GTLB - GitLab: Continuous Improvement Goes A Long Way But Still Overvalued

Summary

- GitLab has an open core business model that helps its grass-root growth, innovation, and cost reduction.

- GTLB stock needs a near-term turnaround in its negative cash flow and a strong growth spur within the next five years to justify its current high valuation.

- With more future development and competition underway, it will be hard for it to cut expenses, although its low debt burden leaves it room to leverage up if needed.

Investment Thesis

With a solid open-source, grass-root culture, GitLab ( GTLB ) is the quintessential tech company that is poised to capture continuous innovation and development in enterprise software development. We assess its expenses and cash flow with an assessment of the future development it is heading into. However, even with a very strong growth projection, we still find the current price is too high.

Company Overview

GitLab is a DevOps platform with a single codebase and interface with a unified data model. The company is open-source, allowing everyone to contribute to the software-building process, which in the end, combines development, operations, IT, security, and business teams into a single platform. Its service plan has three-tier offerings: free, self-managed, and software-as-a-service or SaaS.

Strength

We have talked a lot about the supply chains in recent days. What GitLab does is basically help companies secure an end-to-end software supply chain that can be hosted either in-house within the platform or in a hybrid private/public or multi-cloud environment. It is fitted with the calling, "You build it, you run it." For the investors who are interested, here 's a pretty cool video to show how it evolved in the 11 years' time of development, summarized in 10 minutes (see a snapshot below).

{kind=link}

At its core, GitLab relies on the open-source community for continued innovation and development. Not surprisingly, it has an active and virtuous relationship with the open-source community. The company calls it the Open Core business model. It offers a free tier with a large number of features to encourage usage, solicit contributions and serve as targeted lead generation for paid customers. This could help lower the operating cost over time, but most importantly, the contributions are the key to its ongoing technological development as users are essentially the main developers. Then logically, the developers, which are the group of users that use it the most, are where its typical point-of-sale begins. It then expands to the business teams and up to the senior executive buyers. It called it a land-and-expand sales strategy. This is again rooted in the open-source community and users. To exemplify this relationship, even its corporate handbook is open to contribution by everyone, both inside and outside of the company.

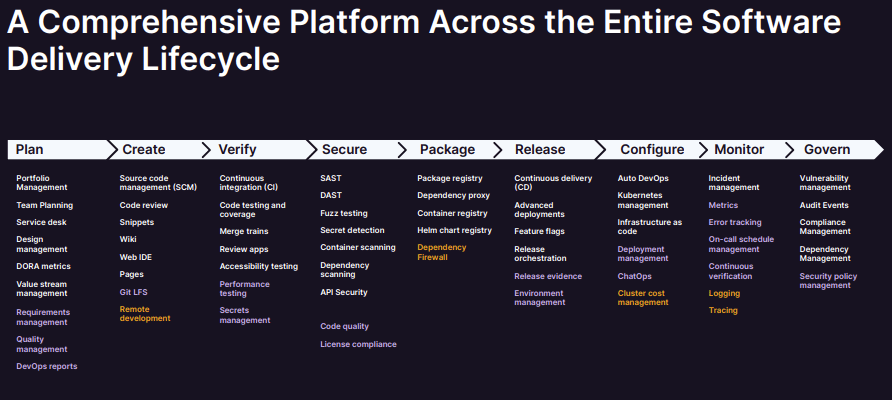

From a competitive perspective, GitLab's strength lies in integrating all the functions into a single comprehensive platform. GitLab actually pioneered this kind of DevOps platform. The company's platform is able to address every stage of the life cycle of the product: Manage->Plan->Create->Verify->Package->Secure->Release->Configure->Monitor->Protect. This helps to maintain full feature parity and a single application experience for developers, managers, and users. And in turn, boost productivity, reduce vulnerability, and enhance growth with faster delivery time.

gtlb (Company Q3 Presentation)

{kind=link}

GitLab's sales channels include its hyperscaler partners such as Google Cloud ( GOOG ) and Amazon Web Services (AMZN), who listed GitLab's platform on its marketplaces, and large global systems integrators, regional digital transformation specialists and volume resellers, who have access to the large enterprise customers.

