RING - Geodrill: Market Overreaction To Recent Quarterly Reports Creates A Buying Opportunity

2023-11-07 19:23:36 ET

Summary

- Geodrill is a microcap company that offers mineral drilling services to the mining industry in West Africa, Egypt, and South America.

- With over 25 years experience, they operate a fleet of 78 rigs and provide advanced drilling operations to support mineral exploration and harvesting.

- Geodrill’s operational reorganization resulted in a slow quarter and a flat year, and management decided to suspend their dividend.

- The market’s reaction to the news was overdone, and now the stock is now set at an appealing price, with an unusually high EBITDA to EV ratio.

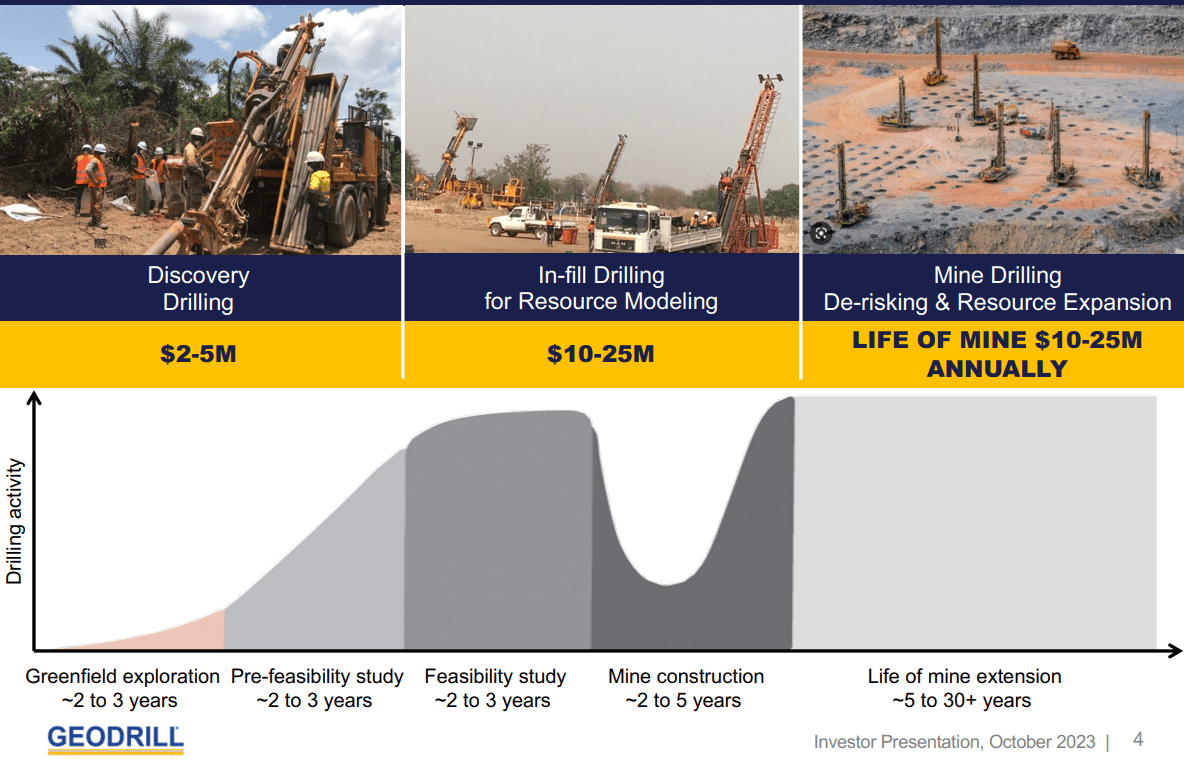

Geodrill ( GEODF ) is a microcap, publicly traded company that provides diverse mineral drilling services to larger drilling operations across the globe. In short, they provide tools and expertise to mining industry in West Africa, Egypt, and South America. They operate a fleet of 78 rigs and provide advanced drilling operation to support mineral exploration and harvesting operations. Their value proposition is based on their offering of multi-purpose, high performance rigs with a network of maintenance and support to keep operations productive from mineral discover through the life of mine. Figure 1 shows how drilling activity is demanded through the different phases of mine operation. Geodrill is able to leverage its relationship with current and former clients, and the company has built a reputation of being versatile and able to complete complicated drill jobs in an effective and efficient manner.

