GNTX - Gentex Corporation: Strong Revenue Growth Outlook With Focus On Margin Expansion

2023-12-20 18:18:29 ET

Summary

- GNTX's 3Q23 results have shown robust revenue growth and margin expansion, driven by continuous product launches and cost reduction initiatives.

- The anticipated growth in the global car sales market will support GNTX's future growth outlook, as it holds a significant market share in the automotive parts and equipment industry.

- My conservative comparable valuation revealed that GNTX outperformed its competitors in all areas. Thus, justifying its higher multiples.

Synopsis

Gentex Corporation (GNTX) is a company that designs, manufactures, and sells automotive products, primarily auto-dimming rearview mirrors, camera-based driver assistance systems, and other technologically advanced automotive equipment, to major car manufacturers globally.

In this post, I am recommending a buy rating for GNTX, and this recommendation is grounded on several factors. In terms of its past financial performance, it has shown a robust and increasing revenue growth trend. Its 3Q23 results also echo the same revenue growth trend, but with a little caveat, which is margin expansion.

Moving forward, the anticipated growth in the global car sales market is set to bolster GNTX's growth outlook. With its continuous product launches and focus on cost reduction, these initiatives position them well not just for top-line growth but also for their bottom line.

Historical Financial Analysis

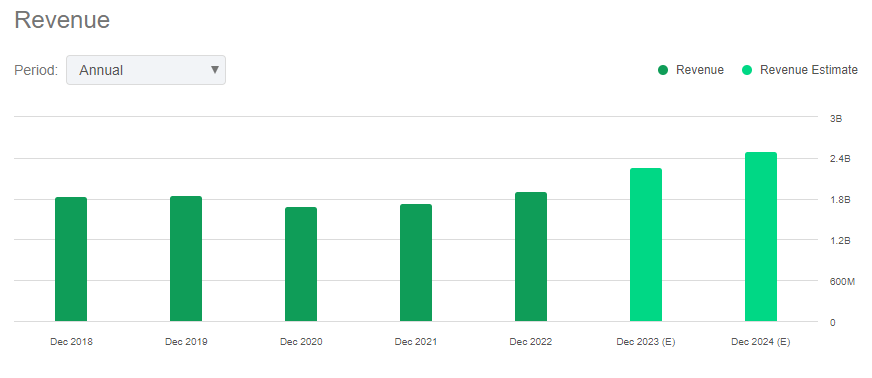

Over the last 4 years , GNTX's revenue growth has been accelerating. In 2019, it grew at a modest rate of 1.35%. In 2021, it improved to 2.55%, and by 2022, it had grown in the double-digit range of 10.85%. In 2020, revenue fell 9.18% due to the COVID-19 pandemic. Its main revenue comes from the automotive sector, particularly from products like automatic-dimming rearview mirrors and automotive electronics. These sectors were significantly affected by the global slowdown in automotive manufacturing and sales during the pandemic.

Author's Chart

Next, let's move on to the margins. Based on the chart I created below, there is a clear trend showing that margins across the board are contracting. Firstly, the gross profit margin contracted from 37.03% in 2019 to 31.78% in 2022. Secondly, the operating profit margin also contracted; it was 26.28% in 2019 and contracted to 19.28% by 2022. Lastly, the net income margin contracted from 22.58% in 2019 to 16.36% in 2022.

Author's Chart

Next, I would like to investigate the drivers behind the contraction of its margins. In terms of SG&A expenses and R&D, these have remained stable over the past four years. It's clear that the primary driver here is the rising COGS. Management has attributed this increase to heightened raw material costs, higher manufacturing expenses, and increased freight and logistics costs, all exacerbated by inflation. Additionally, the company faced challenges such as customer order volatility and supply chain constraints, which also contributed to these rising costs.

Author's Chart

With contracting margins, it's essential to analyze the company's debt level to ensure financial soundness and robustness. In terms of debt, GNTX is essentially debt-free, which is welcome news to me. As a result, its interest expense as a percentage of revenue from 2019 to 2022 is essentially 0%. Hence, I do not foresee any liquidity risk with GNTX.

Author's Chart

Analyzing GNTX's 3Q23 Financial Results: Performing Better or Worse?

