FCO - GHY: Good International Diversification But Distribution Sustainability Is Concerning

2023-12-12 09:16:54 ET

Summary

- The PGIM Global High Yield Fund offers income-focused investors a way to diversify their portfolio with foreign fixed-income securities.

- The fund's performance has been respectable, with shares up 6.69% since October.

- The fund's net asset value per share is up 5.27% over the past two months, indicating strong gains and the ability to cover distributions in those two months.

- The fund failed to cover its distributions over the trailing two-year period that ended on July 31, which raises concerns about its ability to maintain the payout.

- The fund is currently trading at a very attractive double-digit discount on net asset value.

The PGIM Global High Yield Fund ( GHY ) is a closed-end fund that income-focused investors can employ as a method of achieving their goals. The fund certainly manages to accomplish this goal reasonably well, as its 11.13% yield is easily in line with most domestic fixed-income funds, but this one invests its assets in foreign fixed-income securities. This is something that is very nice to see from a diversification perspective, especially for younger investors or others who are highly concerned about the long-term debt problems currently facing the United States and most other developed Western nations. The comparable yield and international exposure thus allow this fund to easily fit into a portfolio that is focused on generating income by owning debt while reducing an investor’s exposure to any individual nation.

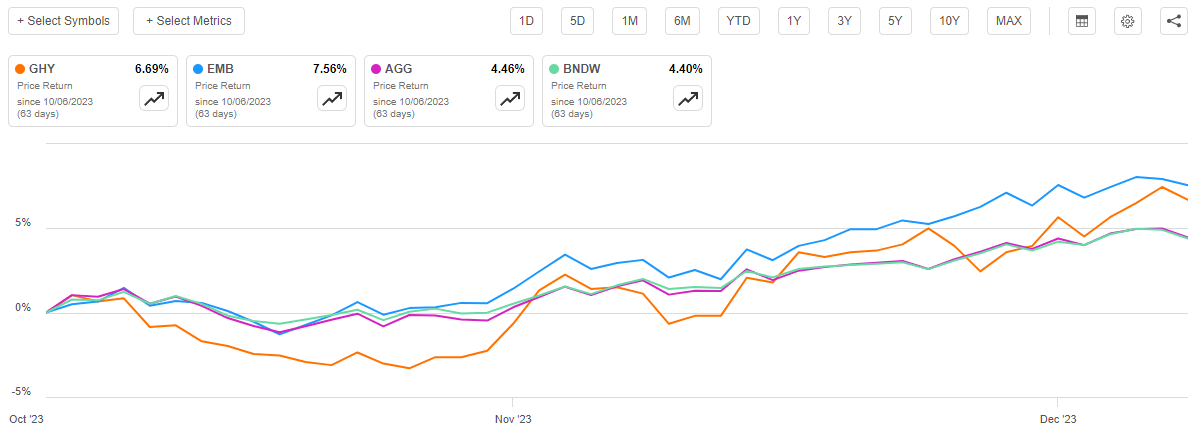

As regular readers can likely recall, we previously discussed this fund in early October so about two months have passed since that article was published. The fund’s performance since that time has been reasonably respectable, as its shares are up 6.69%. This is worse than the J.P. Morgan Emerging Markets Bond Index ( EMB ) but better than most domestic or world bond indices:

{kind=link}

However, one of the interesting things that we have been seeing in the performance tracking of various closed-end funds recently is that share prices have generally been outperforming the fund’s actual portfolio. This is almost certainly being caused by the general euphoria that we have seen in the market since the middle of October. That is, unfortunately, the case here, as the fund’s net asset value per share is only up 5.27% over the past two months. That is still better than the performance of both the domestic aggregate and the world bond indices, though.

That is a very good sign, particularly the fact that the fund’s net asset value is up to such a degree. After all, a rising net asset value per share generally indicates that a fund has managed to cover its distribution over a given period and, in this case, it appears that the fund not only managed to cover all of the distributions that it paid out since we last discussed it, but it managed to accomplish that and still deliver fairly strong gains. This will almost certainly appeal to any investors who are seeking to earn a very high level of current income from their assets.