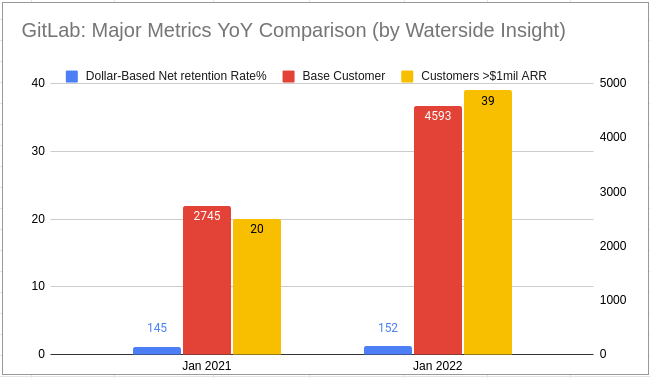

From its core technology to its sales strategy, and channels, GitLab is fairly open and dynamically embedded in the tech community, with strong integration of all its functions on one platform. So far, this has worked well for the company. On a YoY basis, its key metrics have continued improving.

gtlb (Charted by Waterside Insight with data from the company)

{kind=link}

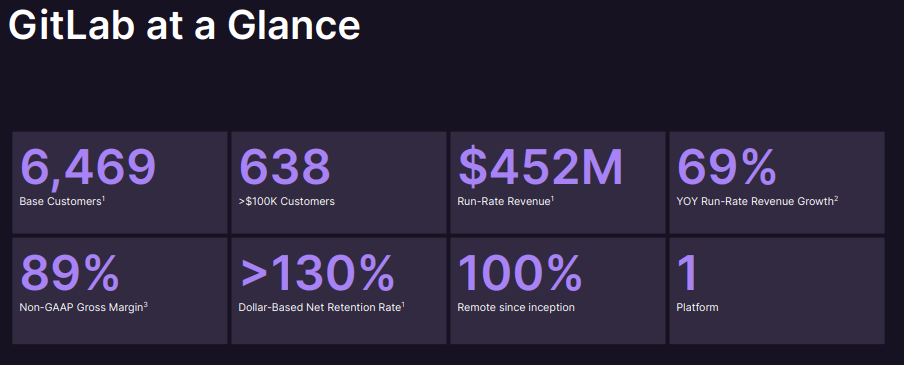

By the end of Q3 last year, its business metrics were the strongest since its IPO. GitLab defines Base Customers as customers with more than $5000 of Annual Recurring Revenue, or ARR, in a given period. At a glance, the number of this cohort of customers has jumped to doubling compared with the number in Jan 2021.

gtlb (Company Q3 Presentation)

{kind=link}

GitLab's revenue has grown to almost double what it was at the IPO, although its net income has been range-bound in the negative territory.

gtlb (Charted by Waterside Insight with data from the company)

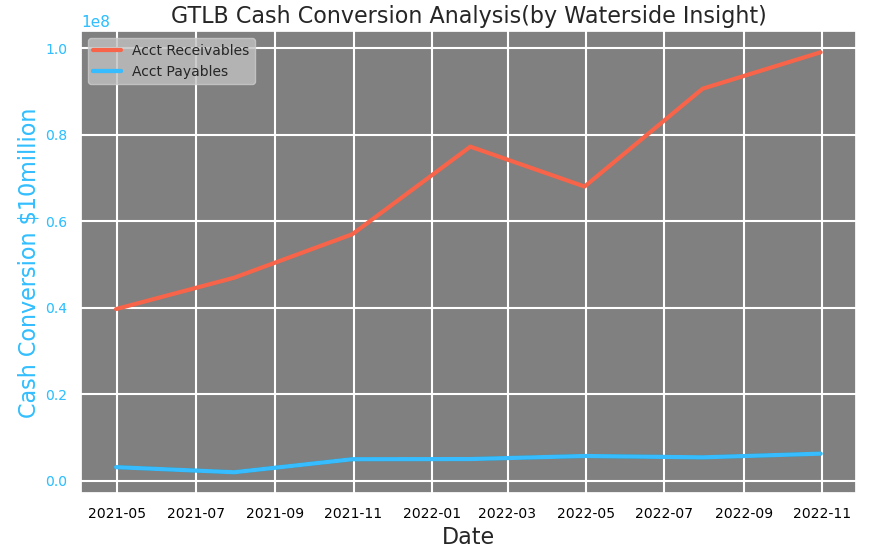

The company has no inventory, so we look at just account receivables and payables for its cash conversion cycles. Its account receivables have been taking off since early 2021 to nearly doubling, while its account payables are staying almost flat. This widening gap ensures its continuous growth in revenue.

