ISD - GHY: Discount Widens But Distribution Coverage Remains A Concern

Summary

- Previously, GHY lacked distribution coverage, which hasn't changed; coverage has fallen a bit further.

- The fund has been deleveraging its portfolio, which could be seen as a positive if they can add more at the right time to catch a rebound.

- Since our previous update, the fund's discount has increased, making it somewhat attractive.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on December 22nd, 2022.

PGIM Global High Yield Fund (GHY) hasn't been experiencing a great year, but that's been most equities and fixed-income as a whole. GHY is also struggling with distribution coverage - where some of its fixed-income peers are still showing strong coverage. Primarily, funds from PIMCO, which take a multi-sector bond fund approach, have been doing incredibly well in that department.

One of the reasons for the lack of coverage for GHY could be that they've continually deleveraged through this year. This could ultimately prove to be a mistake or a great opportunity. Leverage amplifies both upside and downside moves. By deleveraging, they would have reduced losses to an extent.

Of course, leverage was still employed, and the fund had experienced losses for the year. However, since our last update , the fund's performance hasn't been too terrible. We see declines, but the fund's discount has also widened out, causing the losses to exaggerate. The S&P 500 isn't an appropriate benchmark, but it can provide some context to the moves experienced.

GHY Returns Since Previous Update (Seeking Alpha)

These wouldn't appear to be forced deleveraging as their leverage levels were rather moderate. At the same time, with less capital invested, that means fewer income-producing bonds they hold. So if they are able to redeploy that capital at the right time to catch a rebound, the fund could benefit longer-term. The main problem is that with distribution coverage being weak, they are reducing capital that they could rebound with later.

While lacking distribution coverage is a huge negative, the fund is also attractively priced at a discount. It seems that investors are already anticipating a distribution cut and heightened potential credit risks heading into next year. The discount has widened out to over its five-year average.

The Basics

- 1-Year Z-score: -1.50

- Discount: 13.67%

- Distribution Yield: 11.53%

- Expense Ratio: 1.16%

- Leverage: 14.09%

- Managed Assets: $603 million

- Structure: Perpetual

GHY seeks "to provide a high level of current income by investing primarily in below-investment-grade fixed income instruments of issuers located around the world, including emerging markets."

This is a fairly straightforward high-yield bond fund with greater flexibility to invest more internationally. Investing outside the U.S. can help provide greater diversification for investors, eliminating "home country bias." In a previous article on GHY, I noted how high the correlation was with its U.S. peer, PGIM High Yield Bond Fund ( ISD ). So despite its global focus, these two had historically shown a high correlation.

Ycharts

The fund's moderate use of leverage continues as they've now taken leverage down to $85 million. In early September, for our last update, they had around $89 million - which was down from the $129 million in April of this year. The fund, on January 31st, 2022, had $149 million. So the management has been quite aggressive in deleveraging throughout this year.

GHY Assets (PGIM)

In fact, so much so that I'm surprised distribution coverage hasn't sunk even further.

One good thing about deleveraging at this time is it keeps interest expenses relatively mild. Most funds are experiencing exploding expense ratios due to higher leverage costs. Of course, not all leveraged funds are impacted the same because some have hedged their leverage costs.

By moderating out through this year, GHY will keep its expense ratio fairly lower too. The latest fiscal year-end showed a total expense ratio of 1.48%. That was for the period ending July 31st, 2022. Since then, interest rates have risen further, so it would be anticipated that the expense ratio will rise.

It is interesting to note how they are playing it differently through this rate hiking cycle. They added leverage when interest rates peaked in 2019 in that hiking cycle. The fund's expense ratio went from 2.15% at fiscal year-end 2018 to 2.56% FY 2019. Their leverage outstanding went from $258 million to $284 million, respectively. It would seem they are taking an overall more cautious approach in the current environment. That could prove prudent as the entire economic situation seems different at this time.

Performance - Attractive Discount

As noted previously, another benefit of moderating leverage is the downside is less amplified. When comparing GHY to the iShares US & International High Yield Bond ETF ( GHYG ), we see that the fund has underperformed on a total NAV return basis. Considering that GHYG is not leveraged, I'd say that GHY is doing fairly well considering that fact.

I would also note that GHY's duration is longer than GHYG's. At 4.5 years compared to 3.81 years. For every interest rate hike, GHY should be more impacted by the underlying price of its bonds declining relatively further.