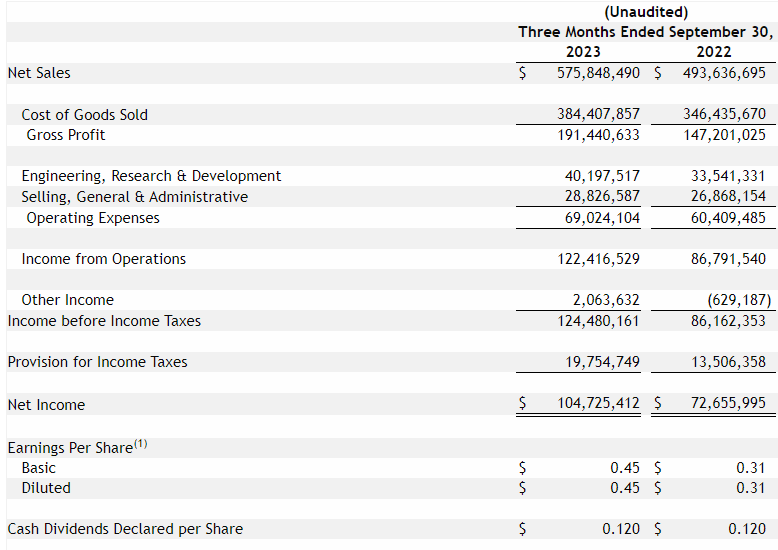

In my opinion, GNTX reported strong 3Q23 results. Its net sales grew ~17% year-over-year to ~$575.8 million. This growth can be attributed to the improving and growing global light vehicle production, which drove demand for GNTX's products. In addition, management stated that this growth seen in 3Q23 can be attributed to its strategy of innovating and introducing new technology-driven products, like the Full Display Mirror. These strategic initiatives are paying off in terms of driving revenue higher. Therefore, from this, I interpret that the strong growth is not just driven by strong global vehicle production, which is macro in nature, but also by idiosyncratic factors such as GNTX's technological innovation.

In my 'historical financial analysis' segment, I noticed and highlighted its contracting gross profit margin, caused by the growing COGS, mainly due to inflation pressure. In 3Q23, the gross profit margin is ~33.2%, an improvement of 3.4% from 3Q22. From this, it's clear that its gross profit margin is recovering, and I see this as a positive signal for the company.

In terms of income from operations, it grew a staggering 41% year-over-year. 3Q23's income from operations was reported as $122.4 million. In addition, its net income also reported extremely strong growth; it grew 44% year-over-year to approximately $104.7 million. As a result of the lowered COGS, both income from operations and net income margins expanded year-over-year. The income from operations margin grew from 18% to 21%, while the net income margin grew from 15% to 18%. As a result of these bottom line margin improvements, 3Q23's diluted EPS grew 45% year-over-year to $0.45.

Author's Chart

Based on the following chart, it's clear that the main driver for these margin expansions is lower COGS. R&D and SG&A have stayed consistent, which is important because, as mentioned earlier, innovation is one of their key drivers of growth.

Author's Chart

{kind=link}

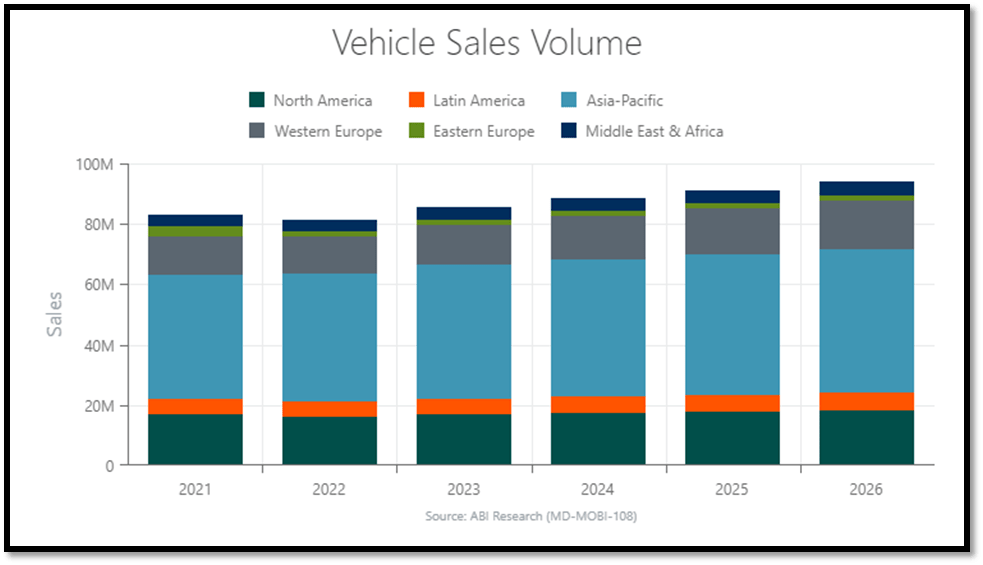

Global Car Sales Growth Will Support GNTX's Growth Outlook

Based on the following chart from ABI Research, it's clear that the global car market is expected to continue growing for the next 4 years. In 2022, the total vehicle sales volume was approximately 80 million, and by 2026, it is expected to reach around 90 million. This represents a CAGR of approximately 2.4% over the next 4 years. In the short term, the global vehicle market is anticipated to continue growing, hence positively bolstering GNTX's revenue growth outlook.

