GBNXF - Gibson Energy: Trading At Just 9x Distributable Cash Flow Offering A 7% Yield

2023-04-22 11:45:00 ET

Summary

- Gibson Energy is active in the infrastructure (oil terminals and pipelines) and the petroleum marketing sector.

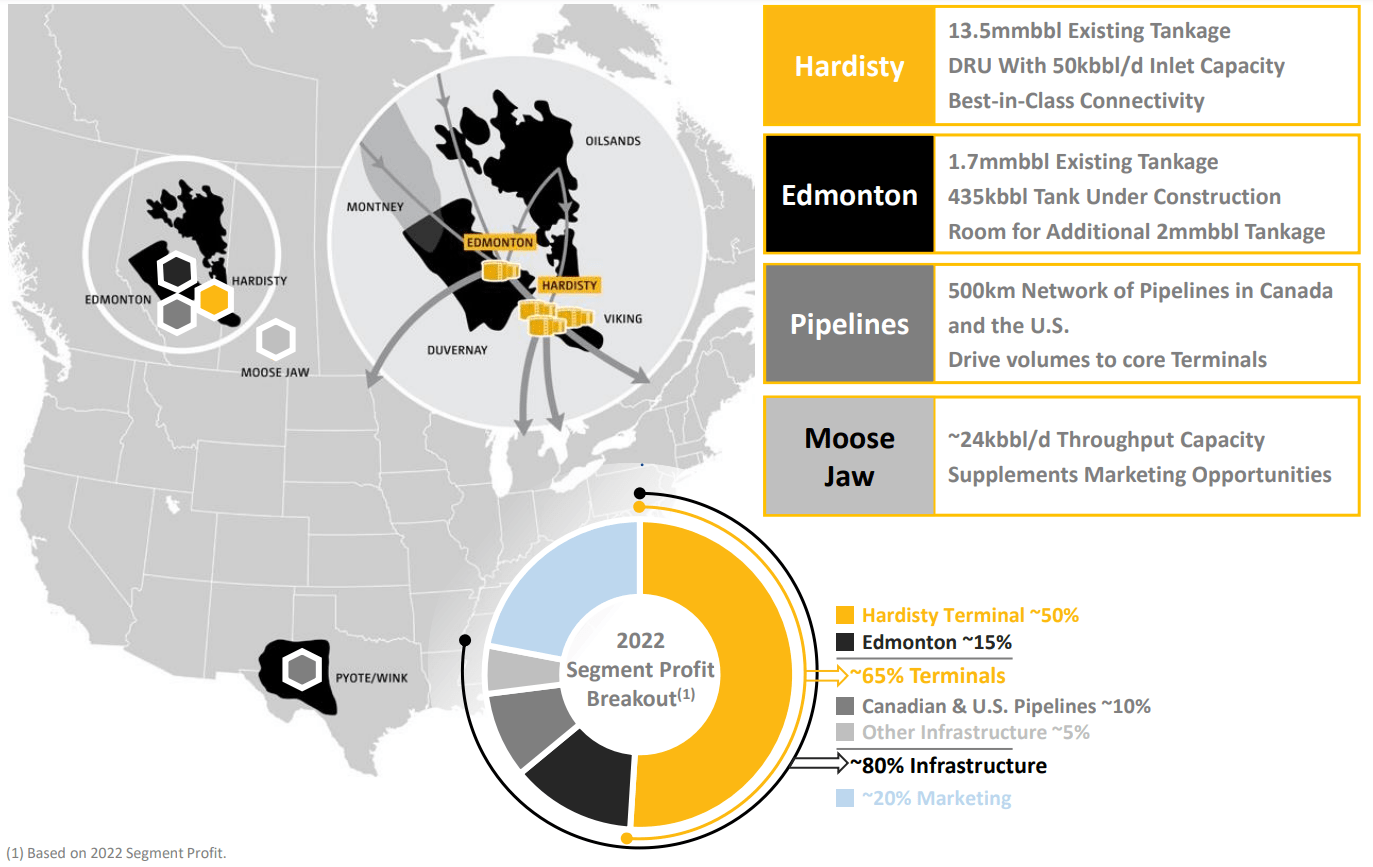

- The infrastructure segment generates just 5% of the revenue, but about 80% of the EBITDA.

- The company generated almost C$2.5/share in distributable cash flow in 2022 and I expect 2023 to be equally strong.

- The dividend was recently hiked but remains below the standard 70-80% payout ratio in Gibson's dividend policy.

