GNTX - Gentex Corporation: Technology Driven Innovation Widening Its Moat

2023-10-05 14:17:05 ET

Summary

- Gentex’s revenue has grown at a CAGR of 6%, while EBITDA has lagged behind at only 4%. Macro headwinds have contributed to margin deterioration, although growth has improved.

- We suspect Gentex’s growth will begin to slow in the coming quarters, as early as Q3, owing to the elevated interest rate environment offsetting any production improvements.

- Gentex’s investment in digitalizing its product portfolio has the potential to future-proof its operations, with good progress thus far.

- Although margins have taken a beating, we do see reasonable scope for improvement, owing to subsiding inflationary pressures and investment in operational capabilities.

- Gentex’s valuation looks to be running high, despite the share price stagnation in recent years. We cannot justify its current premium.

Investment thesis

Our current investment thesis is:

- Gentex (GNTX) is positioned well to respond to future growth trends, with significant investment in R&D, driving its development in areas such as Sensor tech, dimmable devices, and digital vision. When this is considered in conjunction with its market-leading standing and relationships with OEMs, we see scope for HSD growth.

- Although we do not make investment decisions based on near-term performance, there are serious concerns about a decline in financial performance, owing to macro conditions contributing to reduced production. This would normally not be a concern but Gentex is trading at a large premium to its historical average and peer group, implying there is room for negative price action.

Company description

Gentex is a technology company that designs and manufactures automatic-dimming rearview mirrors and electronics for the automotive industry, as well as fire protection products. The company was founded in 1974 and is headquartered in Zeeland, Michigan, USA.

Gentex’s share price performance has been respectable, generating comparable returns to the wider market. This is a reflection of its gradual financial improvement for much of this period, although its fortunes have declined since 2021.

