GTLB - GitLab: Unique Competitive Positioning Creates Appeal

2023-10-17 08:30:00 ET

Summary

- I will share with you a review of the GitLab business broadly, as well as a review of its Q2 2023 earnings.

- In my view, GitLab has been an overlooked, very high-quality software platform that operates in something close to a duopoly with Microsoft's GitHub.

- With ~$1B in cash, no debt, glimmers of free cash flow generation, and decades of growth runway ahead, I believe GitLab represents an attractive value in the mid-$30s and below.

- I do believe it will do well from $45/share-plus. However, as I will demonstrate, I've been consistently waiting to accumulate in the low to mid-$30s/share, and I believe we'll get swings at these levels again in the future.

Revisiting GitLab

In 2021, we initiated coverage of GitLab (GTLB). However, at the time, we found the business to be too expensive from a valuation perspective.

Notably, we liked the business a lot at the time but could not make sense of its valuation.

We then wrote about the business again in mid-2022 but still found it to be too pricey.

Although GitLab checks out on most of our crucial characteristics, it fails to suffice our requirements on valuation. At ~$50 per share, GitLab trades at a forward P/S multiple of ~33x, which is pretty high even for a high-margin and extremely sticky SaaS business. In my view, the stock is fully valued in a market where growth stocks have been hammered to such an extent that most of them are trading way below their fair values. Hence, I am a bit cautious about GitLab.

Gitlab Stock: Taking On Microsoft's GitHub And Holding Its Own

Incredibly, when I (Louis) personally wrote about the business again in September 2022, I still did not believe it was attractively priced, though I said, at the time,

The one issue, as was the case in our original note on the company, is its valuation. With 191M shares outstanding (fully diluted), GitLab presently trades at about $11B in market cap. On an EV to fwd. 12 mo. sales basis, GitLab trades at about 19.7x EV/fwd. 12 mo. sales. This is very expensive. We will wait until $30/share to $35/share, which is where it touched recently.

Finally, in late 2022, during "The Land of the 10 Bagger" market capitulation as I called it at the time, the business fell to the mid-$30/share range where, as I reasoned via the work above, we'd be buyers, and I began buying.

I specifically reasoned that the mid $30/share range would be my buy point for two reasons:

- At that point, the business traded at an enterprise value of $4.4B. Considering Microsoft bought its direct peer, GitHub, at $7.5B in 2018, we thought the value here was likely higher than the market's appraisal of $4.4B in enterprise value (we also traced the growth of fcf/share using assumed margins and growth rates as well, of course, but the GitHub deal was certainly a component of my thinking by November of 2022).

- Google (GOOGL) (GOOG) was a buyer in the mid $30/share range on the open market, which suggested to me that, in an absolute worst-case scenario, GCP or AWS would be willing to "Save the business," were things to go catastrophically wrong for one reason or another. Of course, the business operates in what amounts to a duopoly with GitHub (my opinion of course, and all are welcome to disagree), and it has $1B in cash and no debt whatsoever, so it would take a lot for things to go so wrong, but the GCP/AWS components of the thesis gave me the confidence in March of 2023, when the stock was collapsing 30-40% in a matter of weeks, to state the following:

My Thinking In March of 2023 Following GitLab's Stock Price Collapse

Beating The Market's Business Operating System Channel

In this vein, I found the following commentary from GitLab's CEO noteworthy:

The second topic I want to discuss is how we intend to capture the large DevSecOps market opportunity with a strong go-to-market motion. Strategic partnerships are an important part of our go-to-market execution, and I would like to highlight Google Cloud and AWS ( AMZN ) as two of the most significant. GitLab and Google Cloud are strongly committed to delivering secure enterprise AI offerings across the software development life cycle.

We are thrilled to be working with Google Cloud on delivering our vision of AI-powered workflows. We are leveraging LLM foundational models, including the new coding model family to deliver new AI-powered experiences to all users involved in creating secure software.

Our partnership with Google extends even further. At this year's Google Cloud Next. We announced our plans to integrate GitLab into the Google Cloud console.

GitLab also received the 2023 Google Cloud Partner of the Year Award for the third consecutive year. Google recognized GitLab for our achievements in application development within the Google Cloud ecosystem.

Another key partner is AWS. In Q2, AWS introduced support for GitLab in AWS code pipeline. This is a fully managed continuous integration and continuous delivery service. This new AWS capability allows developers to leverage their The DevSecOps Platform source code repository to build, test and deploy co-changes with AWS code pipeline.

Gartner Magic Quadrant 2023 illustrating the GitLab and GitHub duopoly (again, you may disagree with my characterization here, and that's fine. It's my perception, which can be and is wrong at times):

Gartner Magic Quadrant

Gartner and Forrester issued reports officially recognizing DevOps platforms. This is the category we created. And these reports validate the category's significance and importance. We also proved that the market is moving from point solutions to platforms. I'm thrilled with where these industry analysts place GitLab within the category.

We were named a leader in the Gartner, Magic, Quadrant for DevOps platforms and we scored the highest in our ability to execute of all the participants. And we were the only leader in the Forrester Wave integrated software delivery platforms.

For those that accumulated during early 2023 and late 2022, congratulations on the 50%-plus returns since. I do think GitLab will become a 5x to 10x outcome in the decade ahead from the mid $20/share to mid $30/share range.

Let's now apply my foundational investment frameworks, which I share often with you, my reader, to the business of GitLab.

