GBCI - Glacier Bancorp Deserves Some Upside

2023-06-20 14:24:30 ET

Summary

- Many community banks are trading lower than in February, creating potential buying opportunities for investors.

- Glacier Bancorp, Inc. has a stable deposit base and ample liquidity, making it likely to survive any deposit withdrawals.

- Despite some volatility and a decline in non-interest income, Glacier Bancorp is a decent 'buy' candidate with a lower price-to-earnings ratio than most companies in the space.

In March of this year, the banking sector, particularly the community banking sector, took a wallop. Starting with the collapse of Silicon Valley Bank (SIVBQ) and extending to other banks as fears of collapse spread, the crisis created a great deal of uncertainty for investors in this space, as well as the investment community more broadly. Some of the companies ended up failing, while others were pushed down justifiably.

Some, however, experienced downside pressure that was unwarranted. You would expect the market to quickly account for this by allowing the share prices of these firms to recover. And to some extent, that has occurred. But even so, many of the companies in this space are trading substantially lower than they were in February. This is created an interesting buying opportunity for investors to consider taking advantage of.

One firm that I would say should be on the radar of investors but should not be a high priority prospect is Glacier Bancorp, Inc. ( GBCI ). With a market capitalization of $3.9 billion, this banking holding company is quite small. At the end of the day, it very likely will survive the current pain. In fact, I suspect that shares will, in due time, move up from here.

I do not, however, think that this is the most compelling prospect on the market at this time. While GBCI shares warrant a "buy" rating, I would say that there are better prospects that can be had at this time.

