GNGBF - Getinge: Turnaround Catalysts To Outperform Healthcare Peers

2023-08-15 03:43:11 ET

Summary

- Getinge AB is a Swedish healthcare medical tech company with a $5 billion market cap and leading positions in multiple niches within its target markets.

- The company has faced headwinds in recent years but offers a clear turnaround opportunity with unique diversification and a stable financial foundation.

- Getinge's focus on the bioprocessing market, along with recent acquisitions, positions it to compete with larger competitors like Thermo Fisher and Danaher.

Introduction

Getinge AB ( GNGBY ) is a Swedish Healthcare Medical Tech company focusing on three revenue segments: Acute Care, Life Sciences, and Surgical Workflows. The company is small, valued at a $5 billion USD market cap, but offers a leading position across multiple unique niches within its target markets. This includes multiple #1 market share positions over giant competitors like Medtronic ( MDT ), GE Healthcare ( GEHC ), and STERIS ( STE ). Also, thanks to one recent acquisition, Getinge is now looking to battle the goliaths of Thermo Fisher ( TMO ) and Danaher ( DHR ) in the bioprocessing market. Unfortunately, Getinge has also suffered through various major headwinds over the past few years and this has led to a suppressed valuation and underperforming financials.

The goal of this investment is to capitalize on a return to form, eventually in line with peers. Thanks to unique diversification, temporary headwinds, and a stable financial foundation, I believe the short to intermediate turnaround play opportunity is significant. This article will summarize the current business operational state, historical financials, and future opportunities, all through the lens of a more risk-oriented, fleet-footed investor. However, there is also a chance for long-term investors to benefit, as long as company weaknesses do not continue. And, although there is a stable dividend policy in place, high margins, and a low leverage foundation, investors who are shy of volatility will be better suited with a wide variety of strong peers.