Ycharts

At the same time, the fund's total price performance has been worse. That's where the discount comes in, which has continued to widen out through this year. In fact, it is wider than the average of the last decade. It also would appear that it is near the widest levels we've seen in this period, too, excluding the sharp spike during COVID. That could indicate that, at least in the shorter term, now would appear to be a relatively attractive time to consider this fund.

Ycharts

To look at the longer-term performance of GHY, it has come out on top relative to some of the other global high-yield fund CEF peers. Below is comparing GHY to Western Asset Global High Income Fund ( EHI ) and AllianceBernstein Global High Income Fund ( AWF ). On a total NAV return basis, GHY came out on top - yet came out in the middle in terms of total share price return.

Ycharts

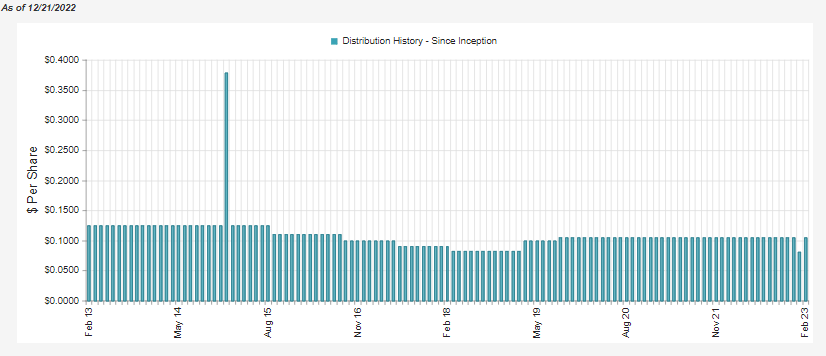

Distribution - Coverage Taking Another Small Hit

The fund has historically not been too concerned with adjusting the distribution as needed. However, with a persistent lack of coverage, it's a bit surprising they haven't adjusted it already.

{kind=link}

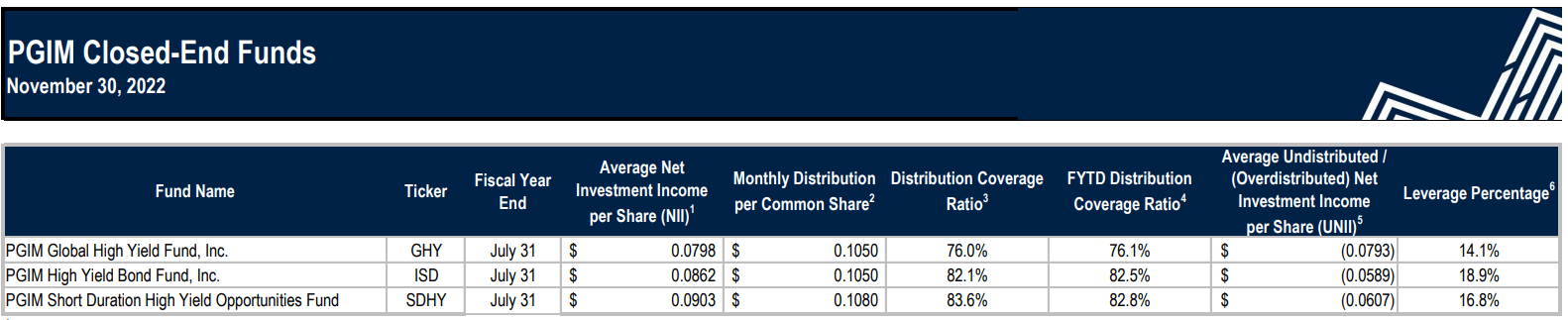

The latest announcement confirms they are moving ahead with the $0.105 monthly distribution at least through February. Previously, distribution coverage was a weak 77.2%. It now comes in at 76% for the last rolling three-month period that ended November 30th, 2022 .

That's both impressive and the biggest disappointment, in my opinion. Impressive because despite taking leverage down, coverage didn't slip all that much. They have some exposure to bank loans, which are generally floating-rate securities that help offset some of the declines we'd see from the reduced assets. Still, at the end of the day, it's a continued shortfall and a continuation of coverage moving in the wrong direction.

{kind=link}

When we look at equity funds, we can expect distribution shortfalls from net investment income. They generally have a better chance of producing capital gains more regularly.

