PTY - GHY: Discount Remains Attractive Caution Remains Distribution Coverage Being Weak

2023-04-04 15:27:55 ET

Summary

- GHY is a high yield bond fund with a global focus.

- The fund continues to remain at a deep and attractive discount.

- However, the fund's distribution coverage remains weak.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on April 3rd, 2023.

Despite PGIM Global High Yield Fund ( GHY ) continuing with weak distribution coverage, as I've noted several times now, they continue to pay the same monthly distribution. As we witnessed in the last earnings update for the fund, we once again see coverage slip further.

One reason a fund may continue to pay out a higher distribution to remain attractive is for the consistency to shareholders can come to rely on the payout. Additionally, that consistency can help with the valuation of the fund. At this point, it hasn't helped with narrowing the fund's discount, as that remains at a significant level.

That being said, some derivatives have contributed to positive realized gains. The downside is that these gains were also offset with realized losses in the latest semi-annual report . Generally, we want to see a fixed-income-focused fund delivering a covered distribution from its net investment income.

Since our last update , GHY's trajectory has been much of the same as the broader equity and fixed-income space. That is to say, there was a strong recovery at the beginning of the 2023 year before starting to drift lower once again.

GHY Performance Since Prior Update (Seeking Alpha)

At a large discount, the fund remains an interesting one for investors looking to gain global bond exposure.

The Basics

- 1-Year Z-score: -0.79

- Discount: 12.52%

- Distribution Yield: 11.49%

- Expense Ratio: 1.16%

- Leverage: 18.96%

- Managed Assets: $633 million

- Structure: Perpetual

GHY seeks "to provide a high level of current income by investing primarily in below-investment-grade fixed income instruments of issuers located around the world, including emerging markets."

One of the reasons for coverage declining before was a reduction in leverage. However, since our last update, they've ramped up leverage to $120 million, bringing up the leverage ratio as the portfolio essentially remained flat. In our last update, they had leverage at $85 million. Though they are still down from the $149 million at the end of January 2022.

GHY Asset Stats (PGIM)

One of the main reasons to deleverage would be because of rising interest rates. As rates were rising, the costs of this leverage were also rising. The weighted average interest rates charged in the last six-month report sat at 4.33% for the period ending January 3 1 , 2023. At the end of their fiscal 2022, which ended July 31, 2022 , we saw borrowing costs of 1.17%. That helps provide an idea of just how rapidly leverage expenses would have been rising.

To help compensate for these added costs, they can utilize hedges from derivatives. They can utilize interest rate swaps or go short Treasury futures. With the latest report, we see that they've actually gone long Treasury futures contracts. Those would become profitable if rates declined, which we know after the report they did through March. They also utilize other derivatives that we'll touch on in the distribution section.

Performance - Discount Remains Deep

Despite the fund's global focus, the fund's total NAV returns only lagged behind its U.S.-based PGIM High Yield Bond Fund ( ISD ) sister by a fairly negligible level. On a total share price return basis, they were virtually the same in the last decade.

Ycharts

While the annualized results might look poor, welcome to bond investing. This is basically what a lot of fixed-income funds look like at this point, as the last year saw sizeable declines.

{kind=link}

In the last ten years, GHY has now beaten out the results of the iShares iBoxx $ High Yield Corporate Bond ( HYG ) and the iShares iBoxx $ Investment Grade Corporate Bond ( LQD ). Neither of these represents global exposure, as they are U.S. based.

It was also hard to find another global bond ETF comparison to provide some color, as most are relatively newer. The VanEck Vectors International High Yield Bond ETF ( IHY ) was one I was able to find. As we can see, it performed even weaker.

To add another comparison even further from the CEF space, which could be considered even more relevant, there is also the BrandywineGLOBAL Income Opportunities Fund ( BWG ). BWG has done extremely poorly, and they represent a fund that's invested almost entirely in global exposure, with about 3% listed as U.S. They also focus significantly on investing in governments of emerging markets.