Understanding GitLab

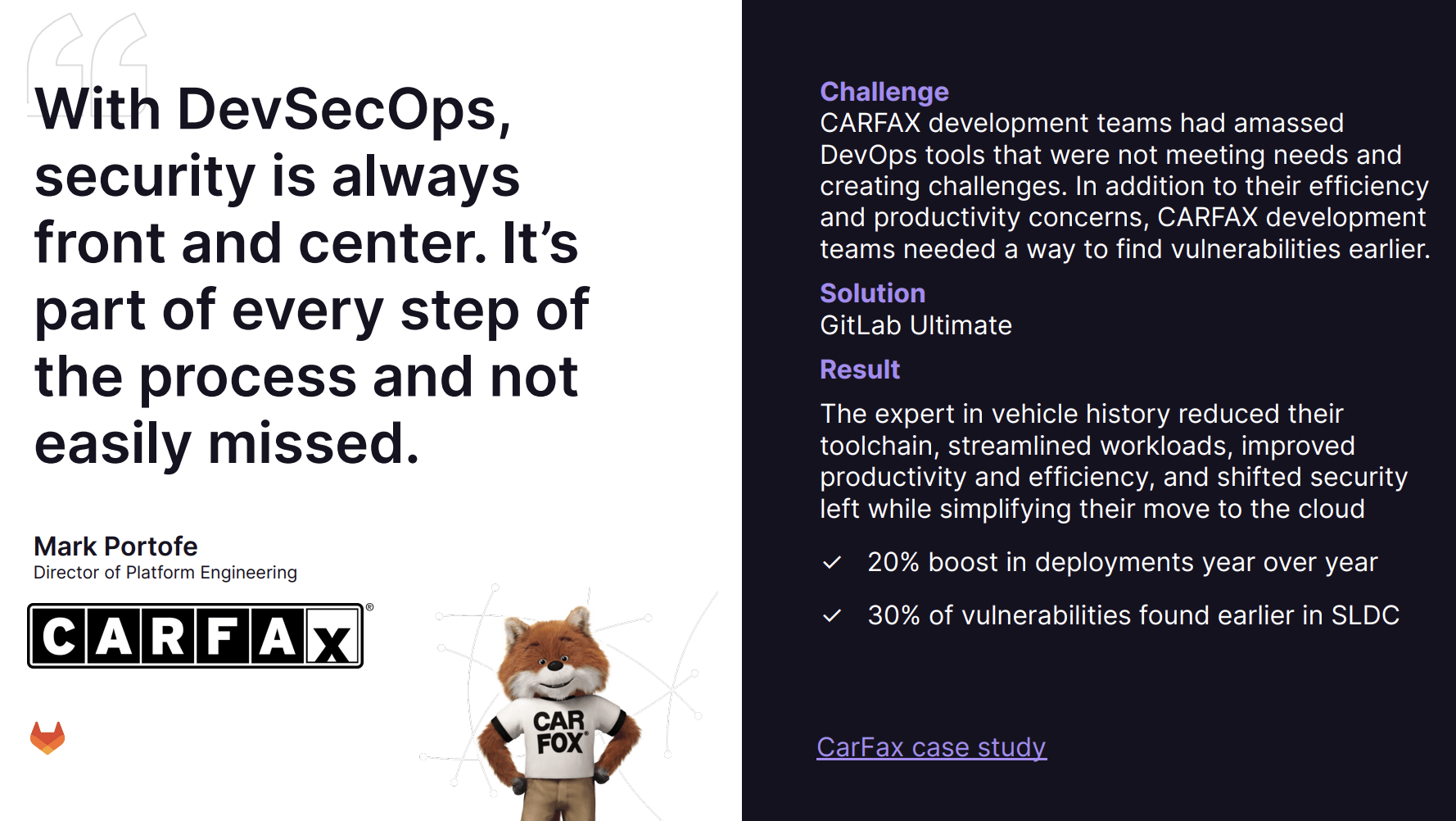

One particular example is the public sector. Speed to mission is imperative in this vertical. GitLab customer, Navy Black Pearl demonstrates this value proposition well. Navy Black Pearl is a DevSecOps service developed and managed by Sigma Defense. This service creates mission applications for the U.S. Department of Navy. Black Pearl uses GitLab to quickly create new applications and continuously modify code in response to evolving requirements and priorities.

Using GitLab, Navy Black Pearls' teams have designed and created custom operational software environments within days rather than months.

A few key elements of the GitLab platform drew me to the business over the last few years despite the valuation concerns:

- GitLab has built a vertically integrated platform on a single source of code.

- The business has solid gross margins and embedding moats, which indicate to me that it has the capacity to expand its free cash flow margin to 20%-30%+ in the decades ahead.

- The business has, like all of our companies, an almost preposterous amount of cash on its balance sheet relative to its age. It also has no debt.

Let's explore the first point a bit together today.

Over the last few months, I've done my best to educate you on the process underlying my business selection.

To a very large degree, as something of a tongue-in-cheek aside, we're buying "pristine balance sheets" such that there are almost preposterous amounts of cash and no debt for the companies we own. This is, indeed, a key component, alongside a series of other components, that draw me to the businesses I like.

As a genuine request to those who may not own many of the businesses for which I create research, please direct me to companies that operate industry- and category-defining products that simultaneously have massive cash hoards and no debt. I'm open to buying most businesses, even outside of the scope of my focus, i.e., consumer discretionary, financial technology, and software. However, I've usually struggled to find the perfect combination of industry-leading products alongside massive cash hoards and no debt elsewhere.

Of course, we're not just buying balance sheets.

Each of the companies I own fits within one of our four foundational investment frameworks, which I've delineated for you often over the last few months.

A solid portion of my companies also fit within multiple frameworks, as is the case for GitLab.

Applying my foundational investment frameworks to GitLab, I believe the business fits within the first and third frameworks, which are:

1. Vertically-integrated product, capture market share in the stagnant mature industry: We target businesses that have created a fully vertically integrated product, within a fragmented, low NPS, and mature industry, whereby that vertically integrated product offers 10x better value; therefore, it captures significant market share rapidly. (Notably, as an example, Monday's platform has become more and more vertically integrated, as it's added MondayCRM, MondayDev (for developers), and its app marketplace products in addition to its core work management product, all of which sit atop Monday's proprietary, open, and configurable architecture. It's a true, vertically integrated work operating system, which, with the creation of MondayDB is more scalable than ever, the evidence of which can be seen in the company's enterprise customer growth, which we'll review later.)

3. Quality cultures that breed innovation within the larger conglomerate: We've often explored the Spawner framework (I'm working on a different name), which entails a company's ability to launch, or spawn, a new successful business/product after a new successful business/product, creating a nucleus of explosive, compounding sales growth. This is the idea that a business creates a culture in which its employees create new products successfully. With multiple products growing rapidly simultaneously, the business overall grows more rapidly and more durably. Some of my favorite examples that fit within this framework are Axon (AXON), Monday (MNDY), Adyen (ADYEY), Sea (SE), Tesla (TSLA), Amazon (AMZN), and MercadoLibre (MELI). Indeed, many of our businesses possess this incredible cultural structure, and that is why we've chosen to own them.

