GEO - GEO Group: The Opportunity Is Still Big

2023-11-08 02:21:30 ET

Summary

- Q3 financial results show a decrease in revenue and operating income, but progress in reducing debt and strengthening the financial position.

- The potential passing of bill H.R. 4367 could significantly benefit GEO Group, as they currently hold a monopoly in this market.

- Politicians will have to tackle illegal immigration issues sooner rather than later, and we believe GEO is uniquely positioned to benefit from it.

Investment Thesis

In our previous write-up of GEO Group ( GEO ), we argued that the company was performing well while reducing its debt, trading at attractive multiples, and facing several catalysts that could propel the stock higher.

Since then, the stock has been up 30% and the catalysts are starting to appear. After going through their Q3 results, we believe that the future of GEO is even brighter than it was before, and we remain bullish on the stock.

Q3 Financial Results

GEO reported its Q3 financial results on November 7. Revenue came in at $602.8 million, compared to $616.7 million for the third quarter of 2022, representing a decrease of 2.2%. The revenue for the Electronic Monitoring and Supervision Services segment declined by 29.5% year-over-year. We will discuss this in more detail later.

Operating income was $83.6 million, a decrease from $98 million one year ago. This decline is attributed to the decrease in revenue from the Electronic Monitoring and Supervision Services segment, which maintains an approximately 50% operating margin. The operating margin of the group was 13.87%, compared to 15.91% a year ago.

Furthermore, the results for the third quarter of 2023 reflect a year-over-year increase of $13.3 million in net interest expense due to completed transactions aimed at addressing the substantial majority of their outstanding debt and were also impacted by higher interest rates. Net interest expense was $54.4 million compared to $41.1 million a year ago. Provision for income taxes amounted to $6.5 million, and net income totaled $24.5 million, marking a 36% YoY decrease. Finally, they reported Adjusted EBITDA of $118.7 million, compared to $136.2 million for the third quarter 2022.

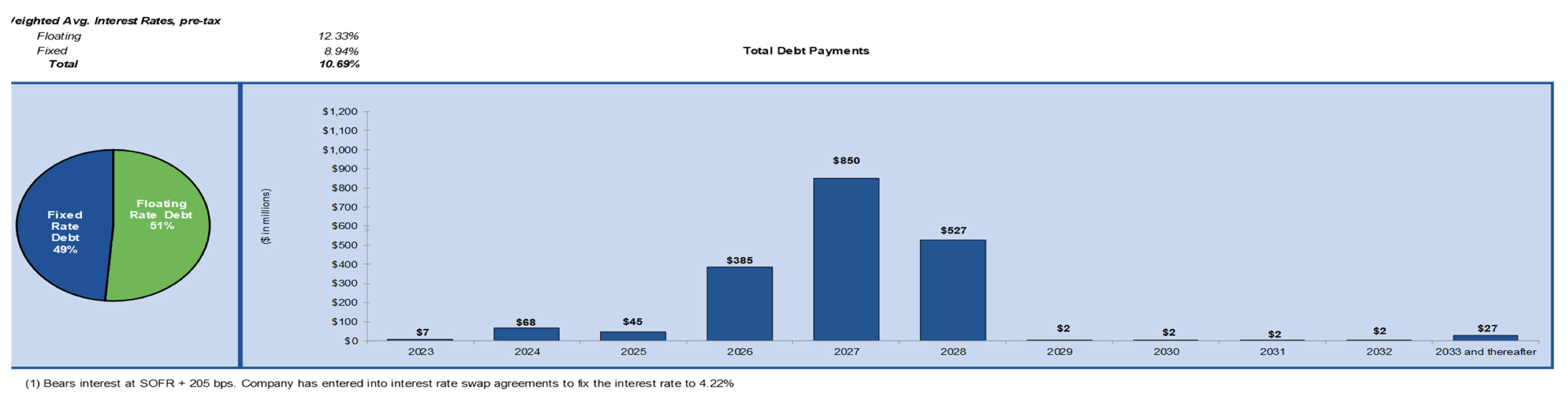

Lastly, the company continued to make progress toward strengthening its financial position. During the third quarter of 2023, they reduced their total net debt by $109 million, ending the period with approximately $1.8 billion in total net debt. GEO doesn't have any meaningful debt obligation till 2026.

