GEOS - Geospace Technologies: Positive Signs Despite A Few Headwinds

2023-07-10 01:20:48 ET

Summary

- Geospace Technologies Corporation's asset utilization increased in 2023 due to interest in its ocean bottom node technology and a potential $20m rental contract extension for Mariner.

- The company's operating margin expanded in Q2 2023 due to cost-cutting measures, and it is also exploring opportunities in carbon capture technology monitoring and analytics.

- Despite these positive developments, the company remains cautious about increasing its rental fleets and cash flows remain a concern. The stock is currently undervalued compared to past valuations.

GEOS Is Gathering Steam

My previous article on Geospace Technologies Corporation ( GEOS ) discussed its business and strategies. In 2023, the company's asset utilization was boosted following increased interest in its latest ocean bottom node technology offerings. Recently, it extended a rental contract duration for Mariner for a potential $20 million agreement. As the cost-cutting measures implemented in Q1 took effect, its operating margin expanded remarkably in Q2. The other promising area for the company is monitoring and analytics in carbon capture technology.

However, the company will likely remain cautious and wait for a more encouraging energy market environment before increasing its rental fleets. Cash flows remain a concern, although its robust balance sheet will help it avoid financial risks. The stock is relatively undervalued compared to its past valuation multiples. I think investors should "hold" the stock until a more favorable energy market situation evolves.

Offshore Activity Boost

{kind=link}

The company's oil & gas business has recently benefited from higher utilization of the OBX rental fleets and higher demand for seismic sensors following increased offshore energy activity. The US offshore rigs increased by 27% over the past six months, leading to the improved utilization of the fleets. The company's latest ocean-bottom node technology offerings can invoke further interest in this sector. I expect enhanced market conditions to persist in the foreseeable future, reducing company performance volatility. Some of these projects are expected to extend in 2024.

In June, the company extended a duration rental contract for Mariner, its shallow water seabed wireless seismic data acquisition node. The estimated value of the agreement is $20 million. Mariner allows contractors to fit ~25% more nodes into a download/charge container. In Q3 2023 and the remainder of 2023, its rental fleets (oil and gas seismic equipment) would operate near full utilization with these contracts.

The Challenges

However, GEOS's capex estimate for FY2023 has been reduced. In this context, investors may note that earlier in the year, it had planned to spend ~$6 million in capex on the rental fleet in FY2023. While it continues to add rigs, the company is now looking at the cost more minutely. Following the limited availability of the procurement of some components, it has found ways to resolve the issue through better design.

However, the company will likely remain cautious and wait for a more encouraging energy market environment (higher energy prices and demand scenarios) before committing to placing new assets and fleets. For a comprehensive understanding of its risk factors, please read my previous article .

Non-energy Business Drivers

The sale of water meter cables, connectors, and industrial sensor products increased in its Adjacent Market segment. The domestic municipalities look to continue to update their smart meter infrastructure. These infrastructure updates can increase the number of contracts for its Aquana smart water shut-off valves. In 1H 2023, GEOS sees headwinds in its emerging market segment. This can change following the recent DARPA (Defense Advanced Projects Research Agency) contract and some potentially undisclosed major defense contractors in the future utilizing its SADAR acoustic arrays.

The other promising area for the company is carbon capture technology. It does not plan to get involved in the core carbon capturing process like capture, transport, or other high-cost initiatives but focuses on monitoring the sequestration to understand whether the plans meet the expectations. It has built a mechanism to monitor at low cost with precision. It has developed highly precise monitoring capabilities using the array technique and analytics.