A Clear Turnaround Opportunity

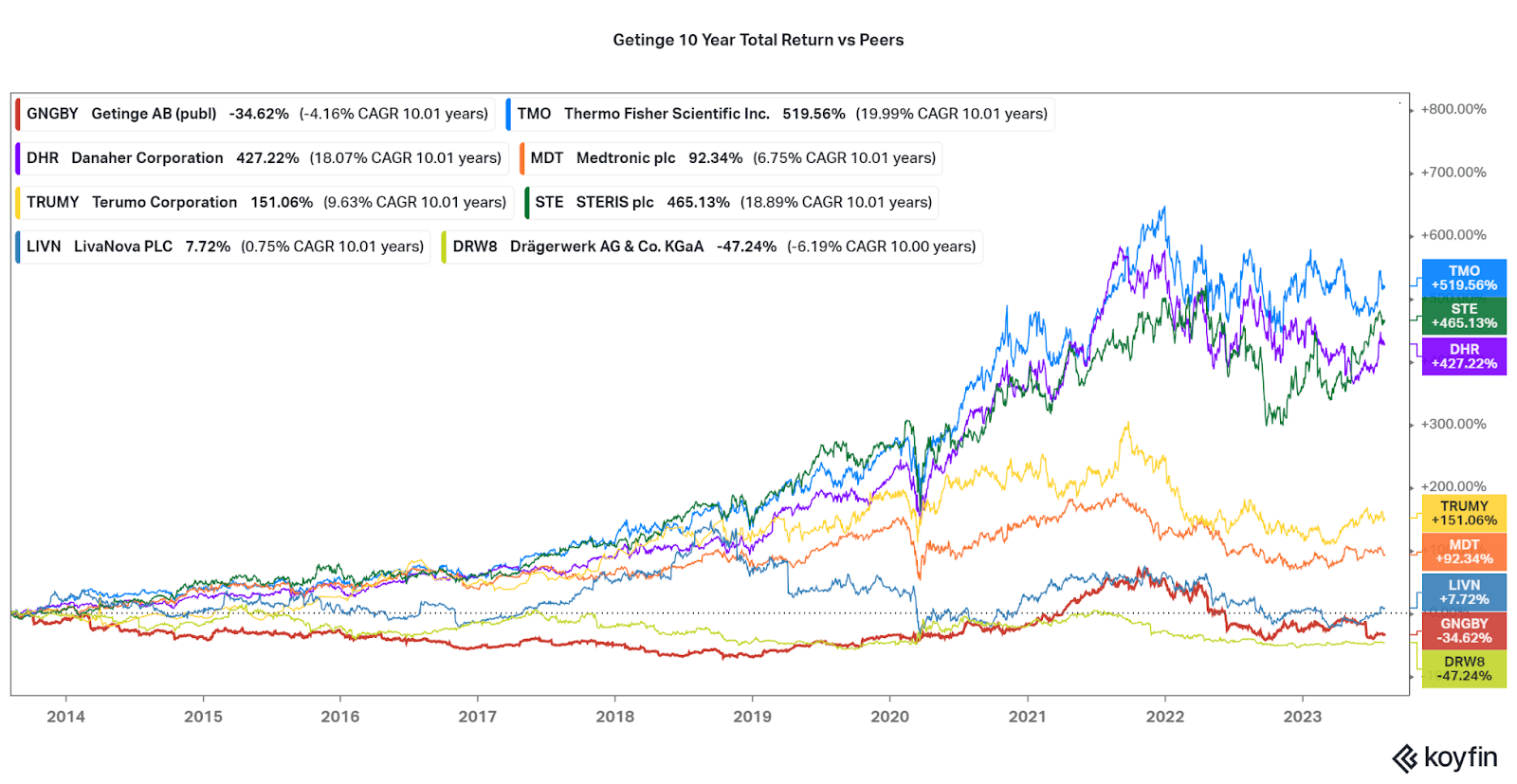

I will start with the weaknesses. First, due to cyclical growth total returns have ended up negative over the past 10 years. This is in line with some other specialist peers like LivaNova ( LIVN ) and Drager ( DGWPF ), but far below the industry stalwarts. As reflected in the chart below, bioprocessing giants TMO and DHR offer significant growth opportunities and will be the goal profile for Getinge's Life Sciences segment moving forward. However, the acute care and surgical workflow segments will likely move in line with peers such as Terumo and MDT but still superior to recent performance. If these goals are met, it is clear significant upside is present based on current valuations. More on that below.

{kind=link}

Recall Headwinds

One reason why investors can feel comfortable with upside rather than downside is that current headwinds are based on temporary regulatory issues. In four separate cases, Getinge has lost CE certification and/or is facing risk issues that have led clients to stop purchasing. While some of the items are still sold as they are listed as essential, there are meaningful financial impacts occurring. Thankfully, the issues seem to be related to packaging defects and third-party supplies, and this limits reputational risk to Getinge technology. With some issues already resolved after a few months and most set to be resolved within one calendar year, we should see a rebound in sales from these four high margin units. The temporary sell-off and underperformance can be taken advantage of in my opinion.

Getinge 2Q23 Presentation Getinge 2Q23 Presentation

{kind=link}

{kind=link}

Getinge Operational Overview

Getinge may only be mid-sized but offers unique expertise in a wide amount of verticals within both research lab and hospital settings. Overall, the company has goals for profitable growth rather than being a more speculative accelerator. Despite some weaknesses over the past 5-10 years, profitability has not been a significant issue for its size, and I expect improvements to come long term. As of the 2022 Annual Report, Getinge has goals for mid-single digit annual organic growth and to drive 10%+ yearly earnings growth off those revenues. With these goals met in the future, Getinge will have a favorable financial profile in-line with far larger peers. And, it will match the opportunity presented by the company's leading market share across its operating segments.

Getinge Annual Report 2022

Acute Care

Getinge's bread and butter is with acute care technologies, particularly with #1 global market position in intensive care tech and cardiovascular surgery products. However, we see that these markets are slower moving and are the cause of some of the company's grief over the past decade. I believe the primary issue is in regard to competitive technologies, such as with Edwards Lifesciences's ( EW ) TAVR products. While there is room for improvement, I believe it is best for management to switch focus to the other revenue segments for future growth.

Data suggests that ICU mortality rates are falling with time. This may mean broader success in non-ICU treatment is limiting growth of the field, despite higher incidences and mortalities associated with cardiovascular disease worldwide. Therefore, Getinge will face issues with growth and profitability in this segment as capital either go towards acquisitions or R&D. It is also important to note this is the segment currently affected by the packaging issues but generates most of the company's profits.

