GBNXF - Gibson Energy Offers An 8% Dividend Yield Even After An Expensive Acquisition

2023-10-13 10:30:00 ET

Summary

- Gibson Energy made a large acquisition in the US to diversify its operations, but the share price has dropped below C$20.

- The company remained profitable and generated C$82.5M in distributable cash flow in Q2.

- The acquisition of the South Texas Gateway Terminal was expensive and may not be as accretive as initially thought. But in the longer run, it will be a good deal.

Introduction

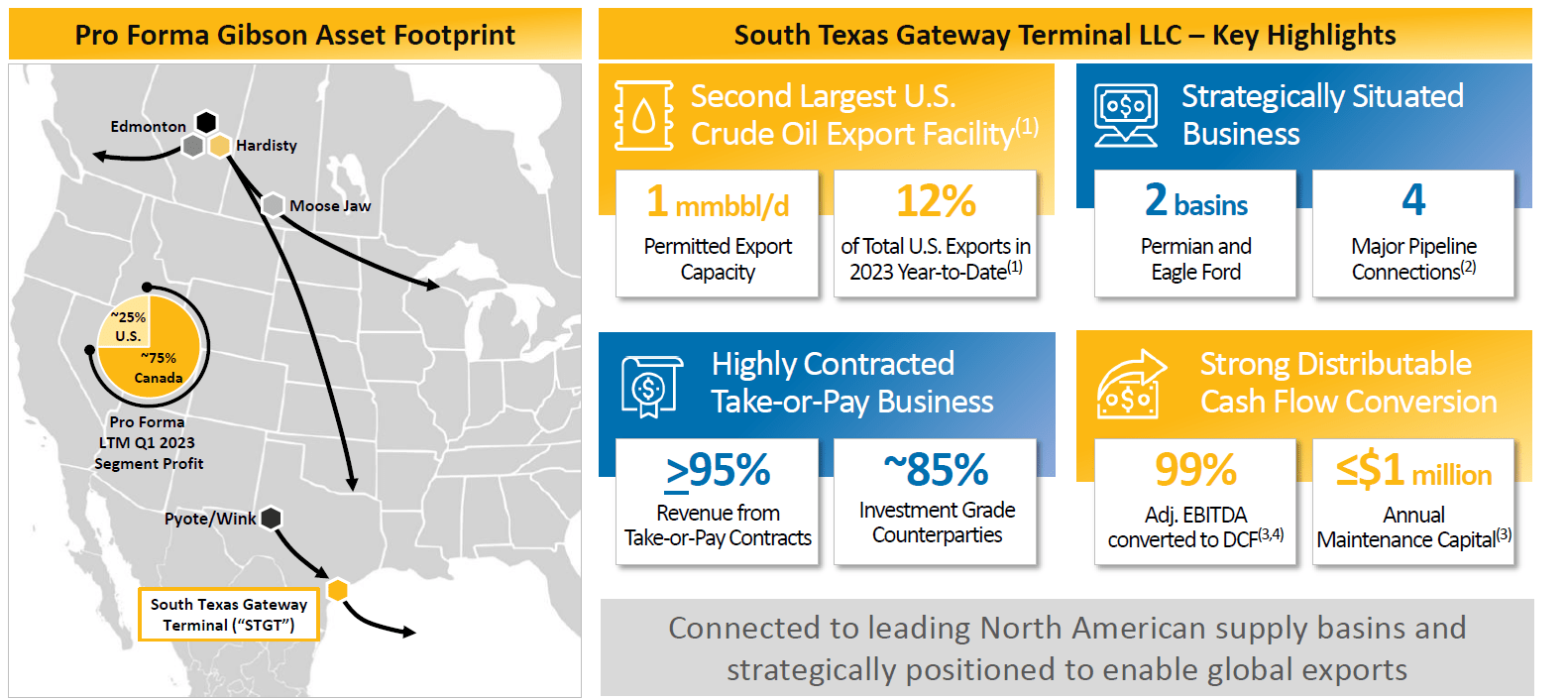

Earlier this year, I made a case for Gibson Energy ( GEI:CA ) ( GBNXF ) as it was an overlooked oil infrastructure play with a robust operating history and strong contracts in place. The company was generating a substantial amount of free cash flow and paid a generous dividend with a relatively low payout ratio. That was attractive, but back in June, Gibson announced a very large acquisition in the US to diversify its operations. It forked over almost C$1.5B to acquire the South Texas Gateway Terminal , the second-largest oil export terminal in the US and one of the only two terminals in the US that are able to load two VLCCs per day.

The acquisition wasn't cheap. Gibson was trading at less than 8 times its distributable cash flow (using the pre-announcement share price of C$22) while its acquisition came with a price tag of 11 times DCF. However, the share price is now trading below C$20 (at the time of writing this article), and that makes the consolidated entity attractive once again.