Analyzing Q2 Drivers

{kind=link}

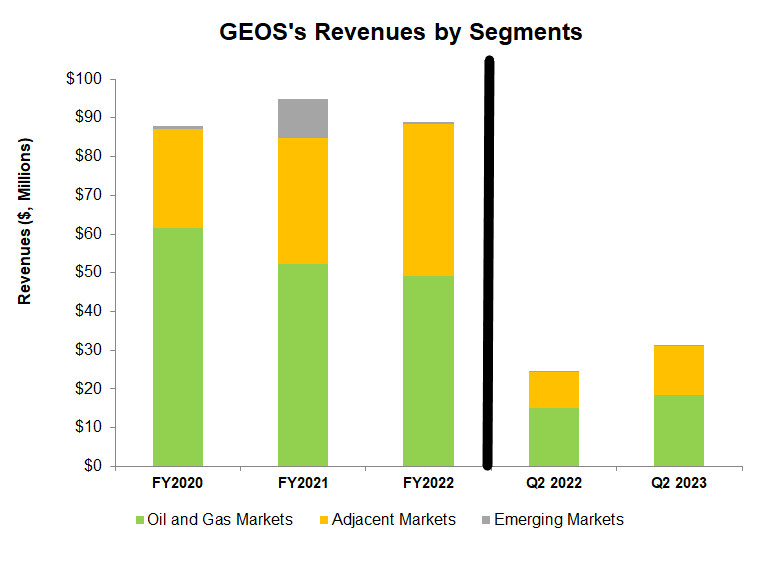

From Q2 2022 to Q2 2023, the company's revenue increased by 27%. Revenues from the Oil and Gas Markets segment saw a 22% rise because utilization of its OBX rental fleets, and demand for the seismic sensors increased. In the near term, the company expects the trend to continue, which will reduce volatility in its business.

Revenues from the Adjacent Markets segment increased by 38% in the past year until Q2 2023. A steep rise in industrial product revenue primarily accounted for the growth. The company's sales of water meter cables, connectors, and industrial sensor products increased in Q2. While sales in the emerging market segment are not consequential, it has $2.1 million in backlog here, which can contribute to sizeable revenue visibility in 2H 2023.

A Margin Discussion

{kind=link}

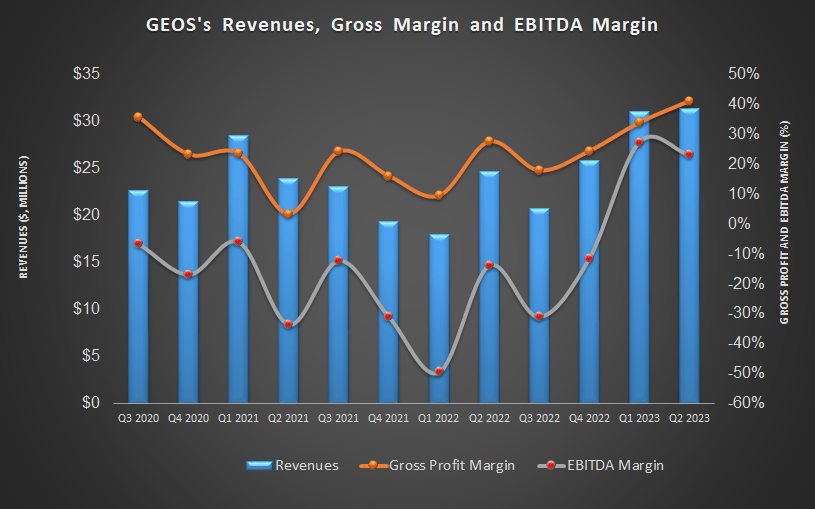

The company's operating expenses decreased by 7% in Q2 2023 (excluding changes in contingent earn-out liabilities). The company's cost-cutting measures that began in Q1 led to the operating cost decrease in Q2. From Q2 2022 to Q2 2023, the company's gross margin expanded significantly (by 1360 basis points), while its EBITDA also turned positive in Q2 2023 compared to negative EBITDA a year ago.

Cash Flows And Liquidity

In 1H 2023, GEOS's cash flow from operations and free cash flow improved but remained in negative territory compared to the previous year. Higher revenues mainly accounted for the slight improvement in cash flows. As its rig fleet stagnates, The company has revised its expected capex to $2 million in FY2023. GEOS has no debt - an advantageous position over some of its peers (FTI and SLB). Its liquidity was $28 million on March 31.

What Does The Relative Valuation Imply?