Fig 1. Geodrill’s services are demanded from discovery, in-fill drilling, and mine drilling; over a lifetime of 15-40 years. (Geodrill, Investor Presentation)

{kind=link}

Market Reaction to Q2 Earnings and Withdraw from Burkina Faso

Dave Harper, President and CEO stated: “In quarter two, we took a step back to reposition the company for future growth by sharpening our focus on favorable geographies. This decision consequently impacted our utilization and ultimately, our financial results for the quarter.” This strategic statement referred to the company’s decision to leave operations in Burkina Faso and deploy rigs elsewhere. Much of the rest of the earnings call focused on the details of this decision and its impact.

The company reported 2Q revenue to be $32.6 M, representing a year-over-year decline of $6.5 in revenue. About half of this decline was attributed to the ongoing withdraw from operations Burkina Faso to target more favorable regions in the future.

The reaction to the earnings report was an immediate stock price drop from $2.36 per share by about 20%. Investors were disappointed by guidance that indicated a reduction in future revenue predictions for 2023 and 2024.

Market Reaction to Q3 Earnings Preview

After the second quarter decision, the stock price continued to deflate to about $1.85 per share as the investors digested the news. Then, at the end of October, the company made a press release whereby they pre-announced key results of the upcoming Q3 results. Management stated that they expect an unaudited, non-cash credit loss of $3.6 M on a pre-tax basis. Further, they expect revenue to come in around $30 M, and earnings will be flat. Consequently, they will not be declaring a semi-annual dividend.