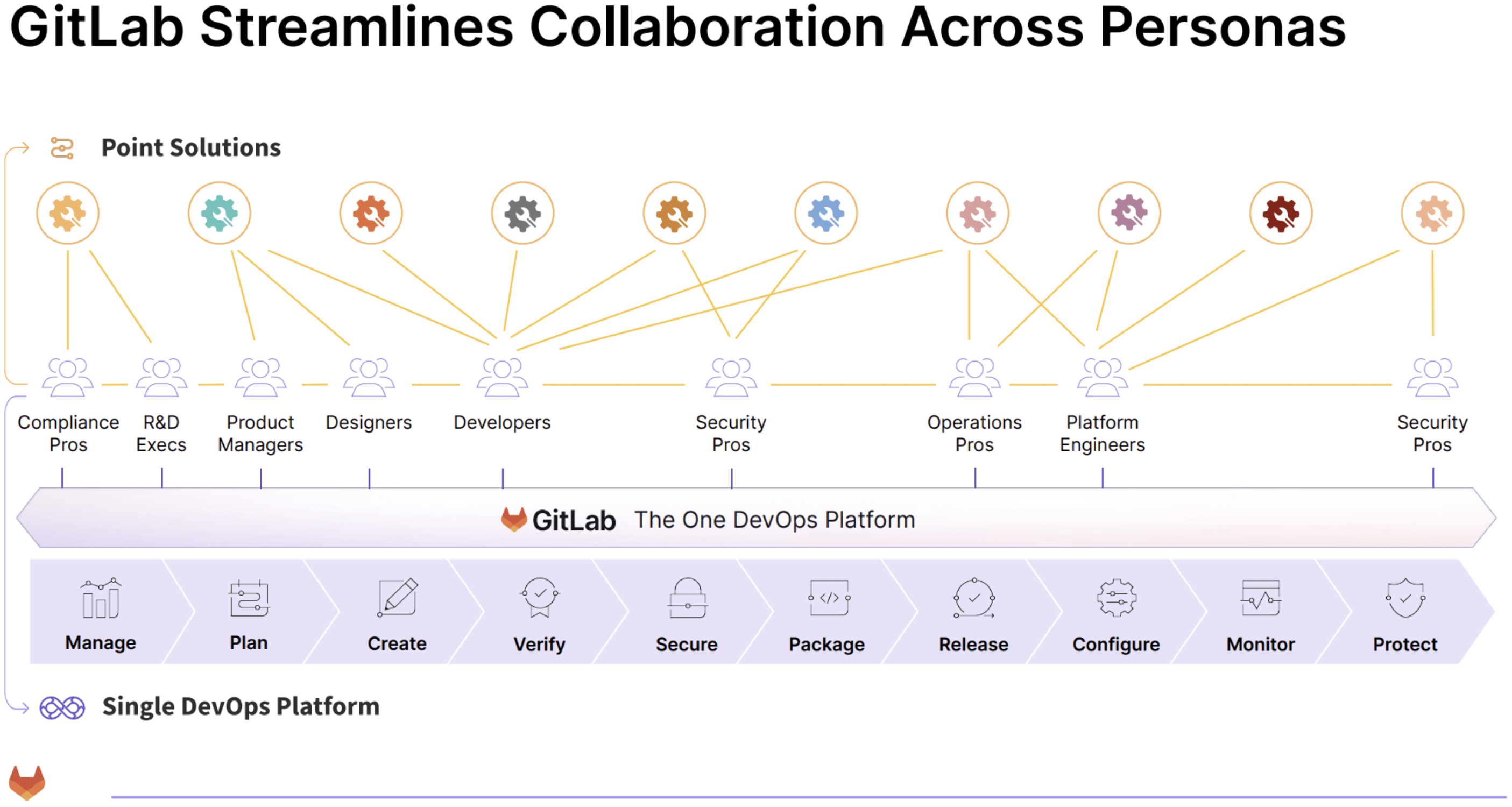

We can see the vertically-integrated nature of the GitLab platform in the slide below:

GitLab Has Vertically Integrated The Multitudinous Point Solutions In The DevOps Ecosystem

{kind=link}

This is the category we created. And these reports validate the category's significance and importance. We also proved that the market is moving from point solutions to platforms. I'm thrilled with where these industry analysts place GitLab within the category.

Sid Sijbrandij, CEO, GitLab Q2 2023 Earnings Call

BetterCloud is a market-leading SaaS workflow automation platform. They turn to GitLab to secure their software supply chain. In Q2, they renewed their business with GitLab to consolidate the fragmented tool chain. And as a result, BetterCloud deprecated multiple security point solution providers. This strengthened data security posture while also enhancing automation and increasing developer satisfaction. GitLab enables customers to make their software more secure without sacrificing speed. This differentiated value proposition resonates across all verticals.

