GEO - GEO Group: Solid Fundamentals And Extremely Cheap

2023-07-19 15:55:17 ET

Summary

- GEO stock has underperformed significantly over the last decade, with shares falling more than 68% since 2013.

- The underperformance can be attributed to Biden Administration's executive order to stop renewing contracts with privately-operated, for-profit prisons, Title 42, their transition into a C-Corp, and the rise in interest rates.

- The business is operating great and GEO management is currently focused on reducing the company's debt.

- We believe the stock is trading at very compressed multiples and the current price represents a great risk-reward opportunity.

Investment Thesis

The GEO Group ( GEO ) owns, leases, and manages correctional, detention, and re-entry facilities mainly in the US but also in South Africa, Australia, and the UK. The stock has underperformed by a wide margin over the last 10 years and is trading at levels not seen since the Great Financial Crisis. However, we believe that the worst is past us and the future prospects of the company are brighter: Title 42 is expiring, they are deleveraging their balance sheet and the valuation is very attractive. We like the risk-reward ratio at current prices and bought some shares.

How We Got Here

We think the underperformance of GEO can be explained because of a few reasons.

The first one is obviously COVID, which reduced the level of immigration drastically. Besides, in March 2020 the Trump Administration invoked Title 42 , which allows US authorities to swiftly remove migrants crossing the border from Mexico - including asylum seekers - using the pandemic as justification. This correlated with empty facilities, and although in the short term, GEO still receives fees for 90-80% of beds even if only 40% are occupied, in the long term low detainee populations will hurt GEO because ICE will likely be reluctant to pay high minimum occupancy rates.

Secondly is the executive order issued by the Biden Administration in early 2021 directing the Department of Justice to discontinue renewing contracts with privately-operated, for-profit prisons. The Justice Department includes the Bureau of Prisons and U.S. Marshals Services. This makes up roughly 25% of Geo Group's revenue. However, so far they have been able to dodge the bullet by turning the detention centers into ICE facilities, and local governments have taken federal funds to manage prisons and then just turned around and given them to private prison operators.

Another reason is the fact that the company transitioned from a REIT into a C-Corp effective at the end of 2021. As a REIT, GEO was obligated to pay at least 90% of its earnings as dividends. But given the increasing amount of debt, the company had to deleverage the balance sheet, and the change to a C-Corp provided more earnings flexibility. They decided to cut the dividend to focus on debt repayment, which caused dividend investors to dump the stock.

Lastly is the rise in interest rates. Because GEO is an asset-intensive business, they rely on a lot of external financing. As a result of the high debt incurred during these past years, interest expense skyrocketed in the past quarters and is affecting the net income significantly.

Despite all of this, as we will see, the operating results of GEO have been quite strong.

Financial Results

GEO reported Q1 2023 financial results on April 25. Revenue came in at $608.2 million, a 10.3% increase YoY. This growth can be entirely attributed to the Electronic Monitoring and Supervision Services segment, which grew revenue more than 50% YoY. This segment provides technology such as ankle monitors for those on parole, probation, and in the immigration process. Because of the high-margin nature of this segment, the operating margin of the group as a whole has risen significantly over the last years, reaching a high of 16.2%.

As you can see, the operational performance of GEO is very strong. However, as we previously discussed, the main problem the company has is the level of debt it carries on its balance sheet. Because of this, interest expense rose from $31.6 million in Q1 2022 to $54.2 million in Q1 2023. This significantly affected net income, which decreased 26.7% YoY to $28 million. Despite this, EBITDA increased 6.3% YoY to $125.6 million.

The company expects 2023 revenue to be in the range of $2.38-$2.46 billion, which would represent a 1.8% growth year over year. We think this is a conservative estimate that doesn't take into account any benefits from the expiration of Title 42. This may have to do with the fact that right after the expiration of Title 42, immigration volume declined sharply . We think any positive development with this can positively impact the guidance and push the stock higher.

Balance Sheet

As of Q1 2023, GEO had $110.9 million in cash and equivalent and more than $1.9 billion in total debt. However, they paid down a significant portion of their obligations since becoming a C-Corp.

The goal of management is to reduce debt to 3.5x EBITDA by the end of 2023 and to 3x EBITDA by the end of 2024. They estimate total debt outstanding will be between $1.815 billion and $1.775 billion at the end of the year, which would mean a $120 million reduction from Q1. Considering that they repaid $70 million in Q1, it wouldn't be surprising that they can repay debt more rapidly than anticipated.

