AZO - Genuine Parts Company: Good Growth Prospects

2023-04-17 14:34:40 ET

Summary

- Revenue growth should benefit from healthy demand for replacement products and services, global footprint expansion, and M&A strategy.

- Margin should benefit tech investments to efficiently manage the supply chain, price increases, and moderating inflation.

- Valuation is reasonable.

Investment Thesis

Genuine Parts Company ( GPC ) is expected to benefit from good demand for replacement products and services due to an increase in miles driven resulting from economic reopening and moderating fuel prices. Additionally, the average age of the vehicle fleet is increasing, which should further drive the demand for replacement parts. Revenue growth is also expected to benefit from global footprint expansion and acquisition synergies, in addition to good demand and healthy end markets.

With the help of its IT investments to efficiently manage supply chains and pricing, and moderating inflation, the company is likely to deliver margin growth. I like the company's prospects and it is also trading at reasonable valuations. Hence, I believe GPC stock is a buy.

Revenue Outlook

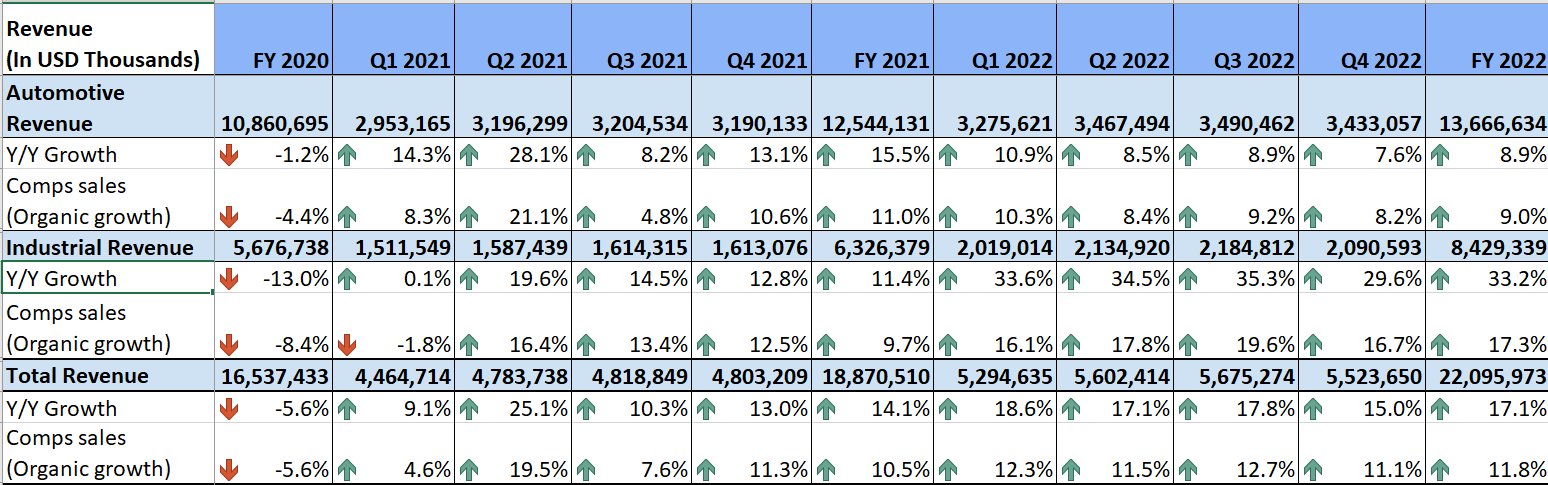

Genuine Parts Company experienced an acceleration in sales growth post-pandemic due to strong demand for replacement products in both the Automotive and Industrial segments. This resulted in the company gaining a good market share over the past couple of years. In the fourth quarter of 2022, the company's sales growth momentum continued. The demand for automotive replacement parts due to an aging vehicle fleet contributed to the company's sales growth. Additionally, the acquisition of Kaman Distribution Group (KDG) in early January 2022 also helped boost the company's revenue. As a result, the company saw a 15% year-over-year increase in revenue to $5.5 billion, with acquisitions accounting for an 8 percentage point benefit and a 4 percentage point foreign exchange headwind.

GPC’s Historical Net Sales (Company Data, GS Analytics Research)

{kind=link}

Looking ahead, I anticipate that Genuine Parts Company should be able to achieve revenue growth benefiting from strong demand for replacement products, the expansion of the company's global footprint, and its M&A strategy.

Following the pandemic, people have started driving more vehicles as offices and schools rapidly reopened and travel restrictions continue to ease. This has led to an increase in vehicle miles driven. Additionally, fuel prices are moderating from their peak levels, which is further contributing to the increase in miles driven. As a result, there is a strong demand for replacement products. Furthermore, the average age of vehicles in use has increased due to lower new car inventory which should drive up the maintenance needs.