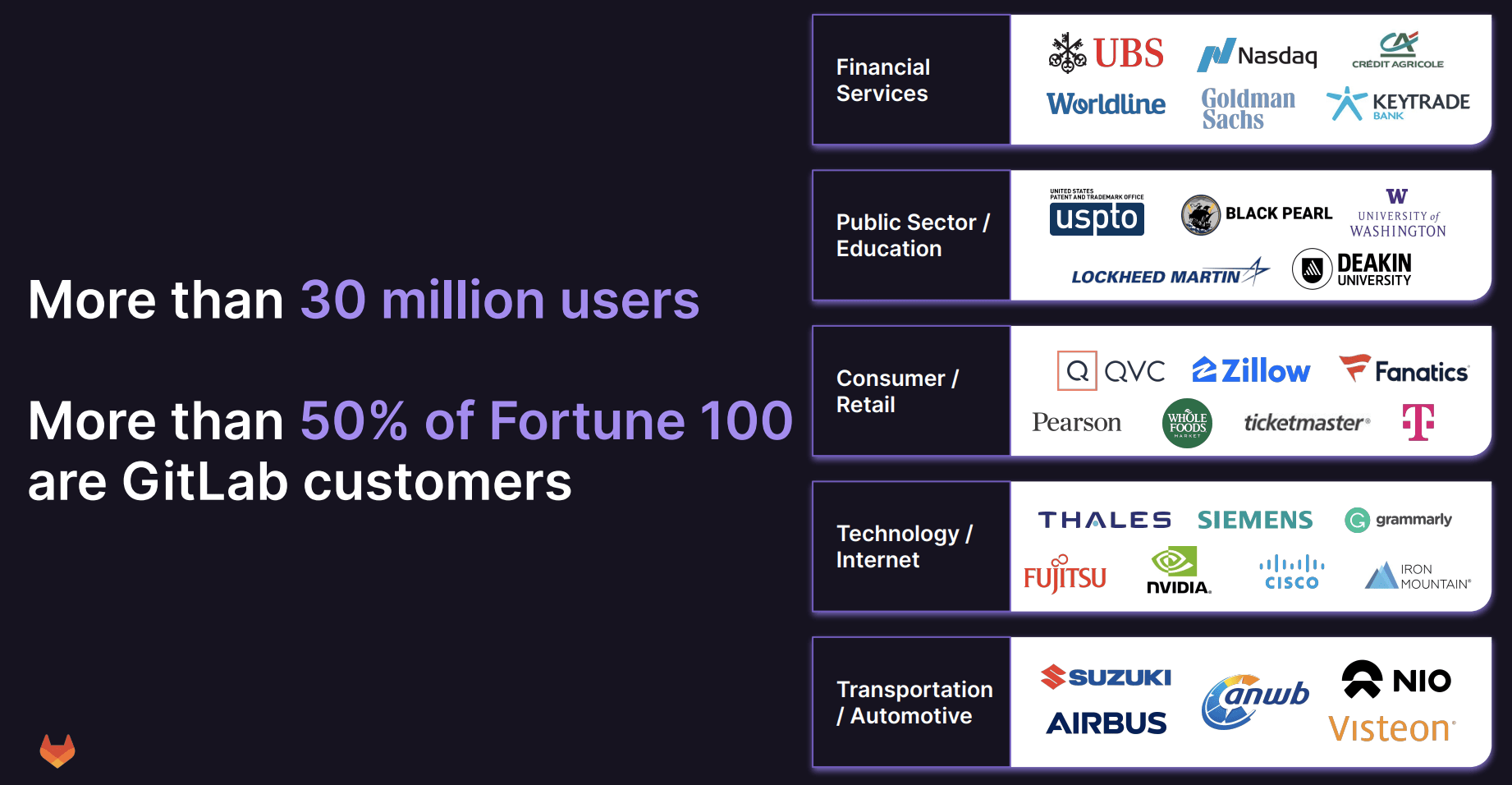

This vertical integration has been a key element driving the adoption of the platform by some of the largest multi-national corporations on earth.

GitLab's Customers Span Many Different Industries And Are Some Of The Largest Companies On Earth

