GBCI - Glacier Bancorp: Potential Upside Not Worth The Risk

2023-06-20 13:00:00 ET

Summary

- Glacier Bancorp has a competitive advantage with its low-cost deposits, but this doesn't translate to a high net interest margin due to low-interest loans.

- The bank's fair value is estimated at $45.84 per share, making it appear undervalued, but the potential upside may not be worth the risk.

- Glacier Bancorp is a hold for now, but if it retests historical support levels, it may be considered for a buy.

Glacier Bancorp, Inc. ( GBCI ) operates as the bank holding company for Glacier Bank; it was founded back in 1955 and is headquartered in Kalispell, Montana.

Over the past month I have been analyzing many regional banks, but of all of them I have rarely been able to find a bank similar to this one on the deposit cost aspect, which is why it will be the main theme of this article. It is as if the sharply rising Fed Funds Rate has not had a significant impact on its balance sheet.

Anyway, despite this positive aspect, my rating for Glacier Bancorp is simply a hold, since as we shall see its fair value does not present a high enough margin of safety.

Analysis of the big picture

As anticipated, Glacier Bancorp's cost of deposits is out of the ordinary because it is as if it does not keep pace with increases in the Fed Funds Rate.

{kind=link}

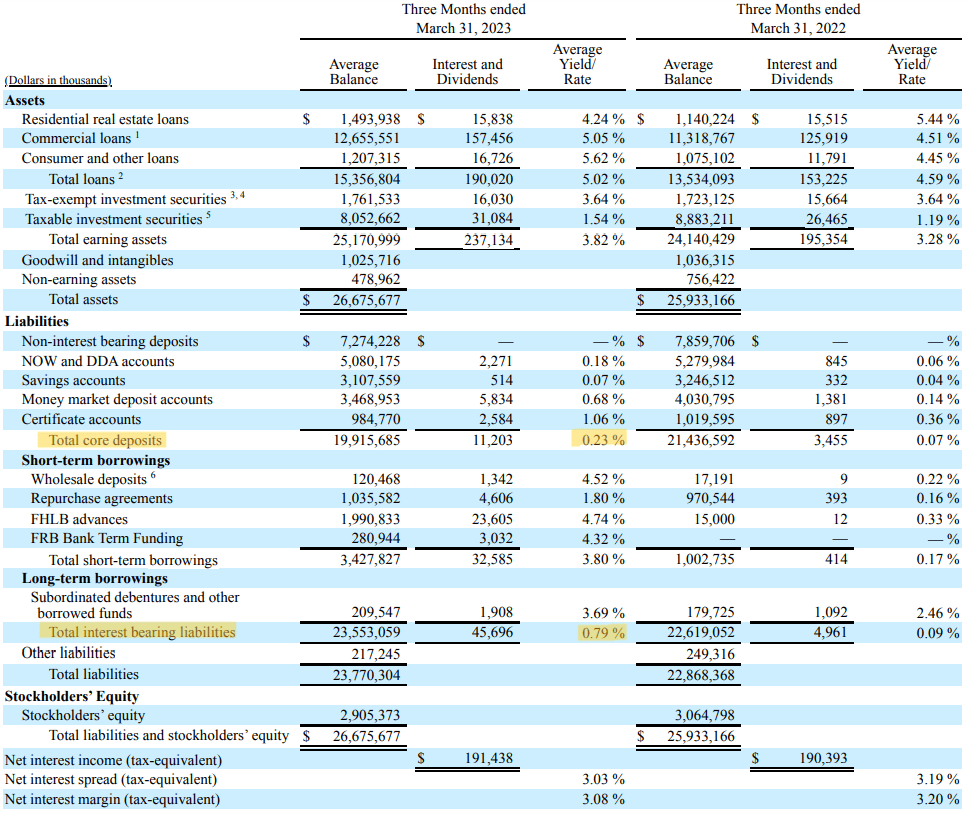

The average rate of total core deposits in Q1 2023 was only 0.23%, 16 basis points higher than last year. As a result, total interest-bearing liabilities also have a very low cost, only 0.79%.