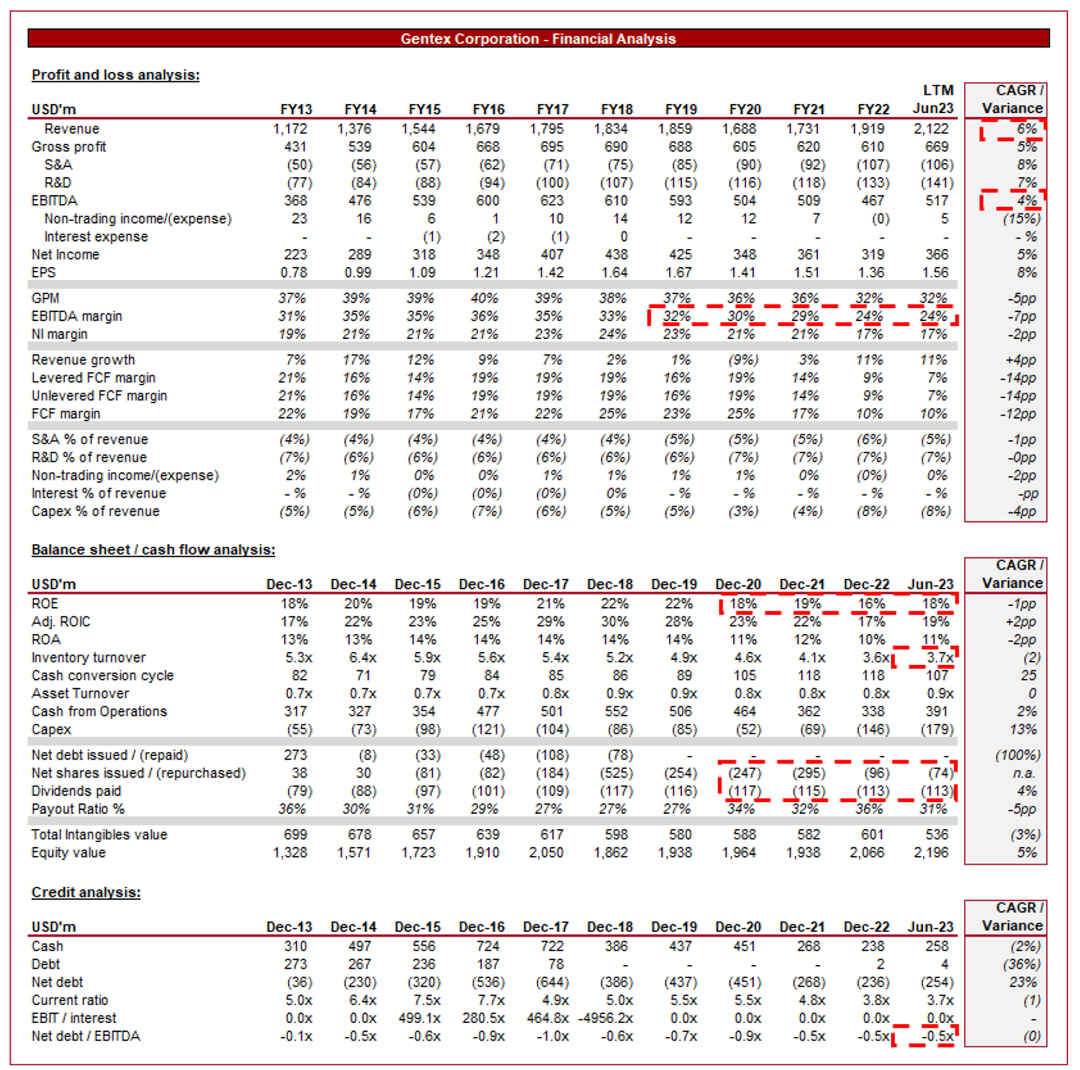

Financial analysis

Gentex financials (Capital IQ)

{kind=link}

Presented above are Gentex's financial results.

Revenue & Commercial Factors

Gentex’s revenue has grown moderately well during the last decade, with a CAGR of 6% and broadly consistent year-on-year gains. EBITDA has trailed these gains, with a noticeable decline in margins post-FY18.

Business Model

Gentex is a technology-oriented company specializing in the design, development, and manufacturing of high-quality products for the automotive, aerospace, and commercial fire protection industries.

A significant portion of Gentex's revenue comes from manufacturing automatic-dimming rearview mirrors for cars. These mirrors utilize electrochromic technology to automatically dim in response to headlights from trailing vehicles, reducing glare for the driver and improving safety. This technology is a major selling point for the company, allowing it to command a premium.

Gentex's mirrors are not just reflective surfaces but integrated with features such as compasses, temperature displays, and rearview cameras. These integrated functionalities add value to its products relative to peers while also appealing to consumers and OEMs who are looking for premium options.

In addition to these core items, Gentex also produces various electronics-based products, including dimmable aircraft windows for the aerospace industry and dimmable glass for architectural applications. It is also involved in manufacturing connected car features, biometric monitoring systems, and other advanced technologies.

We believe the company’s product suite is highly attractive. The company has taken core automotive products, such as mirrors, and innovated them into a market-leading position, contributing to relationships with leading OEMs and the ability to command a premium price. From a downside perspective, its products will always be needed, regardless of trends and changing dynamics (such as EVs). For this reason, credit is owed to the company’s R&D team, with scope for further gains as spending has outstripped Revenue growth.

Component Industry

Given the company’s weighing toward the Automotive segment, our industry analysis will focus on this. The automotive component industry is expected to grow well in the coming years, although will be impacted by various megatrends currently underway. The key driver, as discussed throughout this paper, is the demand from OEMs. For this reason, Gentex is highly reliant on consistently growing production levels.

Gentex faces competition from, and operates alongside, other global component manufacturers, including the likes of Magna International (MGA), Continental AG ( CTTAF ), Autoliv ( ALV ), and Valeo SE ( VLEEF ).

We believe the following factors will be key growth drivers in the coming years:

- Electric Vehicles - The EV transition has the potential to enhance the company’s medium-term performance. With consumers and government legislation encouraging the purchase of new EVs rather than traditional ICE-powered vehicles, the scope for an increase in new vehicle purchases is higher.

- Market Saturation - The automotive mirror market, while stable, could be argued as being saturated on the low end. Many vehicles now come with automatic-dimming mirrors as a standard or optional feature, leaving limited room for exponential growth unless there are significant technological advancements or new market segments created. This limits Gentex’s ability to generate outsized returns or gain significant market share.