{kind=link}

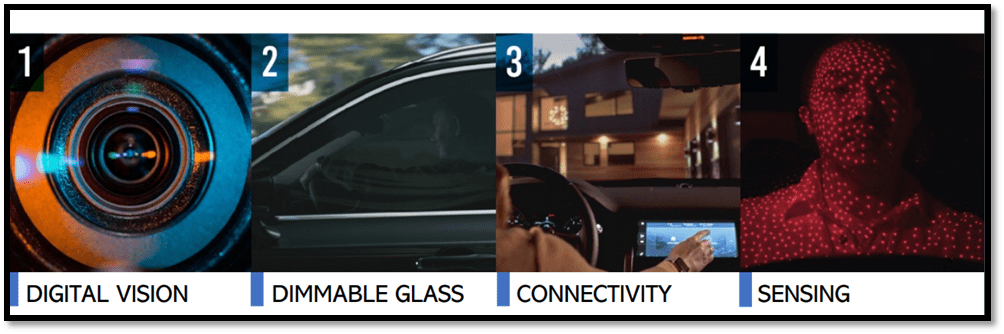

The reason global car sales will bolster GNTX's growth outlook is that GNTX operates in the automotive parts and equipment industry. It manufactures and sells automotive products in the areas of digital vision, glass, connectivity equipment, and sensors. Based on GNTX's past reports , it holds approximately 93% of the market share in the smart rear-view mirror market, and it is trusted by most of the major car manufacturers in the world. Therefore, I believe the growing vehicle sales market will positively influence GNTX's growth outlook.

{kind=link}

Sustaining Strong Revenue Growth through Continuous Product Launches

In 3Q23, GNTX demonstrated their commitment to achieving revenue growth through product portfolio expansion and an emphasis on technological features. Key highlights include its Full Display Mirror and HomeLink. The Full Display Mirror has been a standout product for GNTX. In the quarter, it saw a significant increase in demand for its Full Display Mirror, driven by rising demand from end consumers.

This rising demand from end consumers ties in with the growing vehicle sales market I have discussed above. This has led to higher volumes, indicating strong market acceptance for this innovative product. GNTX reported shipping approximately 1.75 million units of the Full Display Mirror in the first nine months of 2023, with expectations for these numbers to grow.

Continuous Focus on Cost Reduction to Improve Margins

Apart from consistent product launches, GNTX is also placing a lot of emphasis and focus on cost management , realizing the impact of cost on margins. For GNTX's historical financial performance, I have discussed and highlighted how rising COGS has been contracting its margins, raising my concerns regarding GNTX's profitability. In 3Q23, management stated that it is working towards design optimization by sourcing the same quality but more cost-effective components.

Doing so provides GNTX with a number of business benefits. Firstly, from an internal standpoint, it reduces costs, which will effectively improve its margins. Secondly, from a customer's viewpoint, GNTX products' pricing will be much more attractive without any sacrifice in quality.

Therefore, moving forward, I expect this proactive approach from management will continue to bolster GNTX's future margins. With better margins, EPS will improve and ultimately trickle down to its share price.

