VONOY - Getting Ready For A 'Higher-For-Longer' Scenario For REITs

2023-05-15 11:38:53 ET

Summary

- In the past decade, many REITs have become complacent and devised aggressive financing strategies that were underpinned by low interest rates.

- The sudden shift in the interest rates and a probability of a "higher-for-longer" scenario can put a notable share of REITs in a "nuclear winter" territory in my view.

- Nuclear winter is associated with a harsh and a prolonged period of cooling, where the most unresisting crops fail.

- REITs with excessive leverage, tiny margin of safety in the cash flow front and low quality assets face structural risks.

- REIT investors should be cognizant of these elements to shield portfolios from a permanent impairment of capital.

"Nuclear winter" is commonly referred to as a prolonged and harsh global climatic cooling occurring after a system-wide nuclear activity. The cooling effect causes a widespread crop failure - especially for those that are sensitive to fluctuations in the surrounding conditions.

So, why do I think this phraseology is relevant in the context of commercial real estate and more specifically REITs?

First , in the past 10+ years, having an ultra low interest rate policy has been considered a norm. Plus, whenever the prices started to fall or the economy stood at the brink of recession, the Fed stepped in by providing a fresh jolt of stimulus. Namely, low rates and bottom support imposed notable tailwinds for the REITs.

{kind=link}

The chart above captures the essence perfectly. Since the GFC when the Fed assumed an unprecedented dovishness, the overall U.S. REIT sector has moved nowhere but up.

Second , business as usual got disrupted by sudden and aggressive interest rate hikes by the Fed. Prior to March 2022, there was almost a decade when the rates remained extremely accommodative.

From December 2015 to December 2020, we had a very minor interest rate cycle in which the rates got increased by ~2% in an exactly 36-month period. In the grand scheme of things, these hikes were rather welcomed by the market, considering the state of the economy and cautionary characteristics of the interest rate cycle itself.

However, the recent maneuvers by the Fed caught most financial market participants and companies off guard. The pace and magnitude of the prevailing interest rate cycle has cooled the market, sending it into a potentially recessionary environment.

Third , as a result of the completely changed interest rate environment in a combination of consequences from an ultra low interest rate period (e.g., the buildup of excessive leverage), many sectors of the economy are entering a harsh and potentially prolonged recessionary (cooling) period. In these unfavorable dynamics, companies, which are sensitive to slight changes in the systematic conditions, have become increasingly subject to long-term profitability and even going-concern issues.

Now, I am certainly not predicting where the rates will be in the future, but as a relatively prudent investor, I appreciate the historical facts.

Federal Reserve Bank of St. Louis

{kind=link}

If we zoom back and take a look at what levels the Fed funds rate has been historically, ~5% does not seem that low. In fact, the rates have averaged 5.42% from 1971 until 2023. Clearly, there have been years when the rates were even higher and stood there for a prolonged period of time.

In my opinion, investors, who seek stability in a portfolio (either on price or income levels) have to plot a scenario in which interest rates stay at elevated levels for a significant period going forward. And then in the context of such dynamics, answers should be received pertaining to the return prospects of portfolio.

Why are REITs first in line for potential failure?

Let me be clear that I am not saying that all REITs will experience a "doom and gloom" scenario, even if the interest rates continue to climb higher. For example, I am still holding a significant part of my portfolios in equity REITs. Yet, I am confident that a notable chunk of the REIT universe is and gradually becomes subject to a severe financial pain. All this is magnified by the unfavorable interest rate dynamics.

Why is that the case?

- The inherent nature or business of REITs are to fund investments with WACC that are below property cap rates, and to do so in a sizeable fashion.

- One of the key ways to increase the spread between WACC and cap rates is to attract cheap leverage to bring down the WACC.

- Since REITs per definition are forced to distribute most of their earnings to shareholders, where oftentimes a more aggressive dividend policy is assumed to attract investors, there is no ample source of readily available equity.