GitLab Q2 2023 Earnings Presentation

{kind=link}

A GitLab Customer Case Study: CarFax

GitLab Q2 2023 Earnings Presentation

{kind=link}

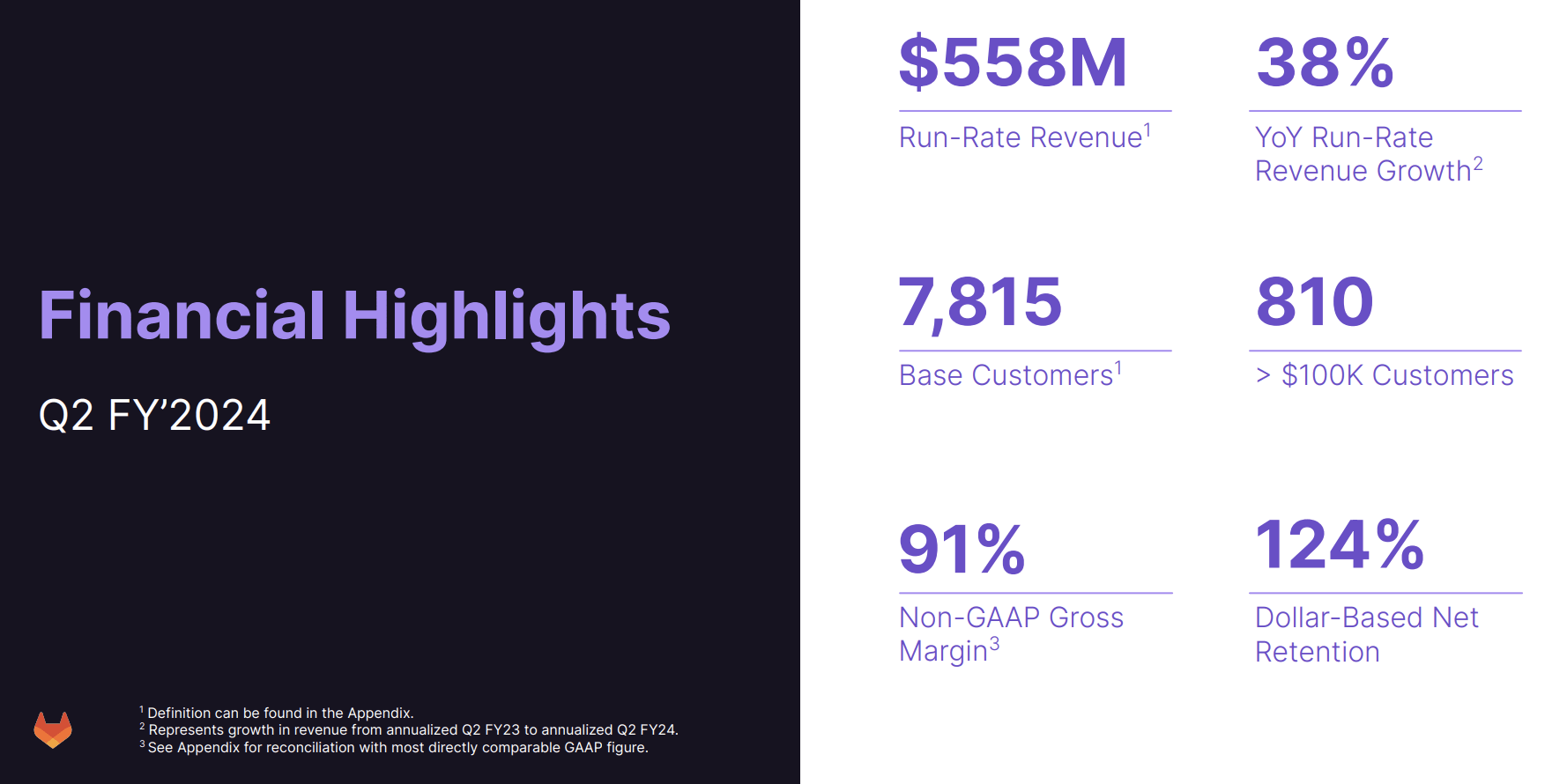

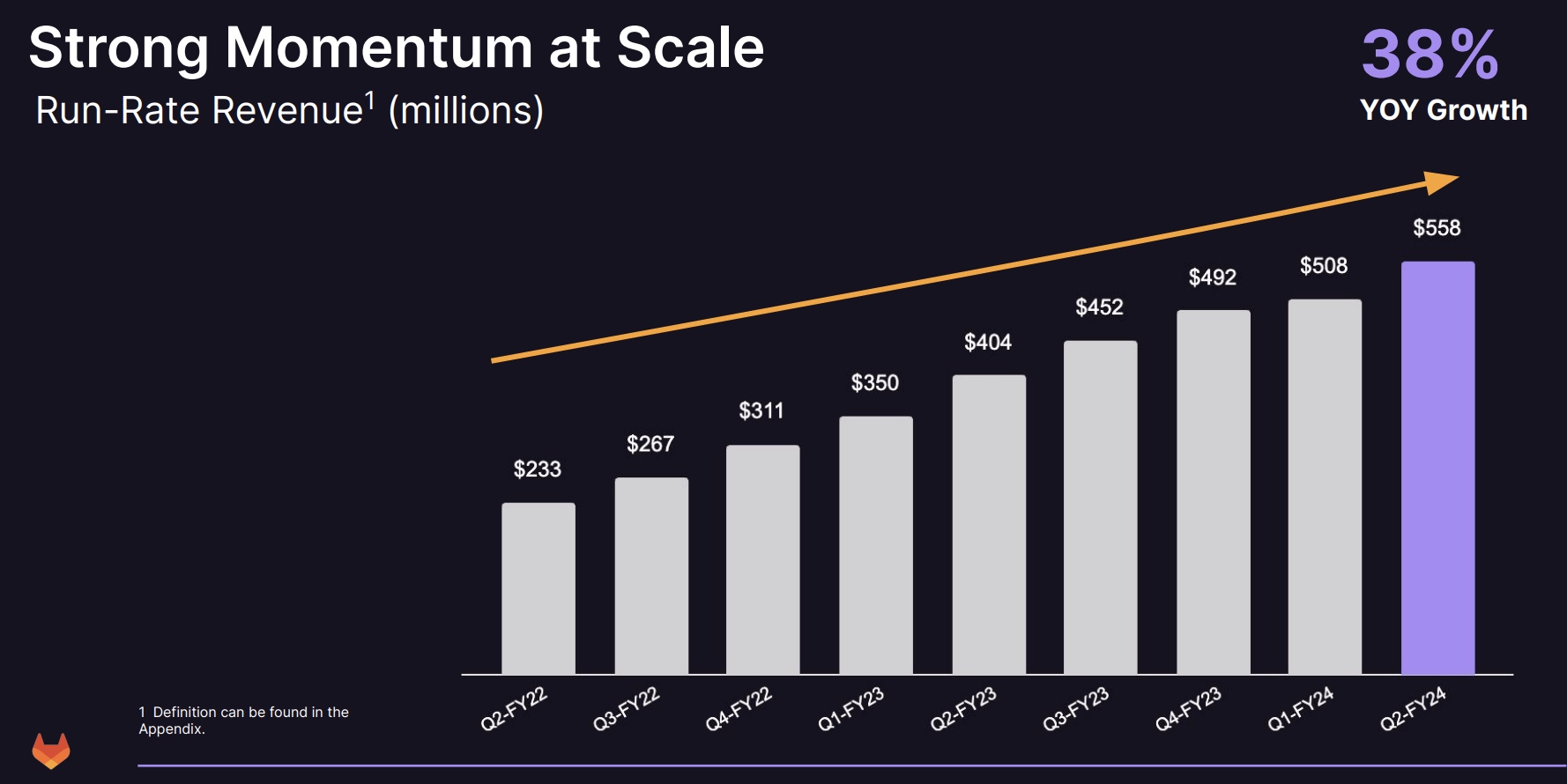

Which has driven the incredible sales growth we've witnessed over the last few years:

Note The Truly Exceptional 124% Net Retention Rate

GitLab Q2 2023 Earnings Presentation

{kind=link}

Late 2022 and Early 2023 Was Brutal For Software, Which Created "The Land of the 10 Bagger," Though Things Have Stabilized A Bit As Of Late