Getinge Annual Report 2022

Life Sciences

Now, the more interesting segment is Life Sciences and, in particular, the Pharma production specialty. Growth rates are far higher in the low double-digits, and Getinge still maintains respectable second-place market share holdings. This is where the market position data is a bit stretched in my opinion, as Thermo Fisher's Life Sciences unit sees over $13 billion per year and Danaher sees over $7 billion in bioprocessing revenues per year. Getinge's ~$400 million in segment revenues pale in comparison.

However, as I will discuss later, Getinge has one particular niche in which they seem to excel in: transportation/logistics thanks to their novel packaging systems, similar to their Acute Care technologies. Tie in a recent acquisition that bolsters its single use bioproduction product portfolio, and I believe that the growth of the Life Sciences division will quickly create the leading revenue segment within a few years thanks to rapid growth.

Getinge Annual Report 2022

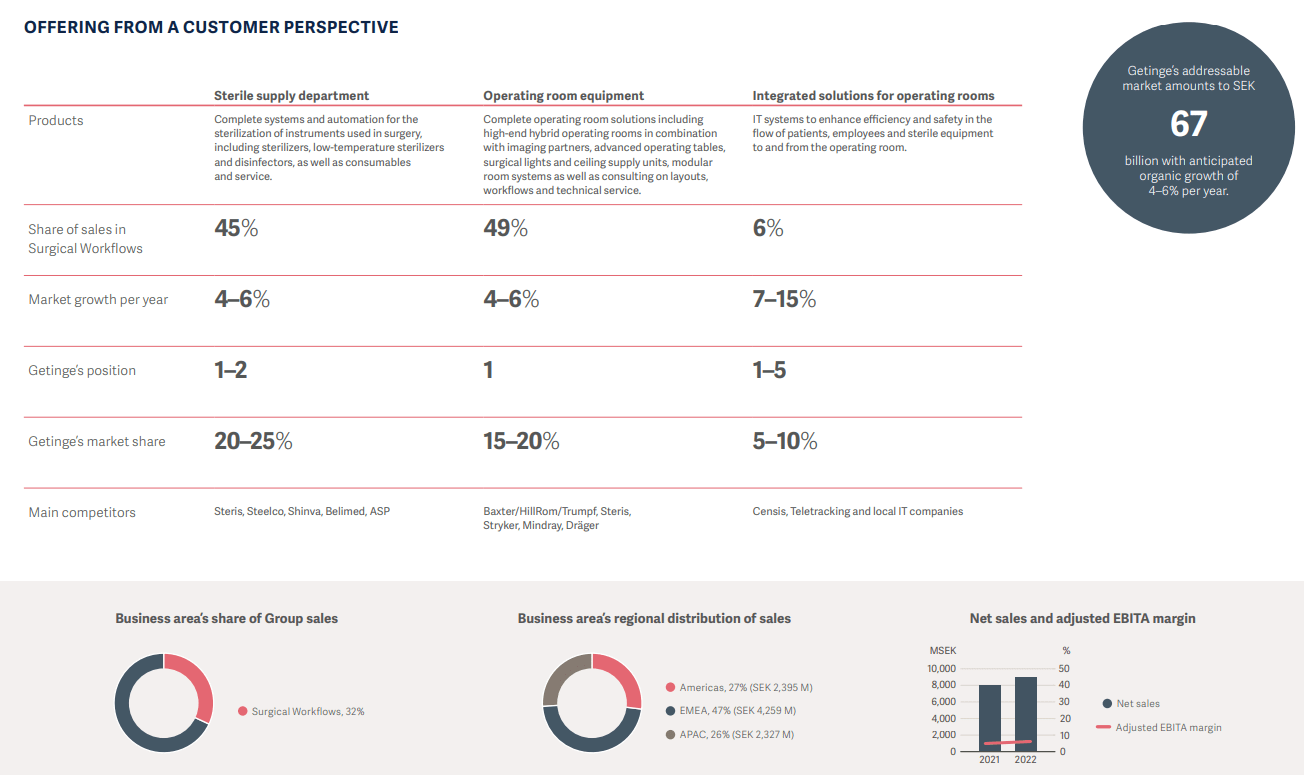

Surgical Workflows

The last revenue segment is an interesting one, most likely set for volatile performance moving forward. Competition is vast for this segment and growth is slower in general than with Life Sciences. However, Getinge touts leading market positions across the board, although the margin of victory is again small compared with peers. STERIS is the closest, far larger peer, but offers a favorable growth profile if Getinge turns their financials around. Therefore, with operational success, I expect this segment to provide strong earnings growth and generate plenty of cash for the necessary anti-competitive investments.