Dissecting Glacier Bancorp

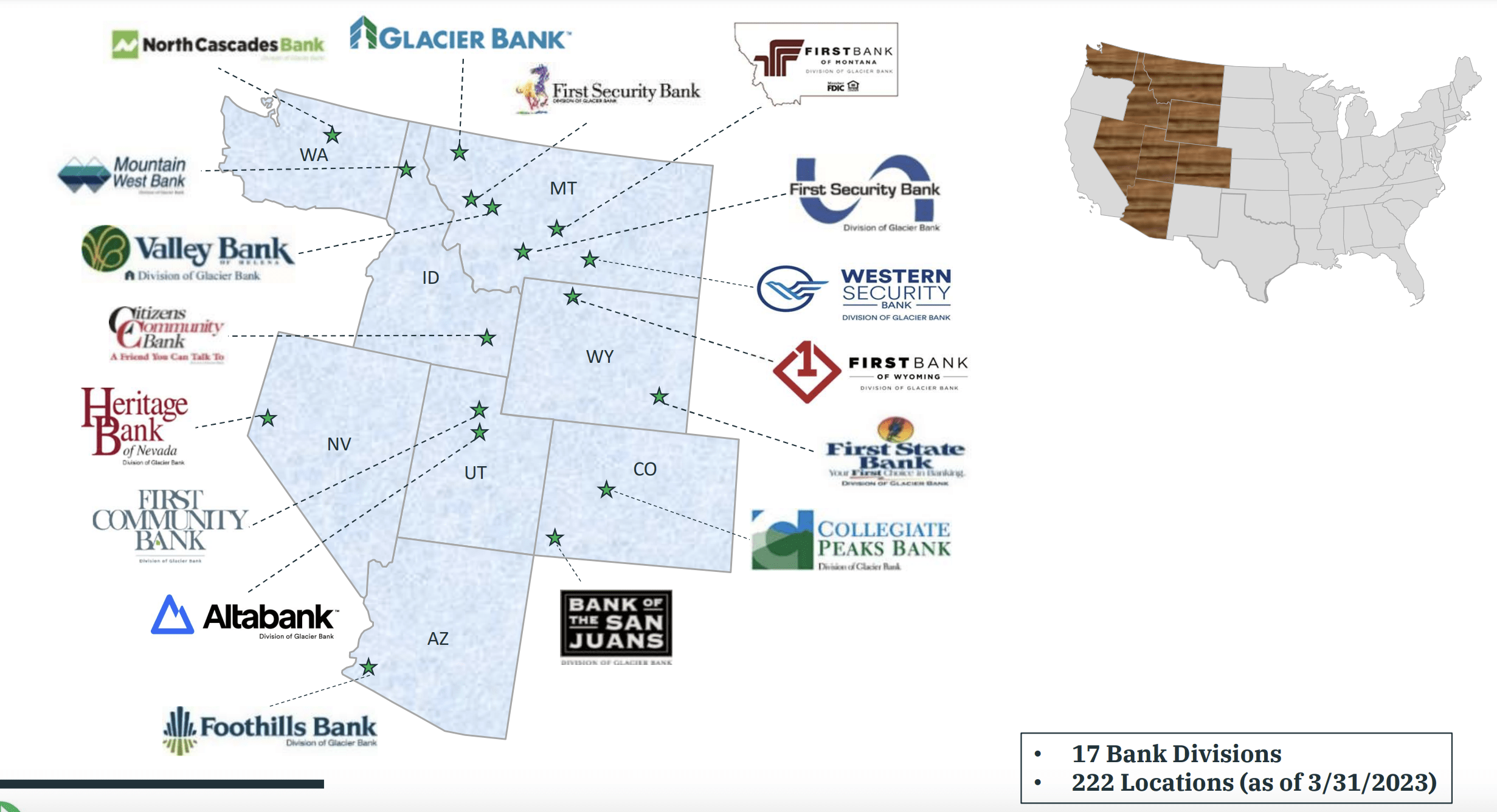

At the end of its most recent quarter, Glacier Bancorp served as the parent company of multiple subsidiaries that collectively operated 222 locations throughout Montana, Idaho, Utah, Washington, Wyoming, Colorado, Arizona, and Nevada. Through 17 different bank divisions, as well as its corporate division, the company provides customers with a wide range of services. These include retail banking activities, business banking, real estate, commercial, agricultural, and consumer, loans, and more. It also offers mortgage origination and loan servicing activities.