{kind=link}

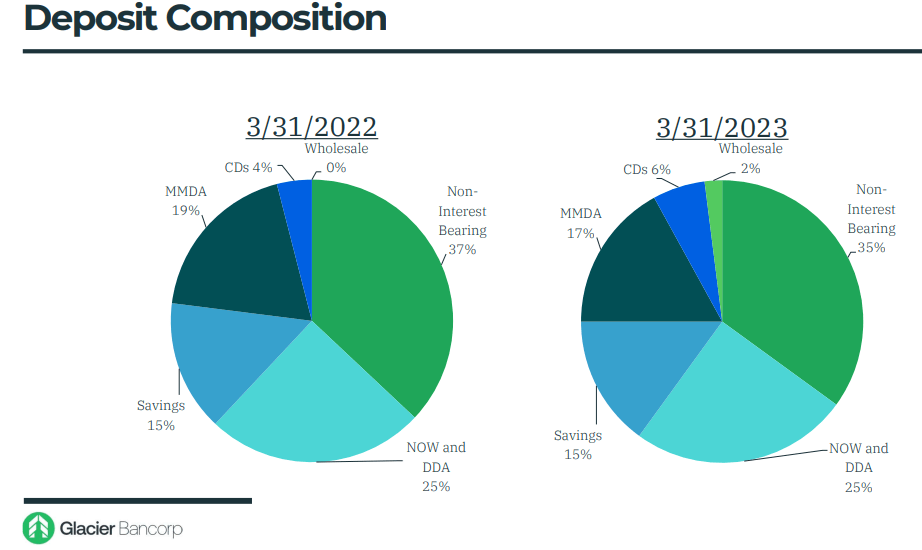

Aiding this has been the resilience of non-interest bearing deposits, which have been reduced in percentage terms by only 2% since last year: basically more than a third of deposits cost nothing.

While other banks have been forced to replace non-interest bearing deposits with much more expensive sources of funding, for Glacier Bancorp the situation is quite different. In my view, the granularity of its deposits has made all the difference.

In fact, according to the company's data, its average retail customer has $14,000 in the account, is a loyal 15-year customer belonging to rural markets. For average business customers only the amount in the bank account changes, averaging $63,000. In short, we are talking about habitual customers who probably care relatively little about the interest rate they receive since they do not own figures of a certain importance. As long as customers are comfortable with the services offered by Glacier Bancorp, I think it is unlikely that they would prefer to receive 1-2% more - of $14,000 - at another bank. Of course, there are exceptions; this is a generalization to make the point.

{kind=link}

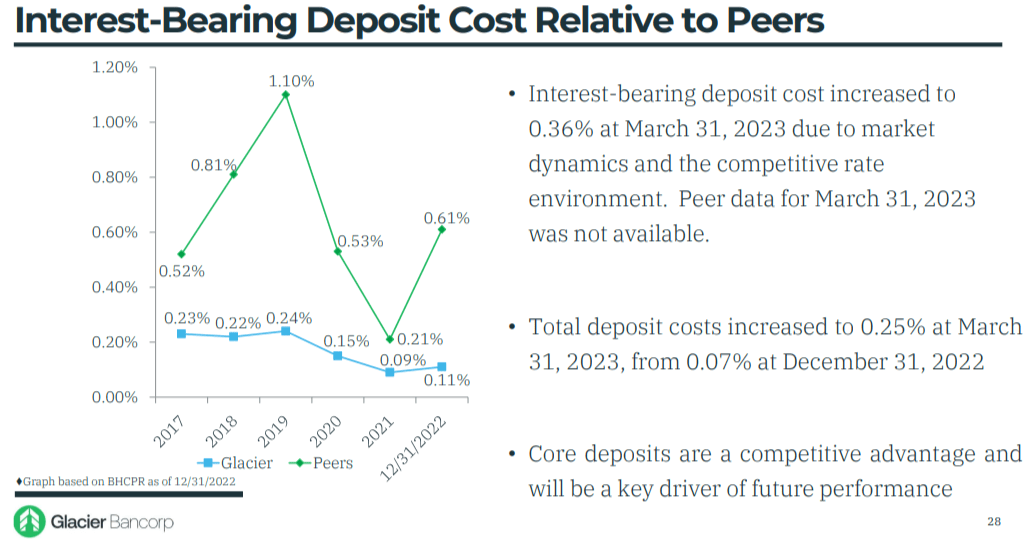

According to this image published by the company, it is evident how peers have already lost control over the cost of deposits. It was 50 basis points higher at the end of 2022, and this gap has probably widened. This comparison is out of date, but since the average rate for the month of March was 36 basis points, I doubt the peers did any better. Over the past month, I have analyzed the deposits of various banks, and they hardly cost less than 1-1.50%. In some cases I even found rates around 3%.

Having ascertained that Glacier Bancorp is well ahead on deposits, it is now important to understand how long this asymmetry will last.

