GTLB - GitLab: Positive Price Increase Offset By Growth Headwinds Pushing Down Multiples

2023-04-11 14:40:33 ET

Summary

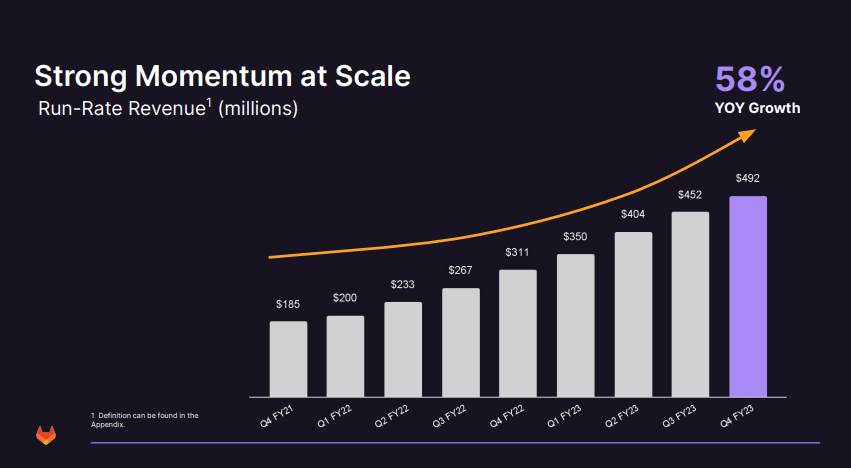

- GitLab guided revenue growth of 25% YoY in FY2024, materially decelerating from 68% YoY in FY2023.

- The stock still trading at a high growth multiple (8.7x EV/FY24E revenue) after a weak revenue guidance is problematic.

- Despite macro headwinds, ongoing deflation momentum creates a floor for rate-sensitive stocks like GTLB.

- The full impact of premium price increase may push out to FY2025.

- I assign a neutral rating, as a 30% price drop after Q4 FY2023 earnings has partially priced in near-term headwinds, creating a fundamental positive bias in the mid/long term.

Editor's note: Seeking Alpha is proud to welcome Hongyi Zhang as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Rationale

GitLab (GTLB) is perceived as a hypergrowth (68% YoY revenue growth in FY2023), DevOps subscription-centered software company that has built a fully integrated platform from end to end. In surveys conducted by Global Market Insights, the COVID-19 pandemic has been accelerating digital transformations. The DevOps market is seeing secular growth tailwinds to achieve over a 20% CAGR from 2022 to 2028 with a $30 billion total addressable market. This should help GitLab gain market share for years to come as the current market penetration is still very low. While I believe the long-term growth trajectory remains intact, given the premium valuation (trading at 8.7x EV/FY24E revenue), I remain neutral as the company is muddling through many macro headwinds in FY2024 (e.g., high inflation, weak manufacturing activities).