- A strong result in 2023 and positive outlook for 2024 may result in another dividend hike.

Introduction

Gibson Energy ( GEI:CA ) (GBNXF) is a Canadian company with a 70-year history when the company started out in the petroleum marketing business and subsequently entered the pipeline business. This was soon followed by the construction of oil terminals, and today, the company should for sure be seen as an infrastructure company: Although the marketing of petroleum products generates almost C$11B in revenue, the profit margins are razor thin at just 1.1%. Meanwhile, the gross profit generated in the Infrastructure Segment is approximately 435M CAD or 83% of the revenue.

{kind=link}

That's also why Gibson Energy publishes a distributable cash flow calculation which makes its performance more comparable with other infrastructure companies.

The distributable cash flow result in 2022 was strong

Although Gibson generates the vast majority of its revenue in the petroleum marketing segment, the main value driver is the infrastructure division so you shouldn't be put off by seeing a very high revenue but relatively low operating income as that's incomparable to other infrastructure companies.

{kind=link}

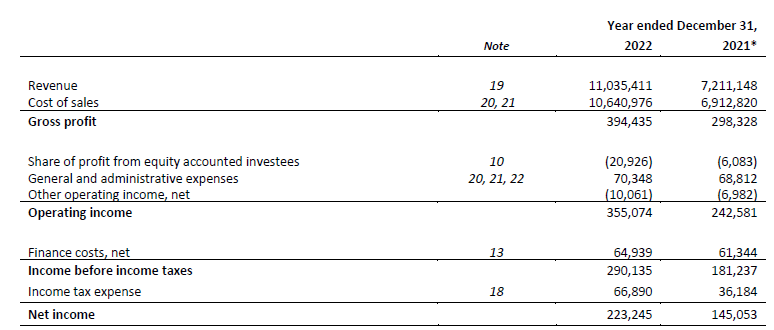

This also means the reported net income of C$223M or C$1.53 per share is not entirely comparable, and that's why the company reports a detailed distributable cash flow calculation. But first, let's have a look at the cash flow statement.

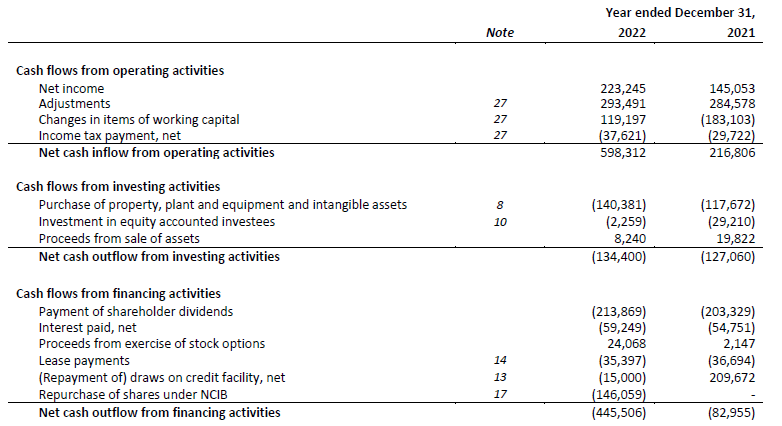

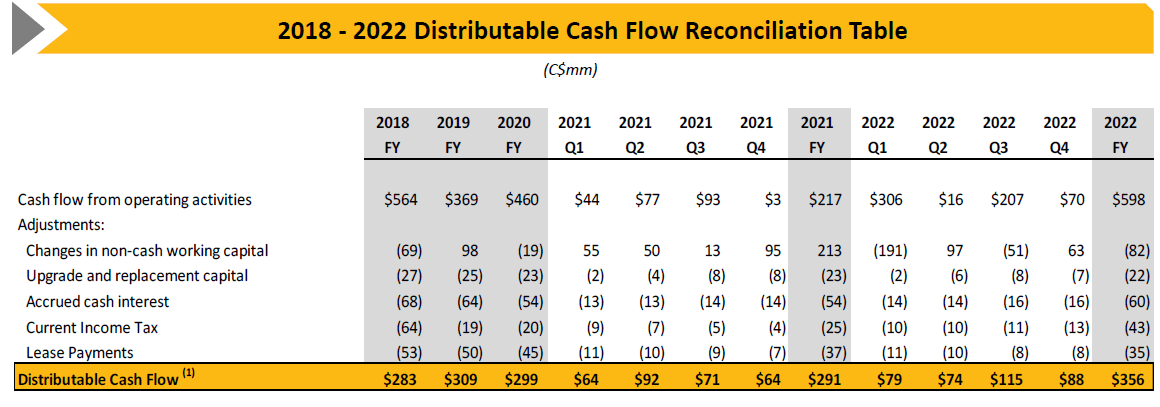

Gibson reported a total operating cash flow of C$598M but this includes a C$119M contribution from working capital changes and also includes just C$38M in cash taxes although about C$67M was due based on the FY 2022 income statement. After also deducting the C$59M in interest payments and the C$35.5M in lease payments, the adjusted operating cash flow was C$$356M.

