GNTX - Gentex Corporation: Returns Not Worth The Risk

2023-06-29 09:54:11 ET

Summary

- Gentex Corporation's valuation is more attractive than it used to be, but the stagnant dividend yield and lack of growth potential make it unappealing.

- Gentex has a strong capital structure, with total assets significantly outweighing total liabilities, but the dividend yield is not competitive compared to risk-free investments and the stock price has been stagnant since 2019.

- The market seems overly optimistic about Gentex growth prospects, and since Treasuries offer better risk-adjusted returns, they are a better alternative.

Since I put out my “avoid” piece last year on Gentex Corporation ( GNTX ), the shares have returned 4% against a gain of about 6.8% for the S&P 500 (SP500). This relative underperformance has me intrigued. The company has reported financials since, obviously, so I thought I’d compare those to the current valuation to see if it’s finally time to bite the proverbial bullet here. Additionally, I think this stock offers me an interesting opportunity to offer some comments about how to contextualize all investments. I’m looking forward to getting up on that soapbox, and I hope you’re looking forward to reading.

One thing my regulars know about me is that I’m absolutely obsessed with making their lives as pleasant as possible. If it doesn’t make your lives a little bit better, then I don’t do it, and if it does, I do it happily. One thing I learned years ago is that some of my readers want to know what my thoughts are up front so they won’t be obliged to go through the entire article, because my writing can be “a bit much.” Thus, the “thesis statement” was born.

I’m of the view that Gentex is “fine.” The valuation is more attractive now, though the dividend yield remains sclerotic, and the dividend has been unchanged for some time, and thus I don’t expect much growth from it. The problem is that in the domain of investing, everything’s relative. In a world where I can earn over 5% on government bonds, I would demand a 10% return from stocks that come with a great deal of risk. Given that the shares are about the same price as they were in 2019, I don’t see that happening. On a relative basis, and on a risk-adjusted basis, I see nothing compelling here, and will thus continue to avoid this stock.

Financial Snapshot

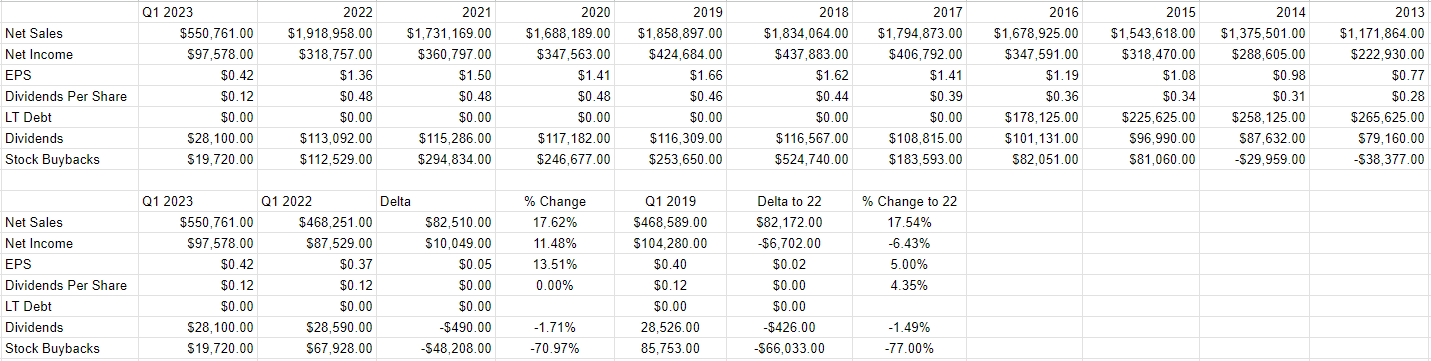

The most recent financial performance was fairly good in my view. Relative to the same period a year ago, the top and bottom lines were higher by 17.6% and 11.5% respectively. Profits are lower now than they were in 2019, though. Additionally, the dividend hasn’t really budged recently, so I’m going to compare the current dividend yield to the risk free rate in my analysis.

Finally, it should be written that the capital structure remains quite strong here, with total assets dwarfing total liabilities by about 7.85 to 1. This massively reduces the risk here in my view, which is a very compelling factor in my view.

I think the financials remain in fairly decent shape, and for that reason, I’d be happy to buy this stock at the right price.