Q3 2023 Supplemental Information

{kind=link}

H.R. 4367

On September 28, the House approved H.R. 4367 . This bill proposes:

Ensure that every alien on the non-detained docket is enrolled in the Alternative to Detention Program with mandatory GPS monitoring thought the duration of all applicable immigration proceedings (including appeals) and until removal if ordered."

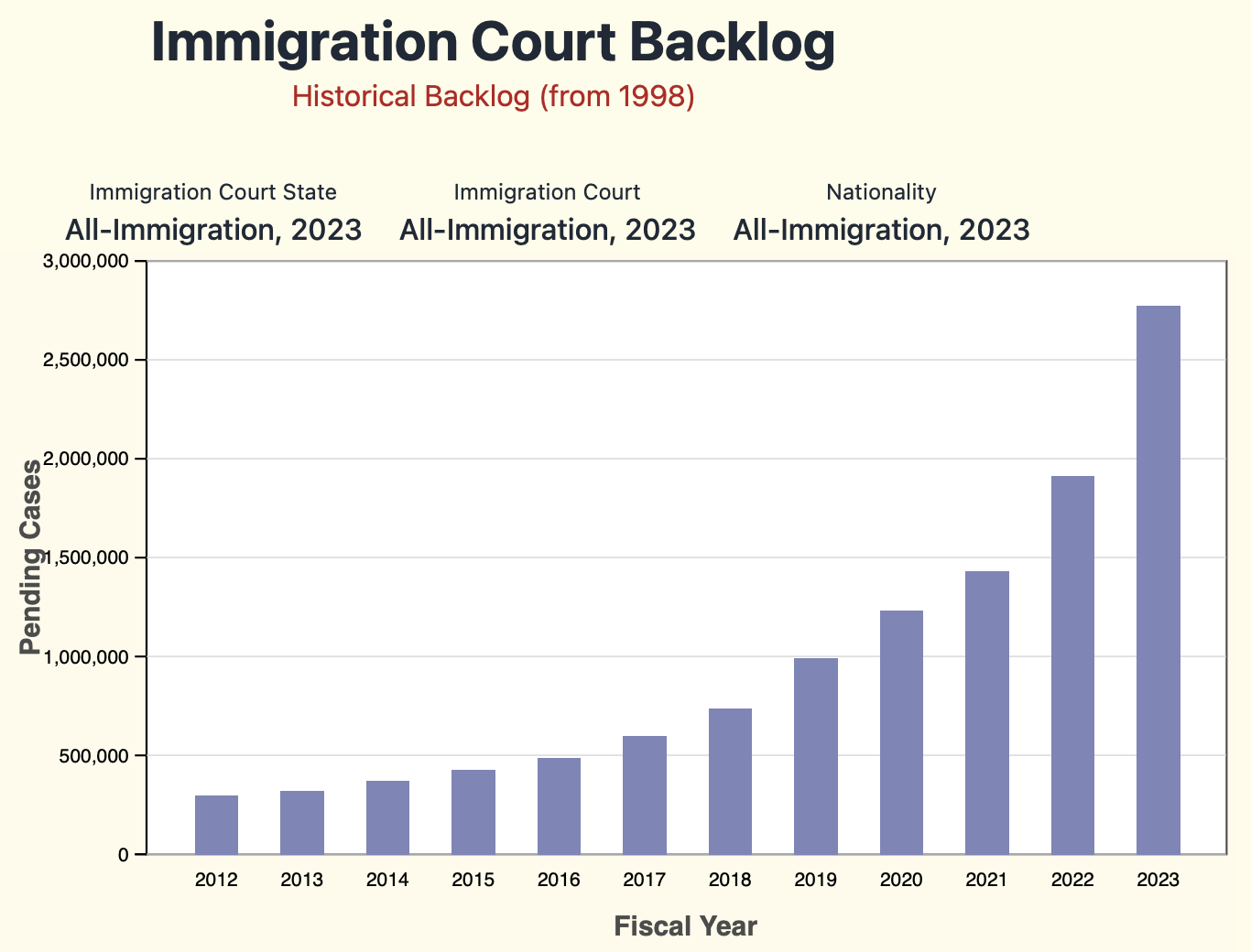

This is significant news for GEO since they currently control 87% of this market. If the bill is put into law, it would increase their current 192,000 to 195,000 participant total in the ISAP program to a potential of 5 million. For instance, look at the immigration court backlog: 2.7 million people are awaiting trial, twice what it was in 2020.