Comparable Valuation

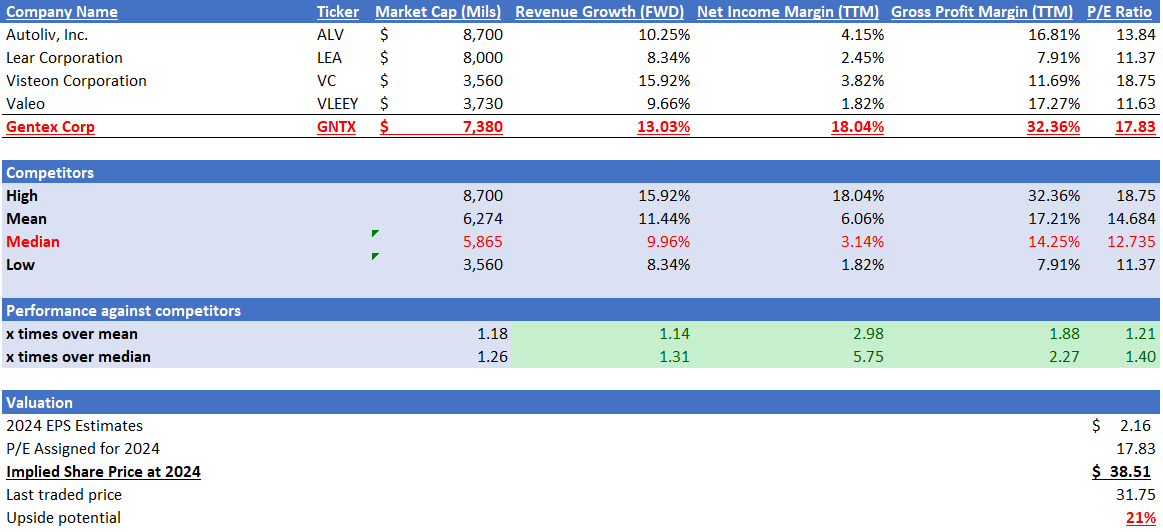

The four competitors I have listed below operate in the automotive parts and equipment industry, just like GNTX. Therefore, this group is a good representation of the industry that will be used for my comparable valuation.

GNTX's market capitalization is ~$7.38 billion; this means that it is ~1.26x larger in terms of size than its competitors', as they have a median of ~$5.865 billion. Although GNTX is a larger firm, its forward revenue growth outlook outperforms competitors' median. GNTX is ~13.03% vs. competitors' median of ~9.96%.

When it comes to profitability, GNTX significantly outperformed its competitors. GNTX's net income margin is 18.04% vs. competitors' median of 3.14%. GNTX's gross profit margin of 32.36% also outperformed competitors' median of 14.25%.

As a result of GNTX's outperformance in terms of both growth outlook and profitability, its current P/E of 17.83x is higher than competitors' median of 12.735x. Therefore, its current P/E ratio seems justified and fair. In addition, its 3-year P/E averages ~20x, which is above what it is trading right now.

{kind=link}

{kind=link}

The market revenue estimate for GNTX is expected to reach $2.26 billion in 2023 and $2.5 billion in 2024. The market estimate for GNTX's 2024 EPS is $2.16. Given my discussion on GNTX's financial strengths and growth catalysts above, it supports and bolsters these estimates. By applying 17.83x P/E to its 2024 EPS estimates, my 2024 price target is $38.51, and this represents an upside potential of ~21%. Overall, my buy recommendation also ties in with Wall Street's average analyst rating, providing a form of a sanity check on my thesis.

{kind=link}

{kind=link}

Seeking Alpha

Downside Risk

One downside risk pertaining to GNTX would be regarding its profit margins. As discussed above, I observed that its margins were contracting over the years, caused by rising COGS. During 3Q23, management did take active steps in an attempt to control costs. However, no one can predict the direction of inflation. Although inflation is on a cooling trend, it's hard to tell if it will take a turn for the worse. In that scenario, GNTX's margin will be under pressure again, and the share price might be affected if market expectations turn negative.

Conclusion

GNTX's historical revenue growth shows an accelerating trend and recovery from the 2020 COVID-19 pandemic impact. However, margins are contracting yearly due to rising COGS. Nonetheless, it is nearly debt-free, which means that its debt level does not pose any liquidity risk to GNTX. When analyzing its 3Q23 results, its revenue continues to report strong growth, which is in line with its historical trend. In addition, this time around, it is showing signs of margin expansion, which is good news for shareholders. This means that GNTX is placing emphasis on margin performance.

Moving forward, the anticipated growth in the global car sales market is set to bolster GNTX's growth outlook as they operate in the automotive parts and equipment industry. With more cars being sold, demand for GNTX's products will increase. To capture this growth, GNTX consistently launches new products. I believe these strategic initiatives will drive its future revenue growth. In addition to top-line revenue, management is also focused on margin improvement, achieved through cost-effective component sourcing.

Compared to its competitors, GNTX has outperformed them in all aspects, such as revenue growth outlook and margins, justifying its premium valuation. With double-digit upside potential, I am recommending a buy rating for GNTX.

For further details see:

Gentex Corporation: Strong Revenue Growth Outlook With Focus On Margin Expansion