GEOS's current EV/EBITDA multiple (7.1x) is much lower than its five-year average (13.7x). So, it appears to be undervalued versus its past.

Why Do I Keep My Rating Unchanged?

In my previous article, I identified GEOS's plans related to the consolidation of its OBX rental operations and reducing costs. It was supposed to benefit from a recently struck defense sector deal related to advanced marine seismic acoustic technology. However, its financials were still suffering from the continued net losses over the past several years. I wrote :

The company also aims to diversify away from the typical border security work with Quantum's Analytics Technology applications. As a result of these positive changes, the company's gross and operating margins grew in Q1 2023. However, investors need to be concerned about the operating risks.

Over the past six months since I last published, the offshore market has improved in the US, which significantly boosted asset utilization. The sale of water meter cables and related products increased in its Adjacent Market segment. But its management has become more cautious over the oil and gas seismic equipment fleet addition plans and will likely keep it unchanged until the energy environment improves. So, I keep its rating unchanged at "hold" versus the previous call.

What's The Take On GEOS?

{kind=link}

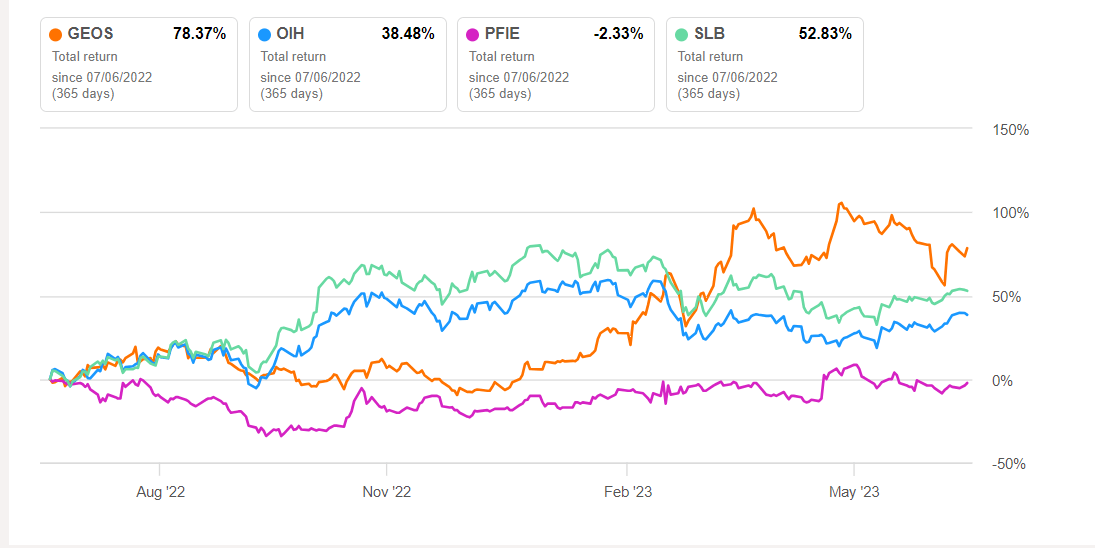

GEOS's primary driver in FY2023 would be higher utilization of the OBX rental fleets and higher demand for seismic sensors. Recently, it has signed an extended rental contract for Mariner, potentially adding $20 million to its revenues. In the Adjacent Market segment, demand for its water meter cable and connector products will stay robust following domestic municipalities' smart meter infrastructure update process. Plus, there can potentially be a few undisclosed major defense contracts in the future. So, the stock outperformed VanEck Vectors Oil Services ETF ( OIH ) last year.

However, the company's oil and gas seismic equipment fleet size will likely remain unchanged in the near term. So, it scaled back its capex plans for FY2023. It also sees headwinds in its emerging market segment. Although cash flows showed some improvements in 1H 2023, they remained negative. Given the relative valuation, I suggest investors "hold" it with an expectation of higher returns in the medium-to-long term.

For further details see:

Geospace Technologies: Positive Signs Despite A Few Headwinds