{kind=link}

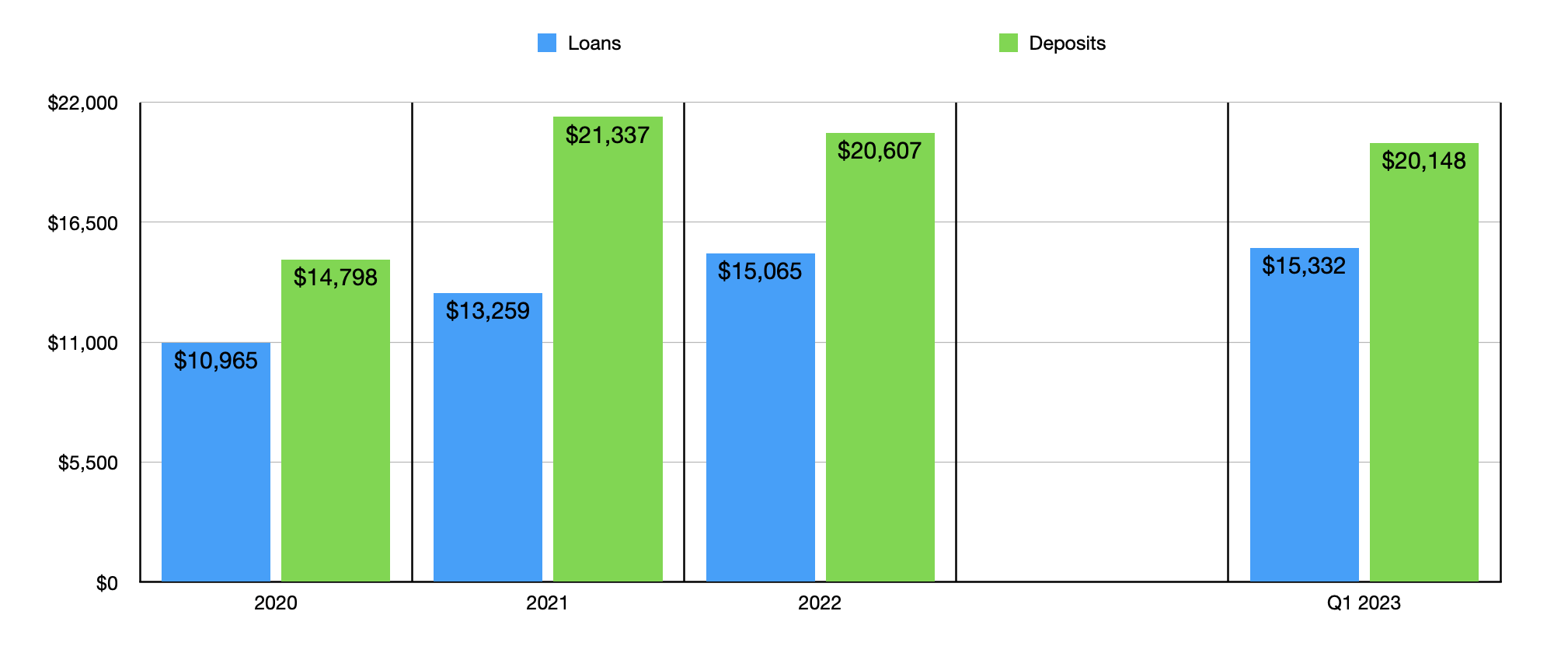

Over the past few years, the company’s deposit base has been a bit volatile. In 2020, total deposits for the company came in at $14.80 billion. This number jumped up to $21.34 billion in 2021. However, this metric ultimately declined to $20.61 billion in 2022 before dipping further to $20.15 billion in the first quarter of 2023.

It's unclear how much of the recent decline was driven by concerns over the banking sector. More likely than not, much of the pain the company has seen on this front has been driven more by the act of consumers responding to higher interest rates by allocating capital toward more attractive investment opportunities.

