GTLB - GitLab Q3 Earnings: Stock Jumps Decoding Its Prospects

2023-12-05 03:30:19 ET

Summary

- GitLab is a tool that simplifies software development tasks and improves teamwork, making the delivery of software faster.

- The stock is reasonably priced and the company is now profitable, with promising growth prospects and a strong financial position.

- GitLab faces challenges in a competitive landscape and convincing enterprises to transition to its platform, but its valuation and profitability make it an intriguing investment opportunity.

Investment Thesis

GitLab ( GTLB ) is a tool that helps software development teams work together better by simplifying tasks like managing code and automating the process of turning code into working software. It's like an organized virtual workspace that makes teamwork smoother and speeds up the delivery of software.

The stock isn't expensive at approximately 11x forward sales (including the premarket pop). But my question of where GitLab's revenue growth rates will stabilize persists.

That being said, the business is now profitable going ahead. For investors, this rapidly growing business with the right narrative, with approximately $1 billion of cash and equivalents and no debt, holds a lot of promise.

Despite some pesky detractions, I am bullish on this stock.

Rapid Recap,

Back in September, I wrote in a bullish piece,

I have some minor doubts about GitLab's recent earnings report for fiscal Q2 2024. While there were positive aspects, such as the upward revision of revenue targets, it fell short of my initial expectations. The question of where GitLab's revenue growth rates will stabilize is concerning, given the recent declines.

However, despite these uncertainties, I'm inclined to be bullish on GitLab.

[...] The company's improved cash flows and determination to deliver profitable growth make me believe that GitLab's current valuation, at around 14x this year's sales, is reasonable.

Michael Wiggins De Oliveira on GTLB

Admittedly, the stock has not been a terrific performer since my bullish assessment, as it's only up the same as the S&P500 ( SPY ). However, as we look through on this latest set of results, there's now more to be bullish on this name.

GitLab's Near-Term Prospects

GitLab serves as a comprehensive toolkit designed for software development teams, enhancing their collaborative efforts. It facilitates activities such as code management, change tracking, and the automation of code transformation into functional software. In essence, it functions as a centralized platform that optimizes the entire software development workflow, fostering seamless teamwork and expediting software delivery.

Moving on, GitLab exhibits strong growth prospects as it continues to position itself as a comprehensive DevSecOps platform, integrating security, compliance, AI, and agile planning in a singular solution. During the earnings call , co-Founder and CEO Sid Sijbrandij underscored the company's emphasis on security and governance capabilities, alongside the integration of AI throughout the software development lifecycle, which distinguishes GitLab in the market.

The Enterprise Agile Planning offering further expands its market reach, providing a compelling alternative to established tools like Jira by Atlassian ( TEAM ). GitLab's financial performance, with over 8,100 customers and a dollar-based net retention rate of 128%, signals a positive trajectory.

Despite GitLab's promising prospects, the company faces notable challenges and headwinds. One challenge lies in the competitive landscape, particularly with the discontinuation of Atlassian's server offering, creating a potential market shift that GitLab aims to capitalize on. However, the displacement of Atlassian's Jira may not be a seamless process, as customers evaluate alternatives. GitLab acknowledges that while it has made strides in AI innovation, there is a cautious approach among customers who want to use AI responsibly. The CEO states, "Our customers are eager to use AI, but they want to do so responsibly." This cautious sentiment may affect the pace of adoption for GitLab's AI features.

Additionally, the elongation of deal cycles in the mid-market and SMB segments, as highlighted by CFO Brian Robins, suggests a cautious spending environment in an uncertain macroeconomic climate.

Moreover, GitLab faces the challenge of convincing enterprises to fully transition to its platform, competing not only with established tools like Jira but also contending with the entrenched practices of organizations using multiple DevOps tools. As Sijbrandij notes, "A leading global financial platform that tried to integrate GitHub with several other DevOps tools" faced complexities that GitLab seeks to simplify. Convincing enterprises to consolidate their workflows on a single platform requires overcoming existing tool integrations and addressing concerns about workflow disruption. This challenge is exemplified by GitLab's focus on enhancing its Enterprise Agile Planning offering to attract non-technical users, acknowledging that the biggest impact is expected in the years after the current fiscal year.

Given that background, let's now discuss its financials in more detail.

