GEO - GEO Group: Taking To 'Strong Buy' After Title 42 Expiration

2023-05-16 09:39:11 ET

Summary

- GEO posted mixed results for Q1, as higher interest rates weighed on its bottom line.

- Any impact from Title 42 expiration is not currently in guidance in my view, and represents a nice upside.

- GEO has the potential to beat estimates and see multiple expansions, setting up a very nice opportunity in the stock.

I placed a "Buy" rating on The GEO Group ( GEO ) in early March. The company recently reported its Q1 results, while Title 42 also just recently expired. Let's take a closer look at its Q1 earnings and the implications of Title 42 expiring.

Q1 Earnings

For the quarter, GEO posted a 10% increase in revenue to $608.2 million. That was ahead of the $606.1 million consensus .

Owned and Leased Secure Service revenue climbed 4% to $277.1 million, while the net operating income was $75.9 million, down -11%. Owned and Leased Reentry Service revenue rose 3% to $39.4 million, while its NOI also rose 3% to $12.0 million.

Managed Only revenue slipped -1% to $133.8 million, while its NOI plunged -40% to $13.6 million. Electronic Monitoring and Supervision Service revenue zoomed 51% higher to $132.6 million, while its NOI rocketed 56% higher. Non-residential service revenue rose 12% to $25.3 million, while its NOI jumped 33% to $5.1 million.

Adjusted EBITDA rose 5% to $130.9 million. Adjusted EPS came in at 22 cents versus 31 cents a year earlier, as high interest rates weighed on the bottom line. Interest expense more than doubled from $26 million to $53.2 million.

{kind=link}

It was a bit of a mixed quarter from GEO. Its Electronic Monitoring program is doing very well, while other areas struggled a bit. High interest rates have also weighed on its bottom-line results givens its variable rate debt.

Outlook

Looking ahead, GEO guided for Q2 revenue of between $585-590 million. Analysts were looking for Q2 revenue of $611.3 million.

The company forecast adjusted EBITDA to be between $124-129 million. It is looking for Q2 net income of between $24-26 million.

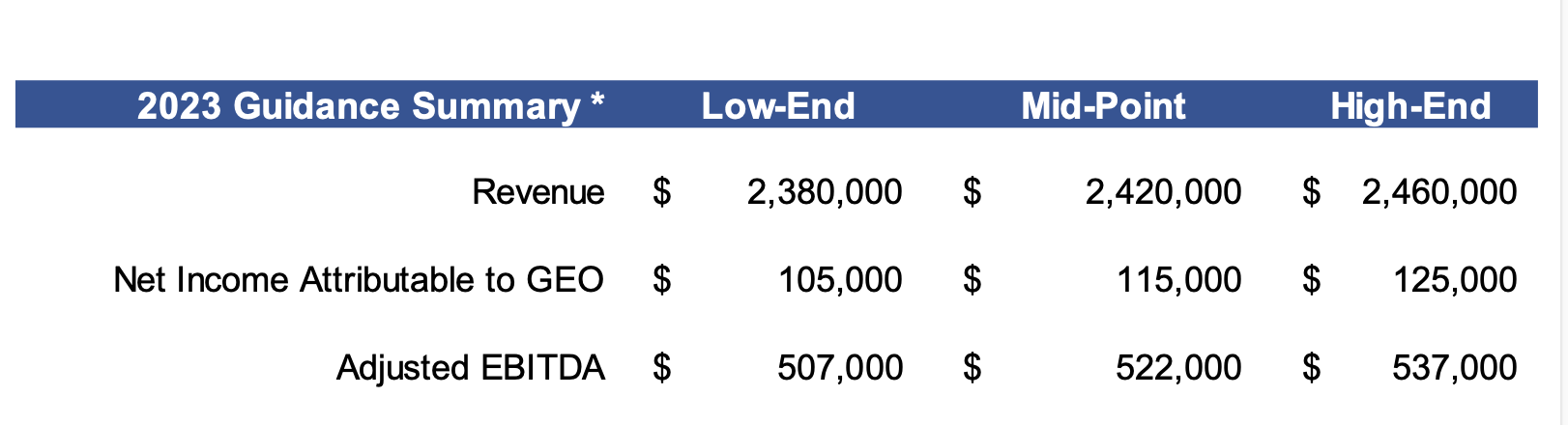

For the full year, GEO narrowed its revenue guidance to be between $2.38- $2.46 billion compared to prior guidance of $2.37-2.47 billion. The analyst consensus was for revenue of $2.46 billion.

