PGTI - Gibraltar Industries: Still Worth Considering Despite Weakness Ahead

Summary

- Gibraltar Industries has done well for itself and its investors in recent years, with sales and cash flows generally rising.

- This is great to see, but there are signs of weakness ahead in the form of a reduced backlog and lower sales volume.

- Given how shares are priced, though, the company does seem to offer some upside potential from here.

One fairly small but diverse industrial firm for investors to consider is a company called Gibraltar Industries ( ROCK ). The company provides its products and services to customers spread across a variety of industries. Leveraging the benefits of diversity, the company has succeeded in growing its top line while maintaining, for the most part, stable bottom line results, with some of its cash flow data even showing growth in recent years. Although not the cheapest player in its space, the company is also cheap enough to warrant some attention from investors. At the end of the day, I wouldn't exactly call this business a prime prospect that will generate returns that are significantly above market. But I do think that it is attractive enough to warrant a soft 'buy' rating at this time, a rating that reflects my belief that shares should marginally outperform what the broader market achieves for the foreseeable future.

A diverse play

According to the management team at Gibraltar Industries, the company operates as a manufacturer and provider of products and services for a variety of customers in a variety of industries. These industries include the renewable energy space, the residential space, the agriculture technology space, and infrastructure. The firm makes its goods and services available through the utilization of the 34 facilities in its portfolio. The list includes 25 manufacturing facilities, a single distribution center, and eight offices, with its assets collectively spread between 16 states, Canada, China, and Japan. To really understand the company, however, it would be helpful to dig into each of its operating segments one at a time. The first of these segments is called Renewables. Through this segment, the company designs, engineers, produces, and installs solar racking and electrical balance systems. The specific applications for these offerings include commercial and distributed generation scale commercial solar installations, with end users largely consisting of solar developers, power companies, and solar energy engineering, procurement, and construction contractors. Using data from its 2021 fiscal year, this segment accounted for 32.3% of revenue and 15% of profits for the enterprise.

Next in line, we have the Residential segment. Through this, the company sells roof and foundation ventilation products, single-point and centralized mail systems and electronic package solutions, retractable awnings and gutter guards, and trims, flashings, and other accessories. As you can imagine, this segment largely caters to the residential market, with new construction and repair and remodeling customers at the top of the list. This is the largest segment for the company, accounting for 47.4% of revenue and an impressive 79% of profits. The Agtech segment of the company provides growing and processing solutions such as the designing, engineering, producing, full-scope construction, maintenance, and support for greenhouses, and other indoor growing operations. Large-scale indoor produce growers, cannabis growers, retail garden centers, conservatories, botanical gardens, and other similar organizations are its primary customers here. In 2021, this segment accounted for 14.9% of the company's revenue but actually generated a modest operating loss. And finally, we have the Infrastructure segment. This unit is responsible for engineered solutions for bridges, highways, airfields, and other similar assets. Its work includes providing structural bearings, expansion joints, pavement seals, bridge cable protection systems, and more. This unit accounted for only 5.5% of revenue but for 6.7% of profits in 2021.