Gibson confirmed its strong position in the second quarter

Before discussing the acquisition and the impact on the financial results in more detail, I wanted to have a look at Gibson as a standalone company first.

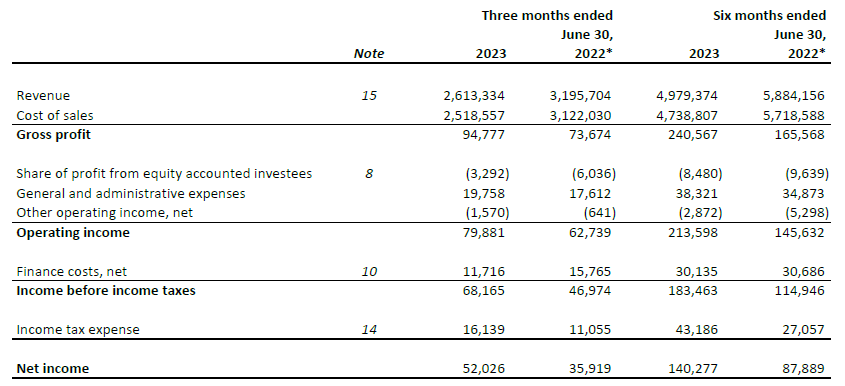

The company remained profitable as it recorded a gross profit of C$95M and a net income of C$0.37 per share (as you can see below), but as it is an infrastructure company, not the net income but the distributable cash flow is the most important metric.

{kind=link}

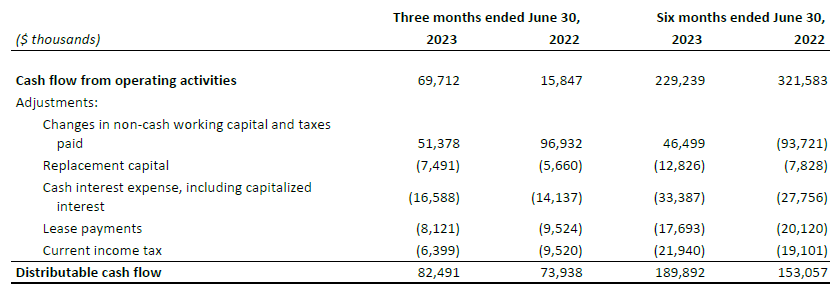

As you can see below, the total amount of distributable cash flow generated in the second quarter was C$82.5M, and this brought the total DCF in the first half of the year to almost C$190M. As there were 141.2M shares outstanding, the Q2 and H1 DCF per share were C$0.58 and C$1.34, respectively.

{kind=link}

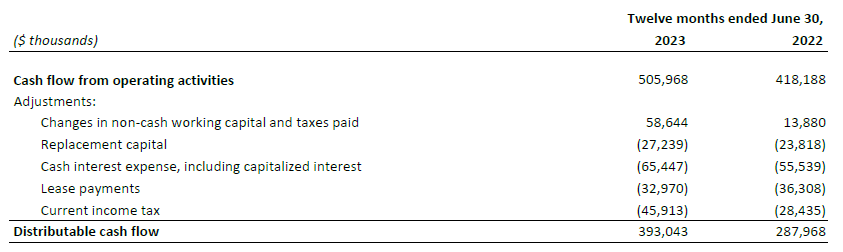

Additionally, the LTM DCF was C$393M or C$2.78 per share.

{kind=link}

This means the current distribution of C$0.39 per share is still very well covered and the payout ratio is just 55% on a LTM basis, which is lower than the company's target of 70-80%.

The acquisition of South Texas Gateway Terminal: Useful diversification, but at a hefty price tag

First of all, let me be clear: The diversification to reduce the exposure to Canadian assets is a good move, there's no doubt about that. But when I combed through the transaction details, I thought the acquisition was pretty expensive and will likely not be as accretive as the market initially thought.

In June, the company announced it entered into an agreement to acquire full ownership of the South Texas Gateway Terminal (hereafter "STLLC" for simplicity's sake and to use the abbreviation used by Gibson) for a total cash payment of US$1.1B in cash. According to the official press release, this transaction implied a multiple of less than 9 times the forward adjusted EBITDA and will be immediately accretive with DCF per share accretion in the mid-teens.

