GHY - GHY: Global Diversification Is Important This CEF Can Provide It

2023-10-06 17:54:39 ET

Summary

- The PGIM Global High Yield Fund offers a high current yield of 11.85%, higher than many other options in the market.

- The fund's performance has been disappointing, with shares down 29.42% since the start of last year.

- The fund's diverse portfolio includes below-investment-grade securities from around the world, providing potential for diversification and capital gains.

- Global diversification is important considering the deteriorating financial situation of the United States.

- The fund failed to cover its distribution over the past year so it is uncertain how sustainable the distribution will prove to be.

The PGIM Global High Yield Fund, Inc. ( GHY ) is one of a bevy of options available for investors who are seeking to earn a high level of income from the portfolio assets that they have accumulated over the years. The closed-end fund aka CEF certainly appears to perform this task admirably, as its 11.85% current yield is significantly higher than many other things in the market. In fact, it is higher than just about anything other than other closed-end funds that invest in certain types of debt securities. As such, there is a certain amount of fear that investors tend to have about funds with such high yields, as anytime something manages to get a yield in the double-digits, it might be a sign that the asset will need to cut its distribution.

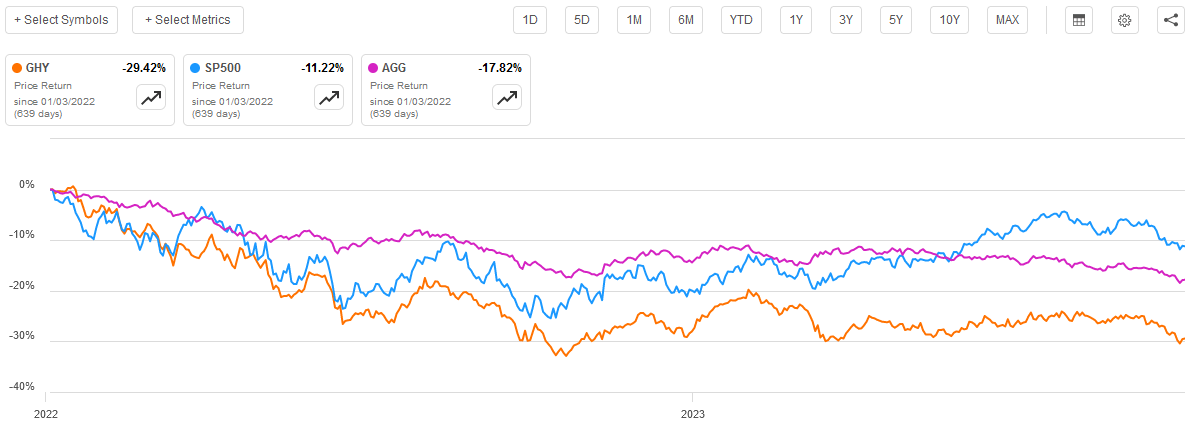

As I have noted in various previous articles, income-focused funds, along with pretty much anything that offers yield as a significant part of its investment proposition, have delivered disappointing performance since the start of 2022. This fund is no exception to this, as its shares are down 29.42% since the start of last year. This is significantly worse than the 11.22% decline in the S&P 500 Index ( SP500 ) or the 17.82% decline in the Bloomberg U.S. Aggregate Bond Index ( AGG ):

{kind=link}

Fortunately, investors in the GHY fund have not actually lost that much because the distributions that the fund paid out along the way offset some of the declines. However, even after we account for these distributions, someone who purchased shares of the GHY fund on the first trading day of 2022 has now lost 15.33% of their money. That is certainly nothing that anyone wants to brag about, but fortunately, there could be reasons to believe that the fund’s performance will be much stronger going forward. After all, the prevailing consensus is that the Federal Reserve will begin cutting rates during the first half of next year, which will cause the price of funds like this one to increase. I will admit that I am less confident of that outcome than the market, though.

With all that said, this fund does have some advantages over some of its peers that could give it a different performance profile over the long term. We should investigate this, as that could result in a very strong case for purchasing this high-yielding fund today.