{kind=link}

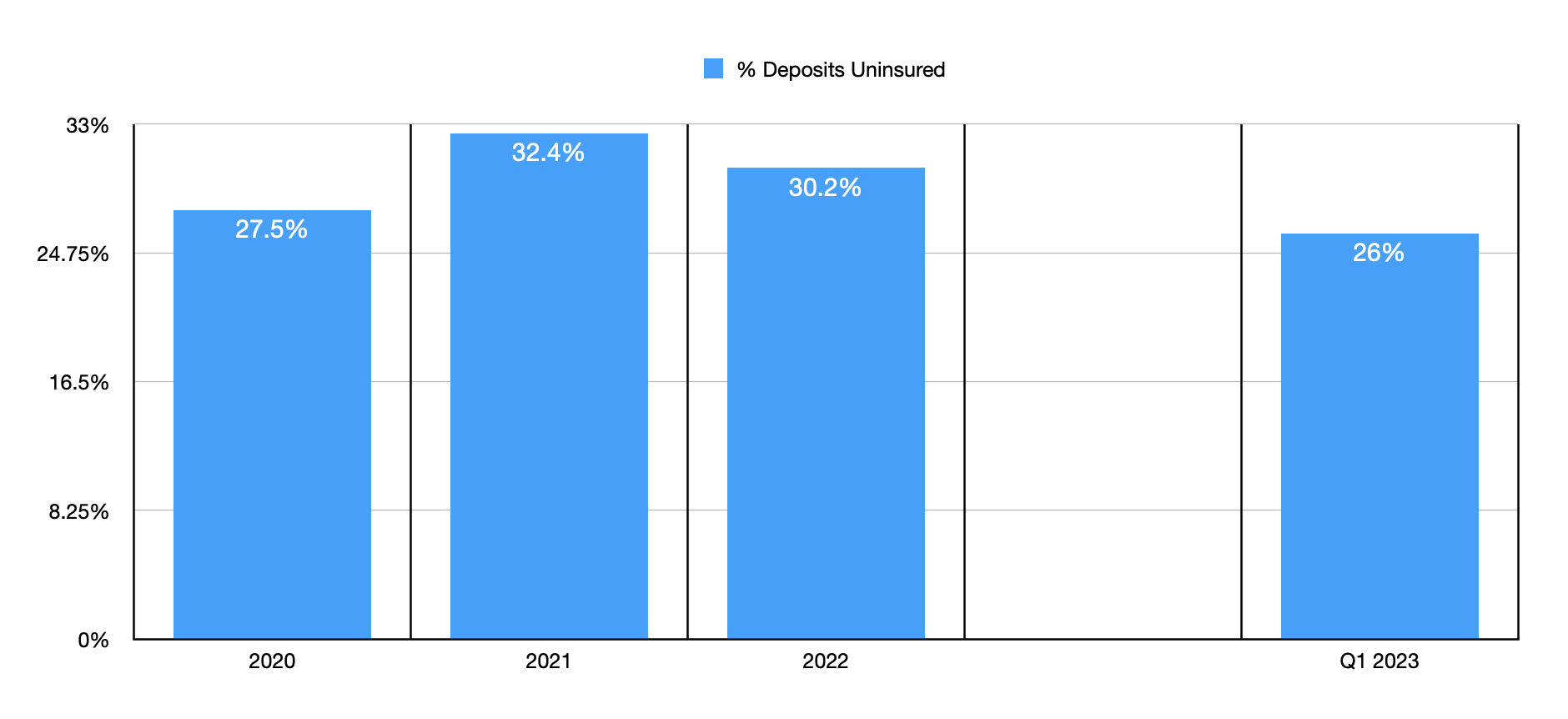

Compared to the banks that experienced a collapse or a near collapse, Glacier Bancorp seems quite stable. At the end of 2022, for instance, 30.2% of the company's deposit base was uninsured. This number did decline to 26% in the first quarter of 2023 . That translates to a decline of less than $1 billion over the course of a single quarter. And it probably is the best approximation of what the banking concerns have done to the firm. In the event that the company were to see some exodus of deposits, it's worth noting that the enterprise has a great deal of liquidity at its disposal. This includes $10.5 billion that it can tap into immediately in the form of available borrowing capacity that it can tap into, unpledged marketable securities on its books, and cash of about $1.5 billion. This is almost double the $5.3 billion that uninsured deposits currently come out to. The company could also access another $4.6 billion worth of liquidity in the form of brokered deposits, over pledged marketable securities, and loans that are eligible for pledging, if it so desired or needed.