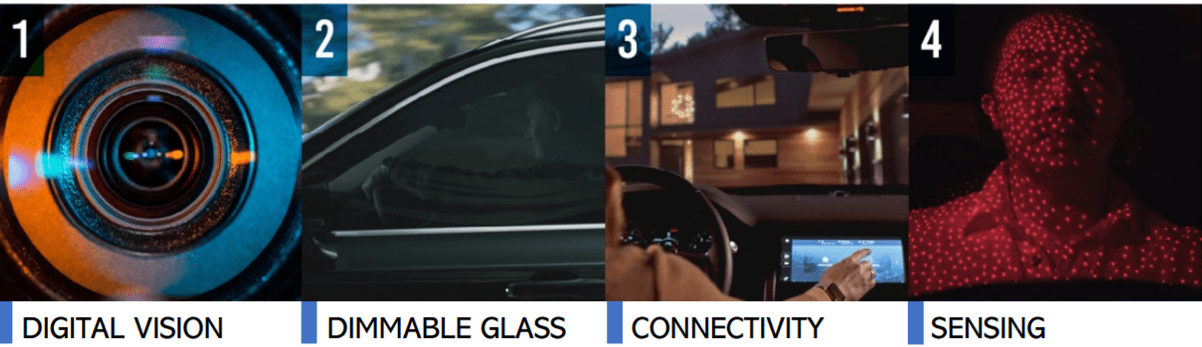

- Technological Advancements - During the last two decades, society has crammed technology into every facet of life, with many “normal”/”traditional” industries utilizing technology to enhance the user experience. This is no different within the parts industry and represents a key opportunity to differentiate products that have historically been basic. Gentex is leaning heavily into this and we consider it critical to the future success of the company.

{kind=link}

- Connected Car Solutions - A key technological development is the “connectivity” of cars. The increasing integration of smart technologies within vehicles has grown, owing to enhanced safety and convenience. Gentex is development services across the spectrum, be it home connectivity or with infrastructure (such as toll payments) and ride-sharing.

- Autonomous Vehicles - In parallel with the EV revolution is the development of autonomous technologies, with the end goal being wholly autonomous vehicles. This is driving demand for advanced vision and sensor technologies, with Gentex well invested within this segment. Importantly, its tech begins with biometrics and driver monitoring (which have a valid use case now), expanding to thermal sensing cameras and in-cabin sensing (which has greater future use cases).