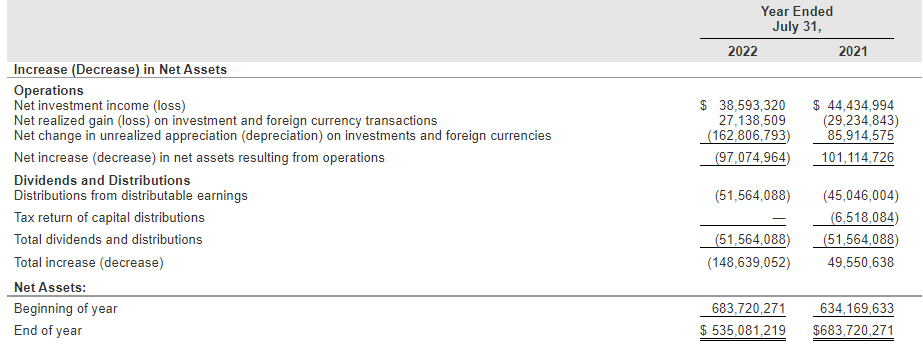

For GHY, being a fixed-income fund, we want to see higher NII distribution coverage. That being said, in the last fiscal year, they were able to cover their shortfall from realized gains. At the same time, the fund's unrealized depreciation still resulted in losses overall.

{kind=link}

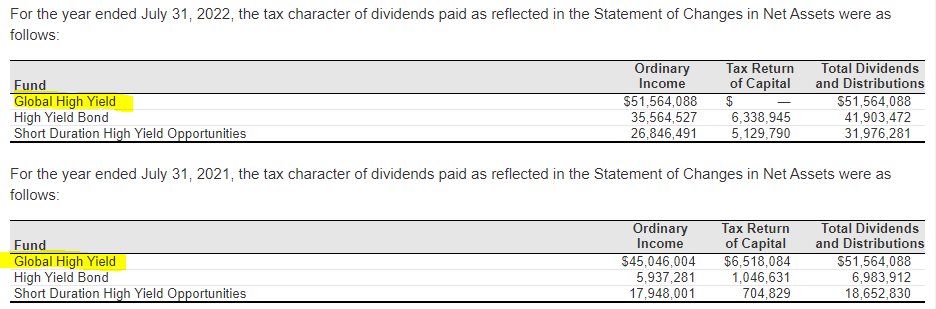

For tax purposes, we see that most of the distribution from the prior two years is classified as ordinary income. This is to be expected as a fixed-income bond fund. That's why it would appear to be the most appropriate for a tax-sheltered account.

However, we also see some return of capital identified in 2021. In this case, it technically wouldn't be considered destructive ROC as the NAV rose during that fiscal year. On July 31st, 2020, NAV per share was $15.50, and on July 31st, 2021, it came in at $16.71.

{kind=link}

GHY's Portfolio

The portfolio turnover rate was 35% which was last reported in their annual report. That's on the lower end compared to the prior years for this fund. So the changes in the portfolio have slowed down more recently, but they are still making some changes nonetheless.

Overall, the fund sticks fairly well by the "global" portion in its name. Over 50% of the portfolio is invested outside of the U.S. Sometimes, some funds call themselves global but have the majority still allocated to the U.S. In this case, you are still getting a tilt outside of U.S. exposure.

GHY Geographic Exposure (PGIM)

I think it is probably worth pointing out here that none of these countries are heavily exposed to the Russian invasion of Ukraine. They are tilted more towards Western Europe, with allocations to U.K. and France.

The fund's largest credit quality exposure is to BB. The fund even carries some exposure to investment-grade bonds in a somewhat material allocation. AAA and BBB combined give us a 12.3% slice in the fund.

GHY Credit Quality Exposure (PGIM)

Although, BBB is only the first rung into investment-grade debt. So definitely tilted toward the lower end overall. CCC also represents a hefty 14.5% of the portfolio. That's quite noteworthy because that's where a lot has to go right for the companies of the underlying debt. Heading into a year that's supposed to bring on a recession, that's a bit concerning. Which is another point that could help explain why the fund's discount has been nearing its widest discount levels.

That's certainly something to watch as it's a negative. On the other hand, we also have the fund representing a fairly diverse portfolio in terms of industry exposure. By spreading out the risks, they can potentially avoid any portion of their portfolio being too large of a drag on performance.