Historically, this bank has almost always paid very little for its deposits, and according to management it is likely that this trend may continue, but there are issues to consider. The first concerns depositor memory, a concept discussed by CEO Randy Chesler during the conference call:

I guess just to step back and some context, we went through a decade of zero to low rates, and so there was a little muscle memory that had to be developed in terms of competing for deposits. And I think that's what we saw in the fourth quarter and to some extent in January to Byron's commentary once we said enough within a week the deposit stabilized and then actually grew.

So I think Brandon is as simple as that. We had been in a mode for a decade of and operating in one environment. It shifted pretty quickly and I think we're squarely now out to retain and defend the deposits and keep them with our relationships.

In short, after a decade of expansionary monetary policy with rates close to 0%, people became accustomed to expecting irrelevant rates from the money market. As a result, this favored bank funding, which was significantly cheaper. As of today, however, this is no longer the case, and a T-bill yields more than 5%. Customers are gradually realizing this, and over time are becoming aware that the decade when interest on deposits mattered little is now a distant memory. The more customers become aware, the more problematic it becomes to be able to keep non-interest bearing deposits high.

In any case, I would not bet on Glacier Bancorp's cost of deposits being excessively high in the future. As explained earlier, granularity is its strength, and its average customer probably cares little about earning a few hundred dollars more with another bank.

The second aspect to consider regarding the future cost of deposits concerns the level of the Fed Funds Rate in the future.

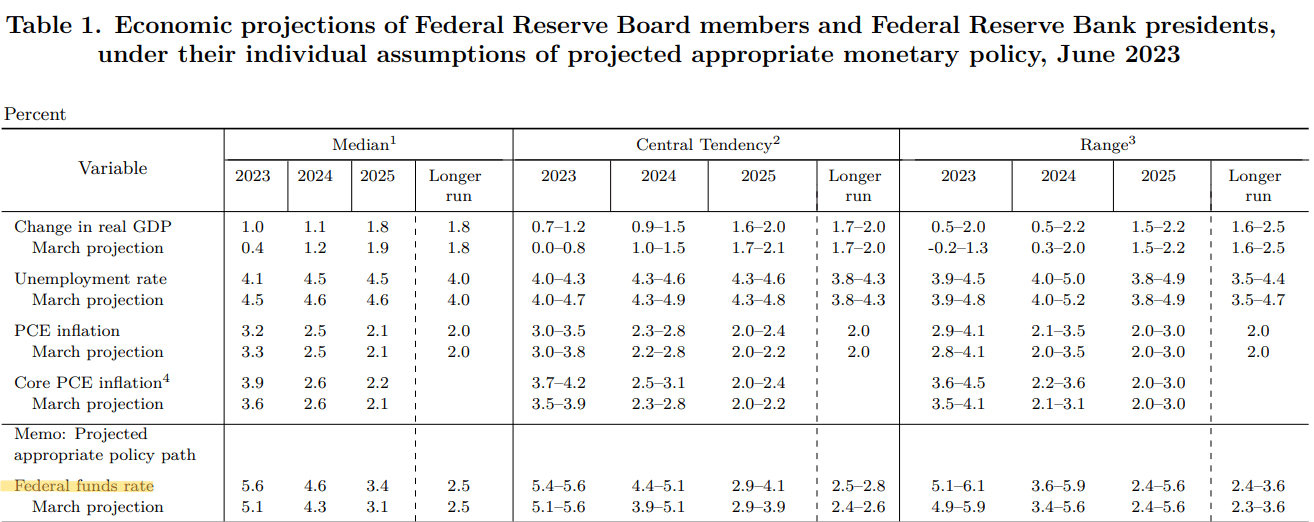

Economic projections of Federal Reserve Board members and Federal Reserve Bank presidents

{kind=link}

At the last meeting , it was decided to keep the level of interest rates stable; however, Fed Funds Rate expectations for 2023 as a whole imply at least 2 more 25 basis point increases. In addition, 2024 is expected to be another year with high interest rates. In short, tight monetary policy will last much longer.

All this puts pressure on the money market, which is forced to grant higher interest rates. Consequently, this leverages the yield offered by deposits: it will necessarily have to adjust to the macroeconomic environment.

The speed with which deposits adjust to new interest rates is called deposit beta, and in the case of Glacier Bancorp it is 15%, which is quite low. However, considering the Fed Funds Rate expected in 2023, the deposit beta may increase in the coming months and Glacier Bancorp will see the cost of its deposits rise. According to CEO Randy Chesler , this scenario is not unlikely:

We're still using 15% through the cycle beta for total deposits. We still think that's a good estimate. It really depends on the Federal Reserve and kind of what rates, what happens from here if we see higher for longer, that is a scenario, where I think clearly we'll have to push through that 15% beta to retain deposit balances. If you believe market expectations and the Fed begins to cut towards the back half of this year, that's a scenario where I think we could maintain and hold to that 15% beta number. So it really depends on what the Fed does from here.