{kind=link}

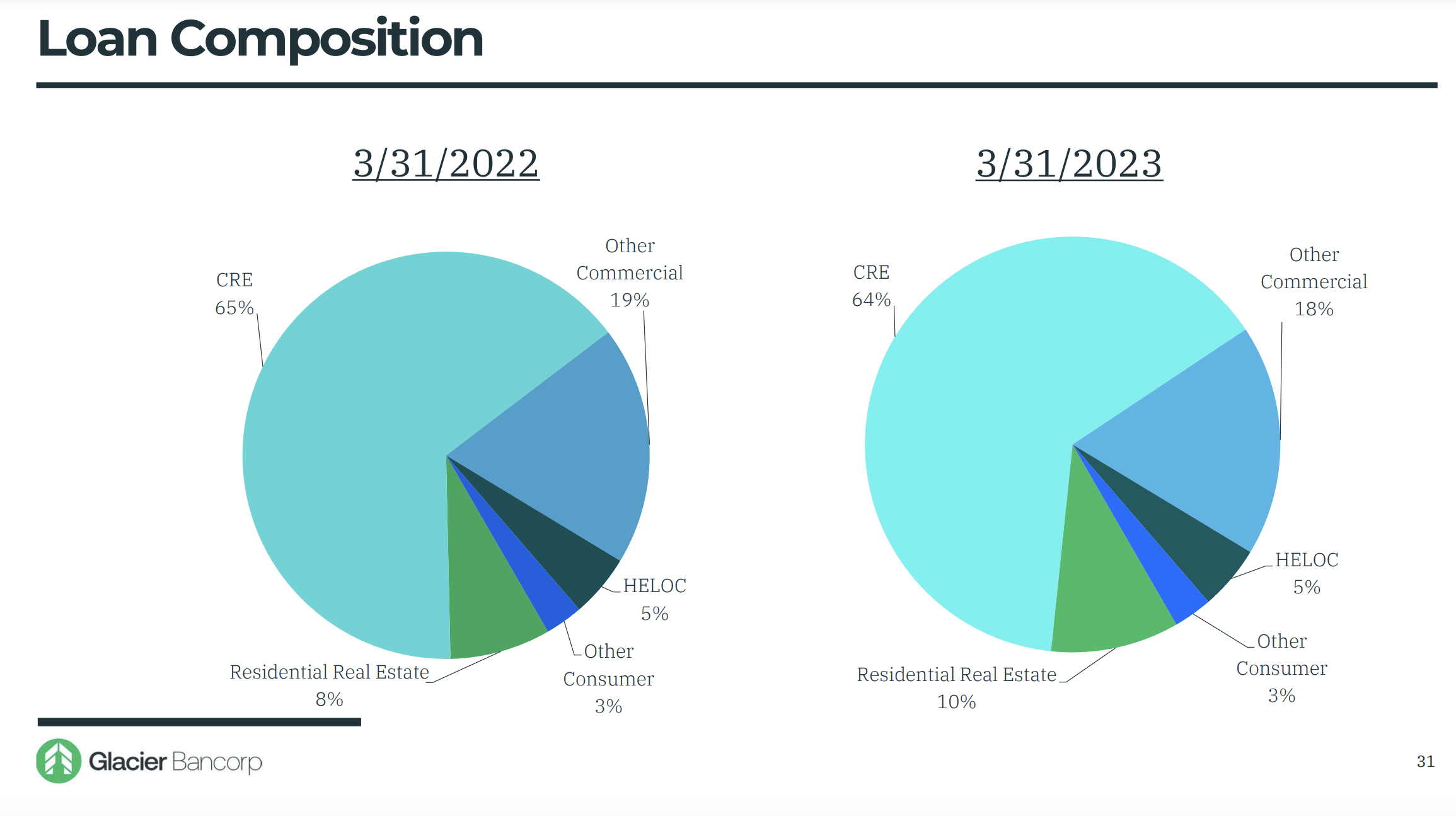

Even though deposits have been volatile, the company has done very well to grow the value of its loans. Total loans that it has on its books as part of its investment portfolio have grown from $10.96 billion in 2020 to $15.06 billion last year. In the first quarter of this year, loans came in at $15.33 billion. As of the end of the most recent quarter, 64% of its loans by value were in the form of commercial real estate. This comes out to roughly $9.8 billion.

I understand that a lot of investors are currently worried about the office category of commercial real estate. I am also concerned about that. However, this is an area of small exposure for the company. Only about $1.5 billion of its overall loan portfolio is in the form of commercial real estate. And of that, 50.3% is owner-occupied.