GitLab Q2 2023 Earnings Presentation

{kind=link}

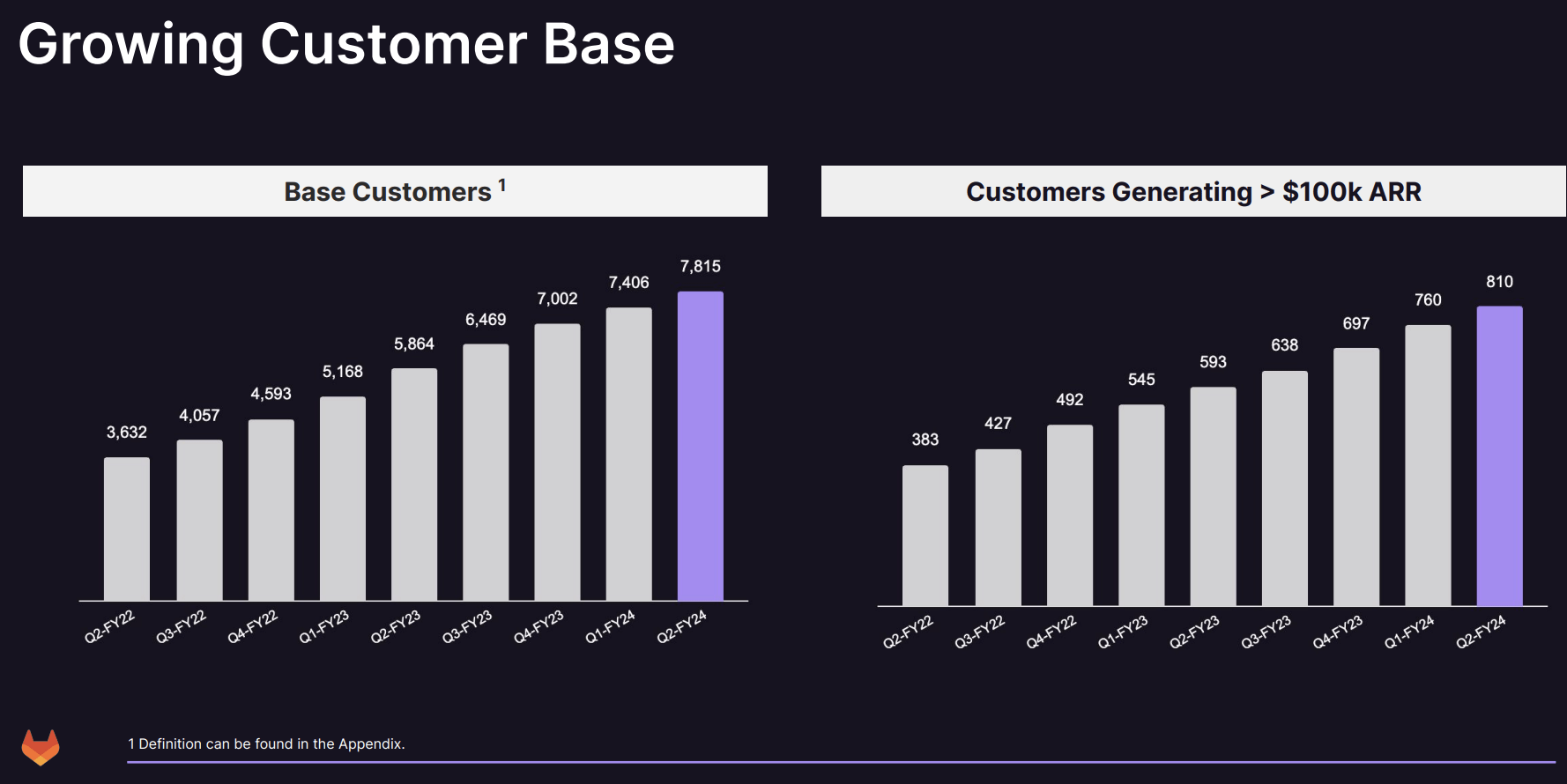

GitLab's Rapidly Growing Customer Base

GitLab Q2 2023 Earnings Presentation

{kind=link}

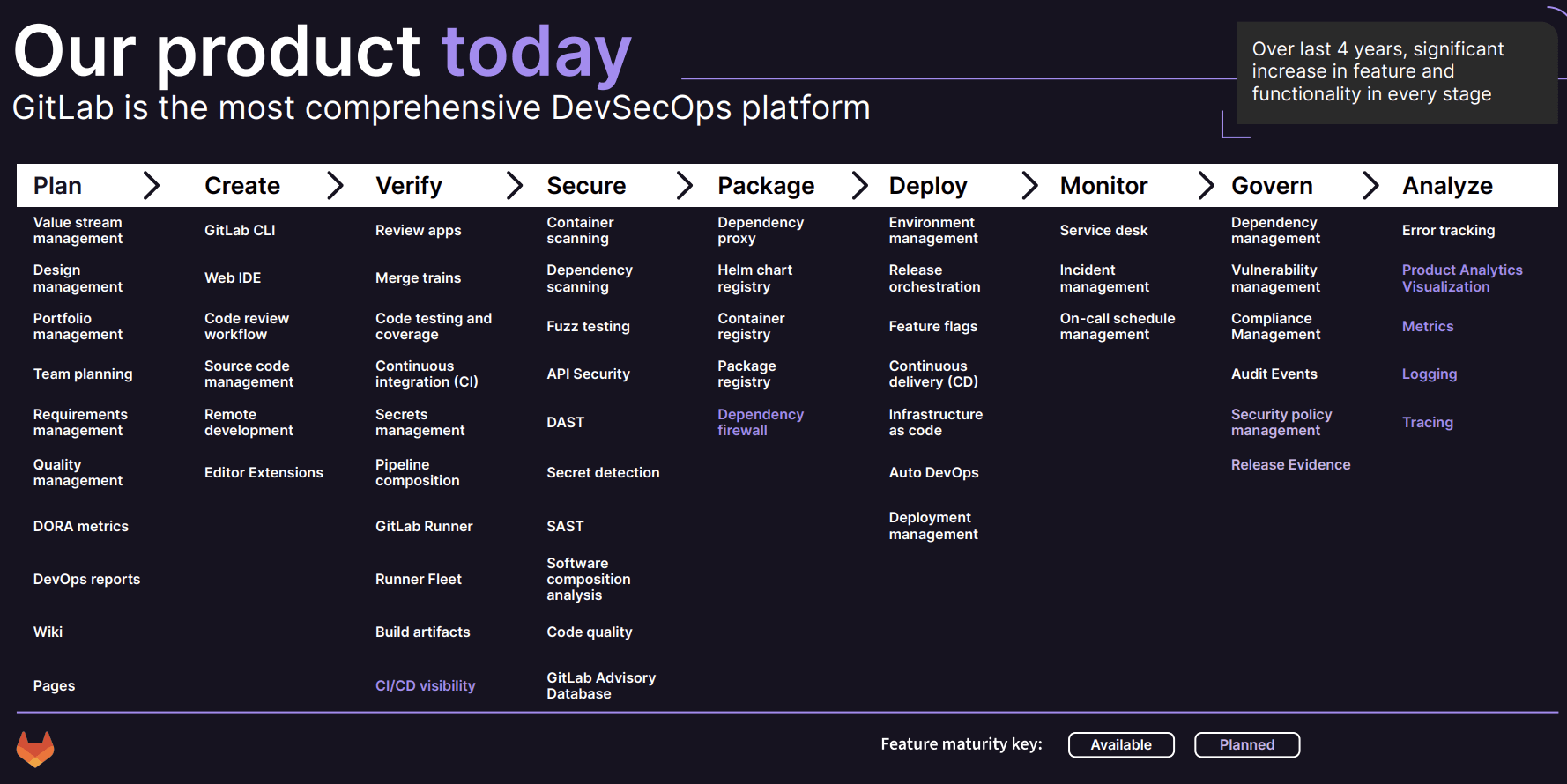

Turning to the evidence of the third foundational, GitLab has demonstrated that it has an exceptional culture that drives rapid internal product development.