In short, it is all in the hands of the Fed, but in my opinion the situation cannot change that much. In Q1 2023 the cost of deposits was only 0.25% with a Fed Funds Rate at 5%, while peers were already offering a rate 2,3,4 times higher. It is fair to expect a higher deposit beta in the coming months, but I think it is unlikely that the situation will be totally turned around.

Finally, to conclude the big picture, I would like to talk about profitability. Since the cost of deposits is extremely low we might expect the net interest margin to be Glacier Bancorp's strong point, but it is not.

Glacier Bancorp Q1 2023

It has been declining since 2020, while net interest income has been declining since 2022. There are two reasons why this has happened:

The first is related to the decision to keep liquidity high for precautionary reasons. The recent banking crisis was of no small concern, so as a result liquidity was held rather than invested.

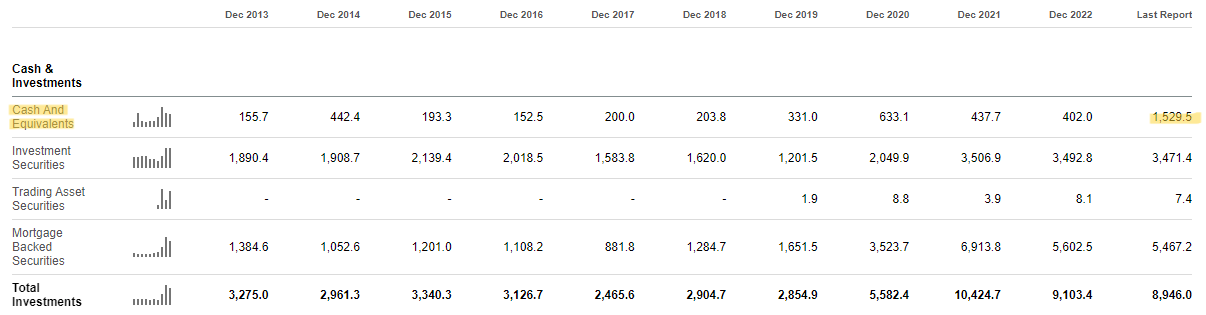

{kind=link}

In the last report it amounted to $1.52 billion, definitely above the figures of previous years. Holding such a large amount of cash carries a not insignificant opportunity cost. In addition, the current loan to deposit ratio is only 77.10%.

The second reason why the net interest income/margin is struggling despite the low cost of deposits is that the return on assets has not adjusted sufficiently as interest rates have risen.

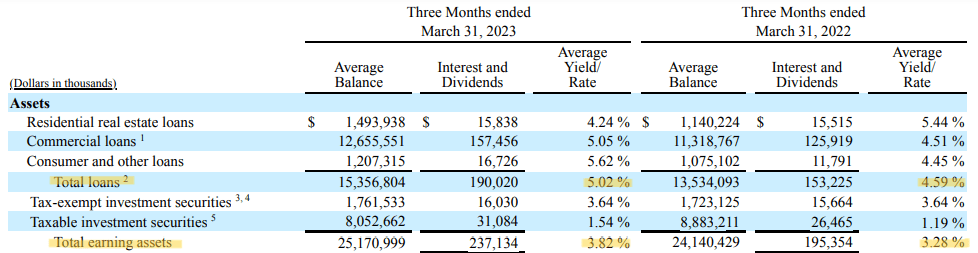

{kind=link}

In fact, in one year total earning assets increased by only 54 basis points. In particular, total loans achieved an even smaller improvement: only 43 basis points.