{kind=link}

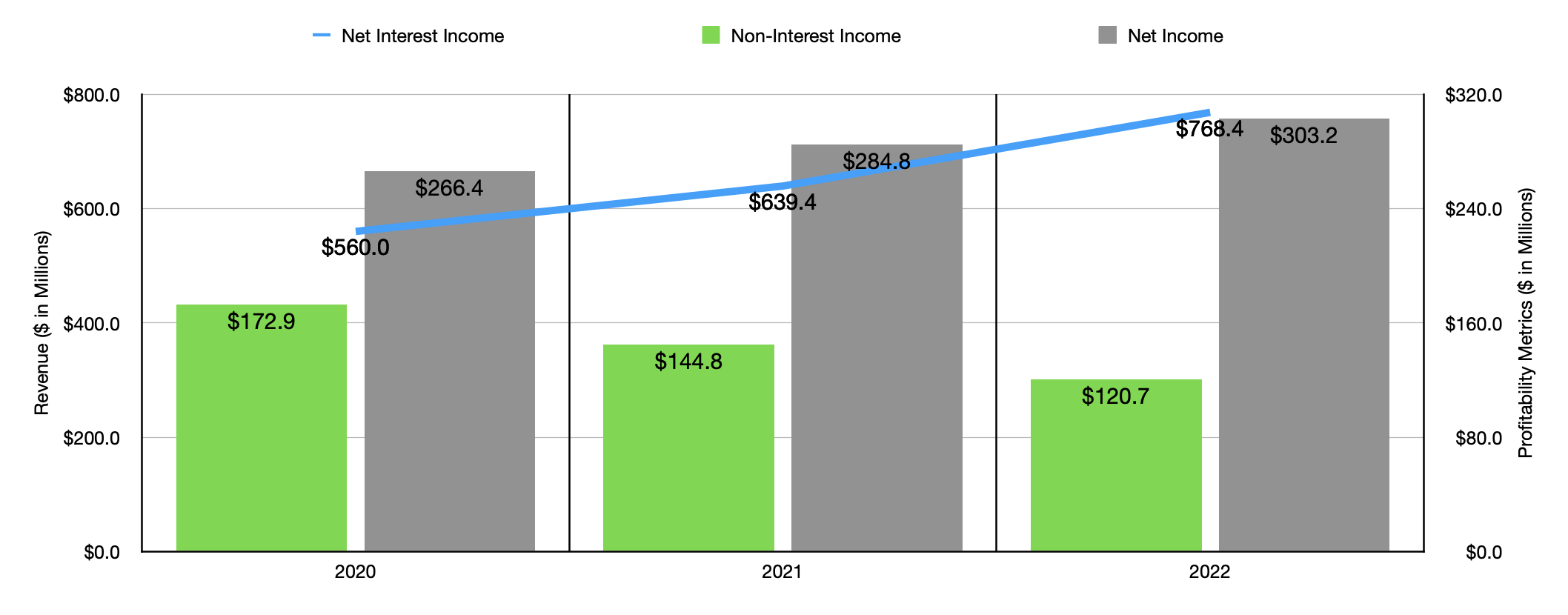

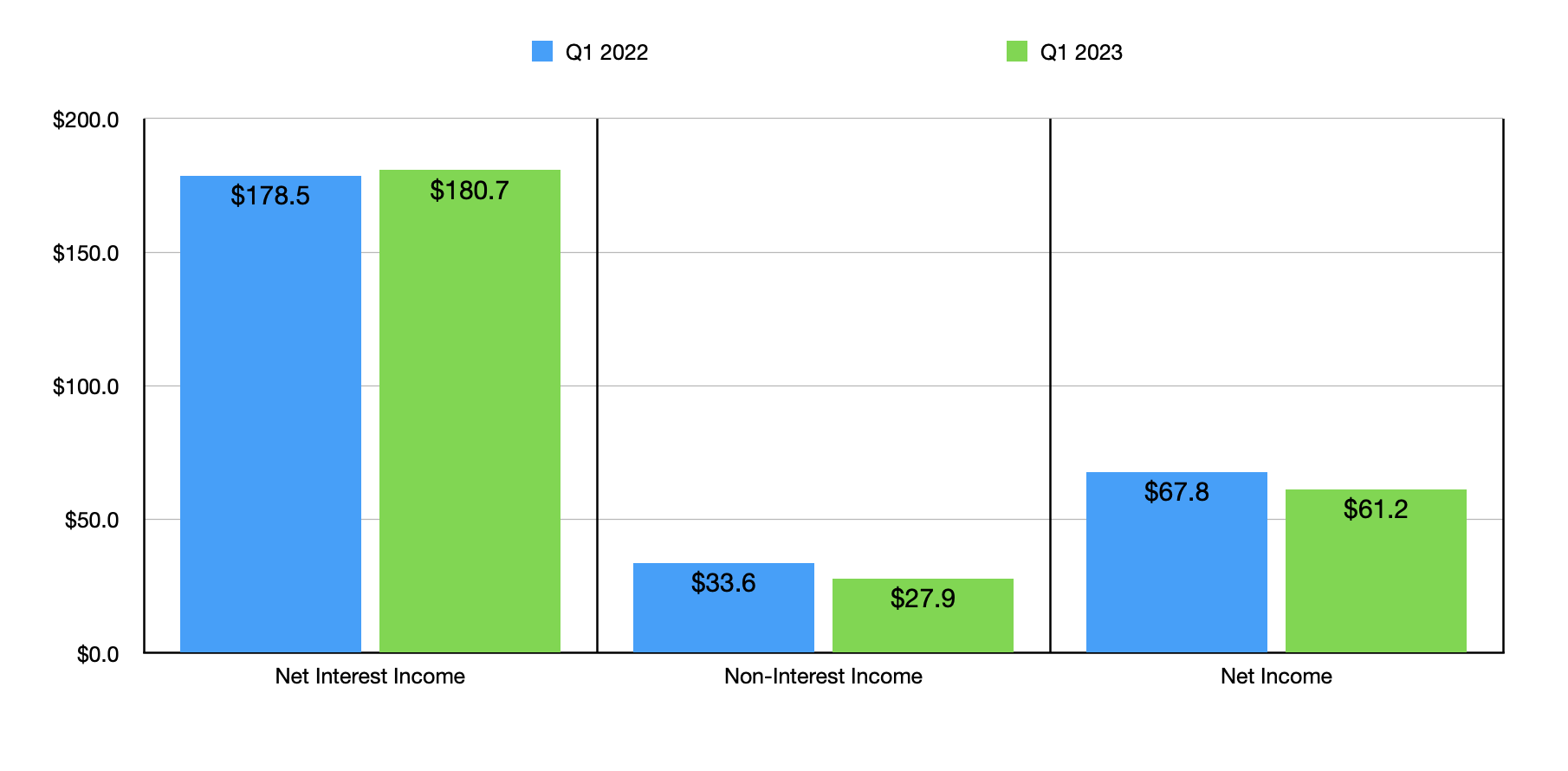

This is great to see. Part of the reason why is because, when coupled with rising interest rates, the increase in loans has allowed the company to grow from a revenue and profit perspective. Net interest income expanded from $560 million in 2020 to $768.4 million in 2022. In the first quarter of this year, net interest income of $180.7 million was slightly higher than the $178.5 million reported the same time last year.

This is not to say that everything has been great for the company from an income statement perspective. Over the same window of time, non-interest income for the company declined. In 2020, it came in at $172.9 million. By 2022, it had dropped to $120.7 million. In the first quarter of this year, it totaled $27.9 million. This is down from the $33.6 million reported for the same quarter last year.

{kind=link}

There are multiple working parts behind this decline in non-interest income. For instance, the company suffered from a $43 million decline associated with the gain on the sale of certain loans from 2021 to 2022. This was somewhat offset, however, by a $12.8 million increase in service charges and other fees, largely thanks to increases in credit card interchange fees because of higher activity and because of an acquisition the company made. Even though the company experienced a decline in income under this category, total net income for the business expanded from $266.4 million in 2020 to $303.2 million in 2022. For the first quarter of 2023, net income did drop slightly compared to what it was the year prior, declining from $67.8 million to $61.2 million. But in the grand scheme of things, that's likely a blip on the radar.