If we couple the aforementioned dynamics with extremely low-interest rates, it is like injecting a huge dose of steroids into an already risky process, where leverage dominates.

As a result, many REITs have become overleveraged, where the state of balance sheets are not sustainable to survive in the long run provided that the interest rates stay where they are - not even talking about further hikes.

Investors, who have an exposure towards REITs, which carry rather debt-saturated balance sheets and operate on a low margin of safety should be worried about their portfolios. The probability for such REITs sourcing fresh equity at depressed prices to deleverage is very high. In the worst case, REITs that have minimal headroom on the debt covenant front, can face the risk of not accessing the financing at all (or at detrimental rates). This is especially relevant for smaller cap REITs with low quality portfolios, where the access to both capital and traditional financing markets is limited.

Below I will outline three fundamental pillars that, in my opinion, should be achieved when assessing REITs and determining buy candidates. Again, this is very relevant under a potential scenario in which rates stay high for a long period of time. And as mentioned earlier - this is not an impossible or low probability event considering the historical levels.

1. Avoid excessive leverage

This one is quite simple, but one of the most important ones. Having a well balanced capital structure, where the assumed leverage is at relatively healthy level is a key to protecting value.

The optimal level of leverage depends on the sector and the underlying nature of cash flows. However, the most common average for REITs in terms of the leverage profile is a net debt to EBITDA of ~7x (or ~50% leverage ratio). Usually, this is considered a sweet spot to maintain flexibility on the covenants and at the same time generate acceptable yield.

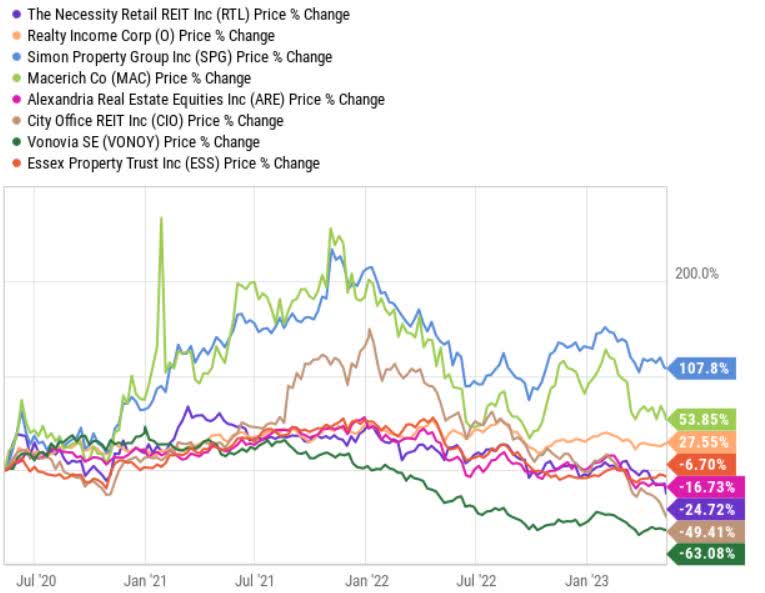

Let's take a look at several pairs of REITs across different sectors to see how the market has treated REITs with healthy balance sheets vs REITs with excessive leverage.

The healthy ones with net debt to EBITDA below 7x and leverage ratio at or below 50%:

- Realty Income Corporation ( O ) - free standing.

- Simon Property Group, Inc. ( SPG ) - regional malls.

- Alexandria Real Estate ( ARE ) - office.

- Essex Property Trust, Inc. ( ESS ) - apartments.

The risky ones with net debt to EBITDA above 7x and leverage ratio above 50%:

- The Necessity Retail REIT ( RTL ) - free standing.

- Macerich ( MAC ) - regional malls.

- City Office REIT ( CIO ) - office.

- Vonovia SE ( VONOY) - apartments.