Syracuse University TRAC Immigration

{kind=link}

During the earnings call , COO Wayne Calabrese stated that they are well-prepared and equipped to handle an increase in demand, potentially involving up to 5 million individuals in alternative detention programs. He emphasized their readiness, with nationwide offices available to meet the requirements of such contracts if necessary.

However, management was expecting an increase in ISAP participants in the final part of the year, which hasn't happened. Budgetary pressures for ICE persist, and the timing of congressional appropriation bill passage remains uncertain, which is the reason why they updated their guidance for the remainder of the year.

Guidance

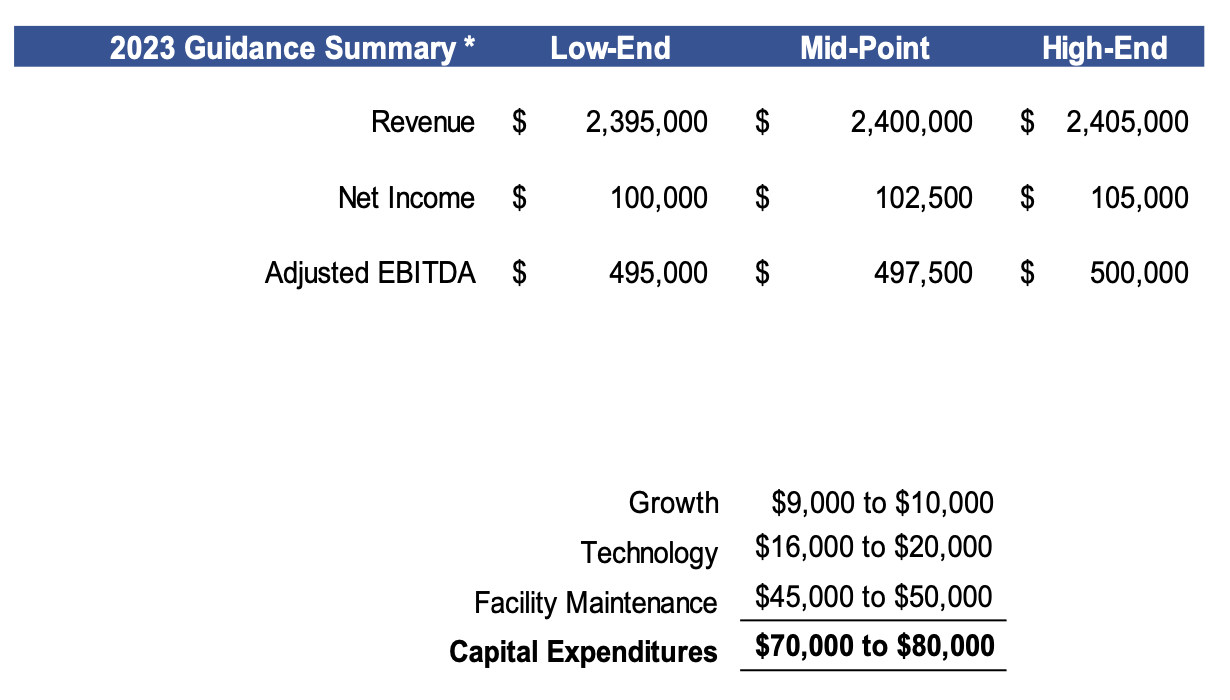

Although the change is not big, the management updated its Adjusted EBITDA guidance for the full year. They now expect Adjusted EBITDA to be between $495 million and $500 million vs. $490 million to $520 million in August, only a -1.5% cut at the midpoint. Revenue and net income remain the same at midpoint of the previous guidance. Capex estimates also remain at $75 million at midpoint.

Q3 2023 Supplemental Information

{kind=link}

Takeaway

The stock currently trades at 5.9x EV/2023 Adj EBITDA, which we believe is attractive given the growth opportunities. Despite uncertain political outcomes, ISAP remains a cheaper alternative to detention and a humane way to monitor immigrants in the U.S. Illegal immigration is a very serious problem that is growing, and politicians will have to tackle it sooner rather than later. We believe GEO is uniquely positioned to benefit from it, and if the bill H.R. 4367 becomes law, the upside for GEO is enormous. We remain long on the stock and reiterate the buy rating.

For further details see:

GEO Group: The Opportunity Is Still Big