GEO - GEO Group: The Valuation Expansion Story May Have Just Begun

2023-10-03 10:00:00 ET

Summary

- The GEO Group's stock has undergone a severe valuation expansion in recent years.

- Ongoing catalysts, such as deleveraging efforts, the surge in illegal migration, and robust profitability in electronic monitoring, are reshaping the trajectory of the stock.

- This could mark the start of a stock valuation upswing, particularly as the likelihood of resumed capital returns grows more plausible over time.

The GEO Group ( GEO ) has seen its stock undergo a valuation expansion over the past couple of months. In my view, this may signify the commencement of a sustained trend, given the positive trajectory of the company's outlook, driven by pivotal catalysts.

These include successfully deleveraging progress, accelerating illegal immigration trends, and strong growth in electronic monitoring. With the company consistently delivering robust profits and steadily enhancing its balance sheet, the likelihood of resuming capital returns appears increasingly promising. Consequently, investor enthusiasm for the stock is likely to endure, particularly if the valuation continues to present an attractive discount.

Let's look at each one of these catalysts individually.

Successful Deleveraging Progress

Trimming down debt has consistently been at the forefront of GEO's strategy over the past few years. GEO's net debt peaked at $2.86 billion back in Q1-2019. This was during the period that all major banks that had been extending lines of credit and term loans to GEO had unequivocally committed to cutting ties with private prisons once all existing obligations were met.

This left GEO's management in a predicament. The prospects for future refinancing appeared dim, particularly due to a shrinking pool of potential creditors being accompanied by the onset of a rising-rates environment. Faced with this challenging scenario, GEO had no choice but to swiftly adopt a deleveraging strategy.

GEO had to pivot towards relying on its internal operational cash flows to finance its future CAPEX. To self-finance, it would have to start diminishing its external obligation. Since then, this deliberate move has not only strengthened the company's financial autonomy but has also paved the way for the potential resumption of capital returns.