The company is looking for adjusted EBITDA of between $507-537 million versus a previous forecast of $500-540 million. The new guidance is an increase of $2 million at the mid-point. It's looking for net income of between $105-125 million, compared to prior guidance of $100-$127 million. The new guidance is an increase of $1.5 million at the mid-point.

{kind=link}

Discussing its guidance of its Q1 earnings call, George Zoley said:

With the reactivation of our Great Plains Facility, we now have approximately 9,000 idle owned beds in our Secure Services segment, primarily comprised of 5 former Bureau of Prisons facilities. We continue to actively market these modern and well-located facilities to government agencies at the state and federal level. And the reactivation of any of these 5 idle facilities could represent significant upside to our current forecast. In addition, the scheduled expiration of Title 42 restrictions at the Southwest border could provide upside to our current forecast. Since March of 2020, Title 42 has allowed the federal government to immediately remove a significant portion of individuals encountered by Border Patrol illegally entering into the United States. Because these restrictions at the Southwest border were implemented under the COVID public health emergency declaration, Title 42 is scheduled to end on May 11, 2023, to coincide with the expiration of the public health emergency declaration.

When Title 42 expires on May 11, it is expected that the federal government will likely have to process a significantly larger proportion of individuals encountered by Border Patrol. It is also widely expected that the expiration of Title 42 may result in an increase in Border Patrol encounters at the Southwest border at a time when there is already an unusual seasonal increase in border activity due to the warmer weather in the summer. While these circumstances could recently result in higher counts in the ISAP program in higher ICE processing center populations, these factors would be policy decisions that our company plays no role in setting and which are difficult to fully estimate. … With respect to our guidance, our outlook for 2023 assumes a lower average count in ISAP participants under technology supervision compared to 2022, and the utilization rates at our ICE processing centers will remain below historic levels. At this time, we have not included any assumptions regarding the expiration of Title 42 in our financial guidance. Should the expiration of Title 42 result in increased border activity and higher ISAP participant counts, those trends would result in an upside to our current financial guidance. Similarly, if the expiration of Title 42 were to result in higher occupancy rates at ICE processing centers, this would also represent upside to our current guidance."

Overall, it looks like GEO was very conservative with its guidance due to concerns over government budgetary issues and building in a continued decline in the ISAP program in Q2, even though it has shown some signs of stabilizing. At the same time, no benefit of the expiration of Title 42 has been placed in its guidance, and that did indeed expire on May 11th after the company's earnings call.

So far, there has been an increase in illegal border crossings just prior to and since the expiration of Title 42. Border control is still preparing for an increase of daily migrants to 12,000-14,000 from a recent average of 2,700 and many detention facilities are already over-crowded. In addition, there were an estimated 60,000 migrants waiting near the U.S.-Mexico border ahead of the expiration. While news headlines may have played down the increase in border crossings, it is happening and it should benefit a company like GEO.

Valuation

GEO trades at a 5.6x EV/EBITDA multiple based on the 2023 EBITDA consensus of $524.6 million (down from $531.5 million when I last looked at it). Based off of the 2024 EBITDA consensus of $551.2 million (was $555.2 million last time I looked at it), it trades at around 5.4x.

It trades at 9.2x forward EPS, with analysts projecting 2023 EPS of 94 cents (down from 99 cents when I last looked at it).

It's projected to grow revenue 2.3% in 2023, accelerating to 4.2% growth in 2024.

Conclusion

I really like the set-up for GEO currently. The bar has been lowered, while at the same time the potential positive impact from the expiration of Title 42 is not in the company's numbers. The stock also hasn't really moved due to the expiration of Title 42.

The company also recently won a deal in Oklahoma to use a facility that was previously idle, taking business away from rival CoreCivic (CXW). It has other idle facilities that if re-activated would add potential upside as well.

While not without political risks, GEO stock should be able to both outperform its current forecast and see multiple expansion now that the Title 42 border restrictions are lifted. I'm taking my rating from "Buy" to "Strong Buy."

For further details see:

GEO Group: Taking To 'Strong Buy' After Title 42 Expiration