LEA - Gentex Corporation: A Downgrade After A Great Run Higher

2023-12-26 05:50:56 ET

Summary

- Gentex Corporation, a supplier of automotive products, has seen its shares rise 21.9% since April 2022, outperforming the S&P 500.

- The company's financial performance remains strong, with revenue increasing by 16.7% in the third quarter of 2023 compared to the same period last year.

- Despite the positive results, the stock is now considered fairly valued and pricey compared to similar firms, leading to a downgrade from 'buy' to 'hold'.

The longer that you invest, the more likely you are to find particular areas of the market that you develop a good degree of skill in gauging. One market segment that I have come to really understand is the automotive space. Not so much when it comes to the big-name automotive companies, but rather automotive suppliers, retailers, and service providers. One company that I have been bullish about in this space happens to focus on the production of digital vision, connected car, and dimmable glass products, on top of some fire protection products that it sells, is Gentex Corporation (GNTX).

The first bullish article that I wrote about the company came out in April of 2022. Since the publication of that article, shares are up 21.9% while the S&P 500 is up 8.2%. More recently, in June of this year, I reiterated my 'buy' rating on the stock. In that article , I talked about the strong financial performance of the firm, particularly on the top line. Add on top of this how cheap shares were, and I believed that a soft 'buy' rating was appropriate at that time. Since then, the stock has shot up 19.5%, which is nearly double the 9.5% increase seen by the S&P 500 over the same period of time.

Operationally speaking, I still very much like what the business does. Financial performance continues to be robust, both on the top line and the bottom line. Having said that, I am no longer as bullish as I once was. Despite continued strength, shares have gotten a bit lofty. To me, they look fairly valued on an absolute basis and they are quite pricey compared to similar firms. Given my interpretation of the data, I have decided to downgrade the stock from a 'buy' to a 'hold' to reflect my view that shares should generate upside or downside that is more or less in line with the broader market moving forward.