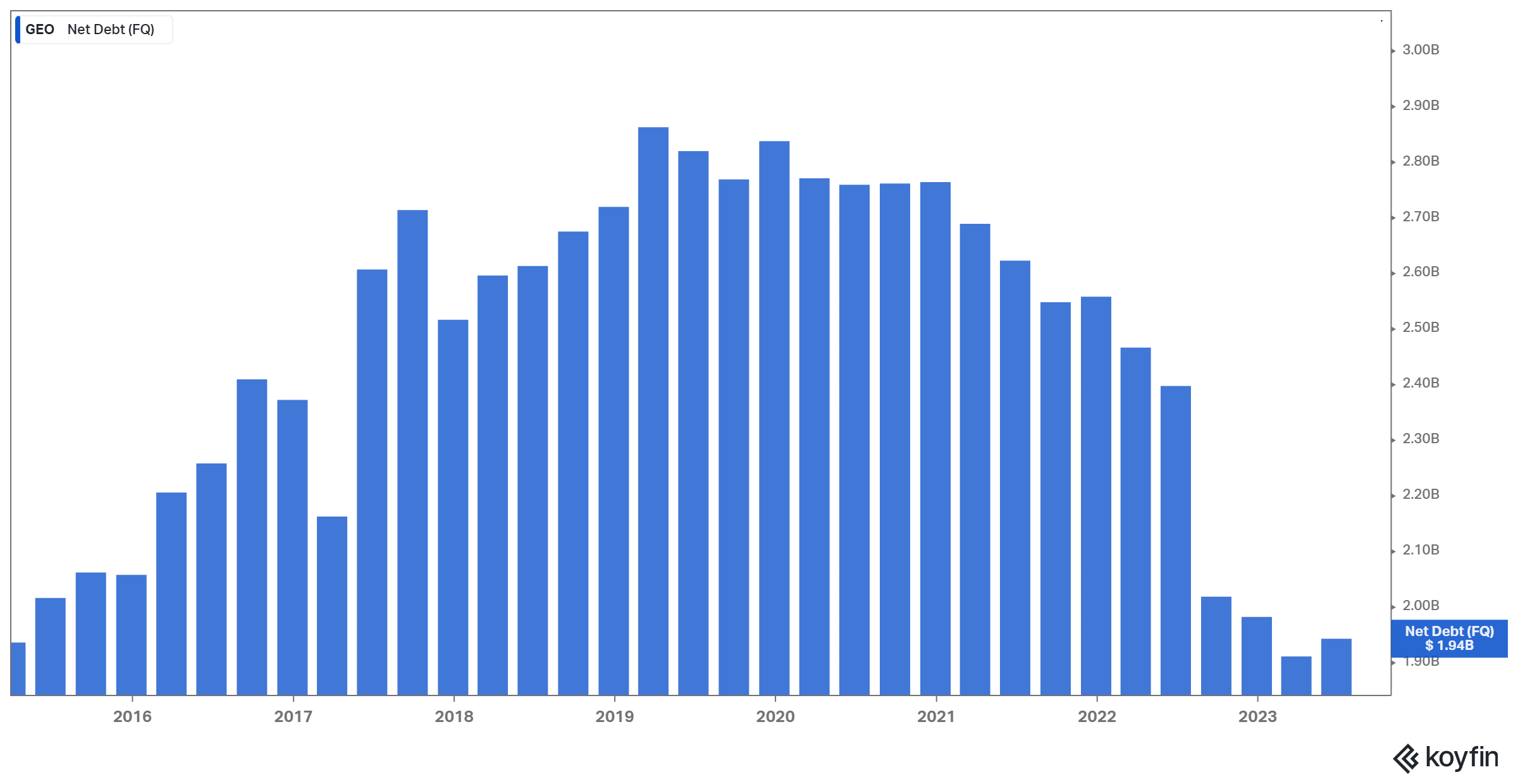

To illustrate the company's deleveraging progress, since Q2-2021, GEO's total debt has gradually declined from $2.86 billion in Q1-2019 to $1.94 billion in its most recent (Q2-2023) results.

The GEO Group's Net Debt (Koyfin)

{kind=link}

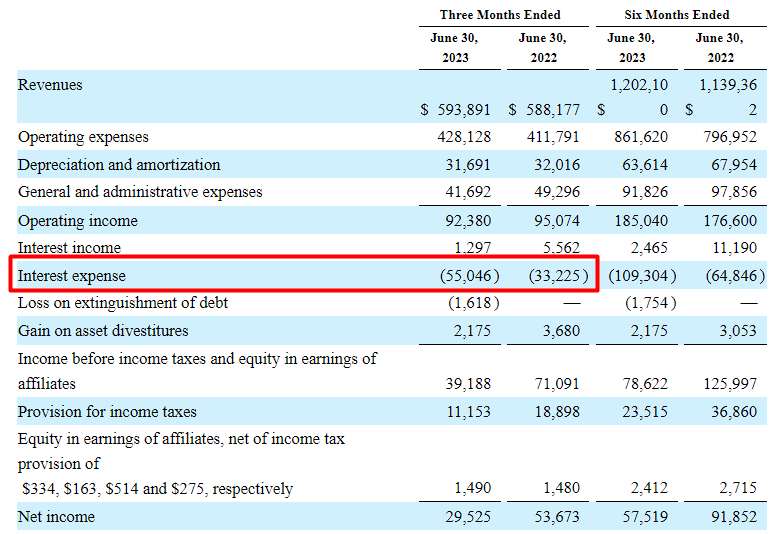

Note that GEO's interest expenses rose significantly in Q2, reaching $55.0 million from $33.2 million in the prior-year period.

GEO's Interest Expenses (10-Q)

{kind=link}

The significant $21.8 million increase, however, was due to GEO refinancing some of its debt in Q3 of 2022. Specifically, in August of 2022, the company exchanged certain of its 5.125% Senior Notes due 2023, 5.875% Senior Notes due 2024, 6.00% Senior Notes due 2026, and certain revolving credit loans and term loans into newly issued senior secured notes and a new exchange credit agreement.

Due to higher interest rates on the new debt instruments, GEO's interest expenses indeed rose. While this may initially seem less than ideal, it serves a crucial purpose in ensuring the continuity of GEO's deleveraging strategy.

Securing the extension of maturities takes precedence in GEO's strategy, so higher interest expenses in the short term should not scare investors, in my view. After all, these increased expenses were inevitable, considering the challenging credit environment (rising rates) currently at play.

The Rise of Illegal Immigration

In the early months of 2023, the U.S.-Mexico border experienced an unprecedented surge in monthly encounters between U.S. Border Patrol agents and migrants seeking entry into the United States, marking levels not seen in over two decades. Regrettably, this upward trajectory shows no signs of waning.

As of June 2023, FAIR estimates indicate that approximately 16.8 million undocumented immigrants now reside in the United States - a notable uptick from their January 2022 estimate of 15.5 million.