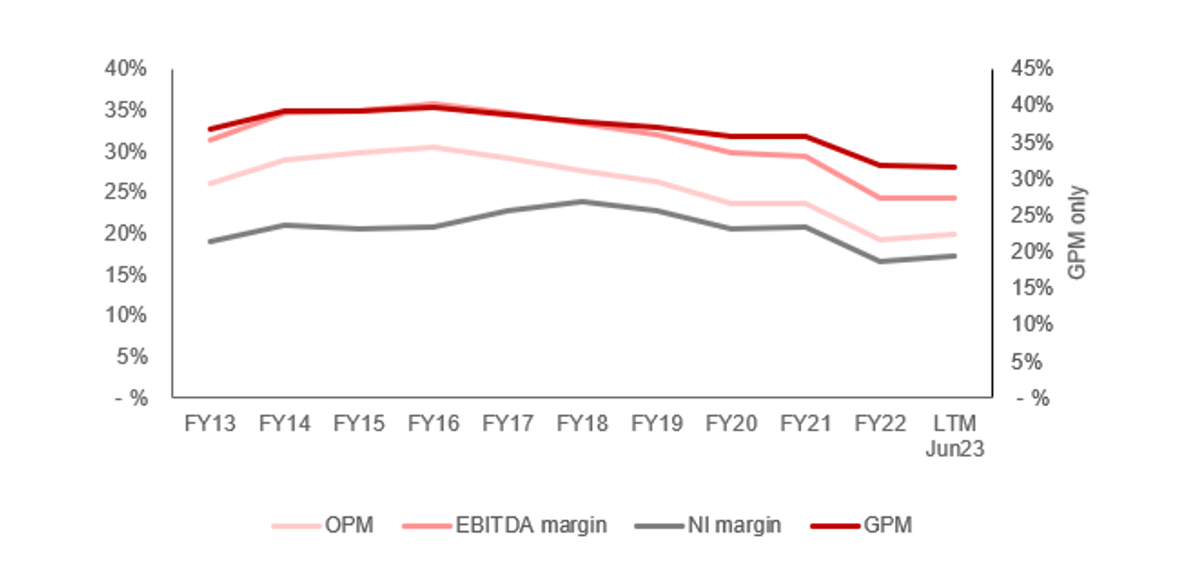

Margins

{kind=link}

Gentex operates with impressive margins, owing to the quality of its products and its position within the market. The company has faced slippage in recent years, some of which is competition-related, Although we predominantly attribute this to macro headwinds. From a competitive perspective, we believe its margins are defensible, owing to the technological capabilities underpinning its products (1,980 patents and 400 trademarks).

Quarterly results

Gentex’s recent performance has been strong, despite the current macro-environment, with top-line growth of +23.5%, +17.6%, +17.6%, and +25.9% in the last 4 quarters. In conjunction with this, margins have slightly improved, contributing to stabilization at an EBITDA-M level.

We attribute this unusual trend to the disruption in the production of vehicles in recent years. When contextualized, the near-term improvement in growth appears reasonable. With supply pressures easing, we are seeing an increase in production, with demand sufficient to maintain a sequential uplift in production. As a result of this, Gentex has benefited from a misalignment from its usual cyclical nature.

{kind=link}

This does imply a rapid slowdown is ahead, as with elevated interest rates and a cost of living crisis across many nations, there is a rapidly declining willingness and ability to purchase new vehicles.

Key takeaways from its most recent quarter are:

- Global light vehicle production (”LVP”) in across key regions increased ~18%, compared to Q2’22, illustrating the significance of the production bounce back.

- Management estimates that Gentex has outperformed its primary market by a staggering 9%, attributing this success to fewer supply chain challenges and the continued demand for its products.

- More specifically, the latter point has benefited from strong penetration rates of its electrochromic technology, as well as the continued success of its Full Display Mirror product line. Finally, Gentex is seeing an improvement in the adoption of other value-add features.

- GPM has increased by 1.1ppt, owing to the significantly higher sales levels, operational improvements in manufacturing, cost recoveries from OEMs, and improvements in freight-related costs and product mix. Management is of the view a GPM of 35-36% can be achieved by the end of next year (implying an EBITDA-M of 28-30%).

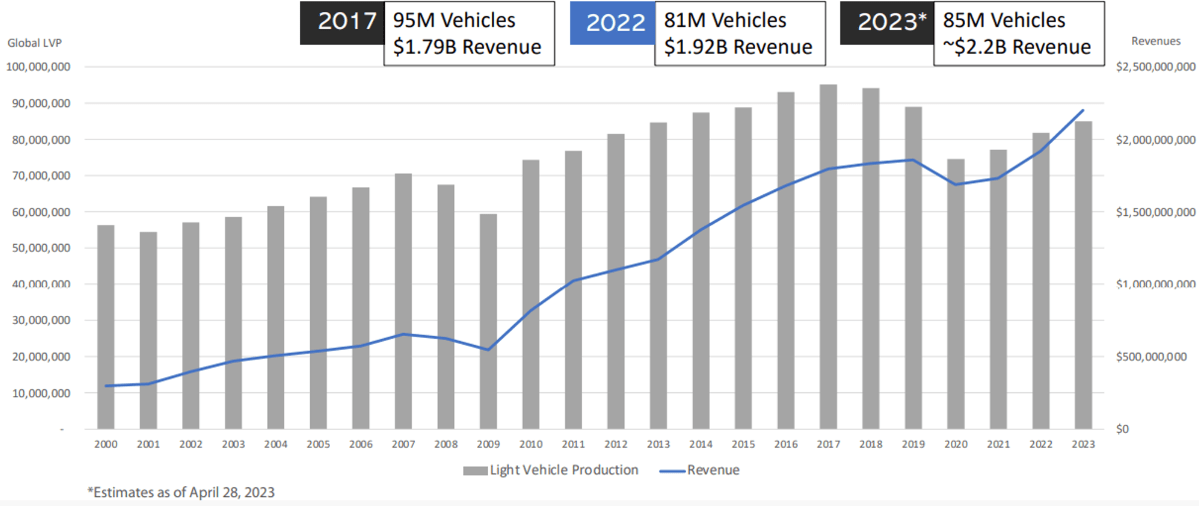

Looking ahead, we suspect growth will rapidly slow in the coming quarters, as the supply chain improvements begin to be offset by current market conditions. The following is S&P’s LVP forecast, which suggests a decline of (3)% relative to Q3’22. Despite this, Management has slightly raised expectations (by c.$100m).