The company operates on a monthly product release schedule, and it has released product updates for many months, which have turned into years, consecutively.

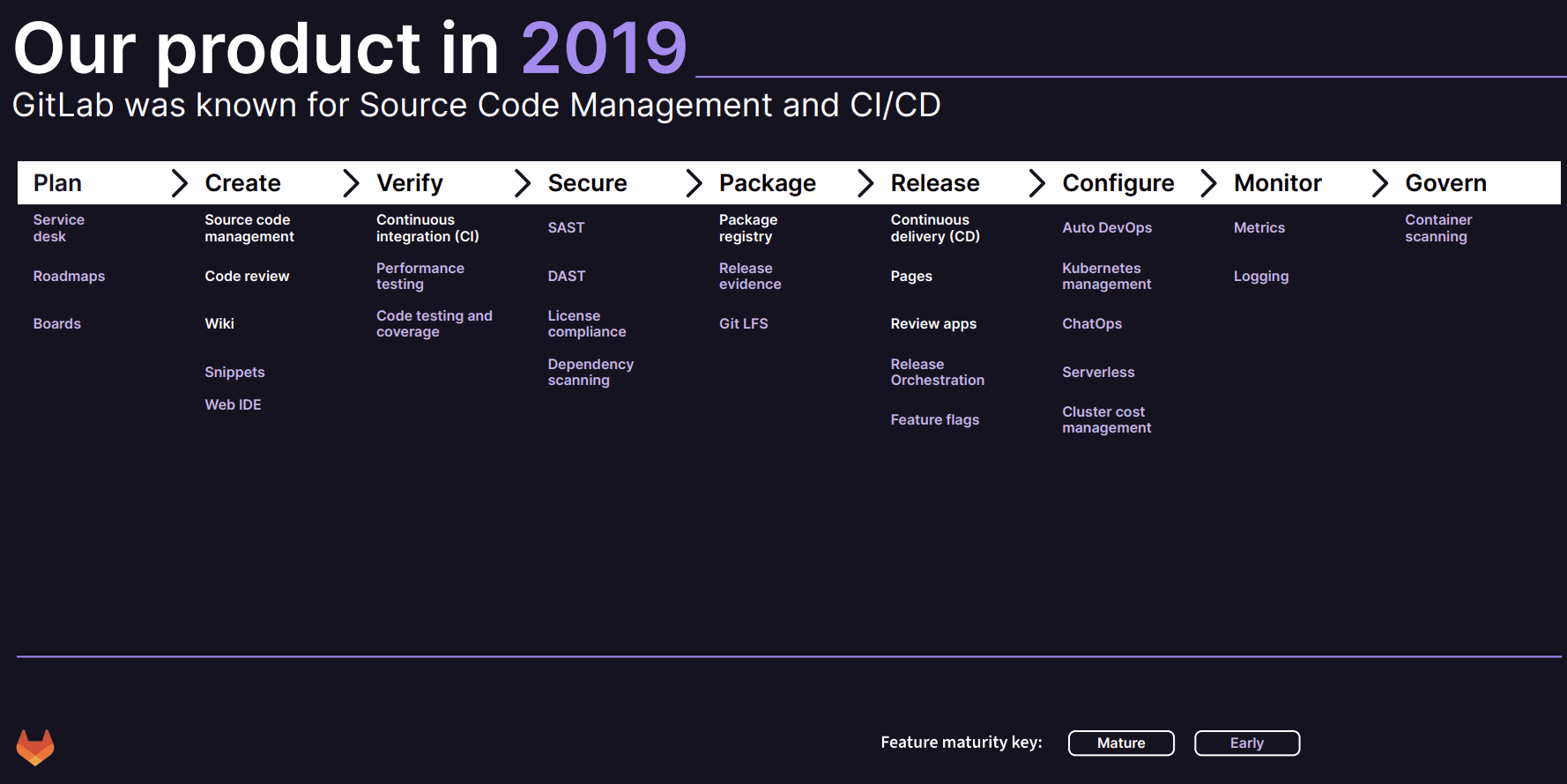

Below, we can see the product roadmap that GitLab has set forth, which will guide its internal product development dispensed through the aforementioned monthly updates.

GitLab's Product In 2019

GitLab Q2 2023 Earnings Presentation

{kind=link}

GitLab's Product By 2023 Evolved Immensely, Demonstrating The Third Foundational Investment Framework

GitLab Q2 2023 Earnings Presentation

{kind=link}

Allan Verkhovski: Hey, guys. Thank you for taking the question. So following the appointment of Chris Weber, CRO, can you guys just talk about what he's been focused on. What's he is looking to implement to help the company scale the next phase of growth? And how are you thinking about potential sales disruption for the year?

Sid Sijbrandij: Yeah. Thanks for the question. So we're really excited to have Chris Weber on board. He's a very experienced sales executive. He's been responsible for multibillion-dollar sales organizations, and that's what we, as a company, want to go to hit. The transition has been very seamless from our side. We spent a lot of time listening to our customers, listening to our sales team. There's no big changes in our go-to-market, so very smooth and setting us up for success in the future.

So long as GitLab continues to innovate internally, building a more expansive and more valuable vertically integrated platform atop a single source of code, I think it will glide through billions in sales in the decades ahead.

In short, the first and third foundational investment frameworks are key components of my ownership of the company, and they are key components of the business' success over the last half-decade, as evidenced by its exceptional growth, and recent free cash flow generation.

