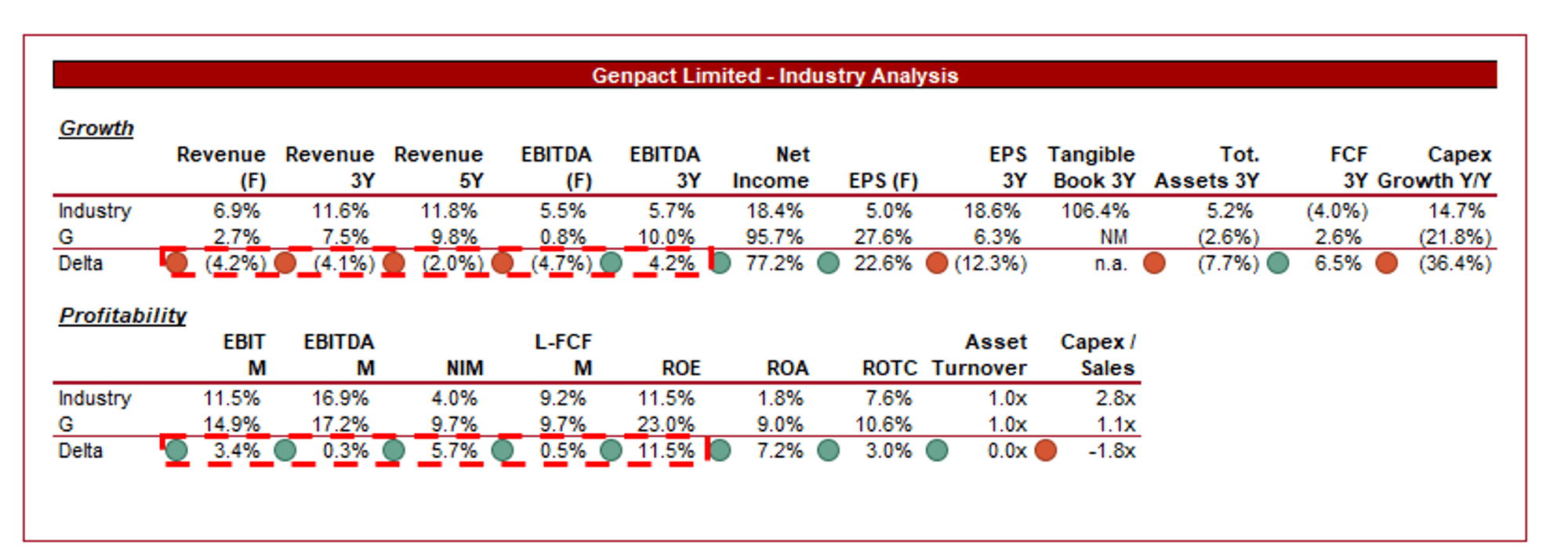

{kind=link}

Presented above is a comparison of Genpact's growth and profitability to the average of its industry, as defined by Seeking Alpha (17 companies).

Genpact performs modestly relative to its peers, without standing out. The company's revenue growth has lagged behind the market on a 3Y and 5Y basis, with the expectation that this will continue. The reason for this is likely a degree of commercial weakness, as peers have been more successful with winning new mandates. From general observations, we have seen other firms be more aggressive with their marketing. Offsetting this somewhat is an outperformance in profitability growth, reflecting the resilience of Genpact's business model. It is one of the largest members of the industry group, making it more difficult to achieve absolute gains but equally provides greater resilience.

Genpact's strength is its margins, with a comfortably higher NIM and ROE, while FCF is slightly above average. This is a reflection of its scale, allowing for greater operating cost leverage. Also, the company is weighted more heavily toward delivery centers.