Production (S&P Global Mobility)

{kind=link}

Balance sheet & Cash Flows

Gentex’s balance sheet is relatively clean, although we do see scope for improvement. Its working capital profile has worsened during the decade, with inventory turnover declining. This has compounded the cash flow impact from the decline in profitability, with FCF falling below 15% for the first time in the decade. Although we see imminent improvement, this is a reflection of poor management.

Gentex is conservatively financed, with the avoidance of debt usage. This has allowed the business to incrementally increase dividend payments, with a respectable CAGR of 4%. This said, distributions have declined from their peak between FY17 and FY21 and we are not wholly sold on the scope for near-term improvement.

This has allowed ROE/ROIC to remain attractive despite the worsening margin performance. With the assumption that margins will improve, we suspect returns could again exceed 20%.

{kind=link}

Outlook

{kind=link}

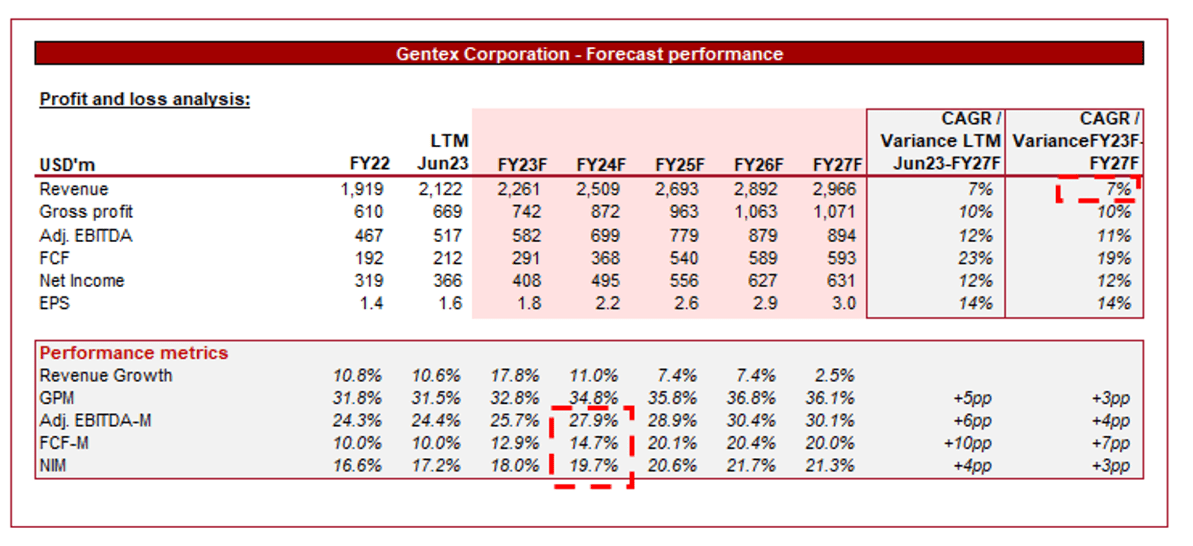

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a continuation of Gentex’s existing trajectory, with a CAGR of 7% into FY27F. In conjunction with this, margins are expected to sequentially improve toward its FY19/FY20 level.

We broadly concur with this assessment. Management has done a good job of transitioning the company’s products in response to the changes faced within the industry. Further, much of its margin deterioration can be attributable to demand and supply conditions, both of which will likely wholly subside by the end of FY24.