However, the most recent data is even more alarming. September witnessed a historic number of migrants crossing the southern border into the United States, with Customs and Border Protection reporting over 260,000 encounters in the last 30 days.

In this unfortunate and challenging scenario, The Geo Group is strategically positioned to leverage the escalating trend of illegal immigration. The heightened demand for the company's expertise in managing and operating detention centers is poised to yield substantial benefits.

As the number of individuals grappling with immigration-related issues continues to rise, government agencies will inevitably seek to collaborate with one of the two foremost authorities in the field - The Geo Group and CoreCivic ( CXW ) - to handle the detention and management of these individuals effectively.

Thus, it's reasonable to expect that this surge in demand for detention services is anticipated to translate into elevated revenues and profits for the company.

Strong Electronic Monitoring Profits

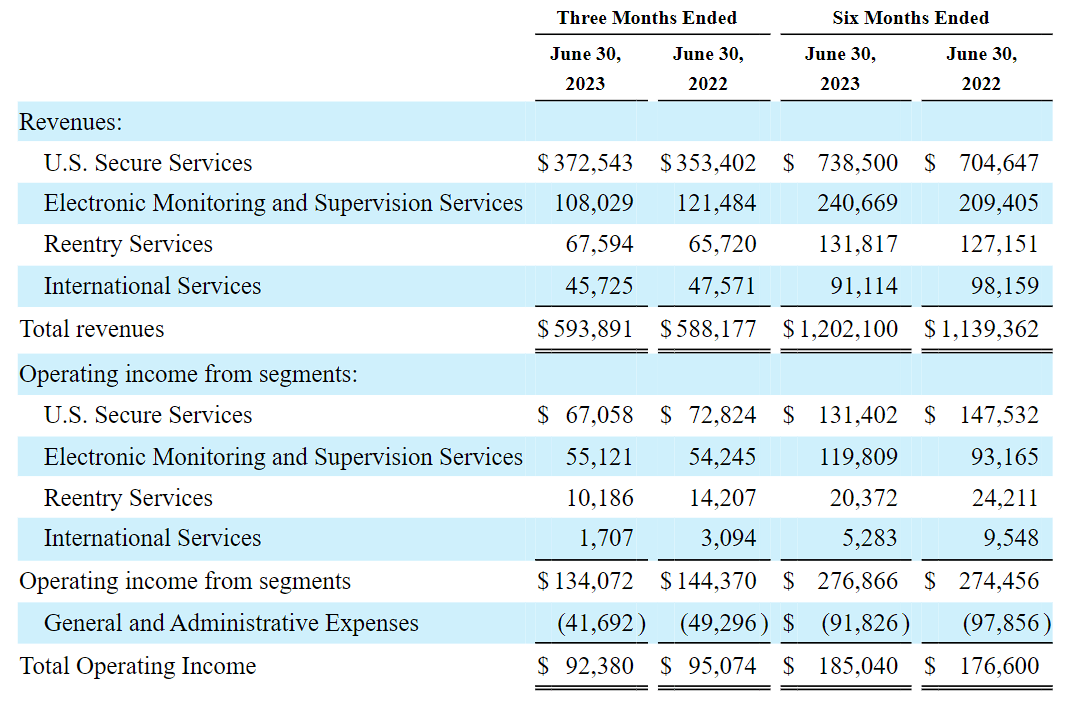

Another positive catalyst for the company's results is its electronic monitoring segment, whose profitability remains very strong and is likely to grow further in the future. Note that in GEO's most recent results, Electronic Monitoring revenues actually declined to $108.0 million from $121.5 million last year.

GEO's Revenues Break Down (10-Q)

{kind=link}

This was because, at the federal level, since the beginning of this year, GEO experienced a drop in the number of participants needed to be monitored under its Intensive Supervision Appearance Program (ISAP) contract with the Department of Homeland Security.

However, management commented that they have lately seen a decline in the rate of decreasing ISAP participants. Moreover, they believe recent policy changes will increase ISAP enrollment.

But besides the growth potential here, I believe Electronic Monitoring should be a strong catalyst for the company moving forward due to its strong profitability prospects. Despite the decline in revenues, Electronic Monitoring posted an operating income of $55.1 million, implying a tremendous operating margin of 51%. Thus, any growth the company is about to see as per management's expectations, should translate heavily into bottom-line growth.