Deleveraging the balance sheet is crucial because it would lower interest expenses and allow management to return capital to shareholders. And frankly, given the high interest rate they paid (+12%) we would rather they repay debt as fast as possible rather than distribute dividends or repurchase shares.

Valuation

What makes the stock very appealing is the current valuation. The stock's EV/EBITDA of 5.15X is almost the lowest multiple GEO has ever traded at.

The company is also trading near its all-time P/E ratio low, which currently is at 6.4x. Given the high level of depreciation and amortization GEO incurs, if we measure the price dividend by AFFO per share ($2.76) we arrived at a multiple of 2.5x, which is low enough to provide a margin of safety for investors in our view.

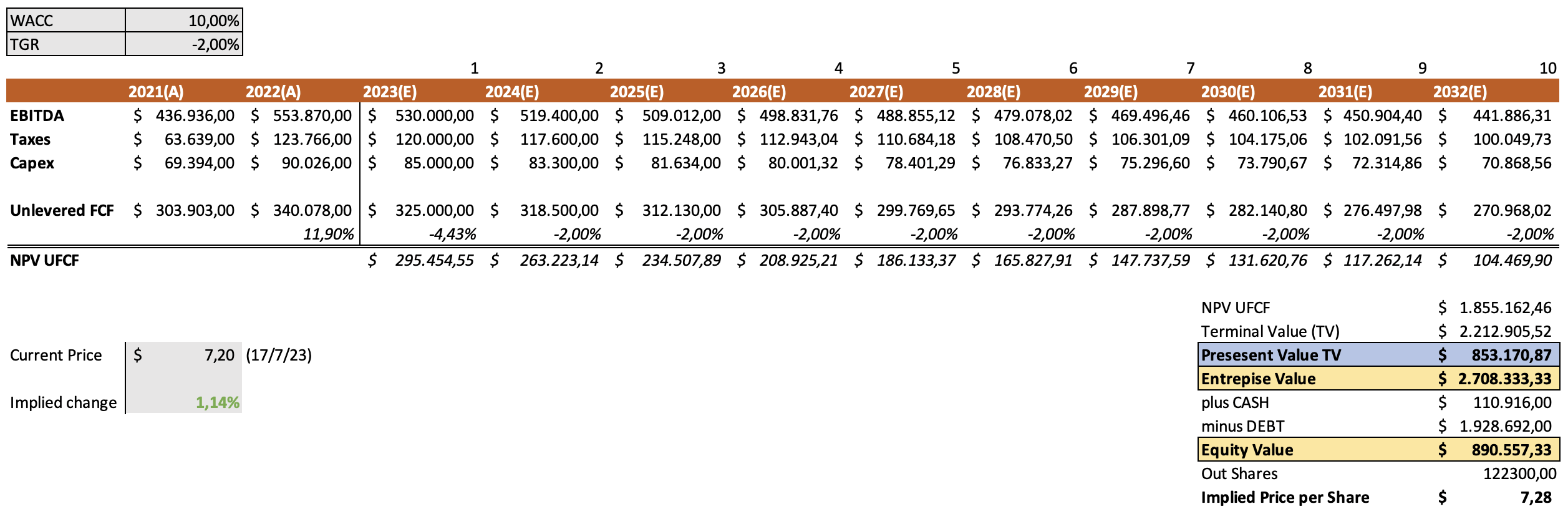

It is also not very demanding to justify the current valuation by doing a DCF model. We assumed that EBITDA would be $530 million in 2023 and decline by 2% annually in perpetuity, with taxes and maintenance capex requirements following this trend. We assumed a WACC of 10%.

{kind=link}

With these assumptions, we arrived at the conclusion that shares are fairly valued, but the model doesn't take into account any growth that the expiration of Title 42 or the Electronic Monitoring and Supervision Services segment may provide. A slightly more bullish DCF can easily give an implied price per share of +$10.

Takeaway

To sum up, GEO operations are in great shape and the company is taking on its debt. What we like the most about the stock is its price. We think investors are pricing the "worst-case scenario" when things are actually better than feared. Also, we should consider that many of the problems the company faces can potentially be "solved" if a Republican president gains the election next year. Overall, we believe there is a great risk-reward ratio at current ratios.

For further details see:

GEO Group: Solid Fundamentals And Extremely Cheap