Industry analysis

Auto Parts and Equipment Stocks (Seeking Alpha)

{kind=link}

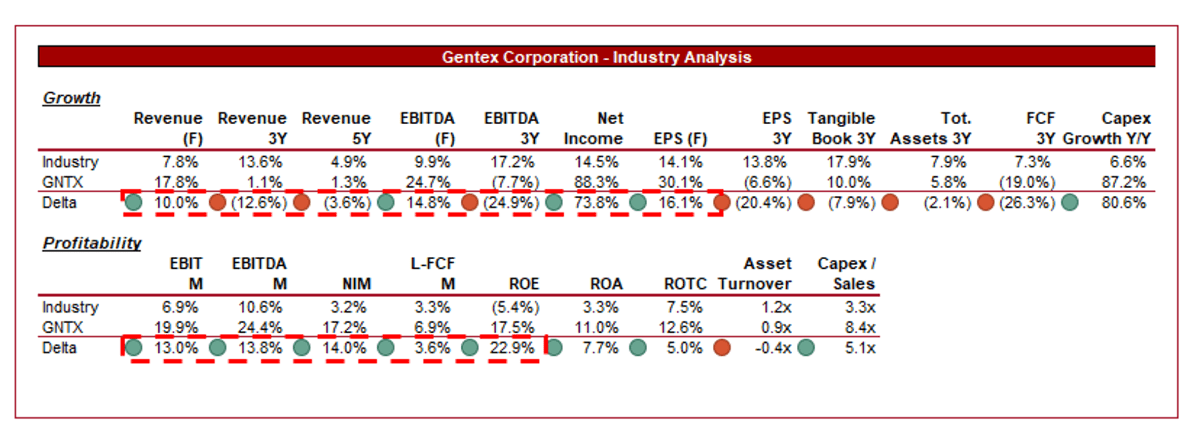

Presented above is a comparison of Gentex's growth and profitability to the average of its industry, as defined by Seeking Alpha (25 companies).

Gentex performs exceptionally well relative to its peers, although does have weaknesses. The company’s growth has materially lagged the industry, both on a 3Y and 5Y basis. We attribute this to its inability to achieve outsized growth in response to the EV trend, as many of its peers have experienced an acceleration. Where Gentex is responding defensively to the EV trend, many of its peers have acted aggressively through the exploitation of new technologies.

Margins are the company’s strong suit. Its leading position within its product segments, efficient global production, and relationships with OEMs allow it to maximize its financial returns. We believe its delta to the industry can be protected, allowing for outsized returns.

With the industry being mature and only benefiting from medium-term headwinds, we have a preference for margins over growth, suggesting Gentex should trade at a premium to its peer group.