As such, let us investigate this fund further and see if purchasing it makes sense today.

About The Fund

According to the fund’s website , the PGIM Global High Yield Fund has the primary objective of providing its investors with a very high level of current income. This makes a lot of sense considering the method that the fund employs in order to obtain this high level of income. According to the website:

The Fund seeks to provide a high level of current income by investing primarily in below investment-grade fixed income instruments of issuers located around the world, including emerging markets.

Thus, the PGIM Global High Yield Fund is a bond fund, which is confirmed by CEF Connect:

CEF Connect

As we can clearly see, 95.26% of the fund’s assets are invested in bonds alongside very small allocations to cash, common stock, and preferred stock. As I have pointed out in numerous past articles, bonds by their very nature are income vehicles. Investors purchase bonds at face value, which they receive back when the bond matures. As such, there are no net capital gains over a bond’s lifetime. After all, a bond has no inherent link to the growth and prosperity of the issuing company or government.

Unlike some other global bond funds like the abrdn Global Income Fund ( FCO ), the PGIM Global High Yield Fund does not invest significantly in foreign government debt. Rather, it prefers to focus its investments on debt securities issued by below-investment-grade companies. We can see this very clearly by looking at the industries that comprise the issuers found in the portfolio. From the fact sheet :

Fund Fact Sheet

There are a few things on here that may surprise some readers. In particular, the presence of cable & satellite providers in the top spot. The companies in this industry are occasionally considered to be utilities or very close to it, with stable cash flows and finances. After all, most people in past years had some sort of cable or satellite television in their homes and in the case of cable television, there was usually only one provider operating in a given area. As such, these companies were monopolies that could generally be relied upon to deliver rising earnings and cash flow over time without investors needing to worry about them very much.

Naturally, though, the world is very different today than it was when we were children. “Cord-cutting” is a very real thing today, as the rise of high-speed internet service has allowed households to stream television shows and movies right into their living rooms at a fraction of the cost of cable television. This has been causing a lot of pressure on cable & satellite providers (see here for some statistics). As such, their revenues and cash flows are no longer as reliable as they once were.

There is one domestic cable and satellite provider on the fund’s largest positions list, Charter Communications ( CHTR ).

Fund Fact Sheet

Charter Communications’ revenues have been slowly but surely growing over the past decade, but its gross profit growth certainly leaves something to be desired:

{kind=link}

This is not exactly surprising considering that one of the major motivators among cord-cutters is to avoid the constant bill increases that come with cable and satellite television. These steady price increases are being driven by television networks increasing their carriage fees that are charged to the cable television company. Thus, the above chart showing revenue growth without much gross profit growth is exactly what we would expect to see.

As the chart of the largest issuers in the fund shows, the PGIM Global High Yield Fund does not solely invest in below-investment-grade companies. We do see some sovereign bonds in the fund, including those of Colombia, Brazil, the Dominican Republic, Turkey, and Argentina. There are also some quasi-sovereign bond issues, such as the bonds issued by Petroleos Mexicanos. I explained the concept of a quasi-sovereign bond in a recent article . In short, these bonds are issued by companies that are either wholly or partially owned and majority-controlled by a sovereign government. As such, they are generally going to be much safer than an ordinary corporate bond. That safety may not always mean a whole lot though, as some of the countries shown above have defaulted in the past. In particular, the Latin American debt crisis in the 1980s resulted in numerous sovereign defaults of countries located south of the United States.