gtlb (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

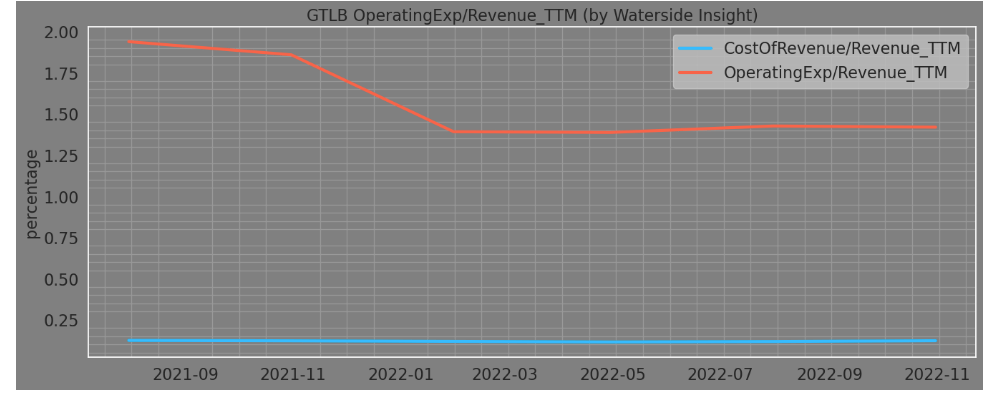

GitLab's cost of revenue as a percentage of revenue had fallen from the end of 2021 to the beginning of 2022, while its operating expenses as a percentage of revenue have been very flat. Partly, the cost saving came from being fully remote. The company has been 100% remote since Jan 2022, which includes its 1630 employees across 68 countries. So far, GitLab hasn't had any significant layoffs. If keeping its personnel fully remote can help it avoid significant layoffs, which is the latest trend in the tech sector, then it could set to benefit from the continuity later on.

gtlb (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

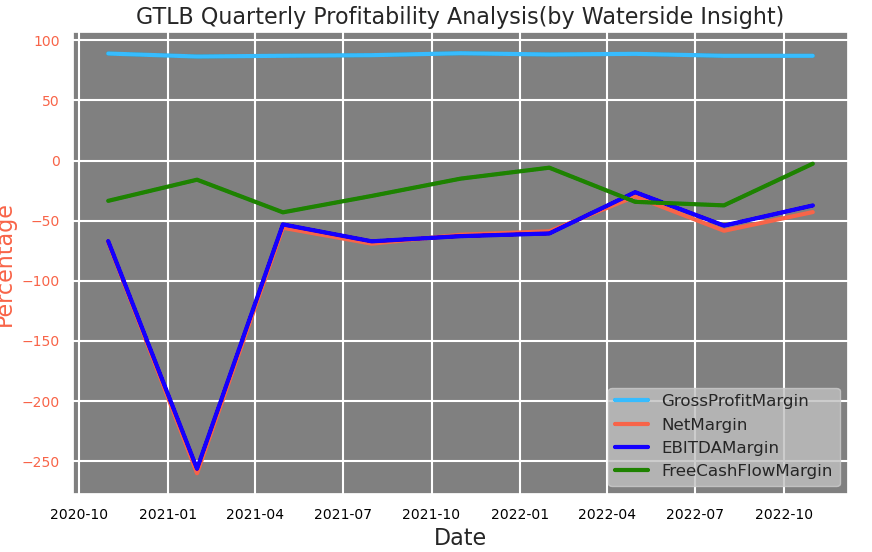

The company's gross profit margin stays at around 88%, while most of its other margins are improving in the last two quarters.

gtlb (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

Last but not least, GitLab's debt burden is still very low. As of Q3 last year, it had total liabilities of $305 million, which is just about 3% of its total equity of $7.8 billion. It still has room to leverage up if it needs to make a significant change or improvements down the road.

