GTLB - GitLab: Hold On To This Long-Term Winner Despite Current Macro Headwinds

Summary

- GitLab's recent financial results have continued to impress investors, with revenue growing 69% during the most recent quarter.

- Strong dollar-based net retention of 130%+ combined with ongoing customer additions supports impressive revenue growth over the coming years.

- Profitability will continue to improve as the company scales, with gross margins consistently around 90%.

- Valuation is the big concern, with the stock currently trading around 12x forward revenue.

GitLab ( GTLB ) is a DevSecOps platform that helps companies maximize the value of their software development. GTLB's solutions offer faster cycle times and greater visibility throughout the DevSecOps lifecycle.

The company continues to post very strong quarterly results, with revenue growth of nearly 70% during the past quarter and consensus expecting 40% growth for their next fiscal year. While the macro may weigh on sentiment, GTLB's motions around existing customer upsell and new customer additions will likely drive sustainable 20%+ revenue growth over the coming years.

The stock is down almost 40% over the past year, but this was largely driven by the broader reset across software valuations. No longer are the days of 20x revenue multiples for software companies growing 40%+ with no profitability. The fears of a potential recession combined with rising interest rates have caused investors to be more risk averse, and GTLB's valuation has pulled back considerably.

However, the company has demonstrated their ability to scale margins, and while operating margins were still -19% during the last quarter, gross margins have consistently been around 90%. FCF burn has continued to come down over the years and GTLB has a strong balance sheet, with over $900 million of net cash available to fund near-term liquidity and investments. Over time, I expect both margins and FCF to materially improve, and given the general focus on eliminating expenses, I believe GTLB's profitability could be achieved sooner rather than later.

Valuation is a big concern here, with the stock currently trading around 12x forward revenue. However, there are not many companies in the market currently growing revenue over 50%, gross margins of 90%, and a clear path towards operating margin improvement. Given this strong combination, along with a solid balance sheet, I believe long-term investors should look to weather any near-term volatility and hold onto the stock long-term.

Financial Review

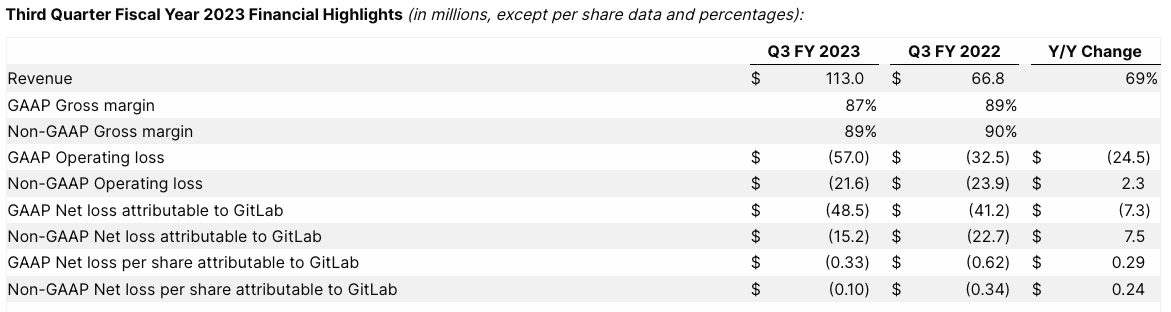

During the company's most recent quarter, they reported revenue of $113 million, which grew 69% yoy and easily surpassed consensus expectations for $106 million. In addition, GTLB continues to post near 90% non-GAAP gross margins, which remain among the highest in the software industry. Yes, they are still generating non-GAAP operating losses, but the gross margin strength should give investors confidence in their ability to achieve scale efficiencies over the long-term.