As mentioned earlier in this article, the PGIM Global High Yield Fund invests primarily in below-investment-grade securities. These are colloquially known as “junk bonds,” and this is something that might concern more risk-averse investors. After all, we have all heard about the high risk of defaults and by extension losses that these securities possess. The fund’s actual portfolio does indeed reflect this description of its strategy, which we can see by looking at the credit ratings that have been assigned to the securities in the fund’s portfolio. Here they are:

Fund Fact Sheet

An investment-grade bond is anything rated BBB or above, as well as cash and cash equivalents. This description results in 17.1% of the fund’s assets being considered investment-grade. The remainder of the securities in this fund are junk bonds, so obviously that is the overwhelming majority of the fund. However, we can clearly see that 68.2% of the securities in the fund are rated either BB or B. These are the two highest categories of junk bonds, and the official rating scale states that issuers of these bonds have sufficient financial capacity to meet all of their current obligations even in the event of a short-term economic shock. Thus, we can assume that these securities probably do not have an excessively high risk of a default-related loss, although it is certainly higher than an investment-grade security would possess. Still, though, these BB and B-rated securities combined with the investment-grade securities account for 85.3% of the portfolio so it does not appear that investors need to worry too much about losses. This is especially true when we consider that no single issuer accounts for more than 2.4% of the portfolio. Overall, we should not have to worry too much about defaults as any loss should have such a limited impact on the portfolio as a whole that we will not even notice it.

One thing that readers will probably notice is that some of the positions in the fund’s largest positions list are American companies. In fact, 48.4% of the issuers whose securities are represented in this fund are American entities:

Fund Fact Sheet

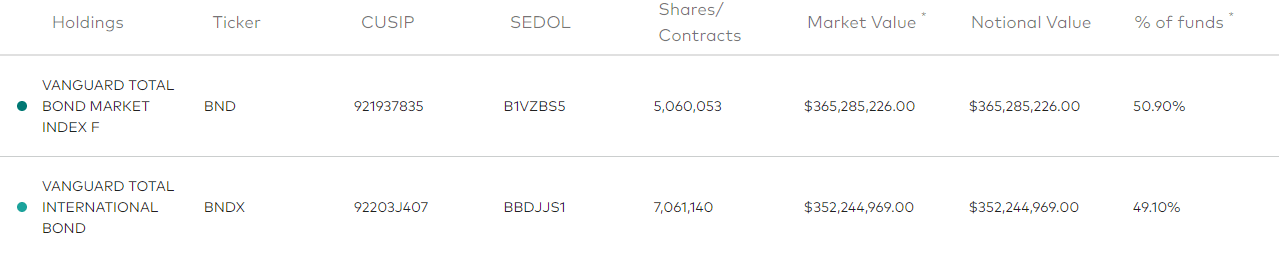

There is obviously no other country with a representation greater than 6%. This is something that could on the surface appear to be going against the fund’s stated goal of investing in securities issued by entities around the world. However, as everyone reading this is likely aware, the United States Federal Government is by far the single largest issuer of bonds in the world, and the low-interest rate environment in that nation that has existed for nearly all of the 21st century has resulted in companies in that nation borrowing tremendous amounts of money from the bond markets. As such, we can expect that American issuers will account for a substantial percentage of the total global bond market. While the exact weighting depends on what index is consulted, the Vanguard Total World Bond ETF ( BNDW ) currently has a 50.9% weighting to American issuers and a 49.10% weighting to foreign issuers:

{kind=link}

We can therefore see that the PGIM Global High Yield Fund appears to be slightly underweight to the United States, which is what we want as part of our efforts to diversify our portfolios internationally. This could be particularly appealing to those investors who are also holding domestic bond market funds, such as the ones that we have discussed over the past two or three weeks.

Leverage

As is the case with many closed-end funds, the PGIM Global High Yield Fund employs leverage as a method of boosting its effective yield beyond that of any of the underlying assets in the portfolio. I explained how this works in my previous article on this fund:

Basically, the fund borrows money and then uses that borrowed money to purchase high-yield bonds and similar income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I usually would like a fund’s leverage to be under a third as a percentage of its assets for this reason.