{kind=link}

To Grow Like Peers, Bolt-Ons Necessary

As shown above, Getinge has a fairly mature operational position with leading market positions. However, with maturity comes slower growth. To remedy this, Getinge must seek medium-sized acquisitions and successfully integrate new technologies. Getinge has a fairly decent pattern of supplemental M&A, including Boston Scientific's ( BSX ) Cardiac and Vascular surgery unit in 2007 for $750 million. The problem is that industry headwinds over the past decade, and a lack of major acquisitions, have failed to drive growth in-line with peers. However, one recent high-profile acquisition has signaled a potential policy shift at Getinge:

In its second acquisition of 2023-and its largest in several years-Swedish devicemaker Getinge has set its sights on High Purity New England, which churns out a range of products used throughout the drug discovery and development processes.

High Purity's portfolio includes custom-made single-use assemblies, lab pumps, sensors, bioreactor systems, chromatography columns and other tools and technologies used by biopharma clients to produce novel therapeutics.

While only a $290 million total acquisition price, High Purity signals a deeper focus on the lucrative bioprocessing segment. With competitors such as TMO, DHR, and Sartorius ( SARTF ) looking to drive growth in single-use technologies, Getinge now has the technological advantage to stand apart, rather than get swept under the rug by the better-capitalized giants. The High Purity acquisition is also complementary to Getinge's own expertise in single-use technologies across all revenue segments, and the integrations may in fact drive meaningful financial improvements quite quickly. To see this in action, watch for Getinge to drive both 10%+ organic revenue growth and rising earnings margins in the bioprocessing segment with time.