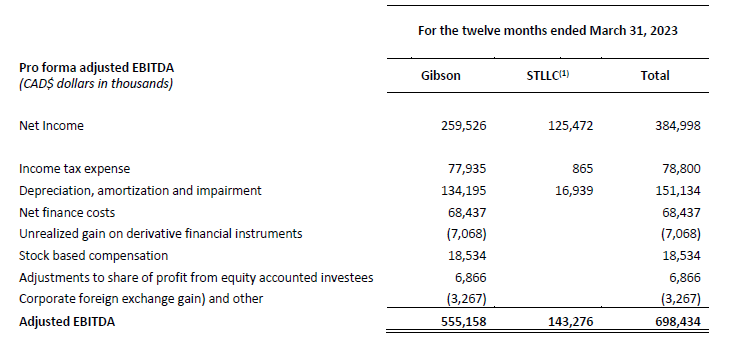

That's an interesting statement as the footnotes to the announcement clearly showed STLLC generated only C$143M in adjusted EBITDA. Assuming an adjusted EBITDA of US$122M would imply a 10% adjusted EBITDA increase in 2024.

{kind=link}

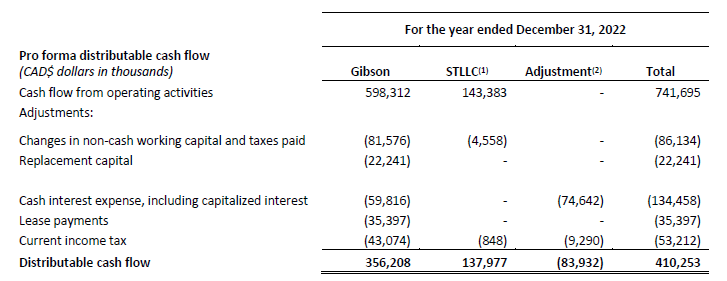

Doable, but looking at the pro forma distributable cash flow calculation, it may not be as easy as Gibson thinks it is. For the year that ended in 2022, STLLC generated C$138M in distributable cash flow on a normal operating level. This means Gibson is paying approximately 11 times the distributable cash flow while it was trading at less than 8 times DCF for its own operations.

{kind=link}

The entire acquisition cost was payable in cash, and this worked out to be close to C$1.5B. The company closed a C$403M bought deal financing issuing new shares while the remainder of the acquisition cost was funded with debt . Gibson Energy issued four new notes, and this is where it gets interesting. I summarized the details of the notes in the table below and included the total expected interest expenses for the new debt. The 2083 notes are fixed-to-floating, but as the coupon is fixed for the first five years, it only makes sense to use that fixed coupon to calculate the impact on the distributable cash flow.

Author's Table

Applying this total cost of debt on the C$138M in distributable cash flow on the operating level results in C$68M in actual distributable cash flow after taking the cost of debt into account, and about C$60M after taking income taxes into account (I used a lower amount than the current income tax adjustment shown in a previous image).

While that indeed provides a 17% increase in consolidated distributable cash flow, let's not forget the impact of the capital raise has not been included in this. The company issued 20 million subscription receipts, which were converted into common shares upon the completion of the acquisition. This means the total share count increased by about 14%. And that implies the DCF per share will only increase by 2-3%.

Of course that's based on the pro forma results in 2022, and if the company is right about paying 9 times the 2024 EBITDA, we should see a C$25M cash flow increase and this will likely add C$17.5M or C$0.11-0.12 per share in the DCF per share. But in order to reach the guidance of a "mid-teens DCF per share contribution" STLLC would have to contribute C$110M in distributable cash flow and I just can't see that happen. Even if the EBITDA jumps to C$180M that would be tough to realize due to the increased interest expenses.

Does that mean this is a bad transaction? It's an expensive one, but I understand the rationale behind it. Gibson was undoubtedly feeling pressure for being a Canada-focused company, and the acquisition of one of the most important oil terminals in the US is a massive step forward.

{kind=link}

Although I didn't like the price tag, the share price has now slipped to a level 10% below the capital raise price but has recovered somewhat since. At the current share price of approximately C$19.5, the consolidated entity remains very cheap.

Investment thesis

Gibson Energy generated C$393M in distributable cash flow on an LTM basis, and the addition of the new Texas asset will add approximately C$60M in pro forma distributable cash flow in the first few years. Considering the consolidated DCF should now be around C$450M per year, and considering there are just under 162M shares outstanding, the DCF per share will be approximately C$2.77/share which means Gibson is trading at a multiple of just 7 times its DCF. And of course, once the first "expensive" bonds will be repaid in 2026, the DCF will jump by about C$15M or C$0.09 per share and that will further fuel the results per share.

I'm looking forward to seeing if Gibson can indeed increase the DCF per share by a "mid-teens percentage" but I doubt that will happen in 2024 unless the acquired terminal generates C$110M in DCF.

If the company keeps its dividend unchanged, Gibson will be able to retain approximately C$180-190M per year in net distributable cash flow and that will obviously be a big help to reduce the net debt, reduce the debt level, and to avoid seeing the interest expenses run up higher. Meanwhile, at C$19.50/share, shareholders are getting rewarded with an 8% dividend yield thanks to the quarterly dividend of C$0.39 .

For further details see:

Gibson Energy Offers An 8% Dividend Yield Even After An Expensive Acquisition