{kind=link}

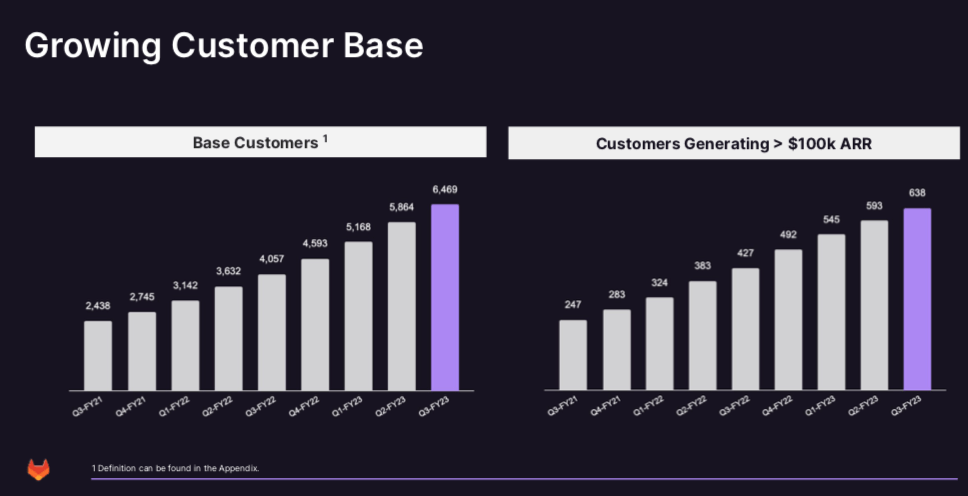

On top of GTLB continually posting 130%+ dollar-based net retention, they also continue to grow their customer count at an impressive rate. During the quarter, customers with >$5k of annual recurring revenue grew 59% yoy to 6,469. Growth was also very strong for enterprise customers, as those with >$100k of annual recurring revenue grew 49% yoy to 638, and now represents around 10% of total customers.

{kind=link}

One of the biggest advantages of moving up market is the stickiness of enterprise customers. In the land of software, SMB customers churn at a higher rate, and while there are more SMB companies in the market, one would have to win a lot more business in order to replenish the higher churn.

GTLB has done a great job on the customer expansion front, as demonstrated by the customer charts above. Additionally, GTLB does an incredible job on the existing customers, as demonstrated by their 130%+ dollar-based net retention rate.

{kind=link}

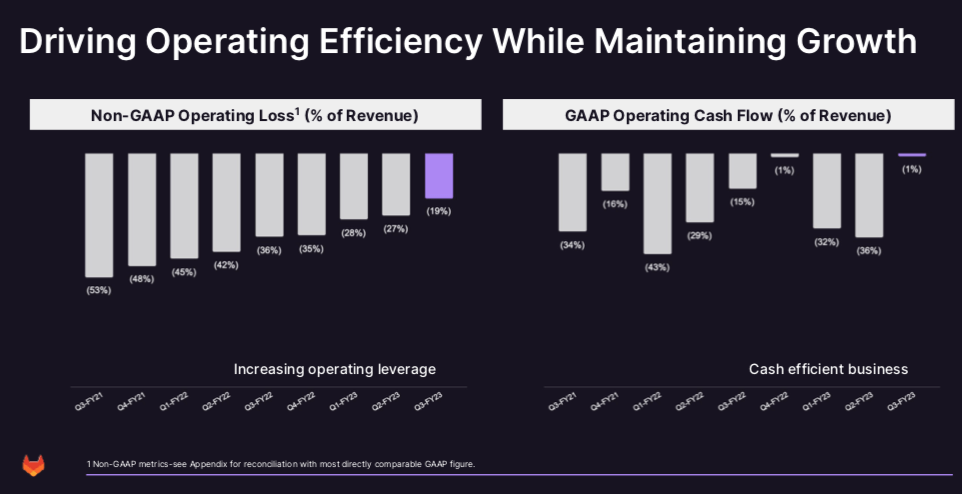

One of the biggest drawbacks is the company's lack of operating profitability. Yes, gross margin remains very strong at 90%, but operating margin loss was 19% this past quarter. While this is a noticeable improvement from the 36% loss in the year-ago period, the company still has a long way to go before achieving breakeven status.

I do believe that as GTLB continues to scale, they will be able to demonstrate operating leverage over the long-term.

In addition, GTLB has generated a FCF loss of $70 million through the first three quarters of the year. This should continue to improve over time, and even if we were to assume a $100 million run-rate FCF burn, the company still has over $900 million of cash/equivalents, giving them plenty of runway to improve profitability.

Valuation

One of the most challenging things in this market is knowing how to value software companies. Post-COVID, it seemed like every software company could justify a 10x revenue multiple. However, with interest rates rising and investors taking a more risk-off approach in fears of a potential recession, unprofitable software companies have significantly pulled back.

GTLB currently trades just under 12x forward revenue, and while this is still a premium valuation relative to the broader software sector, GTLB's valuation has pulled back from over 20x during a good portion of 2022.

While the company is not immune to the broader macro factors, their focus on the developer community can provide some sort of resilience. Developers are not usually the first line of employees to be let go during more challenging macro conditions. Over the past few months, many technology companies have announced workforce reductions, which have largely been focused around S&M operations.

Nevertheless, revenue growth will likely remain very strong over the coming years, with consensus currently modeling 40%+ growth for FY24 (per Yahoo Finance), ending January 2024. I believe given the company's strong dollar-based expansion rate and ability to attract new customers, revenue could remain above 20% for many years to come.

On the margin front, clearly investors are placing more emphasis on profitability, especially given the heightened fears around a potential recession. While GTLB may still be a year or two away from generating profitability on a full-year basis, I believe the company's strong operating margins and history of operating leverage should serve them well.

Despite the stock still trading at a 12x forward revenue multiple, I believe long-term investors should look to build a position in the name.

For further details see:

GitLab: Hold On To This Long-Term Winner Despite Current Macro Headwinds