Valuation

{kind=link}

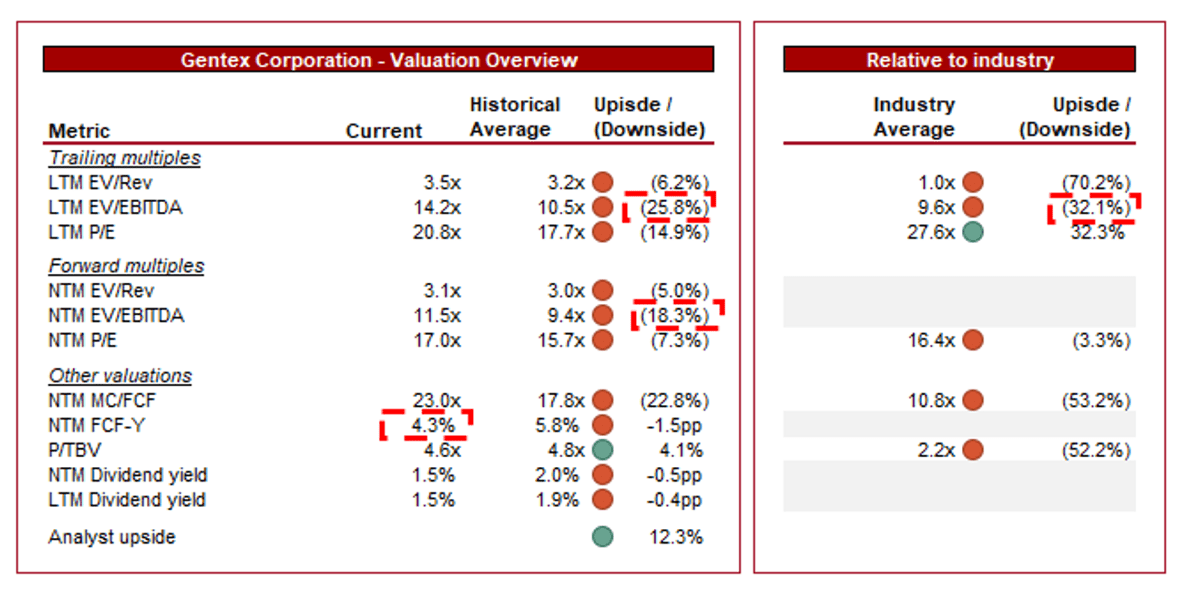

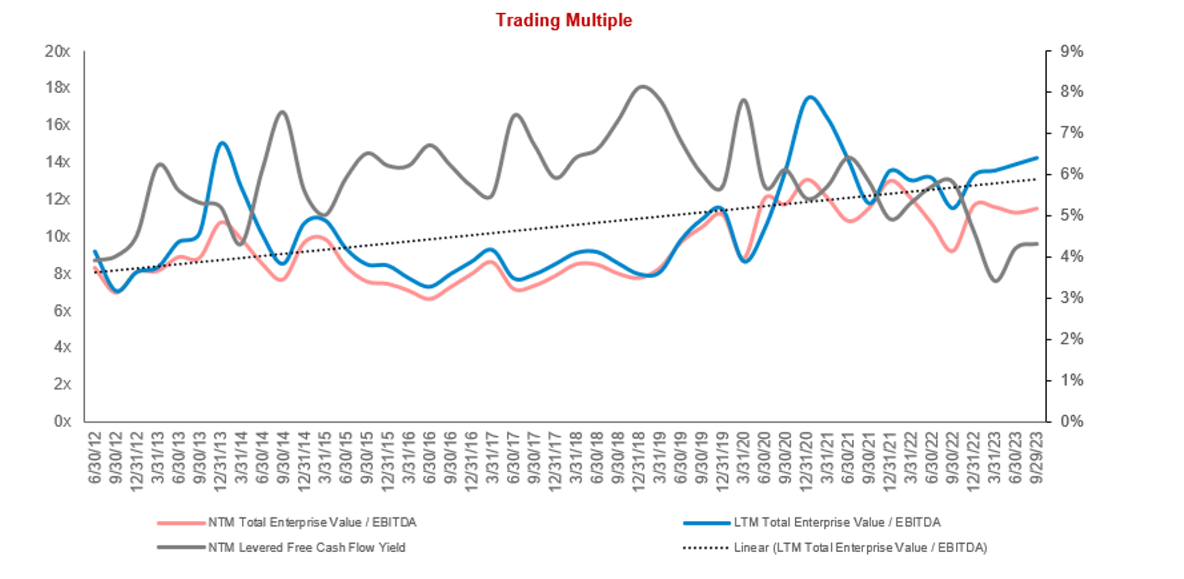

Gentex is currently trading at 14x LTM EBITDA and 12x NTM EBITDA. This is a premium to its historical average.

A small premium to its historical average is justifiable in our view. Although the company’s margins have declined, we have seen positive product development leading to market share growth, an improvement in its technological capabilities, and a reasonable uptick in growth since its “soft” period between FY17 and FY21. This said, we struggle to justify a 15-20% premium, particularly as its NTM FCF yield has declined to below 5%.

Further, the company is also trading at a premium to its peer group, with an LTM EBITDA delta of (32)% and a NTM FCF delta of (53)%. Given its substantial margin superiority, we consider a premium reasonable. This said, we again struggle to rationalize such a high premium.

Overall, we are unconvinced by the potential for an attractive upside at its current share price. As the following graph illustrates, its valuation is trending up, without due warrant relative to profitability we feel.

Valuation evolution (Capital IQ)

{kind=link}

Final thoughts

Gentex is a high-quality business. Through the development of superior products and a long track record of meeting OEM needs, the company has gained a market-leading position in several segments.

There are numerous trends impacting the industry, including embracing technology and the transition to EVs. We believe Gentex is well positioned to achieve healthy growth as a result of this, with its product enhancement efforts showing signs of positive perception. This said, we do think the company will face issues in the near term, owing to the slowing production of LVs.

With the company trading at a large premium to its historical average and peer group, we struggle to rationalize its current valuation, particularly due to the risk of performance declining and a lack of improvement in distributions

For further details see:

Gentex Corporation: Technology Driven Innovation Widening Its Moat