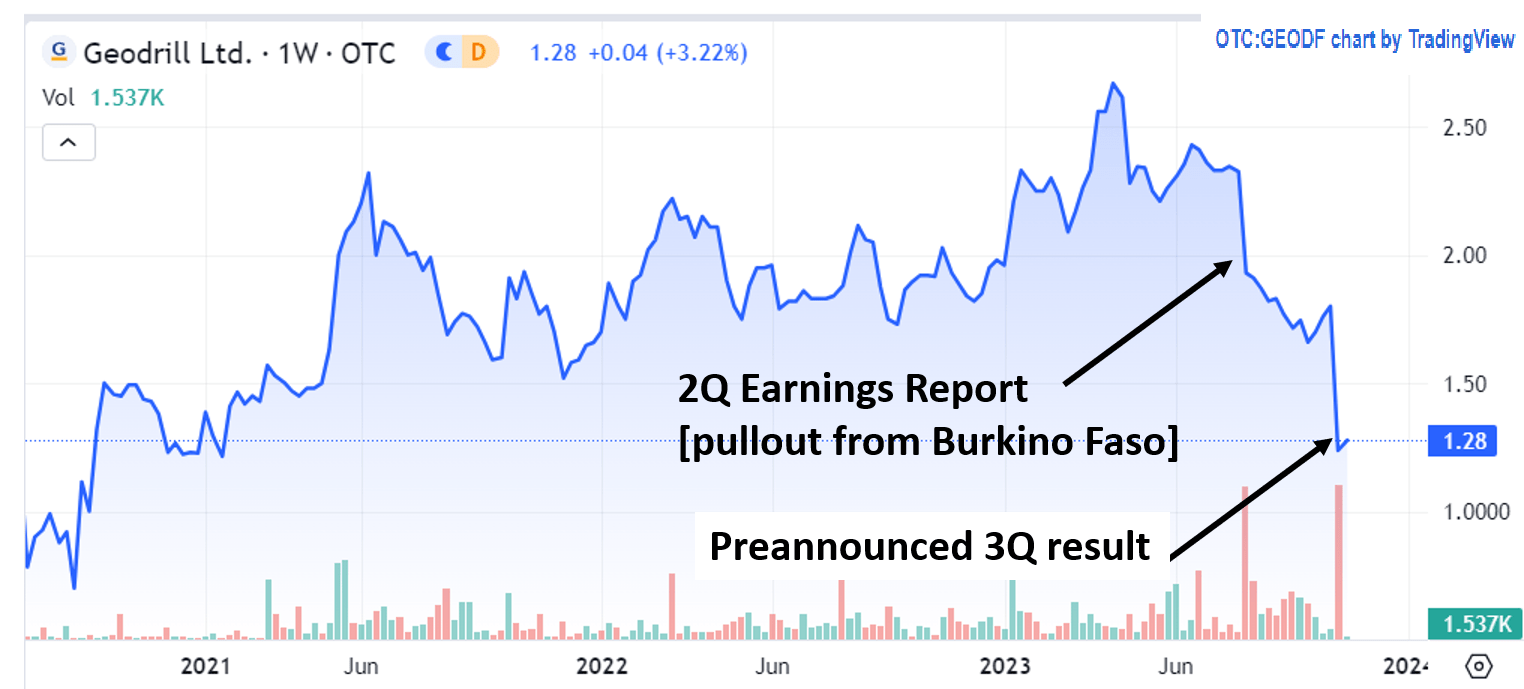

In my view, this announcement is pretty much in-line with the expectation presented at the conclusion of the 2Q conference call; i.e. no new information. Yet, the market reacted harshly a second time, and the stock price tanked by an additional 22% on October 31 st . Figure 2 shows the market reaction to the events. It seems as if a double-dose of the same news—that they expect a flat 2023- combined with the psychological impact of the dividend pause, spurred many investors to sell, potentially leaving the stock undervalued.

Fig. 2 Market response to Geodrill's earnings statements showing two significant drops in stock price. (TradingView)

{kind=link}

Valuation

I will use two methods to evaluate whether Geodrill is currently undervalued. First, I will examine the ratio of Earnings Before Interest Taxes Depreciation and Amortization (EBITDA) to Enterprise Value (EV). Against the convention, I placed EBITDA in the numerator because the ratio EBITDA/EV represents how much EBITDA is generated per dollar of EV. The higher value of EBITDA/EV, the better the valuation.

This valuation metric EBITDA/EV only works for companies that generate positive EBITDA. Geodrill has been EBITDA-positive for years, and Geodrill’s current EBITDA/EV ratio calculated from the past twelve months is 0.64; i.e. Geodrill produced about $0.64 per dollar of its current enterprise value.

