LAND - Gladstone Land Has Become Interesting Again

Summary

- LAND owns farmland real estate across the United States, but especially concentrated on the West Coast and Florida.

- In a recent business update, management revealed that Hurricane Ian did the most damage to its farms in Florida.

- The Western drought poses a continuous threat to farmland in the region, but LAND's farms do have water access plus a company-owned water bank.

- LAND's main problem is its higher cost of capital, especially for preferred equity, which it keeps issuing more of for some reason.

Thesis: Not Quite "Dirt" Cheap, But Close

Gladstone Land ( LAND ) owns farmland as a real estate investment. In other words, LAND has tenant-farmers actually growing the crops and managing the operations of the farm while they pay rent to LAND, just like any other kind of real estate tenant.

As such, LAND provides an interesting way for stock investors to gain exposure to the asset class of farmland, which is normally restricted to the ultra-wealthy or at least accredited investors.

LAND also pays a 3% dividend yield with a monthly payout schedule, making it an interesting inflation-hedge option to consider for income-oriented investors.

At a price of $18.10, LAND still trades at a 16% premium to its NAV per share of $15.60 as of Q2 2022. While that doesn't sound cheap, it is a lot lower than the 167% premium to NAV the REIT had at its peak price in April!

On a cash flow basis, you'd have to go back to early 2021, before inflation took off, to find LAND as cheap as it is today.

I wouldn't quite say that LAND is "dirt" cheap (see what I did there?), but it's a heck of a lot cheaper than it has been anytime in the last year, and it makes an interesting inflation hedge.

There are some issues with the company, namely the external management's insistence upon using preferred equity that comes with a high cost rather than some cheaper source of funding. I'd like to see LAND's cost of capital come down substantially before I become gung-ho about the stock, but I still think the selloff has made LAND interesting as a dividend-yielding inflation hedge once again.

Update On Gladstone Land

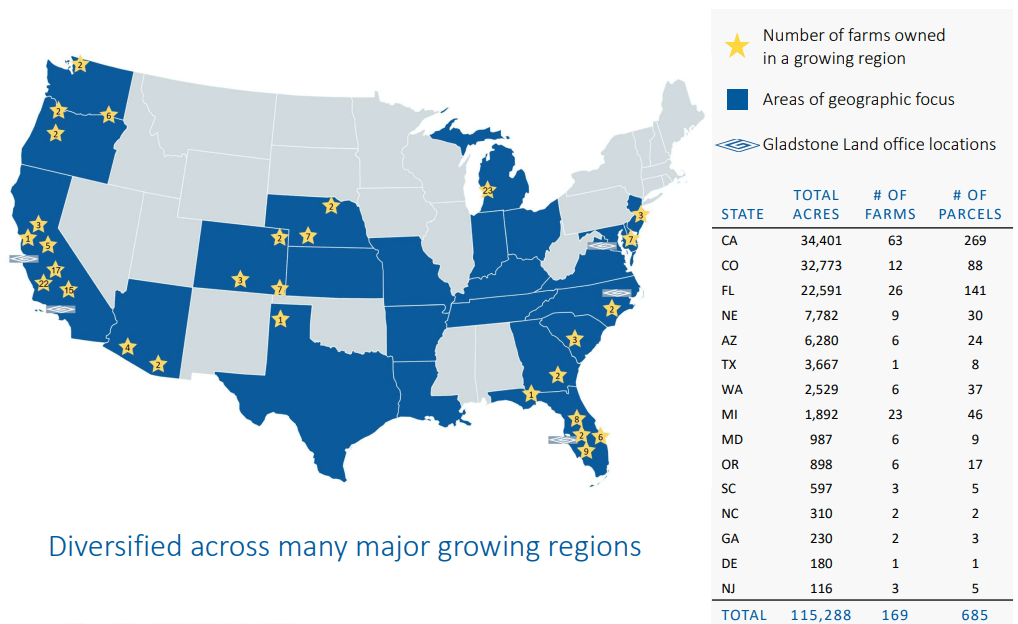

As of the middle of 2022, LAND owned 169 farms totaling 114,000 acres along with 45,000 acre-feet (about 14.6 million gallons) of banked water on the West Coast. Rather than row crops like wheat, corn, and soy, these farms mostly grow higher yielding (in the ROI sense) fruits, berries, vegetables, and nuts.

{kind=link}

There are lots of things I like about LAND. Here are some of the highlights:

- Triple Net Leases. In addition to rent, tenants are responsible for paying all property taxes, insurance, and maintenance expenses. This insulates the landlord (and LAND shareholder) from rising operating costs, such as fertilizer or gasoline.