{kind=link}

Company Background

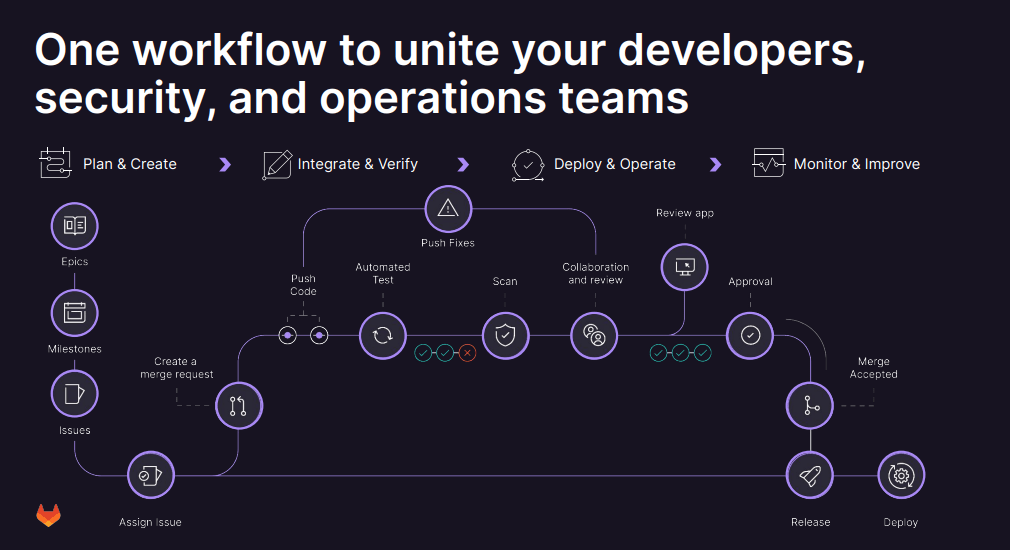

GitLab embarked on its DevOps software journey in October 2011, founded by Valery Sizov and Dmitriy Zaporozhets. In its early years, the company was focused on the platform specialized in continuous integration ((CI)) and later expanded into source code management ((SCM)) to support software developers across all industries. After more than a decade, the company has built a fully integrated ecosystem for customers to develop, deploy, monitor, and manage their software applications. The core services are mainly subscription-based and can be run either on-premise or as Software as a Service ((SAAS)). The company, which has been operating 100% remotely since 2011, offers competitive advantages in terms of cost efficiency and workplace flexibility to attract global talents.

{kind=link}

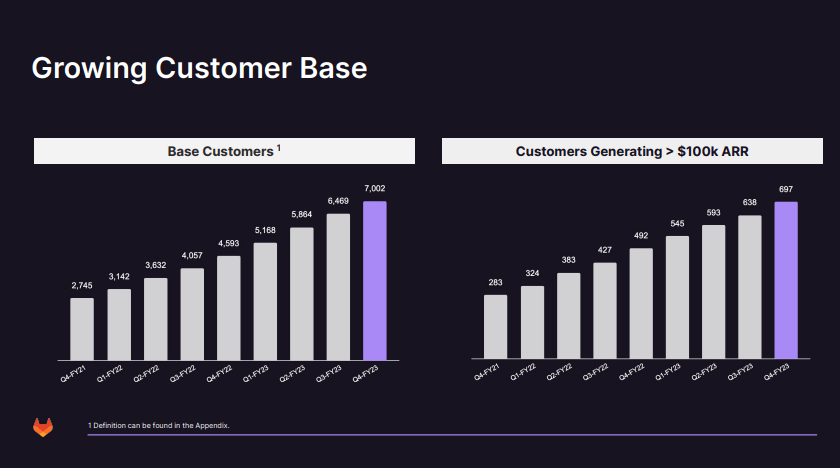

Focusing on a go-to market strategy, GitLab has successfully expanded its user base through direct and channel sales. Its customer base grew 52.4% YoY in FY2023 and 67.3% YoY in FY2022, respectively, which is significantly higher than that of peers. The company has consistently maintained a dollar based net retention rate ((NRR)) of more than 130% in each quarter. According to JP Morgan consensus, a NRR over 120% is considered good, while a reading over 130% is considered great, so Gitlab's NRR being over 130% in the past quarters is considered best in class.

{kind=link}

Q4 FY2023 Key Takeaways

The stock tanked more than 30% after Q4 FY2023 earnings , despite better-than-expected revenue and earnings. Investors were disappointed about the forward revenue guidance in FY2024, even though the management said the effect of premium price increase was embedded into the guidance, which implies a significant slowdown compared to the growth in FY2023. The company guided to 25% YoY FY2024 revenue growth, below consensus of ~40%. The growth also significantly deaccelerates from the 68% YoY growth achieved in FY2023.

{kind=link}

Regarding profitability, the company expects FY2024 non-GAAP EPS to be between -0.29 and -0.24, which is higher than the Bloomberg average forecast of -0.37. Despite improvement on the bottom line, investors were not impressed as the earnings remain in deeply negative territory due to the high interest rate backdrop. Management needs to provide a clear visibility of positive FCF inflection in order to offset the revenue weakness and rebuild the upside momentum.