Positive results persist

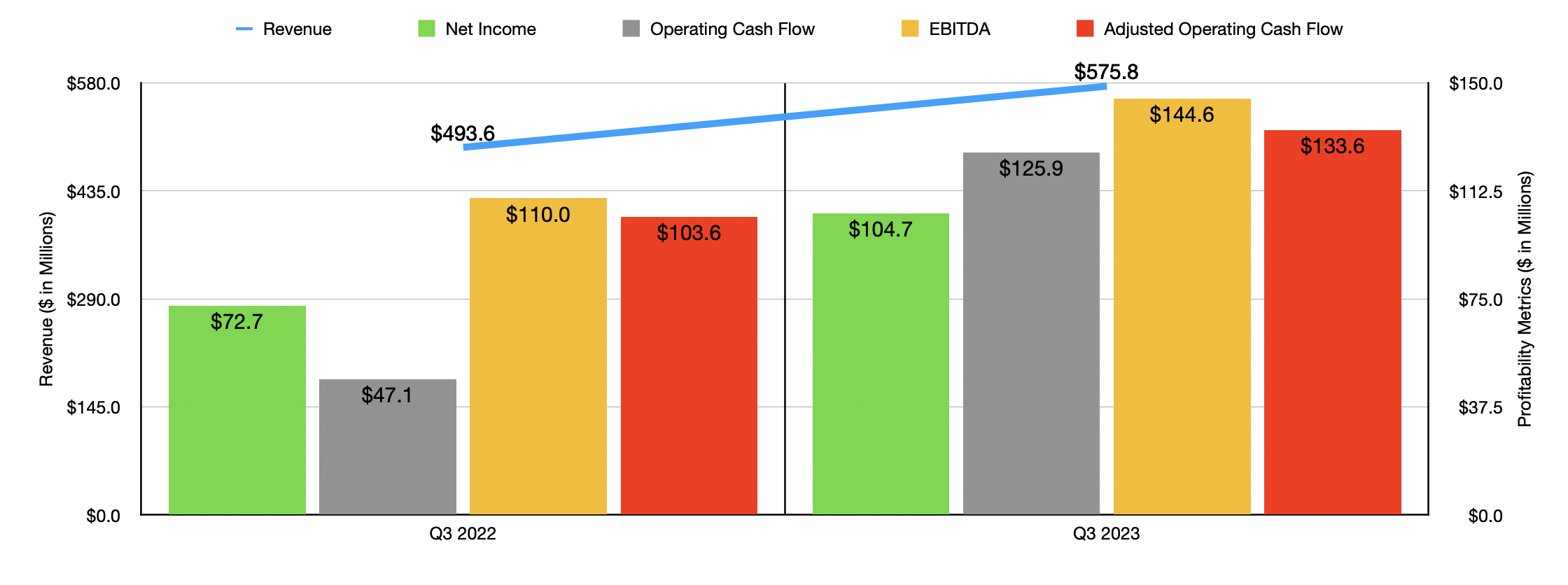

Back when I last wrote about Gentex, we had data covering through the first quarter of the 2023 fiscal year. Now, that data covers through the third quarter of the year. During that quarter, revenue came in at $575.8 million. That's 16.7% above the $493.6 million generated in the third quarter of 2022. This growth was driven by strength across pretty much every sales category that the company reports for.

{kind=link}

For instance, when it comes to the number of units sold, the company reported a 9.7% increase for North American interior mirrors. That took the number of units delivered from 2.16 million in the third quarter of last year to 2.37 million at the same time this year. North American exterior mirror sales were a much more modest 0.7%, with the number of units inching up from 1.60 million to 1.61 million. The firm has also experienced strength when it has come to international interior mirror sales. The number of units in this case jumped 8% from 5.29 million to 5.71 million, while international exterior mirror sales skyrocketed 19.3% from 2.44 million to 2.92 million.

All combined, management claimed that automotive net sales for the business rose by about 17.4%. This makes a great deal of sense to me. For quite some time now, new and used vehicle sales have been incredibly high, largely because of higher prices driven by supply chain shortages. A lot of this had to do with a massive semiconductor shortage that had its roots in the pandemic. According to S&P Global Mobility, it was believed that this caused 9.5 million fewer light vehicles to be produced in 2021 alone than what demand warranted. The industry was short by another 3 million units in 2022. But by 2023, the picture has mostly resolved itself. In the first half of the year, supply constraints regarding semiconductors resulted in only 524,000 fewer units being produced than what demand called for. In an article that I just published on General Motors ( GM ), I detailed how the number of vehicles produced globally in the first nine months of this year came in at 63.46 million. That's 9.3% above the 58.06 million reported the same time of 2022. So with that kind of improvement, it's not shocking to see a rebound in orders when it comes to the products that Gentex offers.

The only weakness for the company came from its fire protection products. Sales in the third quarter dropped by more than half from $10.5 million to $5.2 million. But this was almost offset by a surge in dimmable aircraft sales from $2.2 million to $6.2 million. When it comes to the bottom line, the picture for the company was really quite robust. Net profits jumped from $72.7 million in the third quarter of 2022 to $104.7 million in the third quarter of this year. Operating cash flow almost tripled from $47.1 million to $125.9 million. If we adjust for changes in working capital, we get an increase from $103.6 million to $133.6 million. And lastly, EBITDA managed to grow from $110 million to $144.6 million.

