GTLB - GitLab Shows It Can Grow Even When Headcounts Don't

Summary

- GitLab sells a version control system in a DevOps platform that allows large and even pretty disparate teams to work in an effective chain on code for quick deployment.

- They are a scale-up story at the moment, and they try to land and expand in corporate budgets, charging on a per-seat basis for their platform.

- While headcounts are falling in tech, their exposure there isn't big, and the startup exposure is really low at only 5%.

- Even if headcounts fall in other industries that they serve as well, there is still lots of scope for penetration.

- GTLB shares are expensive, but they can keep up growth and that's what their multiple is demanding.

GitLab ( GTLB ) is a high quality company that offers a version control system through its comprehensive DevSecOps platform, that functions as an IDE and a CI/CD system as well, that has other useful features for coders powered by ML and other SaaS infrastructure. It is designed to allow for collaborating on code and also moving it down the chain to the other developer teams that allows for very rapid deployment of code. This CI/CD system is an addition beyond what other version control systems offer like GitHub, which require more expertise on the customer side to integrate themselves. The key sell of the DevOps platform is that it allows for much faster iteration and deployment of code with the possibility of a lot of intermittent, modular testing of the code The metrics in case studies showing 10-15x growth in releases thanks to the streamlined processes. Despite pressure on corporate budgets, they are managing to grow fast, and that's what their high multiple demands. It's hard to say whether their 14x P/S ratio makes sense, because it's such a high multiple with no margin for error, but for now the company is keeping momentum despite significant pressures, and that's a major plus. The lack of exposure to tech is also appreciated, since that's the sector where headcount risks are most pronounced.

GitLab Q3 Earnings Results Breakdown

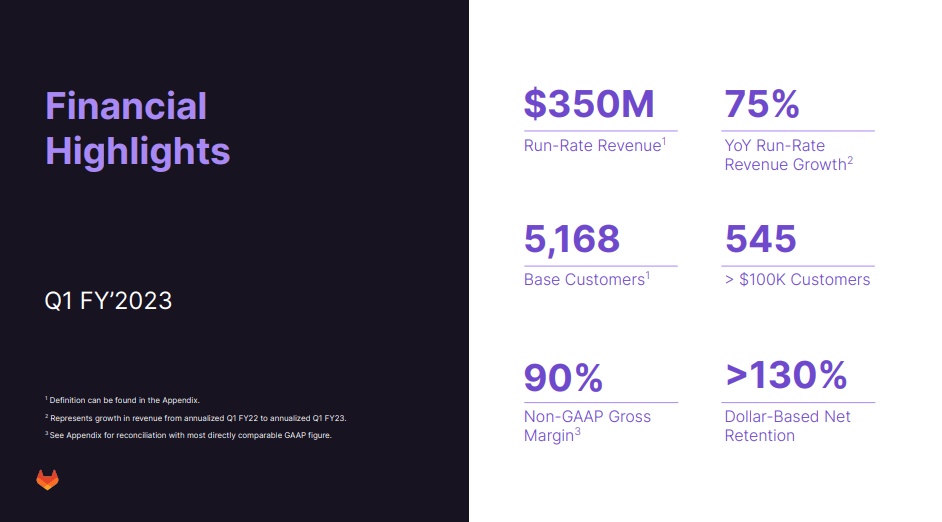

The financial highlights are impressive. It's all about topline, and the company's topline growth is very significant with 75% run-rate revenue growth.

{kind=link}

Financial Highlights (Q3 Pres)

Large customers are the ones that are responsible for a growing share of the revenue growth, and the Ultimate package is what is a larger portion of sales, which means a growing average revenue per seat. This means there is more scope for growth at the companies in which GTLB are landing at higher proportions, and every unit of growth is more valuable. It couldn't be a better topline result.

The ultimate tier continues to be our fastest-growing tier, representing 39% of ARR for the third quarter of FY 2023 compared with 32% of ARR in the third quarter of FY 2022.

It is also testament to engagement with the deeper features that are provided in the Ultimate package, which allow for more instances, more testing, and more passive scanning to reduce error and speed up development and deployment. Other features like machine learning based 'staffing' and security features are a bonus as well provided to Ultimate customers, and the proven appeal should be welcomed by shareholders.