GEO's Valuation Expansion May Have Just Begun

Investors had begun dumping GEO stock all the way back in 2019 with the rationale that the company (REIT at the time) would soon cut its dividend. This ended up being true, as GEO did indeed cut the dividend back in 2021 to focus on deleveraging due to a lack of potential creditors, as I mentioned earlier.

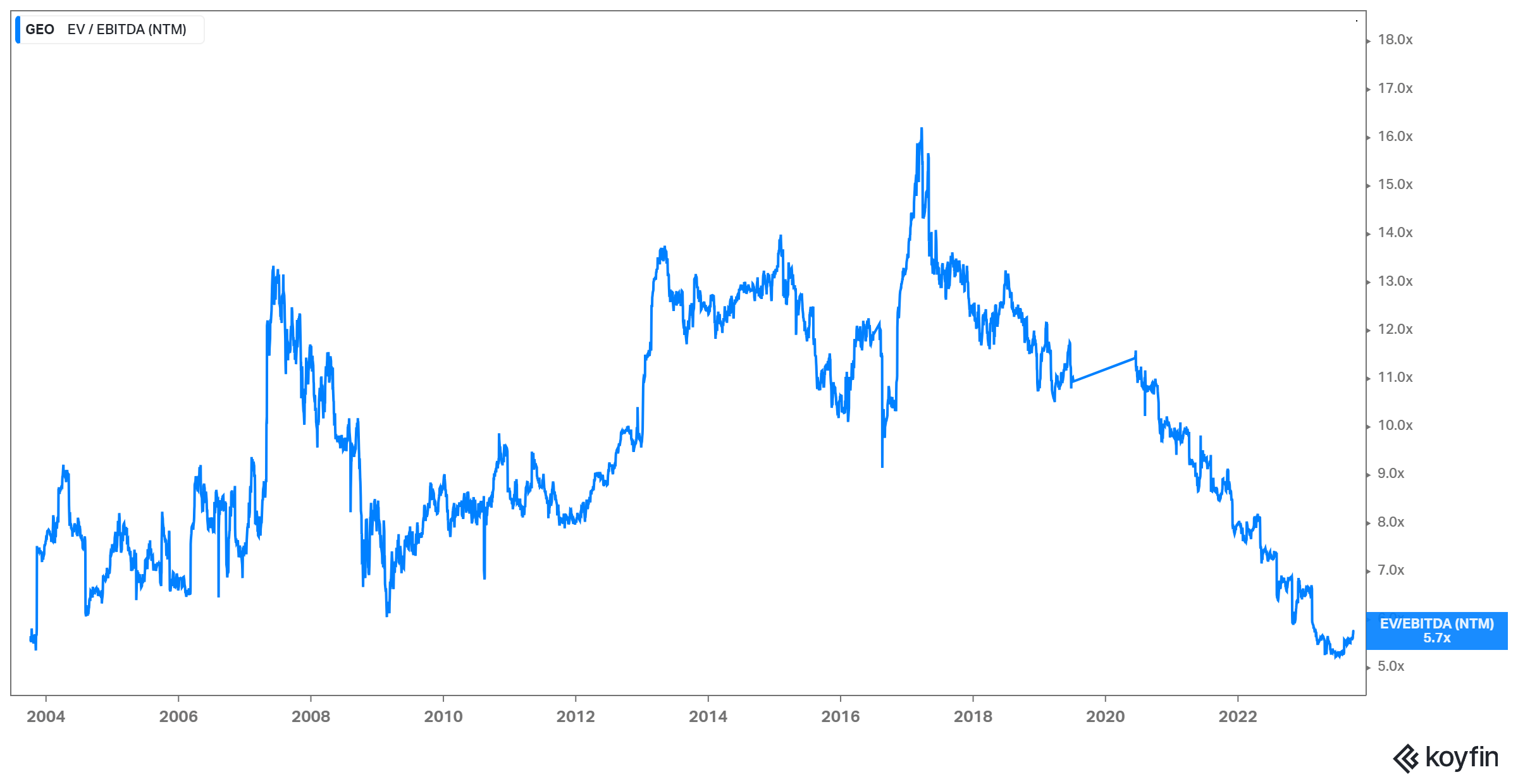

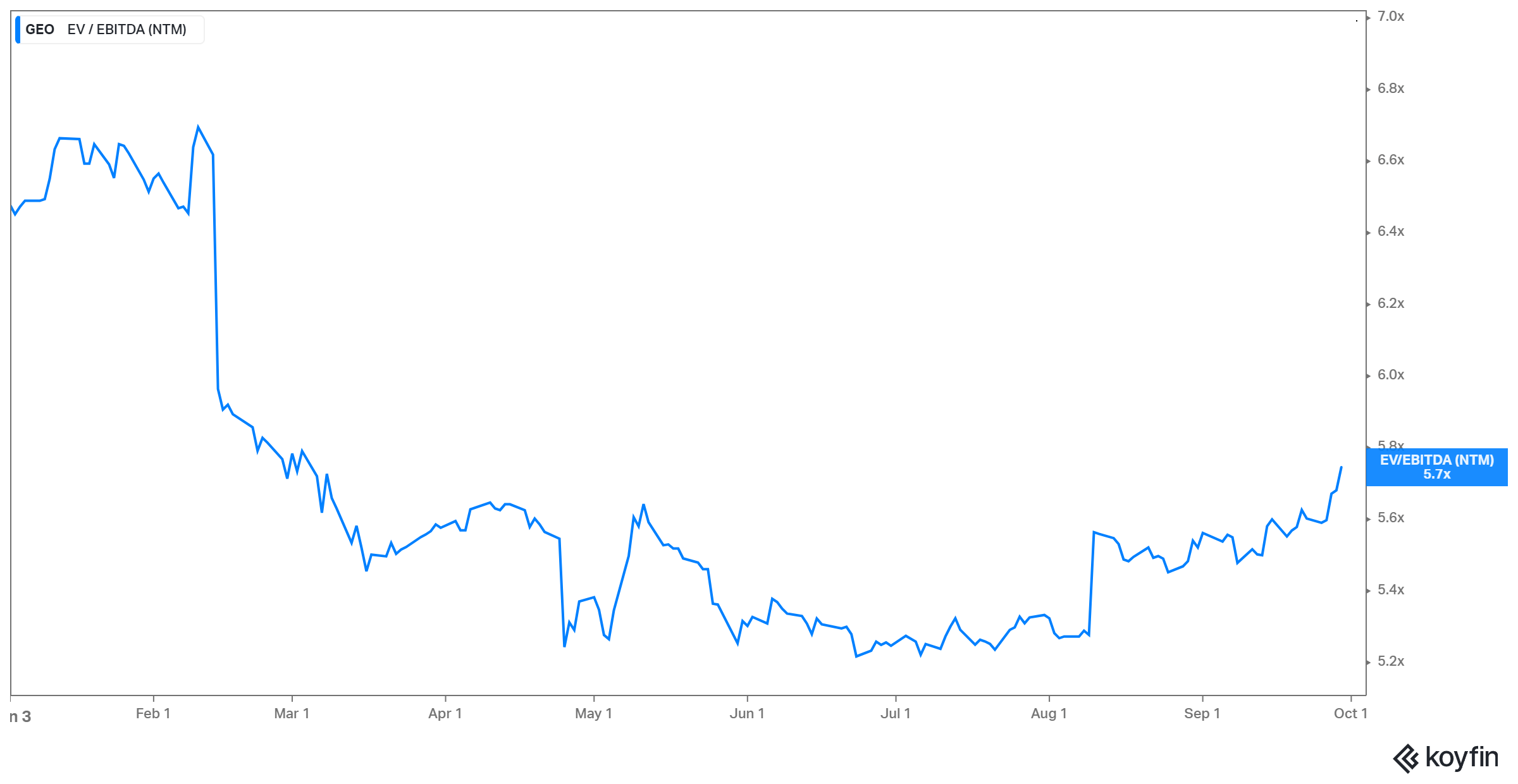

The crux of the matter is that, since 2019, GEO shares have been subject to an ongoing compression in valuation. Notably, this compression has been so drastic that, this summer, the stock's forward EV/EBITDA plummeted to a historic low of approximately 5X.

GEO's Historical Forward EV/EBITDA (Koyfin)

{kind=link}

Year-to-date, the stock's valuation has shown signs of stabilization and even a slight expansion to 5.7X at present, likely influenced by the catalysts discussed earlier.

GEO's Historical Forward EV/EBITDA (Koyfin)

{kind=link}

Nevertheless, considering that the stock's valuation remains significantly below its historical average, there's a plausible scenario wherein the recent valuation uptick is merely the inception of a prolonged trend.

GEO's ongoing deleveraging process should progressively empower management to contemplate reinstating capital returns, be it through dividends or share buybacks.