About The Fund

According to the fund’s webpage , the PGIM Global High Yield Fund has the primary objective of providing its investors with a very high level of current income. This is a very common objective for a fixed-income fund, so that is not really a great surprise. The website further states that the fund seeks to achieve this objective by investing in a portfolio of below-investment-grade securities from around the world. Unlike the websites of most other funds, it does not go into any greater detail than this:

{kind=link}

We can already see a twist compared to many other junk bond funds. In particular, most of them do not invest in foreign securities, and the inclusion of emerging markets is even less common. Nonetheless, this fund does not disappoint when it comes to the inclusion of foreign assets. As we can see here, only 48.7% of the fund’s assets are invested in American securities:

PGIM

This is perhaps the most diverse portfolio of securities that I have ever seen in a global fixed-income fund, at least in terms of country issuance. As I have noted in various previous articles, most of these funds have an outsized exposure to the United States. This one does, too, considering that the United States accounts for a bit less than a quarter of total global economic output, but a 48.7% weighting is substantially less than the 60% to 70% weighting that we see in many other global funds.

This could actually work to the fund’s advantage due to the rapidly deteriorating finances of the United States. In a recent article , I discussed how the high Federal deficits in the United States are likely to continue to starve the private sector for capital. If we assume that the Federal Reserve continues to try and combat inflation, this will result in further interest rate increases due to the supply-demand dynamics in the money market. After all, the only real ways to prevent such a situation are for the Federal Government to slash spending dramatically, which is not possible without cutting mandatory spending, or for the Federal Reserve to resume monetizing the deficit, which will cause inflation.

Thus, it is fair to assume that the long-term interest rate trajectory in the United States is for rising rates and falling bond prices. That will overall not be good for any bond that is denominated in U.S. dollars. As bonds issued by entities in the United States account for the largest percentage of this fund, albeit not the majority, this points to a poor outlook for those bonds over the long term.

However, there are some countries that are in much better shape than the United States. This is especially true in emerging markets. For example, Mexico has a government debt-to-GDP ratio of 49.6%, Brazil has a government debt-to-GDP ratio of 72.87%, and Columbia has a government debt-to-GDP ratio of 63.6%. These countries also have more rapid economic growth than the United States, so their government debt is less of a drag on the private sector or on interest rates. We can see above that issuers from all three of these countries account for some of the largest geographic weightings in the fund.

While the above discussion has focused mostly on the debt positions of the national governments of the countries in which the fund’s issuers are located, the PGIM Global High Yield Fund is mostly invested in corporate bonds. As we can see here, corporate bonds account for about three-quarters of the fund’s holdings, a much higher weighting than government bonds:

CEF Connect

The reason that it is important to understand the debt positions of the respective governments though is because governments tend to be dominant in the markets of any given country. After all, if the given government cannot issue bonds at a reasonable interest rate, then it is a sure bet that no company will be able to accomplish that. For example, can anyone imagine a situation in which any American company will be deemed more creditworthy than the Federal Government? As such, when we have a situation in which the government is running large deficits and the money supply is not growing, it results in private businesses being starved of capital because the government itself is borrowing all of the money available. In such an environment, interest rates tend to rise.

Thus, the fact that this fund is investing in bonds from companies in countries that have governments in stronger financial positions helps to diversify our risks and may, in certain cases, make it easier to obtain capital gains, since the bonds of companies in one country might go up even while American bonds are declining in price.

On its webpage, the PGIM Global High Yield Fund specifically states that it invests in below-investment-grade bonds. These are the securities that are colloquially known as “junk bonds,” and they tend to have a much higher risk of losses due to defaults than investment-grade bonds. This is something that may concern conservative risk-averse investors who are highly concerned about the safety of their principal. However, we may be able to find a certain amount of comfort by looking at the credit ratings that have been assigned to the securities in the fund’s portfolio. Here is a high-level overview:

PGIM

An investment-grade bond is anything rated BBB or higher. As we can clearly see, that only describes 15.6% of the assets in this fund’s portfolio. That is higher than some of the junk bond funds that we have discussed recently. However, it still means that the overwhelming majority of this fund’s assets are invested in junk bonds, which will naturally be concerning to some investors due to the default risks. However, please note that 67.7% of the fund’s assets are rated either BB or B by the major rating agencies. According to the official bond ratings scale , a bond that carries one of these two ratings is issued by an entity that has sufficient financial strength to carry its debt even through a short-term economic shock (such as the worldwide coronavirus lockdowns back in 2020). While a BB or B-rated institution will not quite match the financial strength of an investment-grade one, the risk here should not be substantially worse than an investment-grade company.