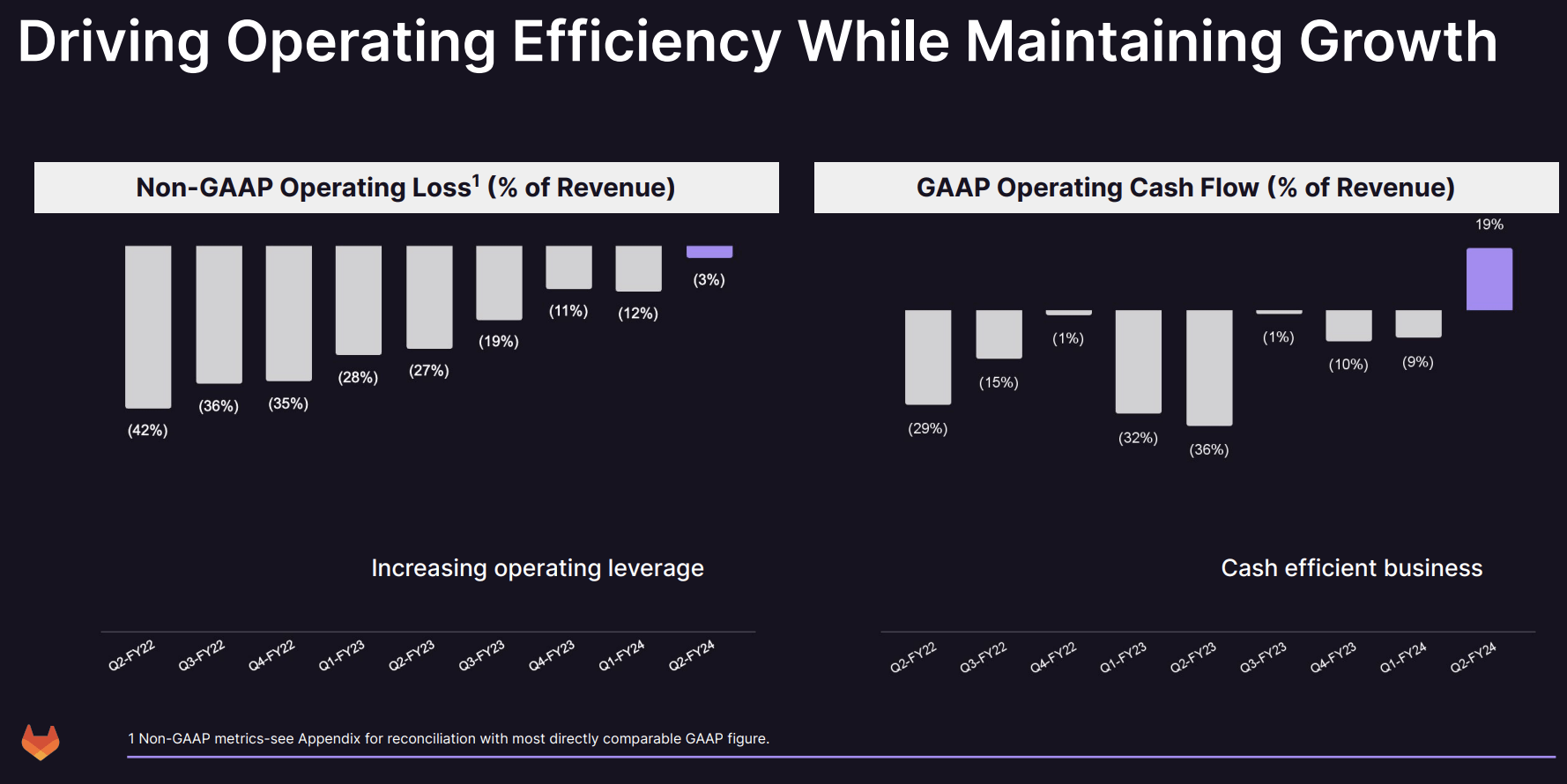

Cash Dynamics

As of Q2 2023, GitLab now generates free cash flow, though it may bounce between a loss, breakeven, and free cash flow generation for the next few quarters before sustainably generating free cash flow.

The business is, to be sure, still quite young.

GitLab Generates Robust Free Cash Flow In Q2 2023

GitLab Q2 2023 Earnings Presentation

{kind=link}

In my prepared remarks, I did say it's likely that we'll reach non-GAAP operating income positive in 3Q. And then we also reconfirm and committed to being free cash flow positive in FY '25.

Many younger companies have IPO'd over the last few years, and, due to their youth, when they went public, they were not free cash flow positive, choosing instead to invest their massive cash hoards alongside no debt into capturing market share and driving growth.

As of late 2023, these are indisputably free cash flow generative businesses, generating healthy free cash flow alongside giant cash hoards and no debt.

Notably, atop these cash-rich foundations, these businesses could, and, in my opinion, will, grow at elevated rates for decades to come, creating the 5x, 10x, and beyond return profiles that are certainly possible (and, in my opinion, probable).

Concluding Thoughts: 90% of IT Still On-Prem

In the interest of brevity, I won't belabor the idea that cloud computing still has a very long runway for growth. However, it certainly bears repeating.

The Cloud Is Still Only 10% Of Total IT Spend

Datadog Q2 2023 Earnings Presentation

GitLab articulates this runway as follows:

GitLab's TAM

GitLab Q2 2023 Earnings Presentation

{kind=link}

Sid Sijbrandij: Yeah. I think that cloud optimization has been a lot of kind of consumption patterns that were hit. I think we were less - much less impacted by that. We do have seen the decline of kind of the expansion of kind of hiring more developers and things like that. I think that's been a headwind for us. And I think as far as moving application development to the cloud, I think we still have a long way to go. We regularly partner with big companies, and they still have a lot of things that need to move to modern practices. A lot of things are still not DevOps. They're still not cloud native. So there's still a big shift ahead of us.

In closing, I think I will wait for GitLab to fall back into the $30s to accumulate further. I am not sure I like the valuation so much here. However, I'm very satisfied with the business and our original entry point!

Thank you for reading, and have a great day.

For further details see:

GitLab: Unique Competitive Positioning Creates Appeal