Houlihan Lokey Presentation

Financial Data Reflects Volatile History

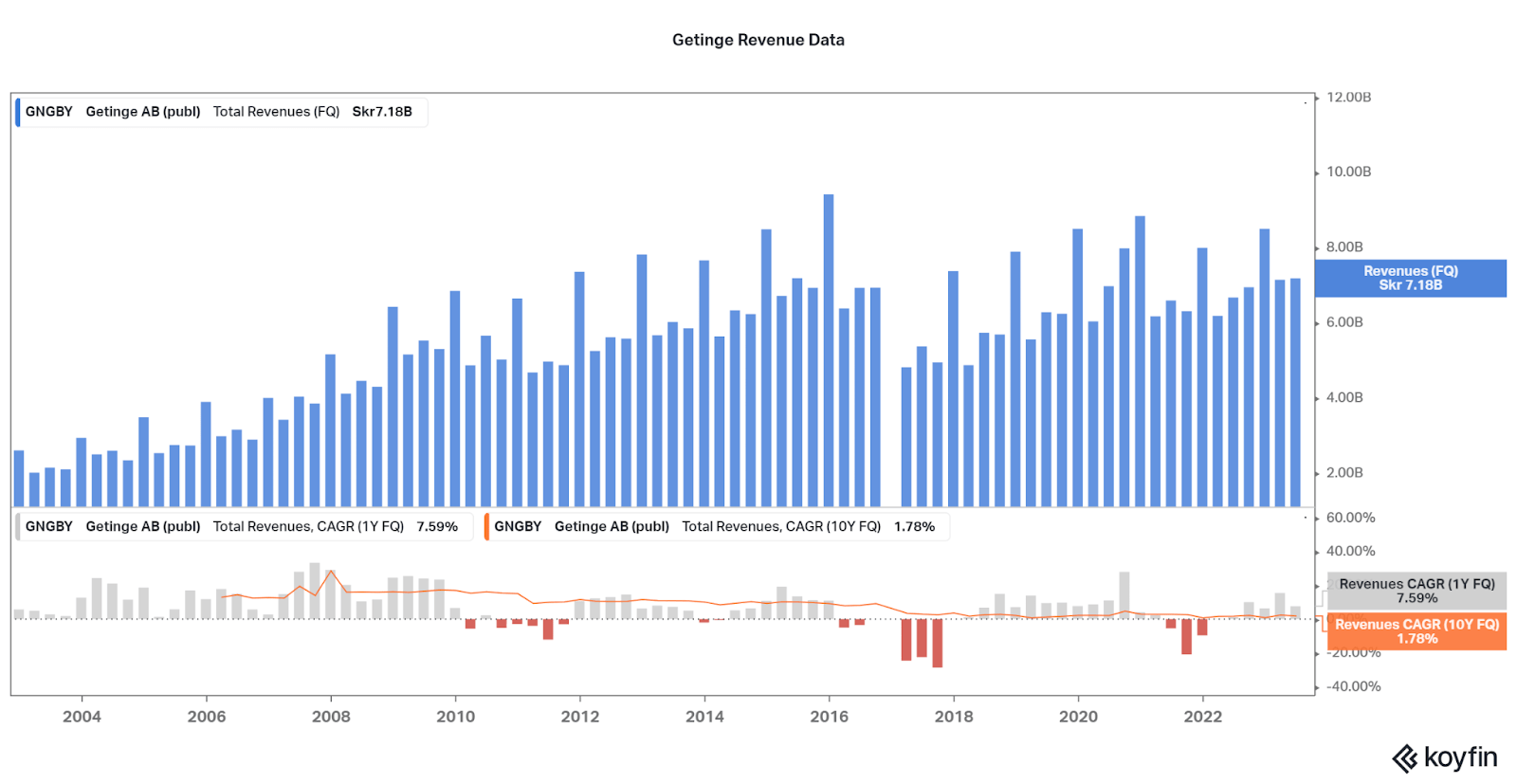

Each of the following charts shows the cyclicality that has prevented Getinge from shining. When looking at the revenue history, there are moments of brilliance, even through the financial crisis period, but the overall trend reflects a lack of inertia. Therefore, the thesis for investors must be based on the fact that Getinge has the tools and resources to bring back growth, especially when the acknowledged headwinds end. I believe that upon normalization, revenues will grow between 5% and 10% per year over the 10-year timeframe.

{kind=link}

Profitability

While revenues have plateaued over the past 10 years or so, earnings have reflected a different pattern. During the acute and surgical care bear market in 2016-18 (similar peers faced weakness at the same time), Getinge saw extremely poor margins. This was an abnormal period, and high margins returned despite the slowdown in growth. Unfortunately, a similar market occurred due to the pandemic and, now, 2023 is shaping up to be hard on company profit generation due to the recalls.

This has created a multi-year era of relatively poor profitability that has driven down the company's valuation. Again, the pieces are there for Getinge to return to the beautiful trend of earnings growth between 2000 and 2015. Therefore, the data suggests that it may be fruitful to take advantage of temporary weakness. However, perhaps the long-term weakness has created an over-leveraged company that is unable to return to the way it once was.