- Steady Farmland Appreciation. Farmland has a strong track record of steadily appreciating in value over time. LAND's management asserts that over the last year, its preferred property type has seen about 20% appreciation in value.

- Internal Rent Growth. Virtually all of LAND's leases feature some form of embedded rent growth or excess revenue participation. In Q2, fixed base rent grew 2%, and recent lease renewals have featured rent growth of nearly 10%. Participation (or percentage) rents are expected to be up substantially this year.

- Large Investable Universe. LAND estimates that there's about $48 billion worth of top-tier farms growing short-lived row crops and permanent crops across about 9,625 farms. Compare that to LAND's 169 farms worth about $1.5 billion.

- Healthy Diet Trend. A subset of consumers has become increasingly interested in eating healthier, cleaner, less processed diets. That includes organic foods, which represent about a third of LAND's farmed produce.

- Renewable Energy Leasing Potential. On the Q2 conference call, CEO David Gladstone mentioned that they are constantly "bombarded" with letters and phone calls asking to use their land for wind or solar installments. While LAND wants to ensure the tenant-farmer's operations are not disrupted, this could present some opportunities to further juice the cash yields on LAND's properties.

- Aligned Interests. Management owns a little over 9% of LAND common stock, which mostly aligns their interests with those of shareholders.

In an October 6th business update , LAND provided the following points of information about the company:

- Farmland is acting as a strong inflation hedge right now. Through August 2022, the CPI increase 8.3%, but food prices rose 11.4% during that time while "food at home" (which is more pertinent to LAND's crops) rose 13.5%. Meanwhile, US farmland booked total returns of 9.7% for the twelve months ending in June 2022.

- LAND's portfolio is 100% leased and occupied, and the REIT has collected 97.7% of rents due so far this year, with the full remainder expected to be collected by year-end.

- During the third quarter, LAND signed lease renewals for six properties in Arizona, California, and Florida at a leasing spread of 9.8% (above the prior rent rate).

- LAND has $642.7 million in debt, virtually all of which has fixed-rate interest payments at a weighted average rate of 3.26%. This rate, says management, is fixed for the next 5.1 years, thereby sheltering the REIT from the ravages of rapidly rising interest rates.

- LAND has lots of liquidity and financial flexibility: $45 million in cash, ~$127 million available on the credit facility, and ~$105 million of unencumbered properties available to be mortgaged for an additional cash infusion, if desired.

- LAND's Florida farms suffered minimal damage from Hurricane Ian. The REIT does not expect to have any delays in rent payments from its Floridian tenants. Notably, the company's two permanent crop farms in the state, both citrus groves, both survived the storm with very little damage to the trees.

- The Western drought continues to be a problem for Californian farms. Though it hasn't caused any impairment to LAND's properties yet, the broader issue persists and could lead to problems next year if there isn't a good snowpack and rainy season. While land without water access is falling in value, land with water access is rising in value. LAND has been vigilant in buying properties with water sources as well as securing 45,000 acre-feet of banked water in the state last year. They're looking for ways to secure more water for their farms.

At the end of the business update, CEO David Gladstone finished by saying:

Outside of the almond market, most crops grown on our properties are seeing strong demand and increasing prices that are mostly outpacing the cost increases of growing these crops. As the probability of a recession looks more likely, we expect demand for food and crop pricing to stay strong, with some sectors experiencing exceptionally strong increases. As an overall asset class, farmland investments have historically performed well during recessions.

Nearly everyone expects a recession to manifest in the coming year, if it isn't here already, which makes Gladstone's comments interesting. Unlike most other income-generating assets (excluding government bonds), he asserts that farmland actually tends to perform well during recessions. That makes sense, since people still need to eat, even if they've lost their job or have to rein in other spending.