During the earnings call , the management forecast that the macro headwinds will persist through FY2024, further delaying the FCF breakeven point. The team saw a higher contraction of seats and longer deal cycle times in Q4, which was affected by macro headwinds. The CFO, Brian Robins, admitted that the guidance has included the impact of the price increase but did not explicitly mention the magnitude and the timing of the impact. He said, "it doesn't take effect for existing customers until they come up for renewal." As a result, it is possible that the potential tailwind of the price increase may extend FY2024 and accelerate revenue growth in FY2025.

The Street's Anchoring Bias

According to BBG average ratings (13 buy, 2 hold, 0 sell), the street still holds a bullish view on GTLB. However, as we previously discussed, the revenue growth is expected to slow down in FY2024, implying a change in the company's fundamental outlook. It is well-known that ratings from most sell-side analysts may come with a lag. I admit that some quantitative strategies rely on the street's ratings for trading decisions. As a fundamental investor, it is prudent to adjust investment decision on a timely basis. If the growth outlook weakens and macro headwinds persist, investors should remain cautious in the near term, despite the street's bullish view on the company.

Valuation

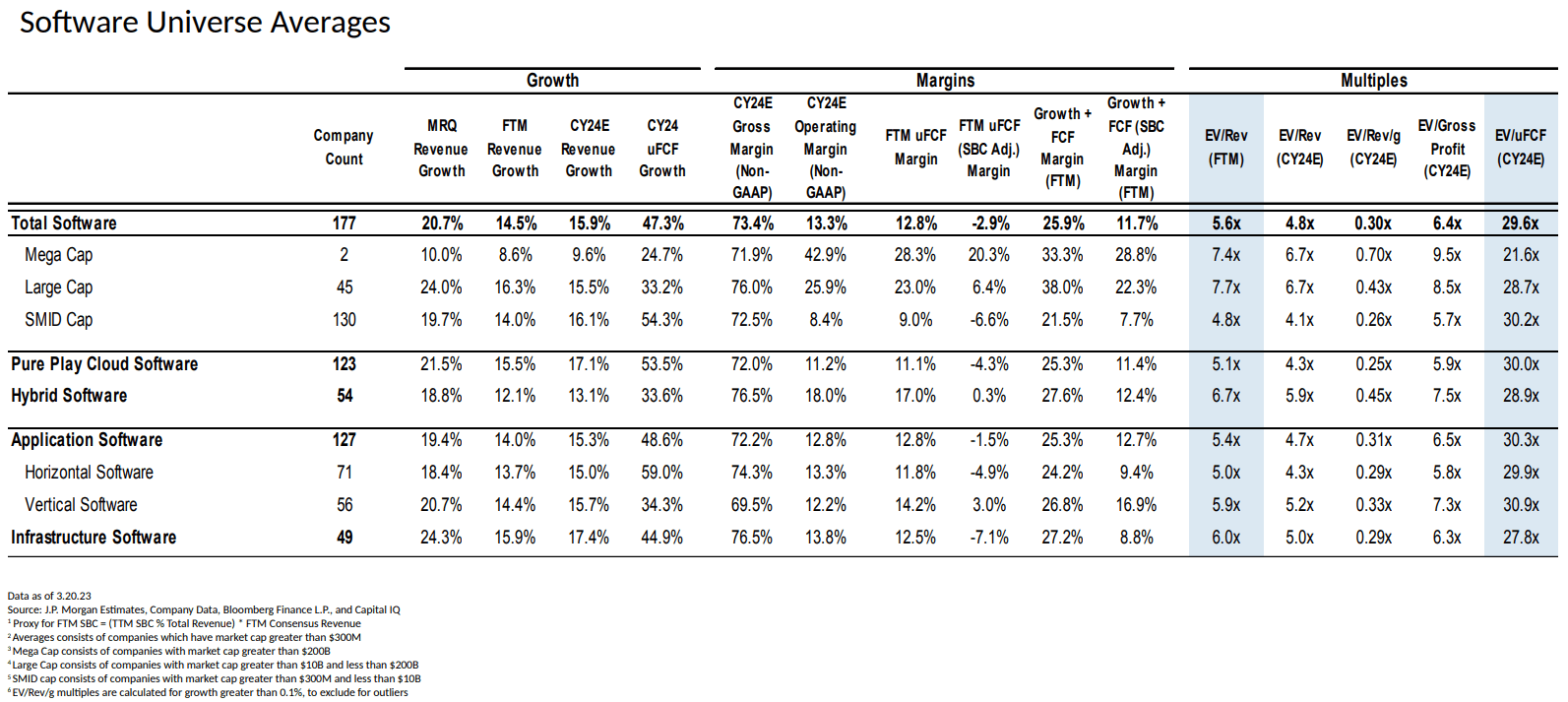

J.P. Morgan Estimates, Company Data, Bloomberg Finance L.P., and Capital IQ

{kind=link}

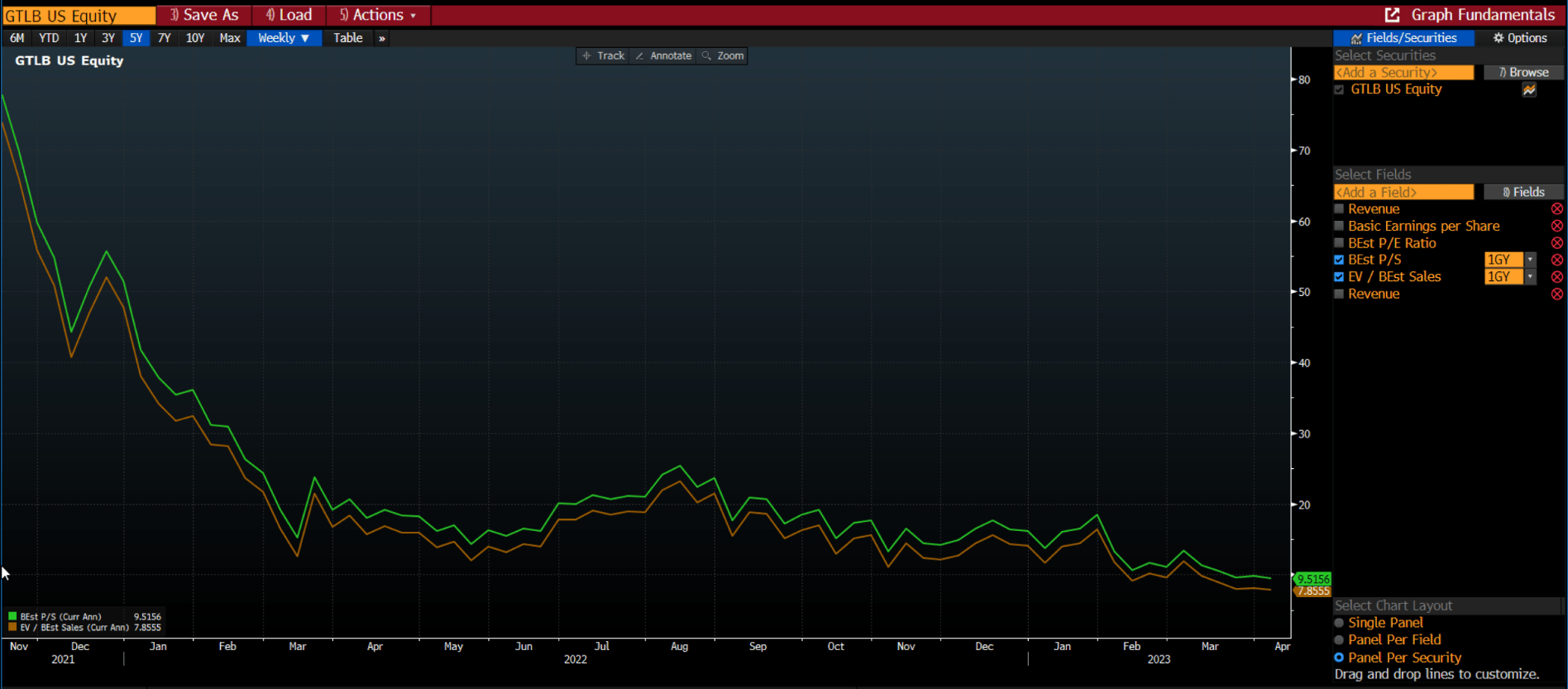

I have a neutral rating on GTLB due to the slowdown in revenue growth, which is putting downward pressure on multiples. However, the price drop of more than 30% after the earnings has already reset market expectations and set a low bar for the next several quarters. The stock is currently trading at 8.7x EV/FY24E revenue (price 3/24/23), which is significantly higher than the average for the software universe at 5.6x. (Please note that the current multiples in the chart below may vary due to recent market volatility).