{kind=link}

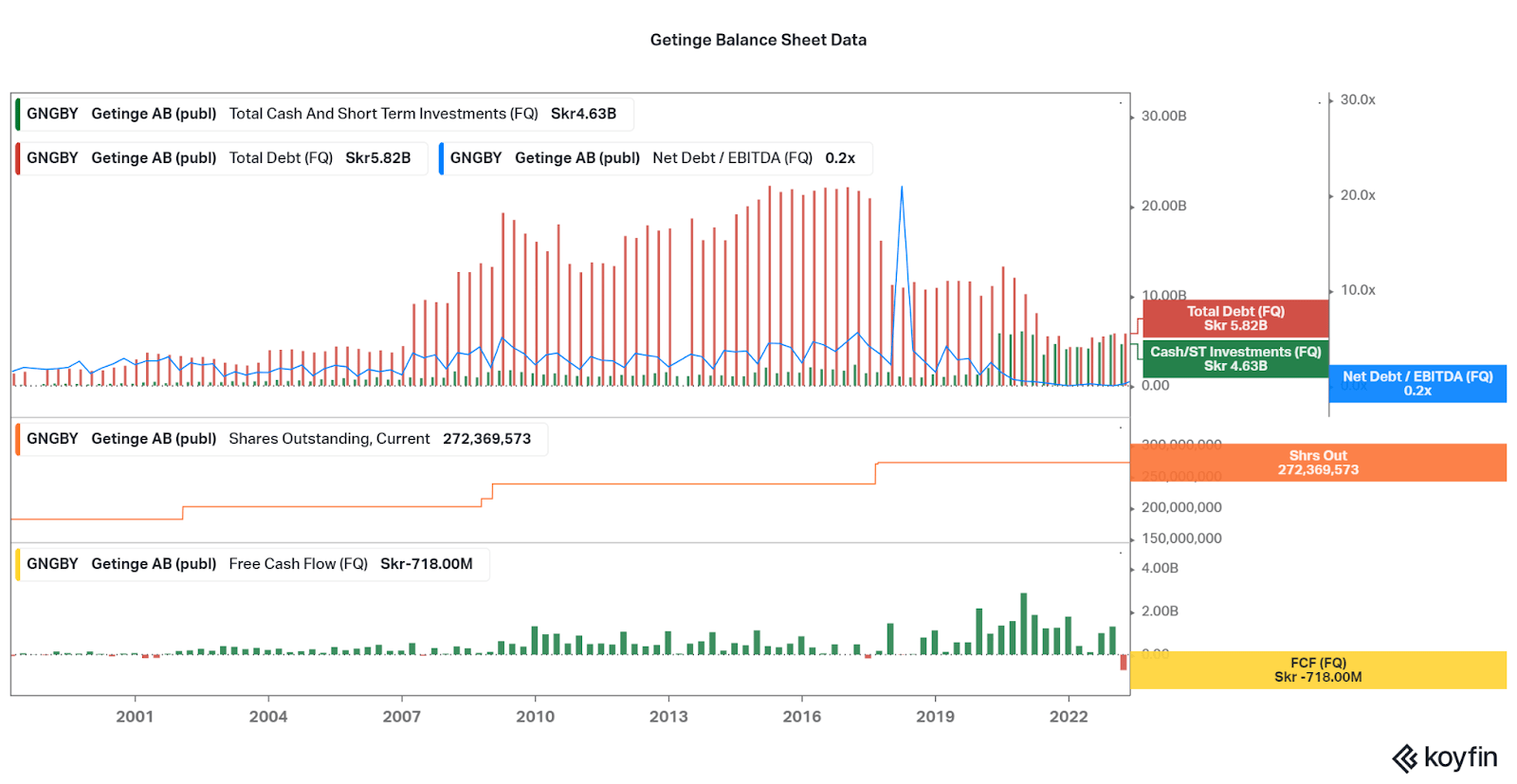

Balance Sheet

Thankfully, this is not the case. As the market soured over the past 5 years, instead of adding to debt, Getinge has instead reduced leverage to all-time lows. Cash on hand now almost equals total debt, and leverage is now 0.2x (net debt / EBITDA). This is the most important financial factor that supports the turnaround play, even more so than acquisitions, market leadership, and industry opportunity. Getinge is just a financially sound company facing short-term issues. Getinge is not alone either, as majors such as Abbott , Medtronic recalls nearly 350,000 defibrillators for risk of reduced shock, and Philips (all have and are facing far larger recalls). Therefore, Getinge should rebound swiftly as the issues are already being resolved.