{kind=link}

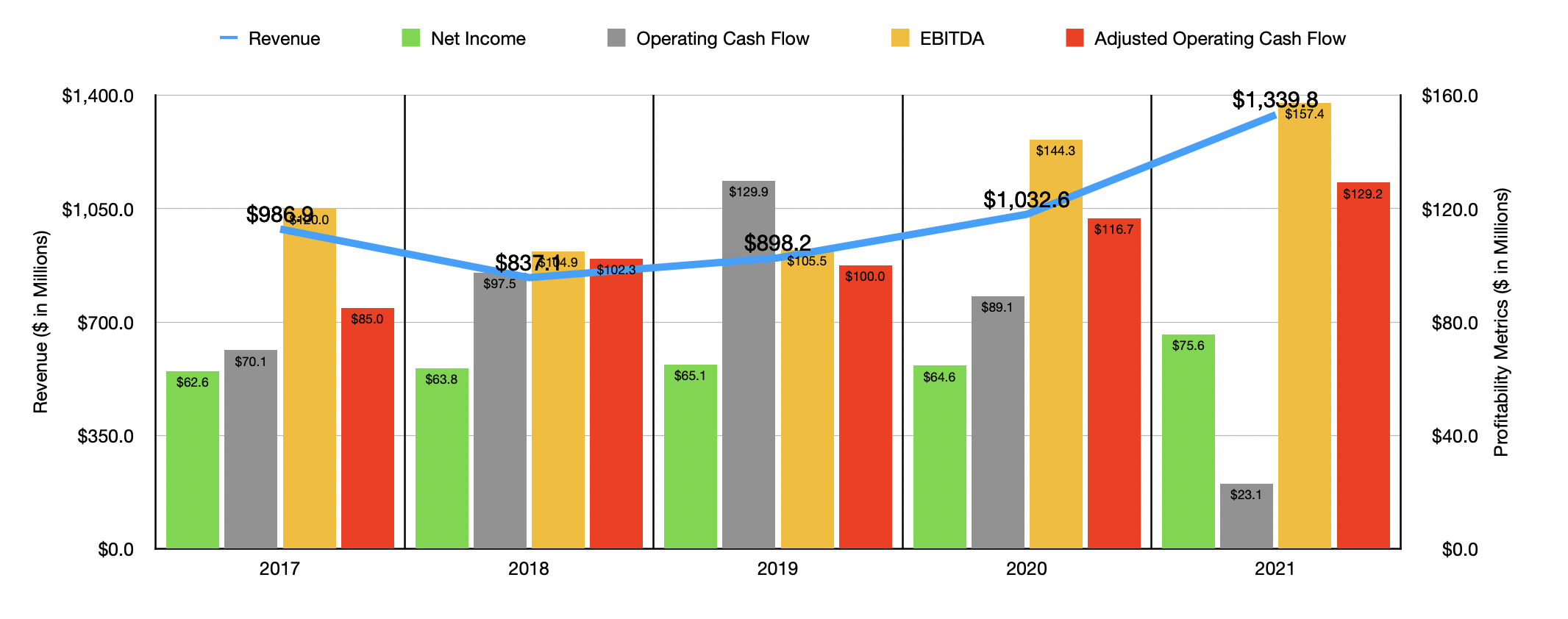

The general trajectory for the company has been, over the past few years, quite positive. Even though revenue dropped from $986.9 million in 2017 to $837.1 million in 2018, the trend since then has been positive, with the metric ultimately hitting $1.34 billion in 2021. The 2021 figure represents a 29.8% increase over what the company achieved in 2020. It is worth noting that the vast majority of this growth came from multiple acquisitions that brought on $215.7 million in additional revenue for the company. Organic growth was a more tepid 8.9%, driven by price increases that added 5.9% to sales while volume grew by 3%. It is worth noting that, despite economic conditions, backlog for the company ended the 2021 fiscal year at $344 million. That compared favorably to the $297 million experienced one year earlier.

Bottom line results for the company have been a bit more mixed. Between 2017 and 2020, net income for the business remained in a fairly narrow range of between $62.6 million and $65.1 million. Then, in 2021, profits popped up to $75.6 million. Operating cash flow has been far more volatile, peaking at $129.9 million in 2019 before dropping over the next two years to hit only $23.1 million in 2021. If we adjust for changes in working capital, however, the metric would have risen in four of the past five years, ultimately climbing from $85 million in 2017 to a high of $129.2 million in 2021. A similar trajectory can be seen by looking at EBITDA, with the metric rising from $120 million in 2017 to $157.4 million in 2021.

