GEO - GEO Group: The High Short Interest Does Not Make A Lot Of Sense

2023-03-07 14:47:34 ET

Summary

- GEO Group is heavily shorted, whereas its rival CoreCivic is not, despite trading at a premium to Geo.

- GEO has successfully navigated the political risk by reinventing its business model.

- Geo's strengthening relationship with ICE, recent border encounter statistics, and the success of ICE's ATD program tell an interesting story.

- Results from a conservatively built DCF model reveal GEO is not fairly valued in the market.

When President Biden took office, the private prison industry braced for impact with his promise to eliminate private prisons, starting from not awarding any new contracts to private prison giants such as The GEO Group, Inc. (GEO) and CoreCivic, Inc. (CXW). At the time, the drop in GEO stock seemed reasonable given that the new administration vowed to target facilities that fall under the Department of Justice and the U.S. Marshals Service, which, according to our previous analysis , accounted for approximately 25% of Geo's revenue in 2020. Using an asset-based approach to estimate Geo's intrinsic value in late 2021, we concluded that Geo, even in the worst-case scenario, should be valued at $8.91 per share. After a volatile 12 months in which GEO stock traded as low as $5.20 and as high as $12.44, GEO has now settled closer to our estimated worst-case-scenario pricing.

Given that the company has made steady progress to mitigate the impact of President Biden's Executive Order while expanding into new business verticals, I believe it would be unfair to value GEO using a worst-case-scenario approach anymore. I was also surprised to notice Geo's short interest (short volume as a percentage of float) of 23% in comparison to CoreCivic's short interest of just 2.5%, which makes GEO one of the most shorted stocks in the market today. After revisiting Geo's prospects and the recent progress, I am convinced that the massive short interest does not make a lot of sense and that the company needs a valuation upgrade.

Navigating Political Risks Successfully

At the time of Biden's Executive Order prohibiting new contracts for private prison companies, GEO generated more than half of its revenue from ICE contracts and state contracts. President Biden, in his campaign, pledged to introduce reforms that cover immigrant detention centers as well, but in practice, this has not happened still. The below excerpt was taken from President Biden's campaign website .

Biden will end the federal government's use of private prisons, building off an Obama-Biden Administration's policy rescinded by the Trump Administration. And, he will make clear that the federal government should not use private facilities for any detention, including detention of undocumented immigrants. Biden will also make eliminating private prisons and all other methods of profiteering off of incarceration - including diversion programs, commercial bail, and electronic monitoring - a requirement for his new state and local prevention grant program.

As new regulatory restrictions do not cover ICE detention centers, GEO was quick to strike new deals with ICE to make use of its infrastructure. For example, the Moshannon Valley Correctional Center, which was closed in March 2021, was reopened as an immigration detention center after signing a contract with ICE.

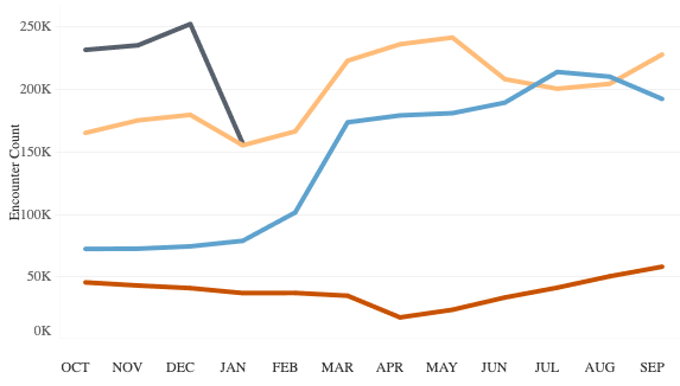

After President Biden assumed duties, the number of immigrants booked into detention facilities rose sharply from around 10,000 per month to over 30,000 per month but declined to a modest 17,559 last December. As of January 1, 2023, there were 20,506 immigrants in ICE detention facilities, and the number has consistently remained above the 20K mark for many months. As the below chart illustrates, border crossing encounters in the Southwest were substantially higher in 2021 and 2022 compared to 2020, which is one of the main reasons behind the high occupancy levels seen at ICE detention facilities.

Exhibit 1: Southwest land border encounters by month (fiscal years)

{kind=link}

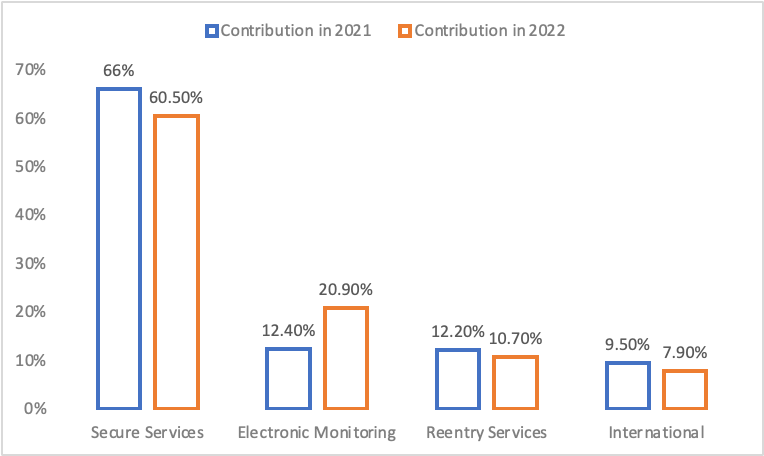

In a commendable move, GEO prioritized its Electronic Monitoring and Supervision Services business, which saw stellar growth in 2022. As illustrated below, this business segment contributed around 21% of company revenue in 2022 and registered YoY growth of 77.9%, more than offsetting the negative impact of revenue declines in all other business segments.