Gentex Financials (Gentex investor relations)

{kind=link}

The Stock

I’ve been accused of being predictable, and I’ll accept that. It’s not the worst accusation that’s ever been leveled against me, so I’m actually quite fine with it. Anyway, given that I’m predictable, you may know approximately what I’m about to write, namely that I consider the stock and the business to be two different things. Gentex supplies, among other things, digital vision for the auto industry. The stock is a slip of virtual paper that represents an ownership claim on the future cash flows of the business, and aggregates the crowd’s collective view on any given day. The crowd can be quite capricious. Also, a stock may be bid up in price simply because the crowd’s feeling buoyant about equities as a group. Additionally, the stock may be affected by the changes in interest rates.

In my experience, the only way to profitably trade stocks is by spotting discrepancies between expectations and subsequent reality. If the market is unreasonably optimistic, you avoid the stock, and if the market is overly pessimistic, you buy. Additionally, another way of writing "overly pessimistic" is "cheap." I like cheap shares because they have that great combination of lower risk and higher potential reward. They're lower risk because much of the bad news has already been "priced in." Additionally, cheap shares are potentially greater reward because a small bit of good news has the potential to send the shares skyward.

I measure the relative cheapness of shares in a few ways, ranging from the simple to the more complex. On the simple side, I like to look at the ratio of price to some measure of economic value, like earnings, sales, book value, and the like. I want to see the company trading at a discount to both the overall market and its own history. In my previous missives on this name, I continued to eschew the shares because they were trading at a P/E of 32.36 and the dividend yield was a paltry 1.71%. The shares are now about 38% cheaper, per the following, but they remain expensive relative to the company’s history. Also, the dividend yield is about 410 basis points lower than what you could get on a risk free investment at the moment.

You may remember that earlier in the article I pointed out that investing is about trying to spot the discrepancies between expectations and subsequent reality. In my view, you want to get out when the crowd becomes too optimistic about the future, and you want to buy when the crowd is down in the dumps.

Being a bit of a math nerd, I want to try to quantify expectations as much as possible, and to do that I turn to “Accounting for Value” by Stephen Penman or “Expectations Investing” by Mauboussin and Rappaport. Both of these books consider the stock price itself to be a great source of information, and the former in particular helps investors with some of the arithmetic necessary to work out what the market is currently "thinking" about the future of a given business. This involves a bit of high school algebra, where the "g" (growth) variable in a standard finance formula is isolated, and thus tells us what the market must be assuming about growth.

Using this methodology, we can work out that the market seems to be assuming that earnings will grow at a rate of about 5% in perpetuity, which is fairly optimistic in my view. Before deciding whether this is “good” or “bad,” I need to put the investment in some kind of context.

TINA’s Not Home Right Now

I’m sometimes astonished by some of the comments I’ve read on this site. I understand the thinking, but it’s flawed, and I’m about to climb up on my soapbox and write about why I think it’s flawed. The notion that’s often expressed is that an investment is “good” if it happens to go up in price after you bought it, and it’s “bad” if it does the opposite. That’s fair enough on first thought, but it misses a very important contextual element. Would you think it prudent to take all of your capital and buy lottery tickets with it? Would the decision be a smart one if, after the fact, you happened to hit it big? Would that make the decision to go all in on lottery tickets a smart one? I’m blathering on in this way in order to remind readers that you need to also factor in the amount of risk taken in order to achieve a given return, and that risk is contextual. You need to remember that in the world of investing, everything’s relative. When you buy a stock, you are, by definition, eschewing a rather large number of other investments. When you buy, you’re really expressing the idea that this is the most effective use of my capital right now, and by buying this investment, you have the greatest chance of receiving above average risk adjusted returns.

Given that an investor can earn 5.3% virtually risk free at the moment, what should they demand from Gentex? How much of a return, above the risk free rate, would you demand to take on the risk of this investment? Would you expect a premium over the risk-free rate of another 5%, as I would? Are you more risk averse than me, and might need 7% over the risk free rate? Are you less risk averse?

Whatever the case, the dividend yield here won’t help matters very much. Either way, the dividend is so paltry, that in order to get excited here, I’d need the shares to move from their current $29.00 to about $31.90 over the next twelve months. The problem for me is that the shares are about the same price now as they were on my birthday in 2019. In case you’ve forgotten, my birthday is December 2nd. So, my view of this company could be summed up onomatopoeically as “meh.”

On balance, I see no reason to think that Gentex Corporation shares will beat the returns you could earn on a government bill, let alone what should be required of a risky stock over the next twelve months, and thus I’m compelled to continue to eschew these. I think government debt represents a much better risk adjusted return at the moment, so I'll be buying Bills instead.

For further details see:

Gentex Corporation: Returns Not Worth The Risk