{kind=link}

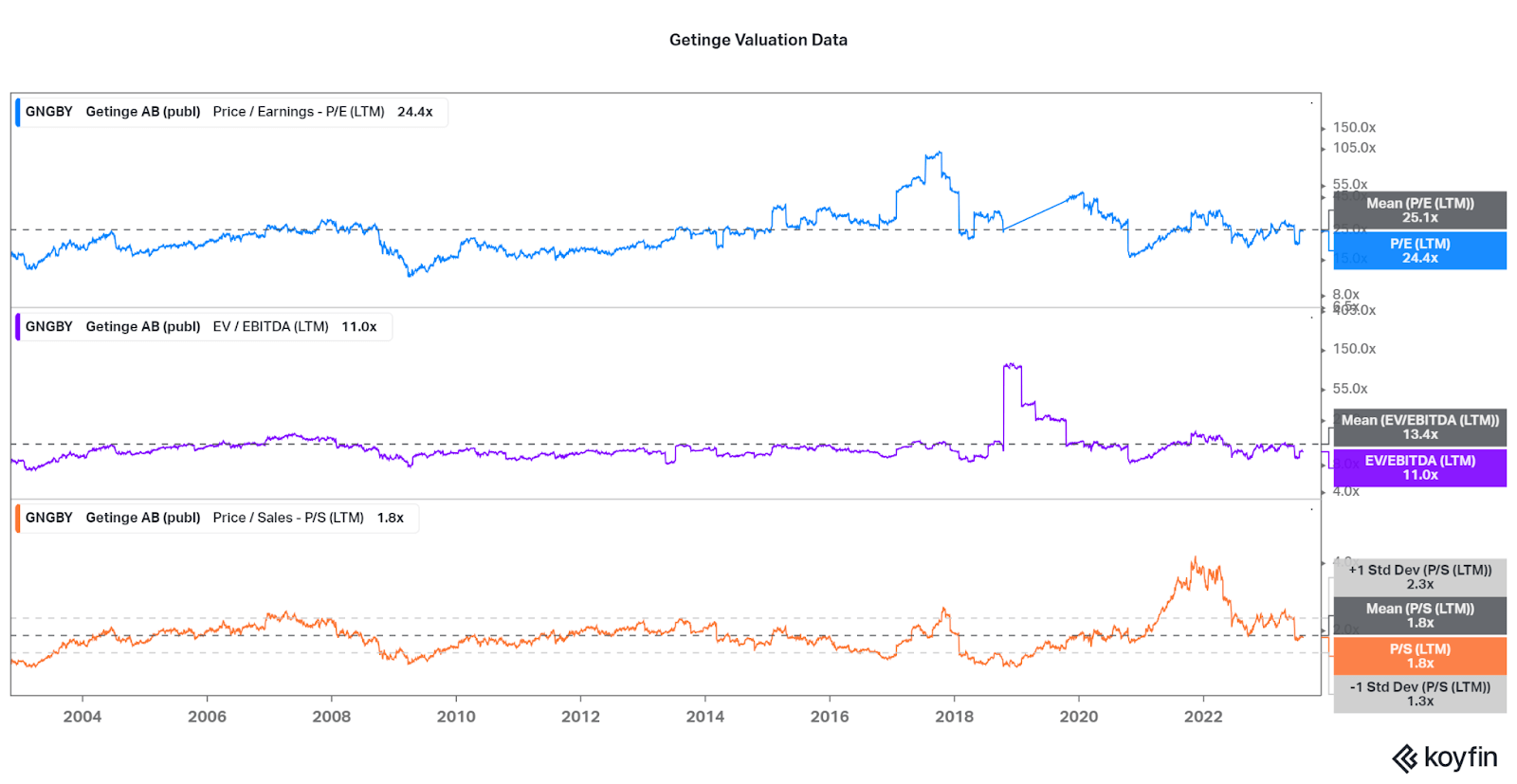

Valuation

Due to the fact that Getinge offers a fairly obvious rebound potential, the valuation is not as low as one may expect. In fact, Getinge is trading close to its long-term average valuation across all metrics. However, this also means that investors can look forward to a return in-line with earnings growth over the coming years. Then, with a return to form, a premium valuation may be earned. I say this because while Getinge may be trading close to the long-term mean valuation, these mean values are far below peers.

Based on the averages below, Getinge has around 60% upside available if taking the average of all the valuation discrepancies between peers. But, the financials will need to improve over a long-term period for the material valuation increase to be justified. Until then, investors should merely trade the upward momentum after recalls are over. In the future, investors can expect the valuation to fall closer to the bioprocessor peers if the High Purity New England acquisition proves to be transformative, or like the medical device peers if a more conservative growth profile emerges. Either way, I believe that Getinge can improve from here.

-

STE, TMO, MKKGY, and DHR Average Valuations: 33 P/E, 19 EV/EBITDA, and 4.5 P/S.

-

MDT, TRUMY, GEHC, and ABT Average Valuations: 30 P/E, 16 EV/EBITDA, and 3.5 P/S.

{kind=link}

Conclusion

The Getinge investment thesis is certainly for more agile investors due to the fact that it relies on unknown future performance. In particular, we do not know the full financial severity of the recent recalls, the impacts on long-term customer favorability, or overall operational health. Getinge may never return to a strong growth profile due to industry weaknesses in acute and surgical care, but I find it unlikely for the bioprocessing segment to face major weakness. Still, the current valuation is not perfect for investors, but I believe the opportunity to be worthwhile.

For me, I will slowly establish a position over the next six months and double down on any major market declines or a bad report. I expect the share price to instead rise on any recall resolutions or with a beat to expectations in the coming quarters. As long as the valuation remains below the historical mean valuation metrics, I believe it is worth adding as financial growth will be the driving factor. I will be sure to update in time as the turnaround play pans out.

Thanks for reading. Feel free to share your thoughts below.

For further details see:

Getinge: Turnaround Catalysts To Outperform Healthcare Peers