{kind=link}

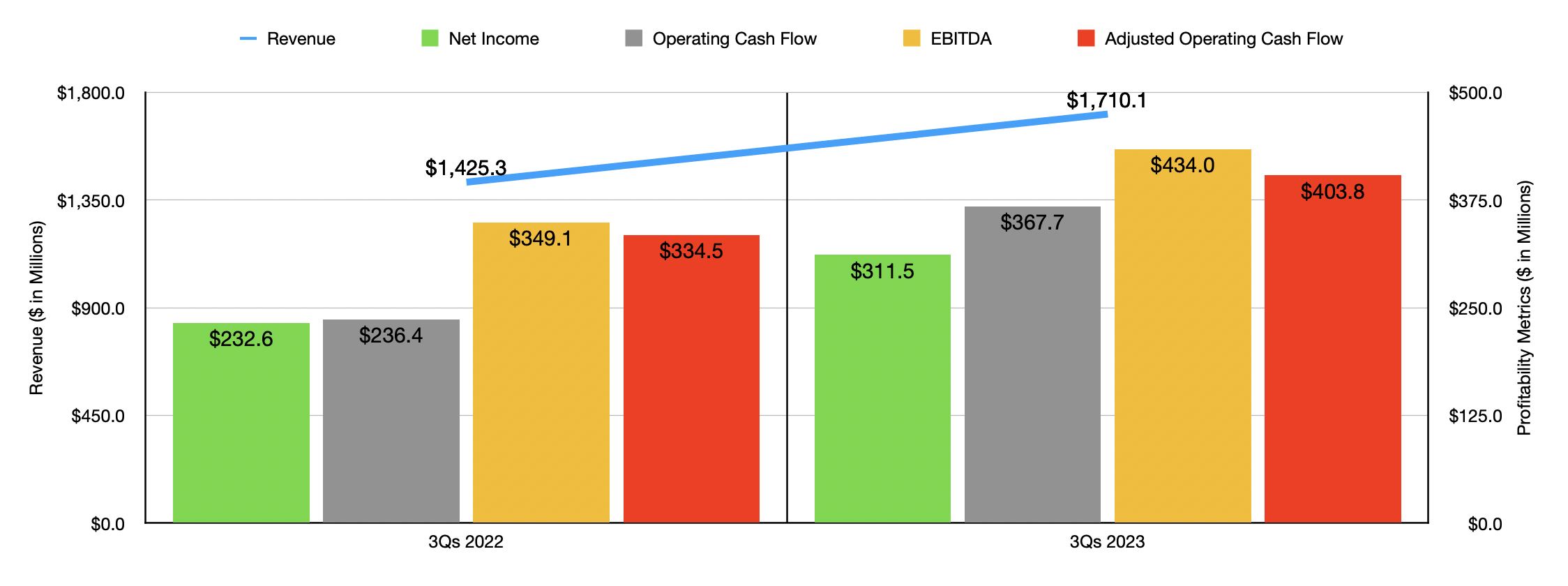

As you can see in the chart above, financial performance for the first nine months of 2023 and its entirety completely outpaced, in every respect, financial performance for the same time last year. The good news is that management expects this trend to continue. For this year, revenue should come in at between $2.2 billion and $2.3 billion. For 2024, revenue is expected to climb even further to between $2.45 billion and $2.55 billion. Management provides some estimates for the bottom line, but only enough to let us piece together what might be realistic. Using their guidance, I calculated that this year should result in net profits of $316.3 million. Adjusted operating cash flow should be $413.6 million, while EBITDA should come in at around $471.9 million.