{kind=link}

GTLB was a hypergrowth name, deserving high multiples in a low interest rate environment as long as its growth momentum remains intact. As US inflation is still running hot at 6% YoY, the Fed is aiming to bring it back down to the 2% target by hiking interest rate to 5% or even higher. In the face of raising interest rates, non-profitable high growth stocks like GTLB are expected to face significant challenges. Moreover, the company's lowering of FY2024 revenue growth to 25% is expected to further compress valuation multiples.

Despite better-than-expected earnings guidance, investors are placing more emphasis on the top-line growth, as it may take years for FCF and earnings to reach breakeven. As a result, DCF valuation is currently not an appropriate method as the management did not provide any meaningful catalysts to breakeven FCF and earnings in a near term. In this article, my particular focus is on the revenue multiple valuation.

Revenue Model (Growth Slowdown)

{kind=link}

Let's take a step back for a moment. The EV was calculated based on the closing price of March 24, 2023. In the growth slowdown scenario, I assumed FY2024 revenue growth would be in-line with the company's guidance, with a subsequent deceleration of 2% in growth rate. There is unlikely to be any significant growth rebound beyond FY2024, as investors have adopted a wait-and-see approach following disappointing Q4 earnings results. Currently, the company is trading at 5.9x EV/FY26E revenue, which is higher than the software average of 5.6x.

Revenue Model (Growth Acceleration)

{kind=link}

On the other hand, I assumed the previously guided revenue growth of 40% is achievable in FY2025, considering that existing customers may require more than 12 months to renew their contracts. In the FY2023 10-K (on page 27), the company addressed, "If our customers do not renew their subscriptions on similar pricing terms, our revenues may decline, and our business could suffer." As a result, revenue growth is expected to pick up in FY2025, driven by the impact of premium price increase on existing customers. However, the multiple is still trading at 6.2x EV/FY25, indicating that it is still expensive.