During times of economic slowdown, people tend to hold on to old products for longer, which increases the demand for repair and replacement products and services. As a result, GPC's Automotive segment is somewhat countercyclical in nature and should be able to remain resilient even in a weakening economy. I expect demand to remain strong in the coming year, and the Automotive business to deliver good revenue growth.

Additionally, GPC is consistently gaining market share. The company's efforts to expand its global footprint are paying off, particularly in Europe, which accounts for 14% of total GPC sales. The rollout of GPC's National Automotive Parts Association ((NAPA)) brand in Europe has resulted in the company winning business with numerous key customer accounts, leading to NAPA product sales of ~EUR300 million in 2022, with an annual increase of 50%. The company has also expanded its Automotive business in Spain and Portugal, further increasing its global footprint, and added 138 new stores across Europe and the U.S. These efforts should lead to further market share gains and contribute to top-line growth.

Genuine Parts Company Addressable Market (Genuine Parts Company Investor Presentation November 2022)

GPC's Industrial segment is also experiencing strong demand from its end markets, such as oil and gas, automation, semiconductors, fluid power, and cement, which are expected to remain healthy. The segment should also benefit from its expanding capabilities in industrial solution offerings, such as automation, fluid power, and conveyance, thanks to its acquisition of Kaman Distribution Group (KDG) in January 2022. KDG is a market-leading business that offers products and services in power transmission, bearings, automation, and fluid power industrial solutions. This acquisition has strengthened GPC's Industrial segment and added ~16.8 percentage points to Industrial revenue growth in 2022. In addition to KDG, the company has also added small bolt-on acquisitions in the Automotive segment to further increase its market share. GPC's balance sheet is healthy, with a leverage ratio of 1.7x (below its target range of 2x-2.5x). This provides the company with the flexibility to continue its M&A strategy and support revenue growth in the future.

Furthermore, GPC's Industrial segment should also benefit from the onshoring of manufacturing in the U.S. to address supply chain challenges. For this purpose, there are many government incentives like CHIPS and Science Act which are catalyzing investments in end-markets such as semiconductors, energy, battery storage, and mining. The company believes that its product and service offerings in automation and robotics should benefit from this reshoring and onshoring of manufacturing activities, as automation is expected to play a major role in meeting labor challenges. This creates a good long-term tailwind for the company's Industrial business.

Management has guided for a sales growth of 4-6% in the current year, which does not include any potential M&A. While the guidance reflects some normalization of revenue growth after a strong couple of years, I like the company's longer-term growth prospects and the resilient nature of repair and replacement products.

Margin Outlook

GPC has successfully maintained its margin levels despite inflationary pressures in recent years, thanks to its effective supply chain management and cost-saving measures. The company was able to cut costs by $400 million during the pandemic period. In the fourth quarter of 2022, GPC achieved margin expansion through a combination of cost savings and price increases. Although these were partially offset by supplier incentive costs, unfavorable mix shifts, higher freight costs, and FX headwinds, the company still managed to increase gross margin by 50 bps YoY to 35.7%, while total segment profit margin increased by 80 bps YoY to 9.5%.

GPC’s Historical Gross Margin and Total Segment Profit Margin (Company Data, GS Analytics Research)

Looking ahead, I believe that GPC should be able to expand its margins in the coming year. The company's investment in technology to enhance its back-office processes should help increase its profitability and deliver margin growth. GPC is adopting data analytics, artificial intelligence ((AI)), and cloud-based systems to pivot toward modern technology platforms. This investment is leading to productivity improvements by modernizing and automating its distribution centres, ensuring that GPC's products and services are available at the right time and in the right supply network. Moreover, these technological investments are also helping the company efficiently manage its pricing actions to offset inflationary pressure. Therefore, I expect these investments to continue to help GPC expand its margins in 2023.

Management has guided for a 20-40 bps improvement in gross margin for 2023 which looks achievable.

Valuation and Conclusion

GPC will report its Q1 earnings on April 20th and I am expecting upbeat commentary despite macroeconomic concerns due to the reasons discussed above. The stock is currently trading at ~18.50x FY23 consensus estimate which is in line with its historical 5-year average forward P/E of 18.56x and at a discount with its peers like O’Reilly ( ORLY ) trading at 24.19x FY23 consensus EPS estimate and AutoZone ( AZO ) trading at 20.43x FY23 consensus EPS estimates. Given the broader macroeconomic environment, I am not expecting any re-rating of the P/E multiple. But even if we assume the forward P/E multiple to remain constant at 18.50x, a $9.62 consensus EPS estimate for FY24 means that the stock can reach ~$178 by the end of this year (or ~7.8% upside.) This coupled with ~2.30% current annual dividend yield should result in over 10% total return (including dividends) over the next year which is reasonably attractive. Hence, I believe the stock is a buy at the current levels.

For further details see:

Genuine Parts Company: Good Growth Prospects