{kind=link}

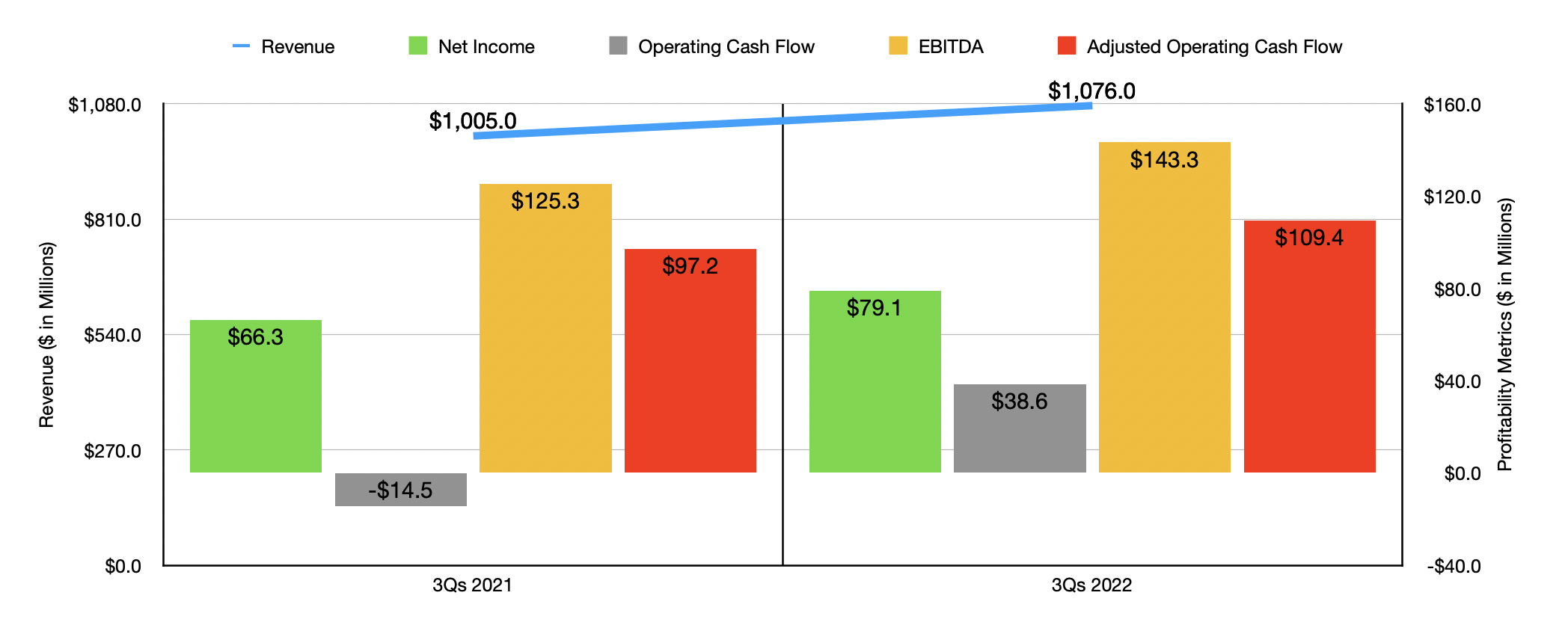

Growth for the company continued into the 2022 fiscal year. In the first nine months of the year , sales came in at $1.08 billion. That represents a modest increase over the $1.01 billion reported the same time one year earlier. This increase, totaling about 7% in all, which is driven by a 6.8% increase in organic revenue and a 1.1% increase associated with acquisition activities. Increased pricing in some of its segments also helped, but this was offset some by a 7% decline in volume, indicating that there might be some weakness in the space right now. Further weakness can be seen by looking at backlog. At the end of the third quarter of 2022, backlog totaled $358 million. Although this represents a nice increase over what the company had at the end of its 2021 fiscal year, it was still down 7% compared to the $385 million reported one year earlier. With the rise in revenue came increased profitability. Net income grew from $66.3 million to $79.1 million. Operating cash flow turned from negative $14.5 million to positive $38.6 million, while the adjusted figure for this grew from $97.2 million to $109.4 million. And finally, EBITDA also increased, rising from $125.3 million to $143.3 million.

When it comes to the 2022 fiscal year in its entirety, management has provided some guidance . They currently anticipate revenue of between $1.38 billion and $1.43 billion. Earnings per share, meanwhile, should be between $2.90 and $3. Using the most recent data available, this would translate, at the midpoint, to net income of $91.4 million. There is a possibility that this calculation could be a bit aggressive. I say this because, from May of 2022 through the end of September of 2022, the company repurchased 1.33 million shares totaling $55.5 million in all. Unthinkable that the company could have bought more shares back in the final quarter. We have no guidance when it comes to other profitability metrics. But if we annualize results experienced in the first nine months of the year, then we should anticipate adjusted operating cash flow of $145.4 million and EBITDA of $180 million.