{kind=link}

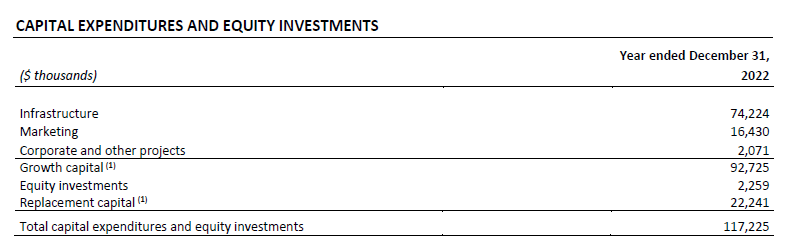

As you can see above, the total capex exceeded C$140M but the majority of this capex was mainly related to growth capex . And as shown below, the total replacement capital came in just over C$22M and in excess of C$90M was invested in growth. The total capex and equity investments of C$117M is lower than the C$140.4M as shown in the cash flow statement and that's caused by an increase in the intangible investments.

{kind=link}

That's why it's useful to see Gibson also publishes a distributable cash flow result. This includes all relevant operating expenses as well as the sustaining capex, but it excludes the growth capex as the dollars spent on growth are a capital allocation decision, funded by free cash flow.

{kind=link}

As you can see in the table above, Gibson's distributable cash flow came in at C$356M in 2022, an increase from the relatively stable result of around C$300M per year in the preceding years. As the net share count at the end of 2022 came in just under 143M shares (thanks to buying back almost 6M shares), the DCF/share was approximately C$2.49.

As the company was paying a dividend of just C$0.37 per share per quarter, the payout ratio based on the DCF was just 60% and that's below the anticipated payout ratio of 70%-80%. Gibson has hiked the dividend again this year and currently pays C$0.39 per share as a quarterly dividend. The current annualized dividend of C$1.56 per share represents a dividend yield of almost 7% based on the current share price.

The company plans to invest in growth this year

The relatively low payout ratio means Gibson has plenty of cash on hand to continue its growth investments. In 2023, the company plans to spend C$100-125M on growth which could potentially increase to C$150-200M if some additional projects that are in the pipeline but haven't been greenlighted yet will go ahead this year.

This means that Gibson will very likely be able to fund 100% of its capex commitments with the free cash flow even after taking the dividend into consideration. That being said, Gibson has announced a new C$150M share buyback program (of which it initially plans to spend C$100M this year) so we will likely see the company take on some debt to fund its growth investments. This should enable the company to repurchase about 3% of its share count and end the year with approximately 140M shares outstanding.

Using the current share count and applying the increased dividend will cost the company about C$223M. Assuming a similar financial performance in 2022 compared to 2023 (I'm not really expecting an improvement compared to last year and just keeping the results steady would already be an achievement in the current volatile climate), this means Gibson will generate about C$130M in free cash flow to help fund a share buyback and the growth capex.

The debt ratio as of the end of last year was just 2.7 (for a total net debt of C$1.4B), and even if we would completely ignore the EBITDA contribution from the petroleum marketing segment, the debt ratio would be just 3.2 times the infrastructure-only EBITDA. That's low for an infrastructure-focused company as for instance Pembina Pipeline ( PBA ) and Enbridge ( ENB ) have debt ratios of respectively 3.6 and 4.7 .

Investment thesis

Gibson Energy is currently trading at just 9 times the distributable cash flow result of 2022, a result I expect the company to duplicate in 2023 despite volatile markets. And this makes Gibson pretty interesting. Not only do you get a 7% dividend yield, the remainder of the free cash flow is used to fund a combination of growth capex and share buybacks and I do believe the latter is a good move given the single digit multiple Gibson is trading at.

I currently have no position in Gibson Energy but after seeing the strong results for 2023, the company is on my radar again.

For further details see:

Gibson Energy: Trading At Just 9x Distributable Cash Flow, Offering A 7% Yield