GHY Industry Exposure (PGIM)

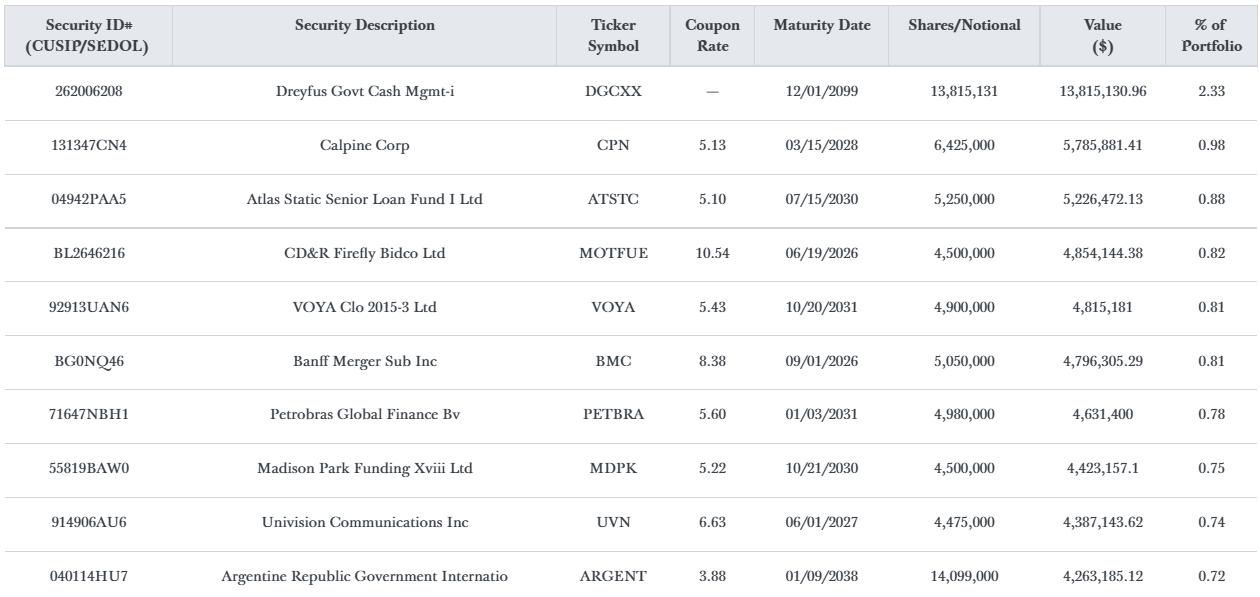

GHY takes the approach of investing in hundreds of positions. According to CEFConnect, they put the number of holdings at 576. With a significant number of overall holdings, that can make each position in the portfolio compose a smaller portion of the capital invested.

This seems to be reflected when looking at the top ten largest exposures. Petroleos Mexicanos takes a fairly large 2.6% weighting of the fund, but after that, the position size dwindles relatively quickly.

GHY Top Ten Exposure (PGIM)

When looking at the top ten, note that this is the largest exposure to each of these entities. Within the portfolio, they can carry several debt instruments of each of the entities listed above. That's why when they note 315 holdings above, CEFConnect can still come up with 576 total holdings.

This can easily be seen when you take a look at their total holdings list. The total holding list also shows us how much money they have sitting in their cash equivalent account. When seeing that, it becomes its largest position at 2.33%. Additionally, we see that when the holdings are broken down to each individual position - after the cash type holding - no position comprises more than 1% of the portfolio.

{kind=link}

Conclusion

Unfortunately, distribution coverage for GHY continues to be an apparent problem. By actively choosing to deleverage their portfolio this year, they've essentially chosen to reduce the coverage that was already in shortfall mode.

However, the silver lining is that the downside should have also been mitigated. They also have more leverage capacity to return to work if they choose to. Coverage could improve drastically if they can time it right to catch the rebound.

I would also say that despite reducing leverage drastically from a year ago, the coverage dip has been relatively mild. January 31st, 2022, they had $149 million in borrowings. Today, it stands at $85 million. Distribution coverage at that time was light at 77.7%, so dropping to 76% is a relatively small drop.

Of course, the trend of lower and lower coverage in the last year has been the main concern. With an ever-growing shortfall in coverage, they are essentially eroding assets away that could rebound later.

An additional positive note is the fund's discount is now getting to a more compelling level overall. That could indicate further discount widening from here could be limited.

For further details see:

GHY: Discount Widens, But Distribution Coverage Remains A Concern