{kind=link}

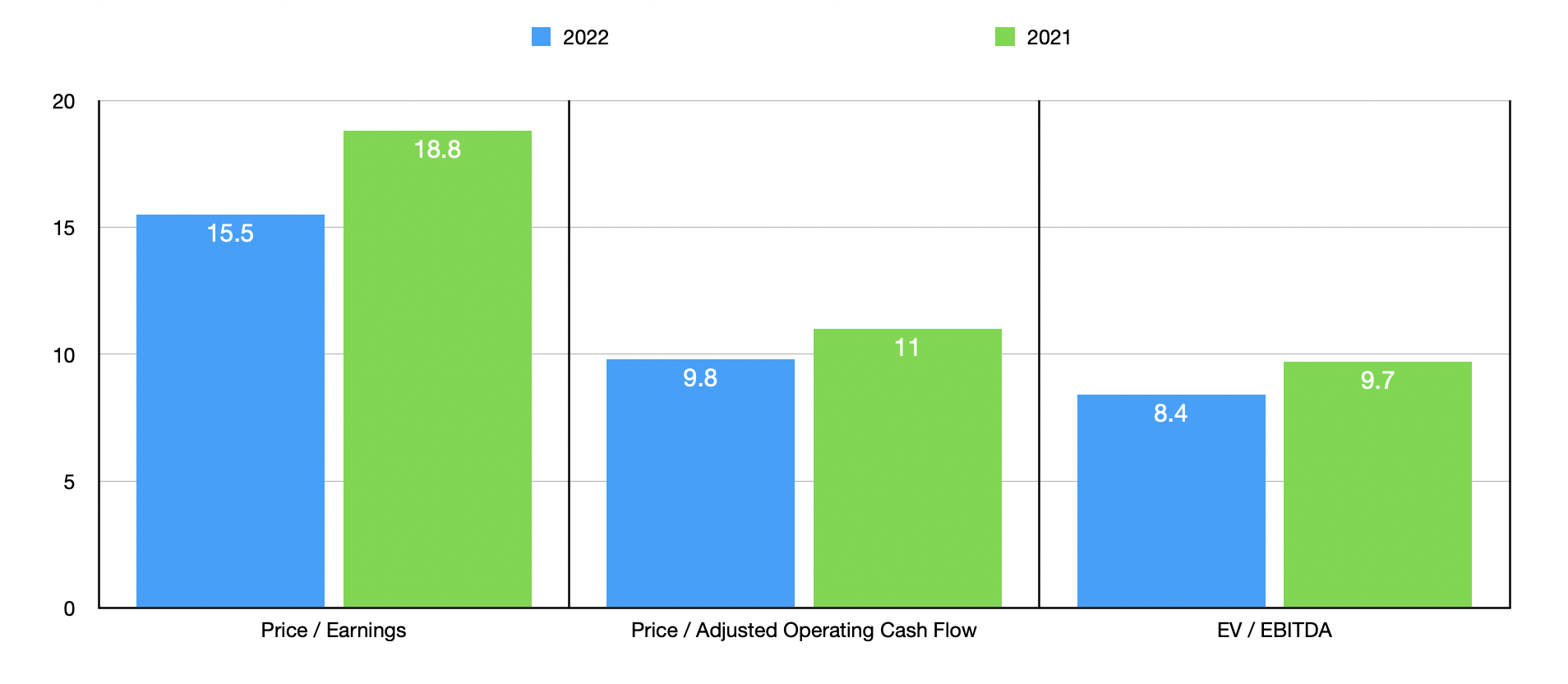

Based on these figures, I calculated that the company is trading at a forward price-to-earnings multiple of 15.5. The forward price to adjusted operating cash flow multiple comes out to 9.8, while the forward EV to EBITDA multiple should be 8.4. As you can see in the chart above, these numbers are lower than if we were to use data from 2021. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 10.5 to a high of 22.8. And using the EV to EBITDA approach, the range was from 6.6 to 13.5. In both scenarios, three of the five companies were cheaper than Gibraltar Industries. Finally, using the price to operating cash flow approach, the range was between 5.5 and 25. In this scenario, only one of the five firms was cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Gibraltar Industries |

| 15.5 |

| 9.8 |

| 8.4 |

| Janus International Group ( JBI ) |

| 16.6 |

| 18.1 |

| 10.6 |

| Tecnoglass ( TGLS ) |

| 12.3 |

| 12.8 |

| 7.6 |

| PGT Innovations ( PGTI ) |

| 10.5 |

| 5.5 |

| 6.6 |

| CSW Industrials ( CSWI ) |

| 22.8 |

| 25.0 |

| 13.5 |

| Masonite International ( DOOR ) |

| 11.7 |

| 13.5 |

| 6.9 |

Takeaway

I can understand why investors would be worried about anything related to the construction space. After all, that market could be hit very hard moving forward. And we are already seeing some signs of weakness, such as decreased backlog, at Gibraltar Industries. But it's important to note that the company is a diverse player and that shares are cheap on an absolute basis even though they might be closer to fair value compared to similar firms. All things considered, I wouldn't be surprised if the company shows some pain in the near term. And for some investors, that may be a good reason to stay away. But when factoring in the current price of the stock and the high likelihood that the firm will weather this storm, I think that it could make for a decent 'buy' prospect for long-term investors.

For further details see:

Gibraltar Industries: Still Worth Considering Despite Weakness Ahead