Weakness/Risks

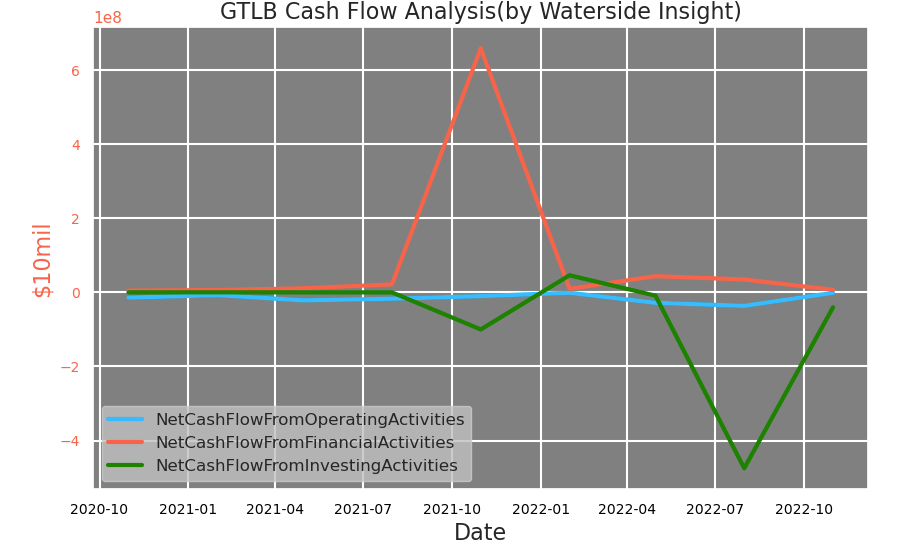

If we break down GitLab's cash flow, we can see its latest cash flow improvement primarily due to cash from investing activities, while its cash flow from operation wasn't improved much. This makes the cash flow improvement vulnerable to a setback into the negative again in the next few quarters.

gtlb (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

And the company's operating expenses are still too high relative to the earnings from the operation. Although it is not deteriorating, it would be beneficial if this ratio could be lowed as this rate of spending is not sustainable in the long term, and could lead to more borrowing needs.

gtlb (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

Future Development

As GitLab is open-source, it is well supported by grass-root movements. However, that doesn't mean it can be exempt from competition. DevOps has become the de facto gold standard most engineering organizations have tried to build towards, but it requires the developers to be able to grasp the entire end-to-end enterprise tool chain. This actually increased the cognitive load on the engineers and created inefficiencies like shadow operations . To cope with this problem, enterprise users developed something called "Internal Developer Platform" ((IDP)) to help lessen this cognitive load on the developers. Internal Developer Platform is basically enabling the delivery teams to self-service, deploy and operate systems with reduced lead time and stack complexity, while emphasizing API-driven self-service and supporting tools, with delivery teams still responsible for supporting what they deploy onto the platform. This has become part of the latest trend in Platform Engineering. GitLab has its own IDP, but will need to continue investing in this direction. Otherwise, it risks spreading out too thin while creating higher hurdles for developers to utilize the single whole platform efficiently-another reason we see that its expenses will be hard to come down.

Financial Overview

gtlb (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

Valuation

GitLab's total cumulative return since its IPO has been a steep loss. After this price decline, is it time to buy?

gtlb (Company 2022 10K)

We take into account all the analysis above and use our proprietary models to assess the fair value of GitLab with a ten-year projection forward. In our bullish case, we priced in several explosive growth spurs in its next ten years' path with minimal negative growth, and it eventually reached over $30 billion in its free cash flow annually; it was valued at $34.62. In our bearish case, its growth leap was less than stellar and with more misses; it was priced at $14.01. In our base case, we added a few more misses in its growth to account for the kind of spending and perhaps more competition down the line, and it still eventually reached $26 billion in its free cash flow; it was valued at $25.31. The key in these valuations hinges on GitLab delivering this growth spur within the next five years. If it takes longer than that, then the valuations will drop by a large portion. The current market price is above our top valuation.

GitLab Fair Valuation (Calculated and Charted by Waterside Insight with data from the company)

Conclusion

We are enthusiastic about GitLab's continuous progress and its open-core, open-source growth model. We expect wider adoption and stronger growth will come in time. However, we also see that there are more platform-wide expenses needed in order for it to keep scaling up. The current valuation is too high for even our most optimistic scenario, and we are still looking for better cash flow in the near term to drum up our perspectives. Otherwise, we lean more towards our base case fair price. At the current price, we will recommend a sell.

For further details see:

GitLab: Continuous Improvement Goes A Long Way But Still Overvalued