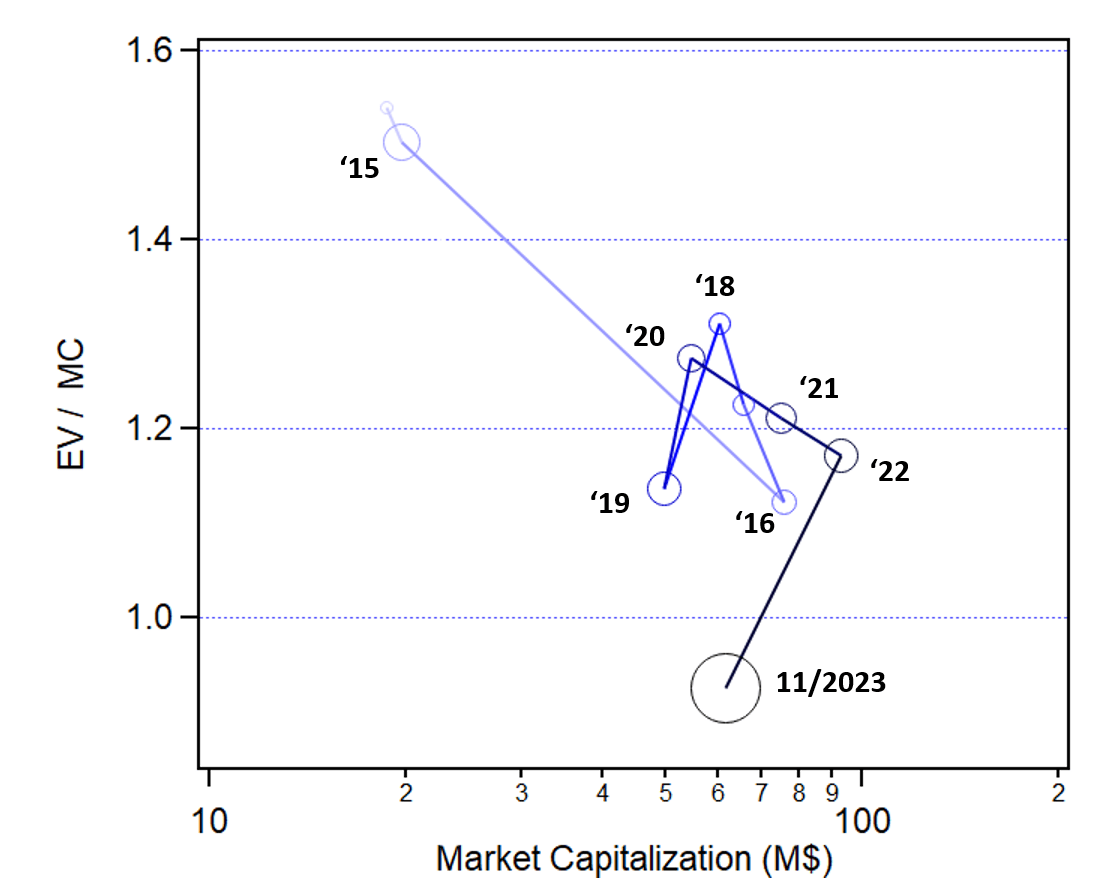

To better understand how the valuation relates to Geodrill’s prior performance, I made a bubble plot with the market capitalization ((MC)) on the x-axis and the ratio of EV/MC on the y-axis. The radius of the bubble is the valuation ratio EBITDA/EV as discussed above. The larger the radius, the more EBITDA generated per dollar of EV. Each data point was taken at the end of each calendar year, and most years are labeled.

The interpretation of the plot is as follows: (i) Geodrill has been EBITA positive for years; (ii) the company has grown its MC over the past decade; and (iii) currently, the EBITDA/EV ratio is significantly higher than it has been for a long time.

Fig. 3. Bubble plot of MC versus EV/MC. The radius of the bubbles is EBITDA/EV. (Figure created by Absolute Valuation)

{kind=link}

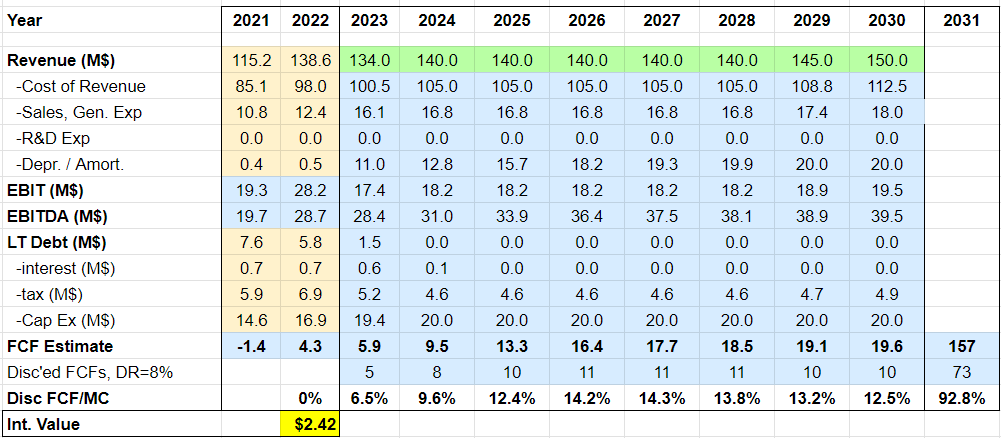

With the possibility that the stock may be undervalued, I conducted a simplified discounted free cash flow model of GEODF's financial performance into the future. I took the analysts’ predictions of revenue for 2023 and 2024, and I held the 2024 revenue prediction of $140 M constant for future years, assuming zero growth. Note that this assumption is very conservative because it goes against the company's track record of consistent and organic growth.