{kind=link}

IS (sec.gov)

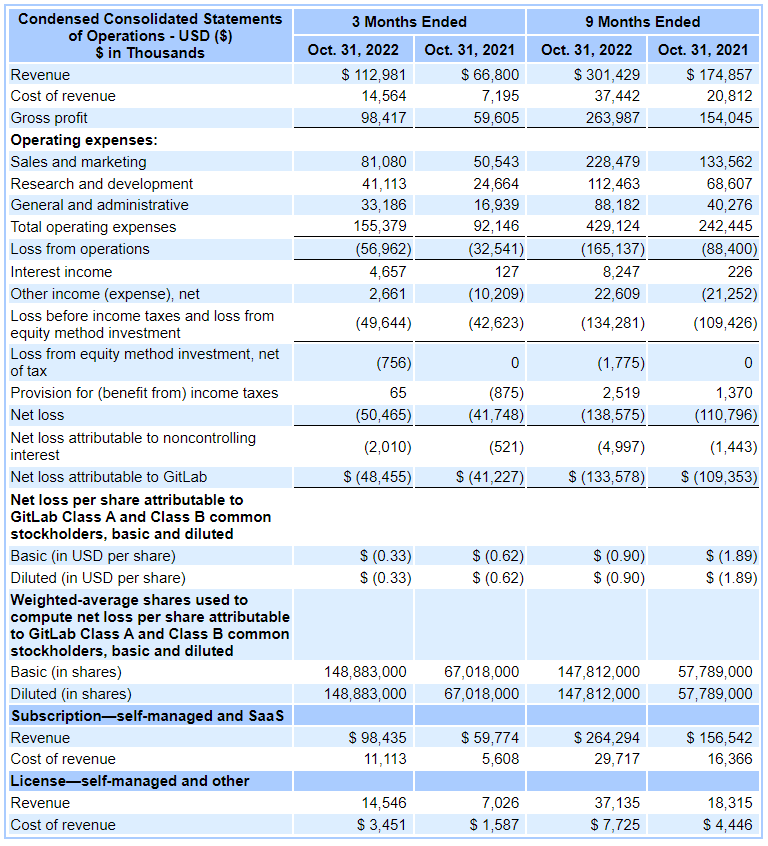

The profitability isn't so great . GM is flat, and as more SaaS elements are packaged into the offering, that GM should decline slightly over the next couple of years. This is one of the pains of scaling. However, some costs responsible for about 10% of the current OPEX related to a China launch are going to draw back soon. Ultimately, the majority of bloat is coming from sales and marketing, and considering the scope for high lifetime customer values and the growing average revenues per customer and per seat, we welcome this expense because really it's an investment.

Bottom Line

Indeed, it's this land and expand concept that makes GTLB appealing. Firstly, old cohorts are still growing quickly. Companies that started working with GTLB 7 years ago are still expanding their use of GTLB, and are a growth source.

To illustrate this, customer cohorts from seven years ago are still expanding today. Despite the ongoing volatility in the macroeconomic environment in the third quarter, we see customers continuing to prioritize the need to leverage a mission-critical platform to build software better, faster, cheaper and in a more secure manner.

Brian Robbins, CFO

New cohorts are larger customers who are launching on the Ultimate package. It can take some years in some cases for all the engineers in a company to end up on the DevOps platform by GTLB, so the current revenue growth is just the first breath into the embers that are going to be a slow-burn source of growth. It's just that there are so many new orders that the current run-rate figures end up being so phenomenal.

The P/S is 14x which is really substantial. The company is guiding for over 50% revenue growth next quarter YoY against a tough Q4 2021 comp, so they are expecting further revenue growth even as macro headwinds take hold of the economy. They are 20% exposed to tech, and only 5% exposed to startups, so macro pressure has apparently not been that noticeable by the company. Even if headcounts shrink in tech, because penetration within companies grows slowly, there is usually growth scope even in shrinking headcounts for GTLB in the limited tech exposure. In other industries there is generally more scope for digitalisation and growth, so GTLB should not have a problem. Overall, the macro headwinds are pretty limited, only minor signs of budgetary contraction are showing themselves in client interactions, but the revenue growth should persist. It's not such a surprise that after this earnings call people really started buying, with the stock price up 9% with last close.

Still, the day before there was substantial selling, and the markets are still clearly apprehensive about high multiple stocks - but only when growth looks threatened. GTLB is one of those cases where it's not.

However, a 14x multiple implies massive need for growth, and it has to be upfront so that the company can then shift its focus to profitability and cash flow. The models here are sensitive, and with the market being uncertain, there's no margin of safety here despite the great quarter. Overall, GTLB is a pass for the prudent investor. There are tech opportunities out there for much less.

For further details see:

GitLab Shows It Can Grow Even When Headcounts Don't