Upside Risks

The management's tone may be overly conservative when considering macro headwinds in FY2024. In order to justify the current price level, we need a catalyst for multiple expansion, such as a growth rebound in FY2025 or a low discount rate. GTIB is a high-beta stock, and it could experience a strong rebound if inflation decreases and the Fed subsequently lowers interest rates. Headline inflation has been deaccelerating since the last year. The recent SVB blowout and banking crisis in early March is adding more downward pressure. The current fed fund futures are pricing in three 25bps rate cuts at the end of 2023, as the market anticipates a potential recession and deflationary pressures, leading to a reduction in interest rates. If the deflation momentum continues, GTLB could have a meaningful rally from its current level, presenting an attractive buying opportunity.

{kind=link}

Bottom Line

All in, I am currently on the sideline as the stock still appears expensive, despite a conservative FY2024 guidance. However, I admit that the company continues to benefit from secular growth tailwinds in the long run due to its fully integrated DevOps platform and robust customer base growth. Additionally, the current platform market still remains fragmented, which gives the company an edge in expanding its market share. It is worth noting that valuation multiples of early-staged hypergrowth stocks are very sensitive to top-line growth momentum rather than margin expansion. If investors perceive that the growth momentum of GTLB has slowed down, sentiment may remain negative in the near term.

For further details see:

GitLab: Positive Price Increase Offset By Growth Headwinds, Pushing Down Multiples