As of the time of writing, the PGIM Global High Yield Fund has leveraged assets comprising 21.93% of its total portfolio. This is an improvement over the 22.85% leverage that the fund had the last time that we discussed it. This is almost certainly caused by the fact that the fund’s net asset value is up 5.27% since the time that the previous article was published. Thus, a static level of leverage would result in the fund’s leverage being less as a percentage of the fund’s total assets. This is a good sign though, as it suggests that the fund is not borrowing more money as its asset valuations increase.

Distribution Analysis

As mentioned earlier in this article, the PGIM Global High Yield Fund has the primary objective of providing its investors with a very high level of current income. In pursuance of this objective, the fund purchases below-investment-grade securities from companies and governments all over the world. As these are junk-rated securities, they will usually deliver a reasonably attractive yield for a given market situation, and in today’s market, the yield is going to be a lot higher than it was only a few years ago. The fund collects all of the payments that it receives from these securities and combines that money with any capital gains that it manages to realize by exploiting changes in securities prices. The fund then pays this money out to its shareholders, net of its own expenses. As such, we might expect that this would result in the fund having a very high current yield.

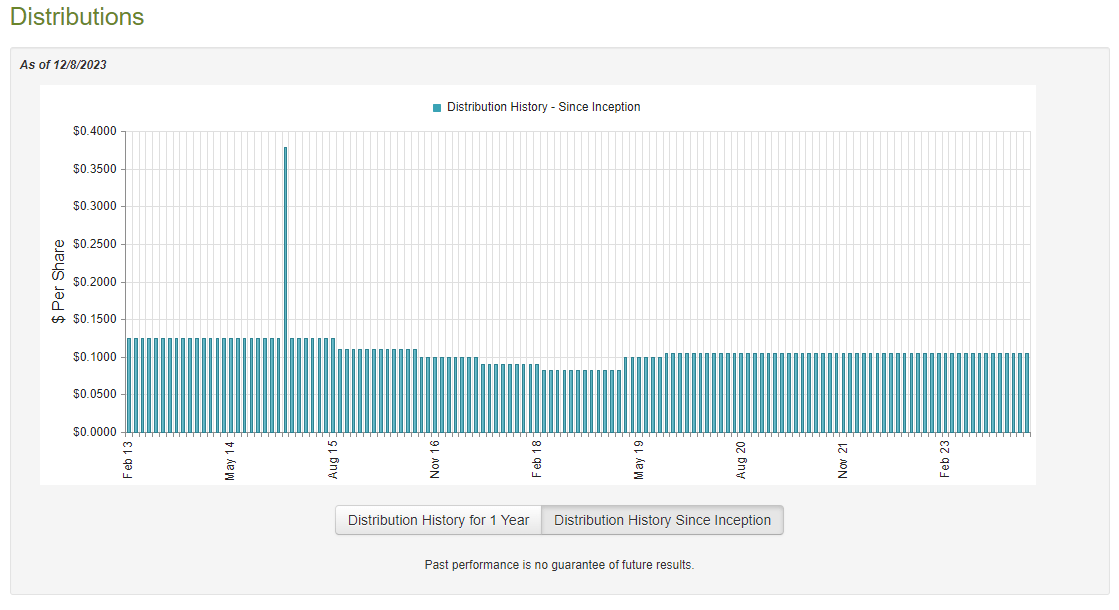

This is certainly the case, as the PGIM Global High Yield Fund pays a monthly distribution of $0.1050 per share ($1.26 per share annually). This gives the fund an 11.13% yield at the current stock price. This is relatively in line with the yield that is currently being offered by most domestic junk bond funds, which works out pretty well for potential investors in this fund. After all, it should be possible to add this fund to a portfolio right alongside domestic junk bond funds without needing to sacrifice income. The fund’s distribution history has been relatively solid too, as it has slowly increased it over the past five years:

{kind=link}

This history seems likely to appeal to those investors who are seeking a safe and consistent source of income to use to pay their bills or finance their lifestyles. It is rather unfortunate that the fund’s history prior to 2018 was not as attractive, however. After all, many income investors are looking for things that they can hold for extended periods of time. This fund has certainly done better than most of the domestic fixed-income funds though, as it is one of the only funds that did not cut its payout in response to the monetary tightening of 2022.