The cost of revenue was based on a 25% gross margin figure, even though several of the previous years exceeded that gross margin. The sales and general expenses were taken to be 12% of revenue, roughly in-line with the prior five years. Depreciation was calculated as a fifth of the prior five years capex investment. EBIT is calculated as the remaining revenue, and EBITDA is calculated by adding back depreciation to EBIT. Interest is assumed to be 8% of long-term debt, compounded annually, and tax is 25% of EBIT. Each year’s free cash flow is calculated by subtracting interest, tax, and cap ex investment from EBITDA. Free cash flow is used to reduce long term debt until paid off. Discounting future cash flow streams at a discount rate of 8%, the model predicts GEODF has an intrinsic value of over $2 per share which indicates the stock is overvalued. The model is simple, and I'm sure there are inaccuracies, but the estimated intrinsic value is about a factor of two greater than the current stock price.

Fig. 4. Table showing results of discounted free cash flow model. (Figure created by Absolute Valuation)

{kind=link}

Key Risks

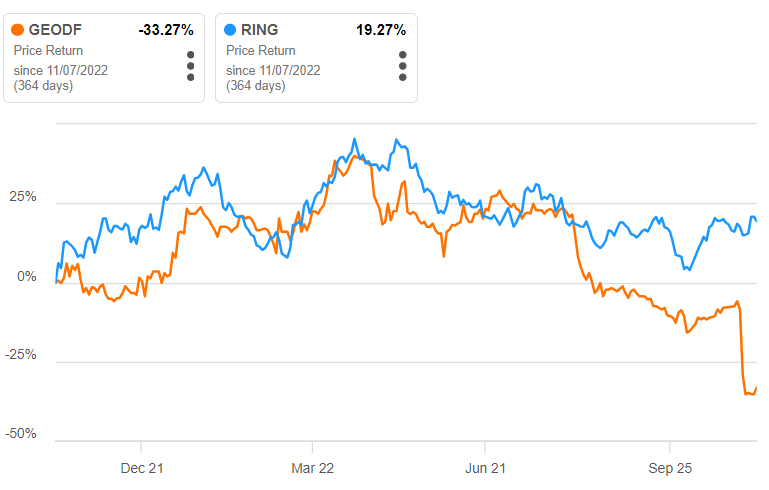

Probably the greatest risk in investing in Geodrill is the overall market demand. Global capital expenditure in the metals and mining sector is expected to decline from 2023 to 2027 , however market strength may be provided by gold and iron ore development. This outlooks is likely dragging the whole sector down. However, Geodrill still stands out as declining disproportionally compared to others. For example, Figure 5 shows a comparison of Geodrill's stock price performance to RING, a benchmark ETF that tracks the MSCI ACWI Select Gold Miners Investable Market Index. Geodrill's price tracked the index well until the Q2 and Q3 news releases when Geodrill's price was driven much lower.

Fig. 5. Comparison of Geodrill stock price performance to RING, a benchmark miner ETF. (Seeking Alpha)

{kind=link}

Political instability in West African countries is a second risk. Geodrill mentioned 'security concerns' in the recent conference call. Security was a consideration that may have led to their withdrawal from Burinka Faso. The recent coup in Niger is not far from some of their operations and highlights how a democratic government can be less stable than once thought. Political instability is a real risk, however, while Geodrill may be present in at-risk countries, the company is nimble. They can pack-up and relocate to other countries within a quarter or two. Their ability to be nimble is certainly an asset that mitigates this risk.

A final risk worth mentioning is that Geodrill is a microcap stock. One should always be a little leery investing in microcaps because what may seem like a small event may be a big event and can affect a large fraction of the business. Examples may include loss of a key customer or an executive. Lots can go wrong.

Summary

In summary, Geodrill appears to be undervalued due to an overreaction to their soft quarter. They have provided rather consistent performance for years, and likely will keep their 78 rigs busy, contributing to EBITDA. While I rate Geodrill a Buy, the two main risks facing Geodrill are overall market demand and political instability.

For further details see:

Geodrill: Market Overreaction To Recent Quarterly Reports Creates A Buying Opportunity