Thus, if we combine the weightings of these funds with the investment-grade securities, we get 83.3% of the fund’s assets that should be reasonably safe from default. This is reasonably comforting, especially when we consider that the fund’s largest position only accounts for 2.3% of the fund’s total assets, and that position is a bond issued by the Mexican state-owned oil company.

As such, the real risk here is interest rates . That is a very real risk, especially considering that no country has issuers comprising half of the fund or more. Thus, this fund is exposed to interest rate risks from a variety of different regimes, but that can be both a good and bad thing.

Leverage

One of the defining characteristics of closed-end funds is that they typically employ a variety of strategies that are meant to increase the effective yields of their portfolios well beyond that of any of the assets in the fund. One of the strategies that is employed by the PGIM Global High Yield Fund is the use of leverage. I explained how this works in a number of previous articles. To paraphrase myself:

Basically, the fund borrows money and then uses that borrowed money to purchase high-yield bonds and similar income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I usually would like a fund’s leverage to be under a third as a percentage of its assets for this reason.

As of the time of writing, the PGIM Global High Yield Fund has leveraged assets comprising 22.85% of its portfolio. This satisfies the one-third requirement, and it is actually a bit lower than most other fixed-income or junk bond funds. Thus, the balance between risk and reward seems to be okay here, although it will make the fund’s shares a bit more volatile than they would otherwise be.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the PGIM Global High Yield Fund is to provide its investors with a very high level of income. In order to do this, the fund purchases junk bonds issued by entities around the world. Due to their higher risks compared to investment-grade corporates or government bonds, the yields on these securities tend to be much higher than that of many other things in the market. This fund collects the money from these bonds and even borrows money to purchase more than it can otherwise afford, which has the effect of boosting the effective yield on these assets. The fund then pays out the money that it brings in from the bonds in the portfolio, net of its operating expenses. When we consider the yields possessed by most junk bonds, we can see that this would probably allow the fund to have a very high distribution yield itself.

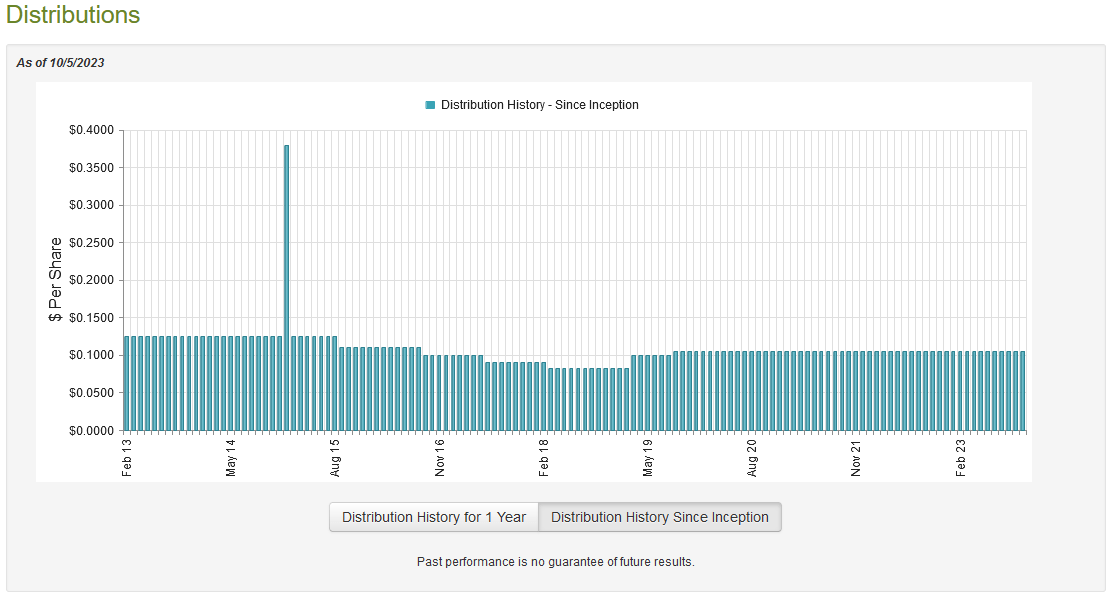

That is certainly the case. As of the time of writing, the PGIM Global High Yield Fund pays a monthly distribution of $0.1050 per share ($1.26 per share annually), which gives it a whopping 11.85% yield at the current price. This fund has not been perfectly consistent with its distribution over the years, but it has done better than most fixed-income funds have managed in this respect. Here is its distribution history since its inception:

{kind=link}

We can see that the fund has increased or decreased its distribution a few times over the years, but it has been much more stable than most fixed-income funds. In fact, this is one of the few fixed-income funds that has not cut its distribution over the past eighteen months as monetary conditions around the world have tightened. Overall, this history might be appealing to someone who is looking for a reasonably stable source of income to use to pay their bills, but as mentioned, it has certainly not been perfect.

As is always the case, though, it is important that we investigate how well the fund is covering its distribution. After all, in many cases in which a fund manages to acquire a double-digit yield, the market expects that it may soon be forced to cut the payout. We certainly do not want to be the victims of such a cut as that would reduce our incomes and almost certainly cause the fund’s share price to decline.

Fortunately, we have a very recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the full-year period that ended on July 31, 2023. This is therefore one of the most recent financial reports available for any closed-end fund on the market, and the fact that it is for a full-year period is even better. This is a period of time that included both the challenging market conditions of 2022 brought about by the Federal Reserve and most other central banks around the world switching from an easy money policy to monetary tightening as inflation took off globally. It will also include the first half of this year, which was generally a very optimistic market in which bond prices were actually rising somewhat in anticipation of rate cuts. The latter of these environments could have provided the fund with the opportunity to make some money by selling appreciated bonds.

During the full-year period, the PGIM Global High Yield Fund received $45,752,954 in interest and $874,535 in interest from the assets in its portfolio. This gives the fund a total investment income of $46,627,489 during the period. It paid its expenses out of this amount, which left it with $34,894,656 available to shareholders. This was, unfortunately, not enough to cover the $51,564,088 that the fund actually paid out in distributions to the shareholders over the full-year period. This is concerning as we generally like a fixed-income fund to fully fund its distributions out of net investment income and this one failed in this task during the period.

However, there are other methods through which a fund can obtain the money that it needs to cover its distribution. For example, it might be able to earn some profits by trading bonds and exploiting changes in their prices due to interest rates or market sentiment. Unfortunately, the fund had somewhat mixed results in this task during the period. It reported net realized losses of $18,060,451, but these were offset by $18,156,960 net unrealized gains.

Overall, the fund’s net assets declined by $16,572,923 during the period. Thus, it failed to cover its distribution during the period, which is very concerning. Fortunately, during the prior year, it did manage to cover the payout out of net investment income plus net realized gains. However, its net assets have now declined for two straight years. It is possible that this fund may be forced to cut the payout, but this is uncertain at the moment.

Valuation

As of October 5, 2023, the PGIM Global High Yield Fund has a net asset value of $11.96 per share but the shares currently trade for $10.61 each. This gives the fund’s shares an 11.29% discount on net asset value at the current price. This is reasonably in line with the 11.49% discount that the fund’s shares have had on average over the past month, and it is overall a pretty reasonable price to pay for the fund. Thus, it could make sense to buy at the current price if this fund interests you.

Conclusion

In conclusion, the PGIM Global High Yield Fund is one of the few closed-end funds that provide access to high-yield bonds issued from entities located in nations other than the United States. This could be good because some of those countries have somewhat more flexibility in their bond markets and they all have very different interest-rate regimes. Thus, the diversification potential could be worth the risk. The fund’s current valuation is also attractive.

The biggest problem here is that the PGIM Global High Yield Fund failed to cover its distribution in the most recent year, so it is uncertain whether or not it will be able to sustain its distribution over the long term. For the moment, though, the fund’s management team appears to be committed to maintaining the payout. However, their ability to do that will depend somewhat on the fund’s performance over the next several months.

For further details see:

GHY: Global Diversification Is Important, This CEF Can Provide It