As is always the case, it is important that we investigate how well this fund can sustain its distribution. After all, this is one of the only bond funds that did not cut its distribution over the past two years and that could be a sign that it is over-distributing. After all, it seems pretty unlikely that this fund could accomplish a feat that very few of its peers have been able to.

Curiously, this fund does not include copies of its most recent semi-annual report or annual report on its website. We can obtain them directly from the EDGAR database run by the Securities and Exchange Commission, however. As of the time of writing, the fund’s most recent financial report corresponds to the full-year period that ended on July 31, 2023. This is a pretty good period for the report to cover, as it should give us a rough idea of how well the fund managed to perform during a variety of market conditions. In particular, the second half of 2022 was characterized by the market adapting to tighter monetary conditions than it has seen in twenty years, which caused the value of both stock and bond assets to decrease noticeably. This undoubtedly had an impact on the fund. However, all of this reversed during the first half of 2023, which was a period of optimism that the Federal Reserve would shortly pivot and begin to cut interest rates once again. The market was trading based on this assumption, and the prices of both stocks and fixed-income securities were rising. While the market was ultimately proven incorrect in its assessment, this environment may have provided the fund with the opportunity to achieve some capital gains by trading in the rising asset prices.

During the full-year period, the PGIM Global High Yield Fund received $45,752,954 in interest along with $874,535 in dividends from the assets in its portfolio. This gives the fund a total investment income of $46,627,489 during the period. It paid its expenses out of this amount, which left it with $34,894,656 available for shareholders. That was, unfortunately, nowhere near enough to cover the $51,564,088 that the fund paid out in distributions during the period. At first glance, this is likely to be concerning as we normally like a fixed-income fund to be able to fully cover its distribution with net investment income. This fund is clearly failing to do that.

However, there are other methods through which the fund can employ to obtain the money that is needed to cover the distribution. For example, it might be able to earn some money by exploiting changes in asset prices when interest rates or market mood changes. Realized capital gains are not considered to be part of investment income for accounting or tax purposes, but they obviously represent money coming into the fund that can be distributed to investors. Unfortunately, the fund did not have a great deal of success at this task during the period. The fund reported net realized losses of $18,060,451 during the period but these were fully offset by $18,156,960 net unrealized gains. The fund’s net assets still declined by $16,572,923 after accounting for all inflows and outflows though. As such, the fund clearly failed to fully cover its distributions. The fund also failed to fully cover its distributions during the preceding full-year period. As such, the distribution might be strained and at risk of a cut in the near future.

Valuation

As of December 7, 2023 (the most recent date for which data is currently available), the PGIM Global High Yield Fund has a net asset value of $12.61 per share but the shares currently trade for $11.32 each. This gives the fund’s shares a 10.23% discount on net asset value at the current price. That is not nearly as good as the 11.62% discount that the shares have averaged over the past month, but it is still a double-digit discount and as such is a reasonably attractive entry point for anyone who wishes to add the fund to their portfolio today.

Conclusion

In conclusion, the PGIM Global High Yield Fund is a reasonably solid closed-end fund that provides its investors with a pretty good way to diversify their income-producing portfolio internationally without needing to surrender any potential yield. The fund still does have some American exposure, but more than half of its assets are invested in debt securities from foreign issuers, so it is one of the better funds in terms of international exposure. The current discount is also quite attractive. Unfortunately, the fund failed to cover its distribution over the past two full-year periods and it is uncertain if it will be able to sustain it and avoid a cut in the near future.

For further details see:

GHY: Good International Diversification, But Distribution Sustainability Is Concerning