{kind=link}

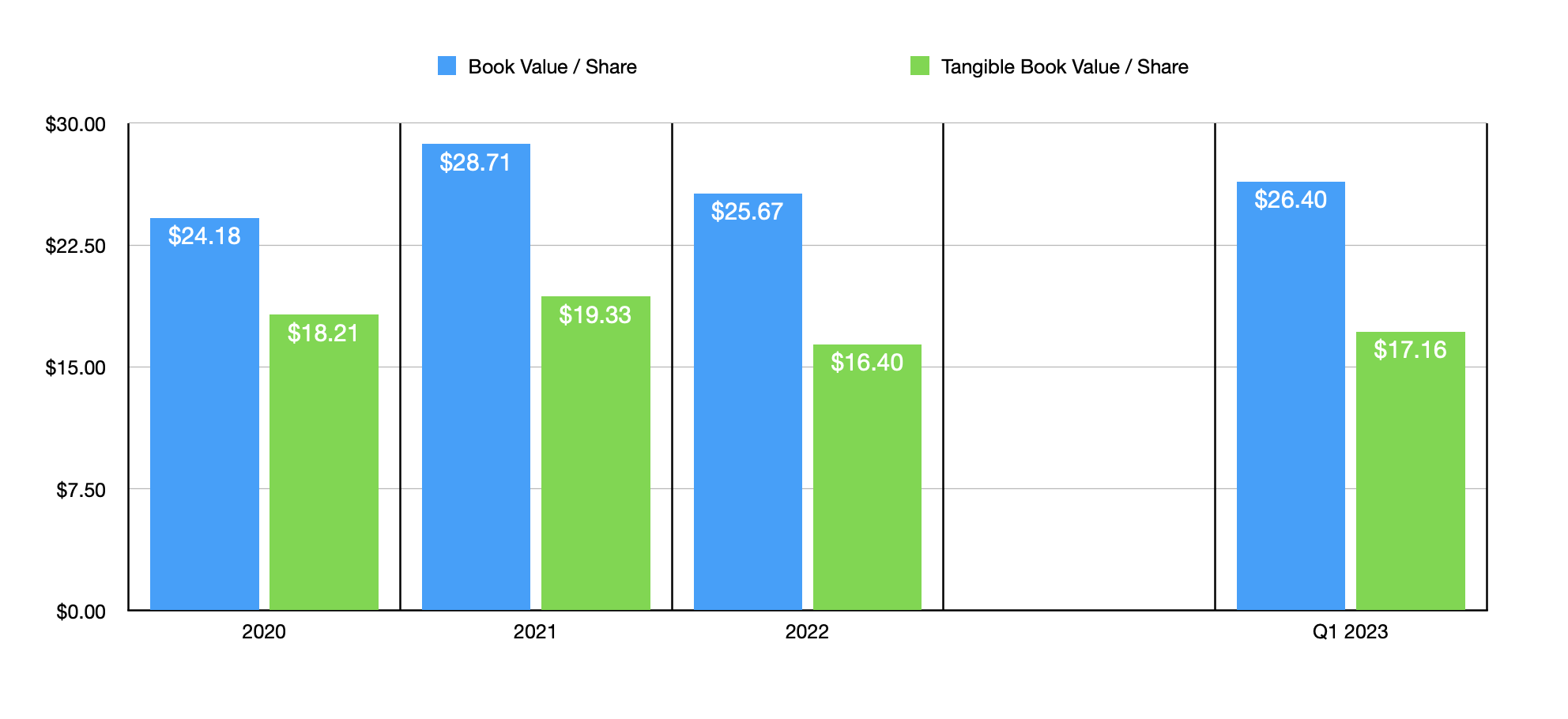

The last thing I would like to touch on is the company's book value. Since peaking at $28.71 per share in 2021, the metric has fallen some. At the end of the most recent quarter, it totaled $26.40. Although it is a negative to see this decline, the most recent quarterly data does represent an increase over the $25.67 that the company reported at the end of last year. Tangible book value per share has followed a similar trajectory. For those wondering, the overall decline that the company saw from 2021 to 2022 was driven by a $502.6 million hit associated with available for sale securities and transferred debt securities. Such a drop is common, especially in a rapidly changing market.

{kind=link}

Takeaway

Operationally speaking, Glacier Bancorp is doing pretty good. Its bottom line continues to expand, even though the most recent quarter was a bit on the weak side. The company has a deposit base that should insulate it from a bank run. And even if it does experience a bank run, it has ample liquidity to cover uninsured deposits and it has total debt of only $3.28 billion. This means that the company would be very likely to survive any real deposit withdrawals.

We have seen some volatility, such as when it comes to book value per share and deposits. The non-interest income decline is also less than ideal. In terms of overall upside, the company probably does offer some. Its price to earnings ratio, for instance, is about 12.8 as of this writing. This is lower than the 16 reading that we get when we look at most of the companies in the space.

Putting all of this together, Glacier Bancorp, Inc. does seem to be a decent "buy" candidate at this time. But I also do believe that there are better prospects in the market today.

For further details see:

Glacier Bancorp Deserves Some Upside