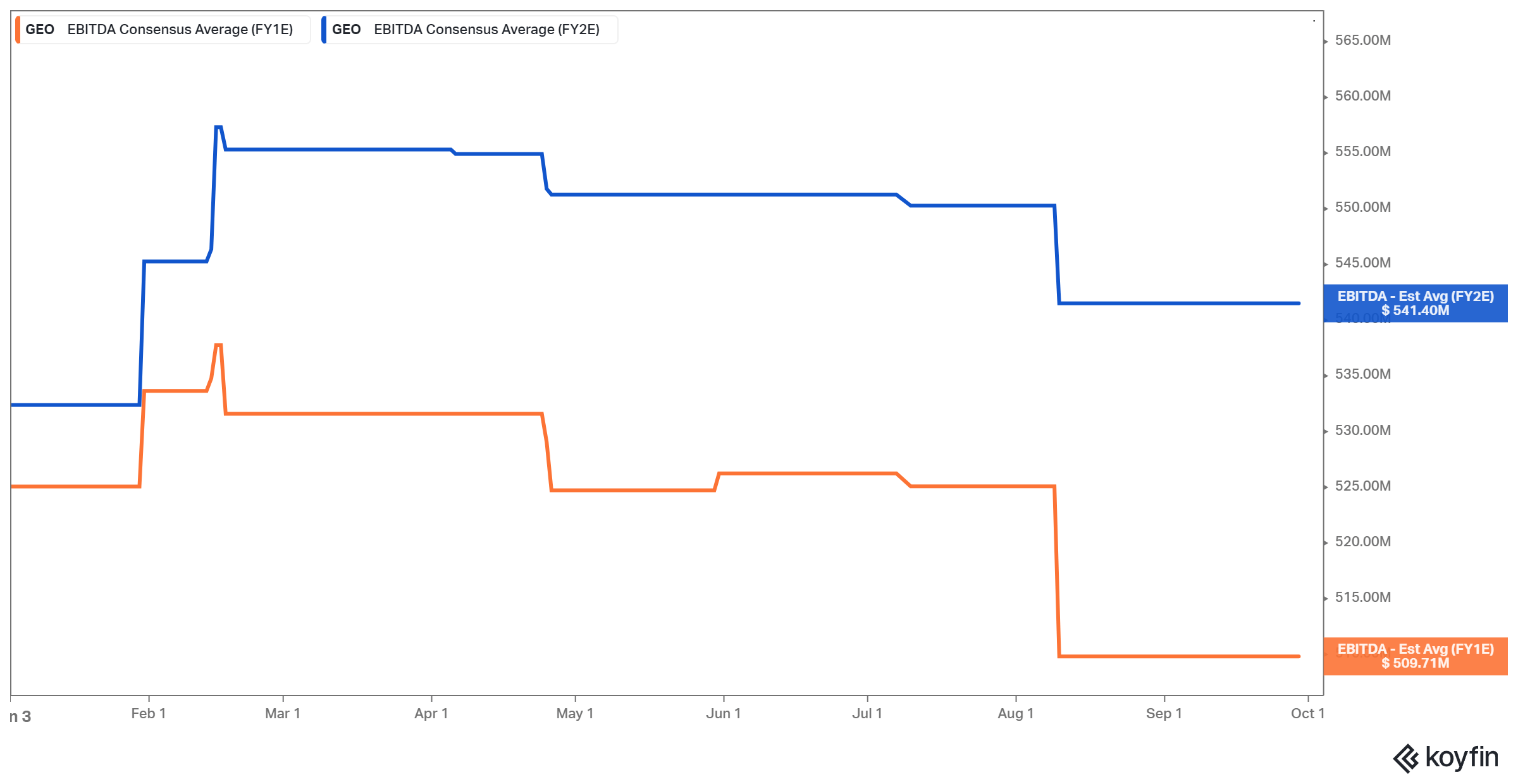

Trading at a mere 2X this year's projected EBITDA and an even more compelling 1.85X next year's projected EBITDA, even a modest allocation of profits back to investors post-successful deleveraging could yield substantial returns at the current stock levels.

GEO's Forward EBITDA Estimates (Koyfin)

{kind=link}

While this may unfold over the next two or three years, with the current pace of deleveraging, investors gradually incorporating this prospect into their "fair valuation" estimates should propel the stock into a sustained trajectory of valuation expansion.

For further details see:

GEO Group: The Valuation Expansion Story May Have Just Begun