{kind=link}

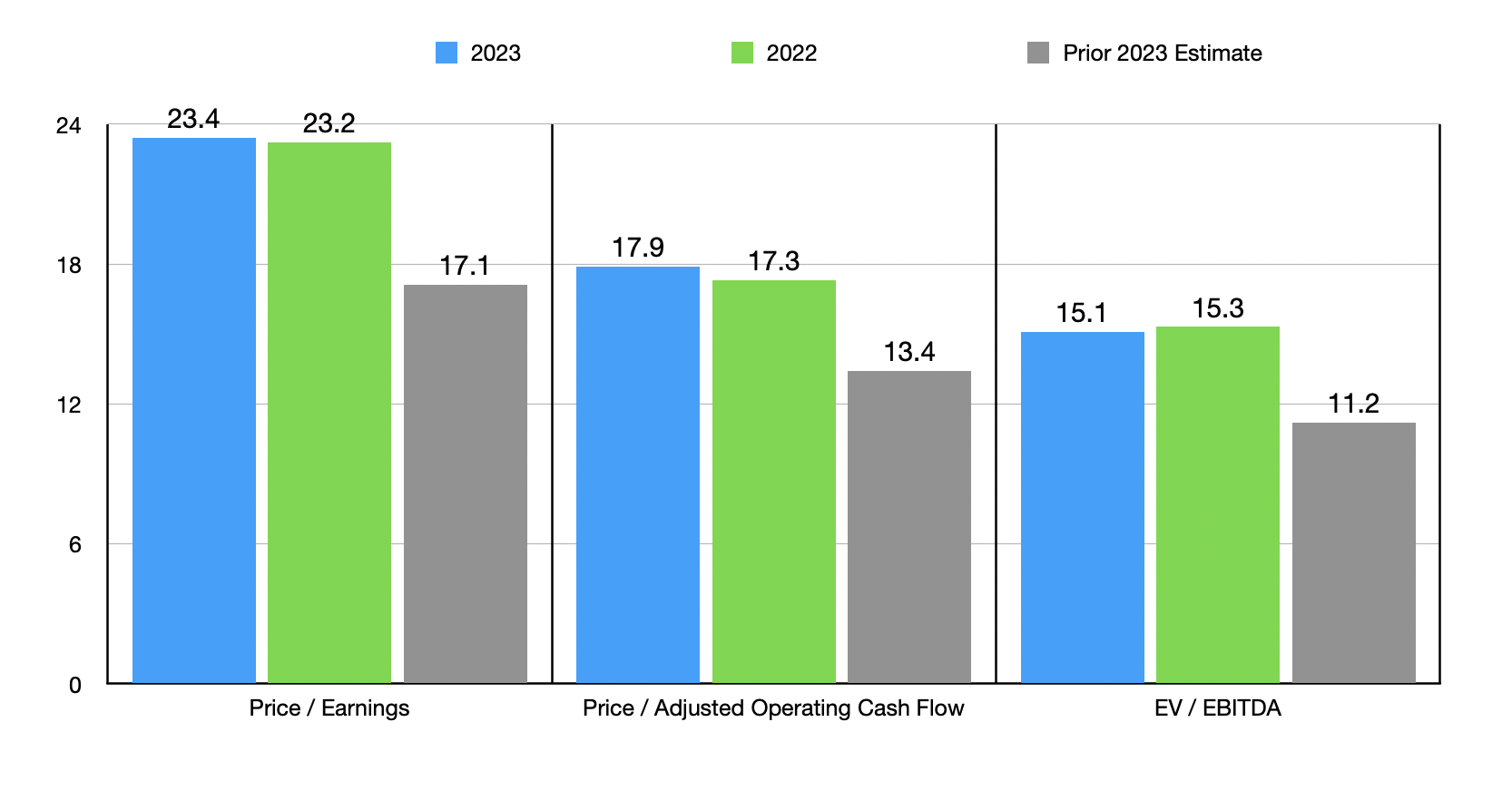

Using these figures, I was able to value the company on a forward basis and also value the company using data from last year. Both of these can be seen in the chart above. Included in that chart is how shares were priced on a forward basis for 2023 when I last wrote about the company back in June. I then decided to compare the company to five similar firms as shown in the table below. In addition to the stock looking more expensive relative to when I last wrote about the business, shares are also very pricey relative to similar firms. Using both the price to earnings approach and the price to operating cash flow approach, four of the five companies I compared it to ended up being cheaper than it. And when it comes to the EV to EBITDA approach, it is the most expensive of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Gentex Corporation |

| 23.4 |

| 17.9 |

| 15.1 |

| Autoliv ( ALV ) |

| 21.8 |

| 9.1 |

| 9.5 |

| Lear Corp ( LEA ) |

| 14.8 |

| 6.9 |

| 6.8 |

| Fox Factory Holding Corp ( FOXF ) |

| 16.9 |

| 11.2 |

| 10.9 |

| Standard Motor Products ( SMP ) |

| 25.1 |

| 4.9 |

| 7.6 |

| Modine Manufacturing ( MOD ) |

| 15.0 |

| 19.0 |

| 11.6 |

Takeaway

From all the data at my disposal, I would argue that the long-term outlook for Gentex should be positive. I suspect that the automotive market in general will be quite bullish next year, at least so far as the US is concerned. This should result in continued growth for the company, though I do not think that it still makes sense to be all that bullish about the business from a share price perspective. The stock looks to me to be fairly valued or awfully close to it. Even though the stock very well could continue to appreciate, it's important to be conservative when it comes to financial expectations. And following that approach, I do believe that downgrading the firm to a 'hold' is the most logical step right now.

For further details see:

Gentex Corporation: A Downgrade After A Great Run Higher