{kind=link}

Looking at the chart above, for the most part all of the reflected REITs that have entered the COVID-19 and high interest rate environment with stronger balance sheets have outperformed their peers with more debt-saturated capital structures.

On a go forward basis, the notion of having fortress balance sheets will be critical as it will mitigate the need to access external financing at large amounts when the liquidity is weak. Low leverage will also render less of an impact on the cash flows due to a smaller base, which is subject to higher interest rates (costs). Ultimately, if balance sheets are in tact, the risk of worst case scenario - when shareholder-unfriendly equity infusions take place - is significantly decreased.

2. Distant refinancing is good, but not a magic bullet

Many REIT analysts consider a good sign when low cost of debt is locked in for several years ahead due to distant debt maturities. Clearly, this is positive, but at the same time investors should not get complacent. If the scenario of "higher-for-longer" materializes, then eventually all REITs will have to recognize higher interest costs and see whether the cash flows are sufficient to cover all of the expenses and dividends.

Even a slight uptick in the cost of financing level bears a notable impact on the cash flows. Let's take Global Medical REIT Inc. ( GMRE ) as an example.

{kind=link}

An increase of 1.4% in weighted average interest with the leverage remaining more or less stable, the effects on the interest expense component have been massive. The interest costs have nearly doubled imposing headwinds on the underlying FFO figure. Purely due to higher interest rates GMRE faces an elevated probability of dividend cut (see for more details in my article: Global Medical REIT: Dividend Cut Is Coming ).

GMRE's case illustrates perfectly how slight changes in rates can have large consequences.

Let's now take a look at VONOY, which has a net debt to EBITDA above 15x and current cost of financing at 1.5%.

{kind=link}

Since the Fed (and ECB) started to raise rates, the stock just got destroyed by the market. All this has happened, with growing top-line and the cost of financing at only 1.5%.

In my opinion, that market as a future cash flow discounting machine has priced in a convergence to the market level interest rates, which in VONOY's case are at ~6%. The combination of ~ 15x net debt to EBITDA and gradually increasing financing rates put the company at a massive equity dilution risk.

The takeaway here is that the safeness of your REIT and its dividends should be viewed through the lens of at least the prevailing market rates. Otherwise, you are taking an implicit bet that the interest rates will go down and do so before the major refinancings take place.

3. Fly to quality

Looming recession, tightness in banking lending and relatively weak capital market activity inflict damage on REIT stocks from two directions.

First, the access to capital on a reasonable terms is limited. Highly indebted REITs with low quality portfolios, where the durability of cash flows is questioned are exposed to the financing problem the most. While in most cases the capital is attracted, the financing terms can be drastic (i.e., aggressive credit spreads). As stated above, even a slight uptick in the cost financing has a tangible effect on the cash flows.

Second, even if the capital is accessed, the financing terms are unfavorable due to soaring interest rates and structural uncertainty within the commercial real estate sector.

To mitigate the refinancing risk and increase the relative attractiveness of received financing, high quality assets come in handy. If an asset is of a high quality for which there always will be a buyer and / or which generates stable and predictable cash flows, the chances are significantly higher for accessing cheaper capital.

In closing

When the Fed conducted a stimulative policy, REITs thrived and generated superb returns. To a large extent these returns were driven by cheap leverage in massive amounts that warranted a favorable spread between WACC and cap rates.

Many REITs since the GFC have become too leveraged and are on the brink of becoming incapable of servicing dividends and / or maintaining going concern without additional equity injections. We can already see the gap in share price performance between well-managed REITs and those that have too much leverage.

Investors should be prepared for if that "higher-for-longer" interest rate scenario materializes. In such a case, a prudent strategy for risk-averse investors seeking income stability would be to:

- Avoid REITs with excessive leverage.

- Factor in higher interest rate costs into cash flow analysis.

- Invest in REITs with high quality assets.

For further details see:

Getting Ready For A 'Higher-For-Longer' Scenario For REITs