Ycharts

The bottom line here is that GHY has had weak results, but that's bond investing, as we are seeing it today. A big hit came from the ramping up of interest rates at a record pace combined with bonds being able to be issued at rock bottom rates for most of the last decade, with interest rates at zero.

Of course, then there is PIMCO which was able to buck that trend of relatively slim returns. This can highlight why some investors are willing to pay significant premiums for something like PIMCO Corporate&Income Opportunity Fund ( PTY ).

Ycharts

However, we can see that premium has come down, so we see the damage that investing at higher premiums can also have on a fund. I know these funds aren't similar because PTY is a multi-sector bond fund with a higher emphasis on U.S. exposure, but I wanted to highlight why valuations can matter. PTY's total NAV return clearly outperformed GHY in the last decade, but the total share price returns were much closer. That can happen when a fund is trading at a significant premium that comes down sharply.

GHY, on the other hand, had its valuation come down from where it was ten years ago, but it wasn't nearly to the same degree. The fund remains trading just below its decade-long average.

Ycharts

Distribution - Coverage Remains Weak

Thanks to an increase in leverage, the fund's earnings coverage could climb going forward. The latest figures show us that leverage is at $120 million, while leverage averaged around $90.109 million in the last semi-annual report. The spread between what they can earn and what they are paying for the added leverage isn't as attractive as it once was, but bond yields are also higher than they once were. Therefore, we should see some NII increase going forward.

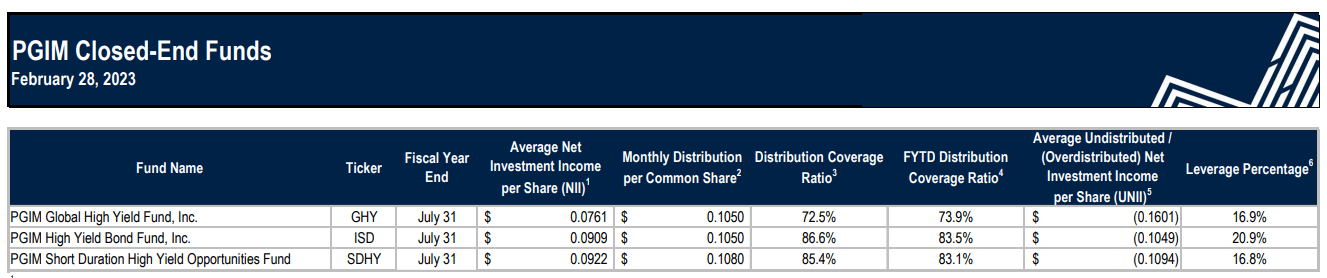

That being said, the latest UNII report from PGIM for their three fixed-income fund shows us that GHY's distribution coverage ratio has shrunk to 72.5% for the quarter that ended February 28th, 2023. So that was a continuation of a declining coverage when we saw the coverage ratio at 76% for the period that ended November 30, 2022.

{kind=link}

That's also above what we see in the semi-annual report for the six months that ended January 31, 2023. That gave us NII coverage of 69%, a decline from the fiscal year 2022, which saw coverage come in close to 75%. The longer reporting time frames can be a better gauge as it can smooth out what a fund is earning.

{kind=link}

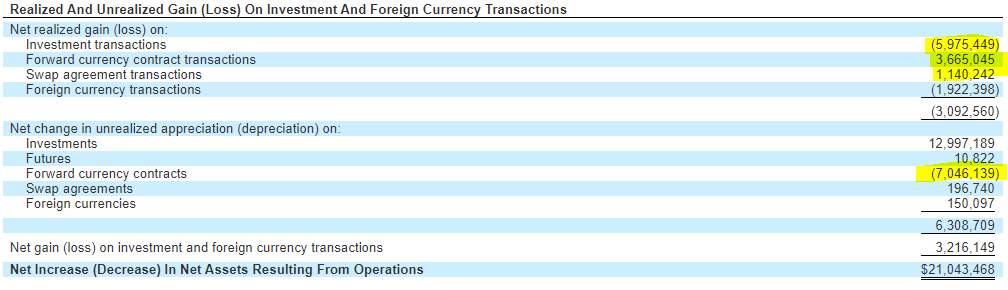

Any of the figures we look at, though, all point to one thing; a lack of distribution coverage. The silver lining is that thanks to some of the derivatives they are utilizing in their strategy, some capital gains are being realized from these contracts.