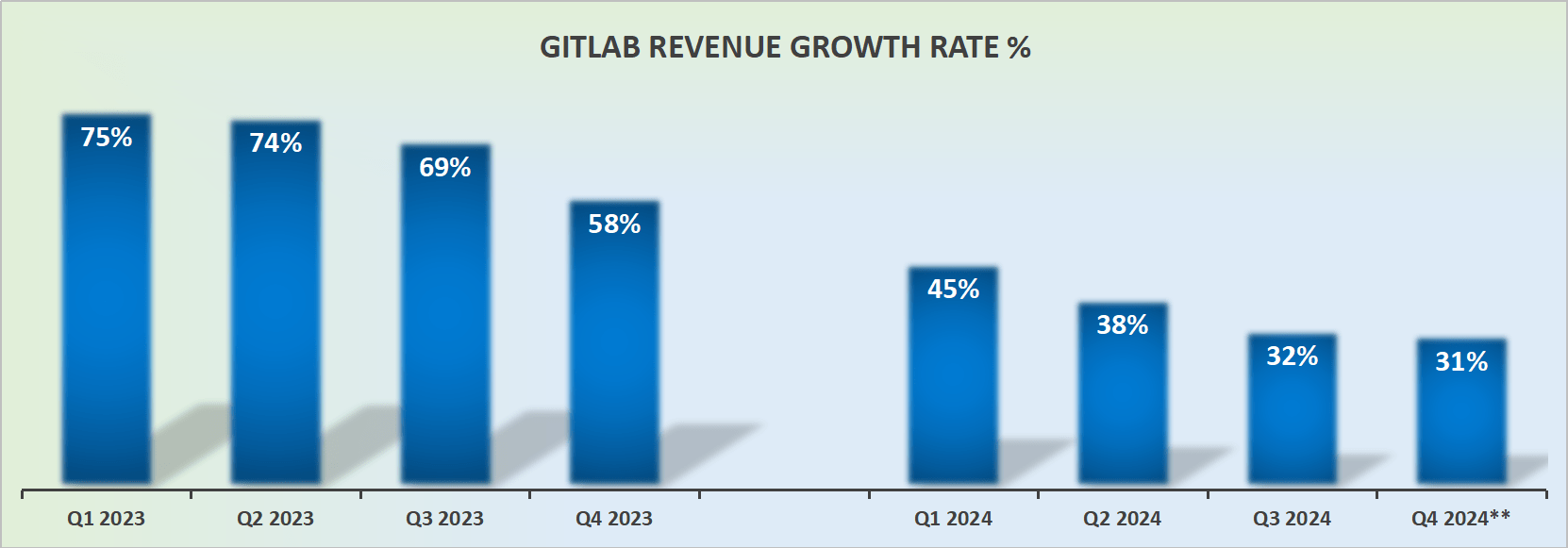

Revenue Growth Rates Are Still Strong, With a But

{kind=link}

There's good news and bad news. The good news is that GitLab is growing very fast. Of that, there's no doubt, and there's little more than can be said about it.

The bad news emerges as soon as we ask, "how fast is GitLab growing in fiscal 2025 (starting February 2024)"? Even though the stock is up significantly on the back of these results, in the coming days, once the dust settles, this question will gain pertinence.

After all, the business is up against easier comparables with the prior year and even as we take the high end of its guidance and add a few points on top of that, the fact remains that GitLab's growth rates are decelerating at a steady rate.

This isn't an immediate problem, but if GitLab's growth rates continue to slow down, investors will soon question whether the stock is too expensive for what it offers.

The Bull Case: Now Profitable

In my previous analysis, I said,

[...] looking out to next year, GitLab reiterates that it will be delivering breakeven free cash flow.

Therefore, we are once again reminded that GitLab is determined to deliver profitable growth.

Indeed, on the back of GitLab's Q2 2024 results, GitLab was expected to end this year with negative operating margins of about -5%. That meant that investors had to wait until the next fiscal year before they could see GitLab as a profitable enterprise.

However, its newly updated guidance now points to positive operating margins of just below 4%. Not only does this mean that there's now a profitable enterprise in GitLab, but also that it's become profitable ahead of schedule.

Why is this milestone so important? Because it shows that despite GitLab clawing towards profitability, it has succeeded in doing so while delivering its fast revenue growth rates.

GTLB Stock Valuation -- 11x Forward Sales

As noted already, it's difficult to get a sense of GitLab's growth rates for next year. Let's make the case that in fiscal 2025 (starting in February 2024), GitLab's revenues grew by 30% y/y.

This would leave the stock priced at 11x forward sales, which, as far as these DevOps companies go, is very much a fair price that lines up with what monday.com ( MNDY ) is priced at. In fact, GitLab's valuation is a few turns cheaper than Atlassian's valuation.

On the other hand, Atlassian is reporting close to $4.5 billion of revenues this fiscal year, while GitLab is reporting about 15% of those revenues. Put another way, investors are paying a much bigger premium for Atlassian for the "confidence" they have that Atlassian can grow at scale as a tried and tested business.

The Bottom Line

In weighing GitLab's investment allure, the juxtaposition of its valuations against its growth rates stands as a crucial consideration. The stock, currently trading at approximately 11x forward sales, reflects a reasonable valuation, especially given its profitability trajectory.

The uncertainties surrounding GitLab's revenue growth rates, while a point of contemplation, are accompanied by a resolute commitment to profitable growth. The positive shift in operating margins to just below 4%, ahead of initial projections, underscores the company's ability to balance growth with fiscal responsibility.

This positions GitLab as an intriguing prospect for investors, supported by its robust financials, a comprehensive toolkit for software development, and a strategic emphasis on DevSecOps integration. The 11x forward sales valuation, in light of the potential 30% year-over-year revenue growth in fiscal 2025, appears not only reasonable but a good entry point.

For further details see:

GitLab Q3 Earnings: Stock Jumps, Decoding Its Prospects