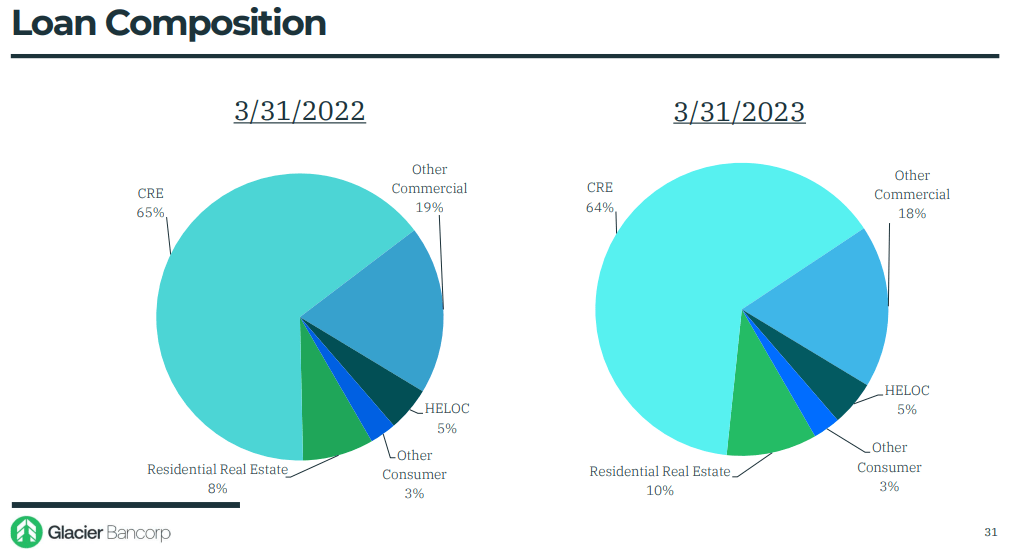

{kind=link}

64% of loans belong to the CRE category, which is generally considered risky because it is more volatile to business cycle trends. However, the average LTV is only 59%, which significantly reduces the riskiness. Therefore, in my opinion Glacier Bancorp could not increase the yield of its assets significantly: after all, little risk little return.

Overall, Glacier Bancorp has an important competitive advantage on deposits, however, their low cost does not allow for a high net interest margin because the loans it makes have relatively low interest rates. An overly risky portfolio is preferred to be avoided, just as liquidity is currently preferred to new loans.

Valuation

The valuation of Glacier Bancorp will be conducted through three methods, analyzing book value, earnings, and dividends.

- The average Price / Book ((TTM)) from 2010 to date has been 1.85x; multiplying this by the current Book Value per share of $26.40, the fair value amounts to $48.84 per share, much more than the current price.

- The average P/E since 2010 has been 22.51x; multiplying this figure by Seeking Alpha analysts' estimated EPS for 2023, $2.13, the fair value amounts to $47.94.

- The final method to understand what Glacier Bancorp is worth is to use a dividend discount model. The model inputs will be as follows:

- Annual Payout ((FWD)) of $1.32 per share

- Growth Rate of 8%, down from the average of the last 10 years. I expect that in the coming years the dividend will not be as easily increased as in the past.

- RRR of 12% as this is a rather risky investment.

The result is that the fair value of Glacier Bancorp is $35.64 per share.

Applying a weighted average where the first two are worth 40% and the last method is worth 20%, the total fair value amounts to $45.84 per share, so Glacier Bancorp seems undervalued.

Conclusion

Glacier Bancorp is a bank with quality and not expensive deposits but due to low yields on assets it has failed to increase net income margin over the past few years. There will probably be a deterioration again this year, as a net interest margin between 2.95% and 3% is expected. Weighing on this guidance are excess liquidity as a precautionary measure and low LTV.

As for valuation, on paper Glacier Bancorp looks undervalued; however, I do not think there is a sufficient margin of safety to buy it. After all, we are talking about a bank with only $27 billion in assets and capitalizing $3.80 billion. In short, investing in it means being willing to bear a rather high risk dictated by the little impact this bank has in the financial markets.

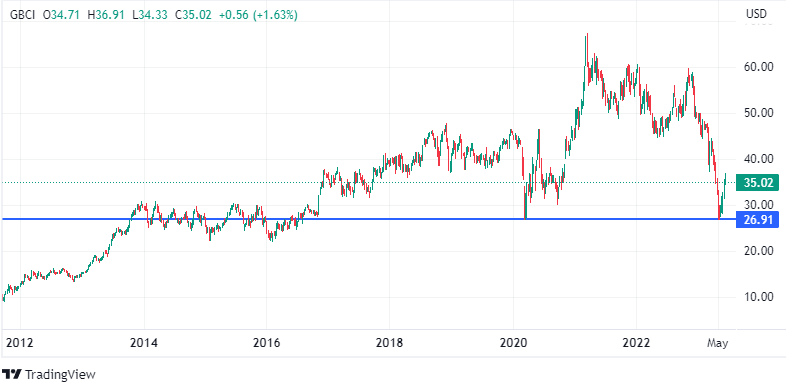

{kind=link}

When support was touched last month at about $27 per share, that was probably a good time to buy with a decent margin of safety. That support has been touched several times, including during the pandemic. Today at $35 per share it is still undervalued, but the potential upside may not be worth it for the risk taken. Should it retest that historical support I might consider a buy, but for now it is only on my watchlist.

For further details see:

Glacier Bancorp: Potential Upside Not Worth The Risk