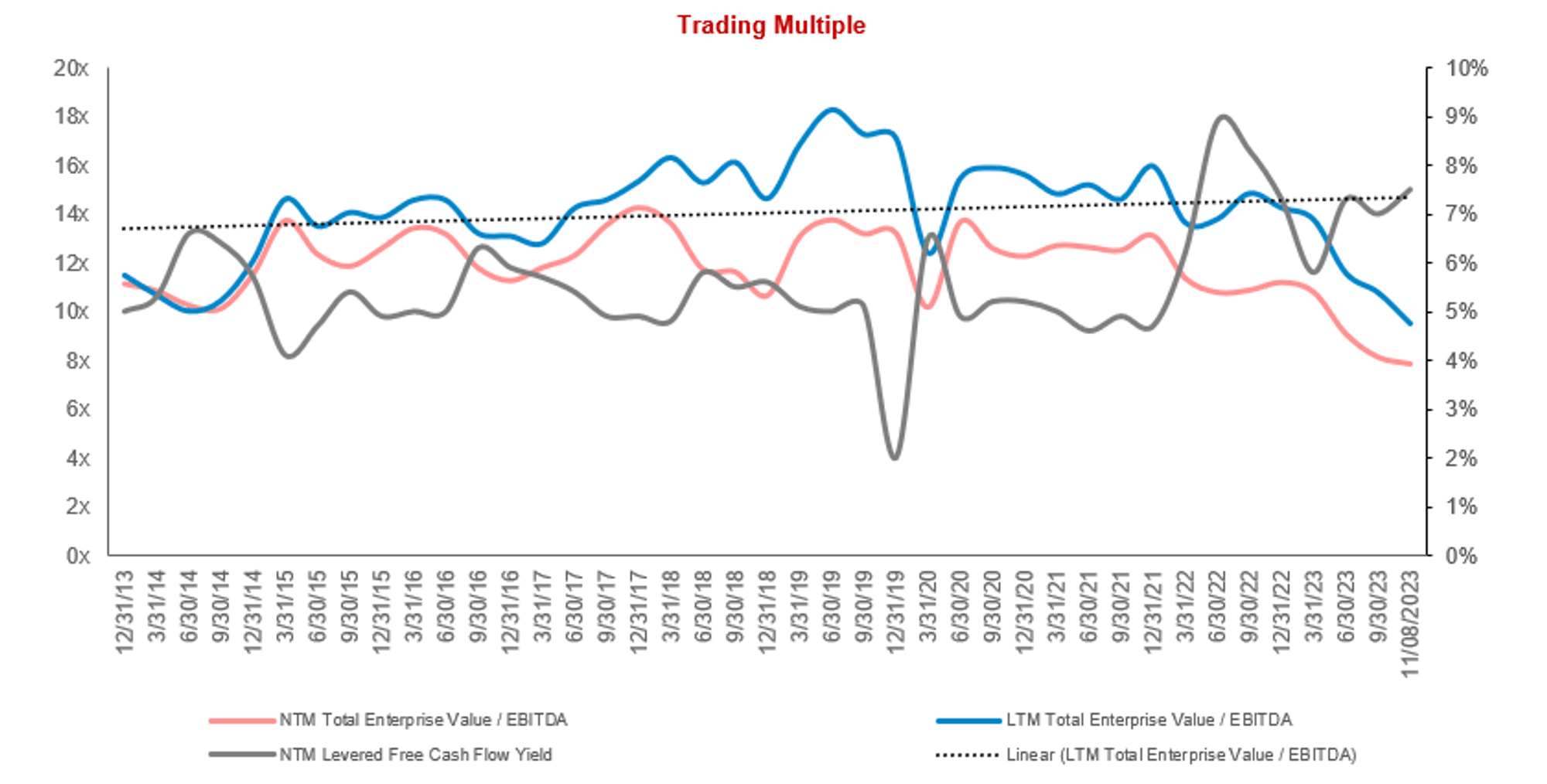

Valuation

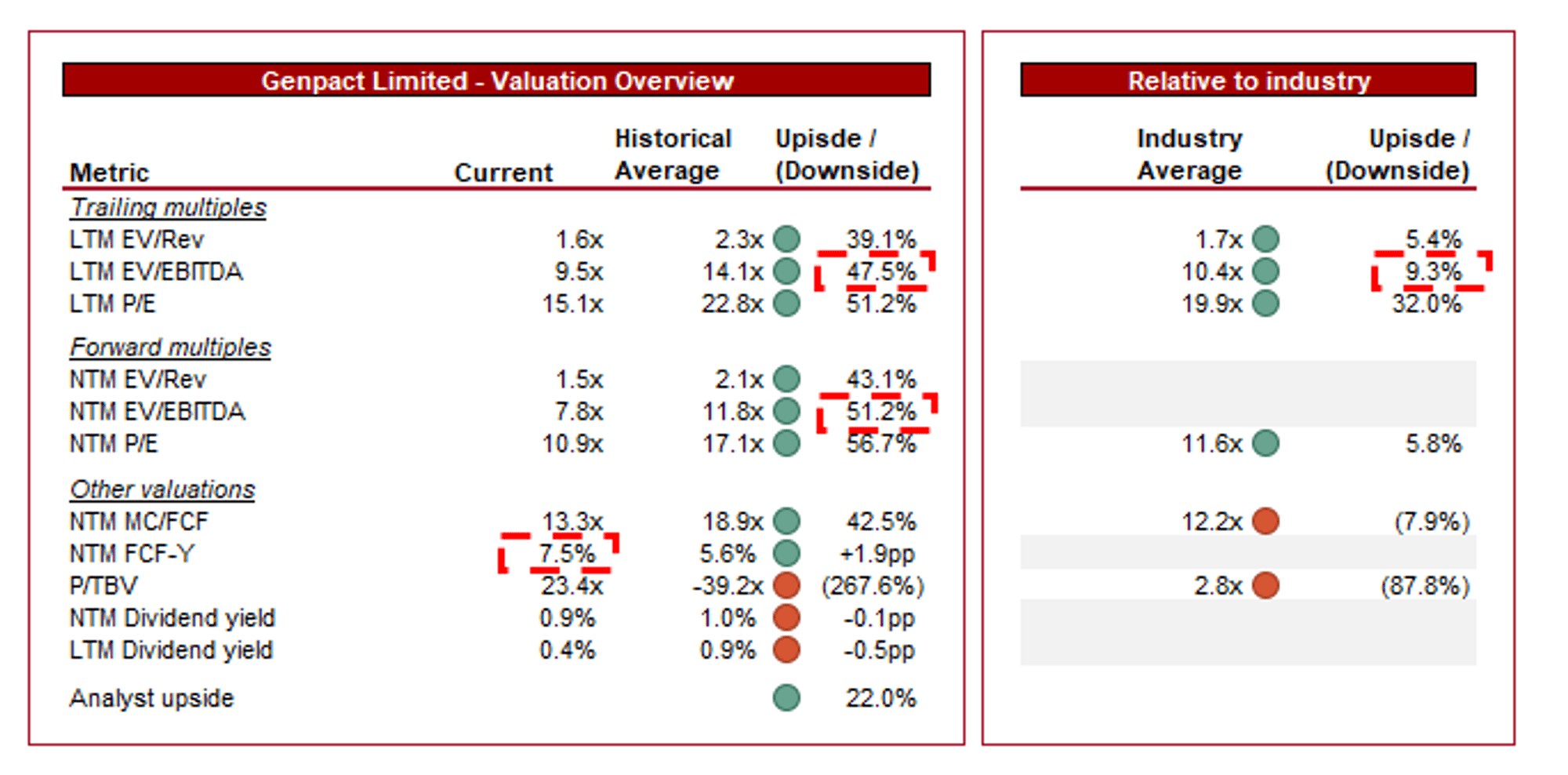

{kind=link}

Genpact is currently trading at 10x LTM EBITDA and 8x NTM EBITDA. This is a discount to its historical average.

A noticeable discount to its historical average is difficult to justify in our view, primarily due to the resilience of its demand and margins, as well as its strong commercial position within the market that should allow for a continuation of its current growth. Genpact's valuation was heightened for an extended period post-pandemic and so a 15-25% discount should be baked in to reflect this.

Furthermore, the company is trading at a discount to its peers on a LTM EBITDA basis and a NTM P/E basis. Given the revenue growth weakness and only minimal margin superiority, we would suggest a small premium based on the scope for outsized returns through profitability.

The historical analysis implies a ~25-35% upside in our view, while the relative valuation is lower, closer to low double digits. Our weighting would be toward the historical metrics, given the limited valuation volatility and greater directional uniformity.

As the following illustrates, Genpact's valuation had been on a slight upward trajectory, with the recent share price decline bringing the company well below its average. This gives the company a NTM FCF yield of ~8%, an attractive return in our view given the investment in distributions.

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- Declining competitive position - Genpact's business plan appears strong and the industry growth is clearly high, yet the business has seemingly been unable to sufficiently outperform given its size. There is the risk that Genpact is inferior in how it targets and sells to clients. Firms like Endava ( DAVA ) have been extremely good with marketing their services and gained market share rapidly via this.

- Economic downturns - Macro conditions will continue to affect client spending on professional services. The extent to which rates begin to decline and expansionary policy returns will be critical to growth accelerating.

Final thoughts

Genpact is a solid business that has achieved healthy growth for an extended period of time. This has been achieved through a combination of deep expertise, scale and capabilities, a strong track record, and industry tailwinds encouraging an increasing level of adoption. Although the specific technology and transformation exercise will change, we believe the broader trend remains strong, implying a continuation of its current growth.

Genpact is far from perfect, with its performance relative to peers underwhelming (but still strong, owing to its size). We believe there could be a degree of losing its attractiveness in the market relative to newer firms. Further, we are not sold on the capital allocation.

Following the substantial share price decline at the start of the year, this appears to be a good option to gain exposure to a growing industry. At a NTM FCF yield of ~8%, investors are well rewarded.

For further details see:

Genpact: AI And Cloud Likely To Drive Transformational Demand