Exhibit 2: Revenue contribution by segment

{kind=link}

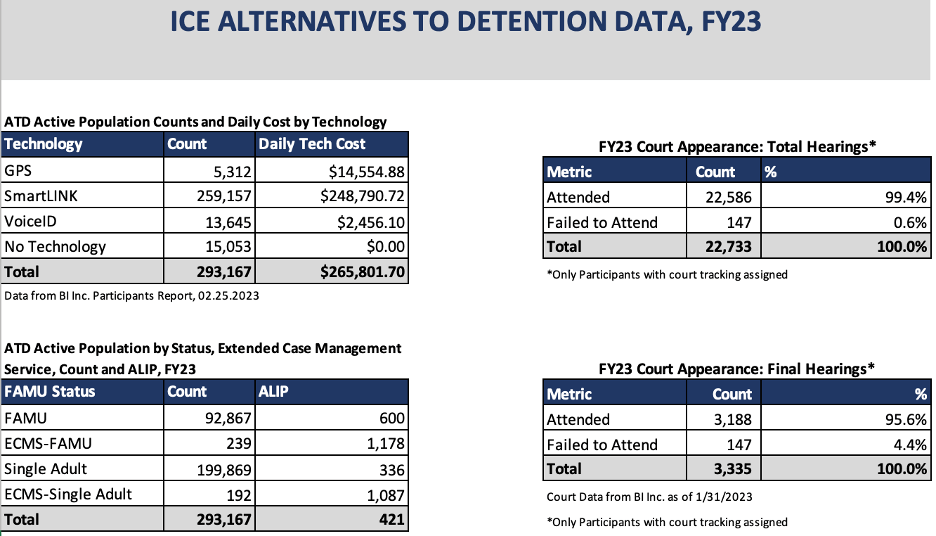

The rapid growth of ICE's Alternatives to Detention program (ATD) has been a tailwind for Geo's electronic monitoring business. According to data published by ICE, there were 293,167 immigrants enrolled in the Alternatives to Detention program at the end of fiscal 2023 (the federal government's fiscal year ends on September 30). In comparison, the ATD program had less than 135,000 participants in October 2021, which highlights the exponential growth of this program.

Exhibit 3: ATD program statistics

{kind=link}

Geo's electronic monitoring devices include GPS-enabled watches to monitor program participants in real-time, radio frequency monitoring systems, alcohol monitoring systems, mobile apps, and web-based software platforms for government agencies. These products are likely to remain in high demand in the coming years as ICE rolls out new initiatives to promote its ATD program.

Appealing Valuation

When my colleague and I built our valuation model for GEO back in 2021, the idea was to estimate a worst-case-scenario value for GEO stock given that there was a lot of uncertainty about the company's future. There is still a lot of uncertainty today but I believe a valuation upgrade is warranted given that GEO has successfully reduced the exposure to high-risk contracts with the federal government, strengthened its relationship with ICE, and diversified into new business segments. For these reasons, I thought it best to use a discounted cash flow model with conservative assumptions to determine the intrinsic value of the company.

Wall Street analysts expect Geo's revenue to grow over 3% in each of the next two fiscal years, but in my updated model, I only expect revenue to grow by just 100 basis points in each of the next five years. I expect the electronic monitoring business to register double-digit growth in the forecast period but these gains are to be nearly offset by declining revenue in its core business. I was tempted to model slightly better growth projections for the next couple of years at least, but I still wanted to be on the safe side with GEO given that the company's fortunes are closely tied to regulatory decisions. Below are my revenue projections.

| Fiscal year |

| Projected revenue |

| Implied YoY growth rate |

| 2023 |

| $2.4 billion |

| 1% |

| 2024 |

| $2.42 billion |

| 1% |

| 2025 |

| $2.44 billion |

| 1% |

| 2026 |

| $2.47 billion |

| 1% |

| 2027 |

| $2.5 billion |

| 1% |

Source: Author's estimates

Below are some of the other important assumptions used in my model.

- Average EBITDA margin of 21.5%.

- Capital expenditures to average around 3% of revenue.

- An average tax rate of 27%.

- A cost of capital of 12.5%.

- Perpetual growth of 2.2%.

I believe GEO deserves a much higher perpetual growth rate assuming the company will survive the next five years. It would have been reasonable, in my opinion, to assign a perpetual growth rate closer to 3% but again, I wanted to be cautious with my estimates. Using these assumptions, Geo's intrinsic value estimate comes to $10.24 per share, which implies an upside of close to 16% from the current market price.

Even from a relative valuation perspective, GEO seems attractively priced. CoreCivic is valued at a forward P/E of 16.59 whereas GEO is valued at a modest P/E of below 9.0. From a cash flow perspective, GEO is valued at 5.7 times the expected EBITDA next year in comparison to CoreCivic which is valued at over 7.5 times the expected EBITDA next year.

Takeaway

In the last couple of years GEO has successfully navigated political risk by introducing several strategic changes to its business model. The electronic monitoring business is delivering much-needed growth at a time when its core business is beginning to stabilize aided by the company's ongoing relationship with ICE. GEO is heavily shorted whereas its main competitor CoreCivic has not attracted short traders despite being valued at a premium to Geo. This valuation disparity between the two private prison giants has created a good opportunity for investors, and the results of a conservatively built DCF model confirm GEO is not fairly valued in the market today. Investing in Geo, however, is not for everyone because of the substantial risks associated with the company.

For further details see:

GEO Group: The High Short Interest Does Not Make A Lot Of Sense