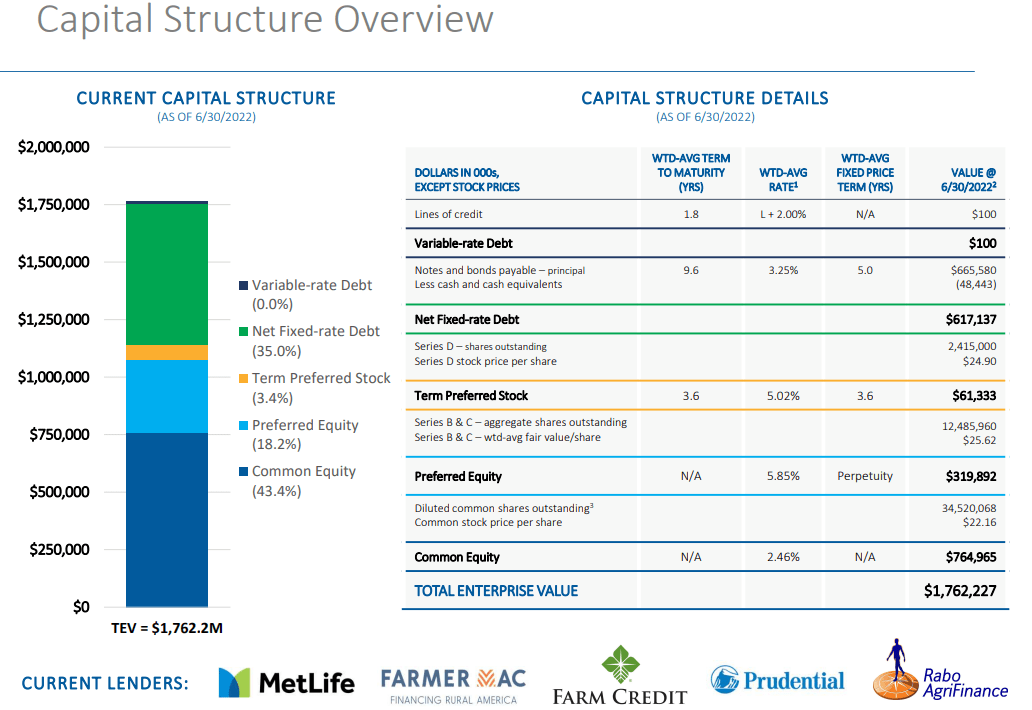

The Biggest Drawback

The biggest issue for LAND is that its cost of capital is simply too high relative to the initial cash cap rates for permanent crop farms of 5.5-6%. Here's the REIT's capital structure as of Q2 2022:

{kind=link}

As Gladstone admitted in his prepared comments on the Q2 2022 conference call :

In the meantime, we're looking for ways to adjust our overall cost of capital to better match the changes that we're seeing in the farmland acquisition market. Our issues is that our preferred stock and our borrowings have both become expensive for current farmland prices and rents.

So, Gladstone sees that LAND's cost of capital is too high and said during the last conference call that he'd like to lower it. But then what does LAND do? They go and issue up to $255 million in their new 6%-yielding Series C preferred equity (formerly up to $500 million).

This is exactly the same yield as the initial cash yields generated from LAND's Q2-Q3 farm acquisitions. As such, unless other sources of capital are included, the investments made from this preferred equity capital won't immediately be accretive to per-share AFFO growth.

Now, over time, they will add to AFFO growth, because embedded rent escalations in the leases should increase the effective yield on invested capital over time. But I never like to see investments that provide zero boost to the bottom line right away.

I'm grateful management halved their originally intended amount of Series C issuance, but I also concur with Gladstone that LAND needs to focus on lowering its cost of capital going forward.

The good news is that, just prior to the recent spike in interest rates, LAND secured a $5 million loan with an effective interest rate of 2.89% that is fixed for five years. Moreover, the weighted average maturity on all debt is about 9.5 years, with nearly 3/4ths of all debt maturing after 2026.

Unfortunately, though, even inclusive of this loan, LAND's loan-to-fair value ratio is about 44%. On its own, a lower LTV is generally a good thing. But in LAND's case, it means that a greater percentage of its capitalization comes from higher-cost preferred stock.

Bottom Line

The REIT currently pays an annualized dividend of $0.5472 per share (on a monthly payout schedule), which equates to a payout ratio of about 84% based on annualized 1H 2022 AFFO per share of $0.65.

For some reason, in their presentations, management continues to tout their intent to raise dividends at a rate that outpaces inflation, despite having failed to do that for the last five years in a row. But LAND does provide some dividend raises, albeit meager ones. Perhaps if management is successful at (eventually) lowering their cost of capital, they will be able to grow externally faster and thereby increase their dividend at a rate commensurate to inflation.

That hope surely must play a part in any long-term investment thesis for LAND.

As for me, I am tempted to buy back into LAND now that it has reached a 3% dividend yield again. I like the idea of having exposure to farmland. But LAND's cost of capital issue is unattractive, and management seems intent on continuously using high cost preferreds, for some reason.

I will wait to hear management's commentary on Q3 results before deciding whether to buy LAND.

For further details see:

Gladstone Land Has Become Interesting Again