At least in the latest semi-annual report, forward currency contract transactions and swap agreements have contributed positively to the earnings of the fund. While GHY is a fixed-income fund, these are areas that can generate gains. Additionally, the unrealized appreciation in their underlying investments had a strong upswing in the six-month period being reported.

{kind=link}

However, even though these contracts were delivering gains, we can see that it hasn't all been positive. First, the investment transactions (meaning the net gain of what they bought and sold) were negative. Second, the forward currency contracts that they realized were positive. There were still another $7 million plus in the unrealized losses category. Those losses could eventually be realized if they don't start going management's way.

All that being said, they continue to declare the same monthly distribution. Historically, they've cut before, so they are standing their ground now, perhaps as they expect yields to drop. That would help propel gains in the underlying portfolio holdings as well as their long futures contracts, which could then be realized to cover the fund's distribution.

{kind=link}

GHY's Portfolio

To further help mitigate some of the damage from higher interest rates, GHY had included some exposure to floating rate loans. However, it wasn't a sizeable allocation for the portfolio, and it had a marginal impact. The fund had quite a minimal turnover in the last six months at only around 10%. That puts it on pace for the slowest buying and selling we've seen in the last five fiscal years. In the last five years, the lowest annual portfolio turnover figure was 35% in 2022, and the highest was 96% in 2019.

Since the fund focuses mostly on high-yield investments, it's a natural hedge against higher interest rates because of being less interest rate sensitive. They have relatively lower maturities and higher yields, and that often translates into a lower duration. The leverage-adjusted duration for GHY comes to 4.6 years. Therefore, every 1% increase in interest rates should move the fund down (or up) by about 4.6%.

The trade-off for higher yields is that the portfolio can experience higher defaults. Defaults haven't been rampant or anything, as the economy has been pretty strong so far. That being said, with an expected recession on the horizon, that could see defaults tick higher.

It would come down more to trusting management and expecting them to make quality decisions even in the lesser quality bonds they focus on. BB makes up the largest allocation of its portfolio in terms of credit quality. The CCC debt is one area to watch closely when investing in high-yield funds.

GHY Credit Quality (PGIM)

With the fund's global focus, thus why the fund also has been utilizing currency exchange contracts as a hedge, so an investor can get some added diversification. U.S. exposure is the largest single country exposure by a significant degree, but with only around 50% of the fund, the total means you are getting quite a bit of exposure outside the U.S.

GHY Geographic Breakdown (PGIM)

Some of the debt the fund holds outside of the U.S. is allocated to the issuing country. Several of these are represented in the fund's top holdings, where we see Mexico (Petroleos Mexicanos is state-owned,) Colombia, Dominican Republic, Brazil and Argentina.

GHY Top Holdings (PGIM)

Additionally, the fund is highly diversified, as we can see the fund held 329 different holdings. On top of this, each position remains a fairly small allocation in the fund. Only the Petroleos Mexicanos comprise what could be considered a fairly outsized weighting relative to the allocations of the other holdings. At 2.6% of a weighting, though, on an absolute basis isn't going to make or break the fund.

Conclusion

GHY is an interesting fund for global bond exposure. However, a lack of coverage could see the distribution cut at some point if they can't start producing more NII or have their derivatives pay off. While they continue to maintain the same distribution, it still hasn't seemed to pay off with a narrowing of the discount either. So at this point, it really seems they wouldn't have much to lose but more to gain as they could retain these assets instead of eroding through a higher distribution rate.

For further details see:

GHY: Discount Remains Attractive, Caution Remains, Distribution Coverage Being Weak