LANDP - Gladstone Land Series C Preferreds: 7.8% Yield From Farmlands

2023-09-12 11:10:15 ET

Summary

- Gladstone Land Corporation is a REIT specializing in acquiring and owning farmland in the US.

- Farmland has historically delivered strong long-term returns and Gladstone has enjoyed consistent rental growth.

- The Series C preferred shares of Gladstone Land could be an interesting investment opportunity, currently yielding 7.8%.

A few months ago, I wrote a bullish article on Gladstone Land Corporation (LAND), an agricultural-focused REIT. Farmland had historically protected investors against inflation and LAND had fallen to a discount to NAV.

This article looks at a related investment in preferred shares issued by Gladstone Land, specifically, the Gladstone Land Corporation 6% Series C Cumulative Preferred Shares (LANDP).

Brief Company Overview

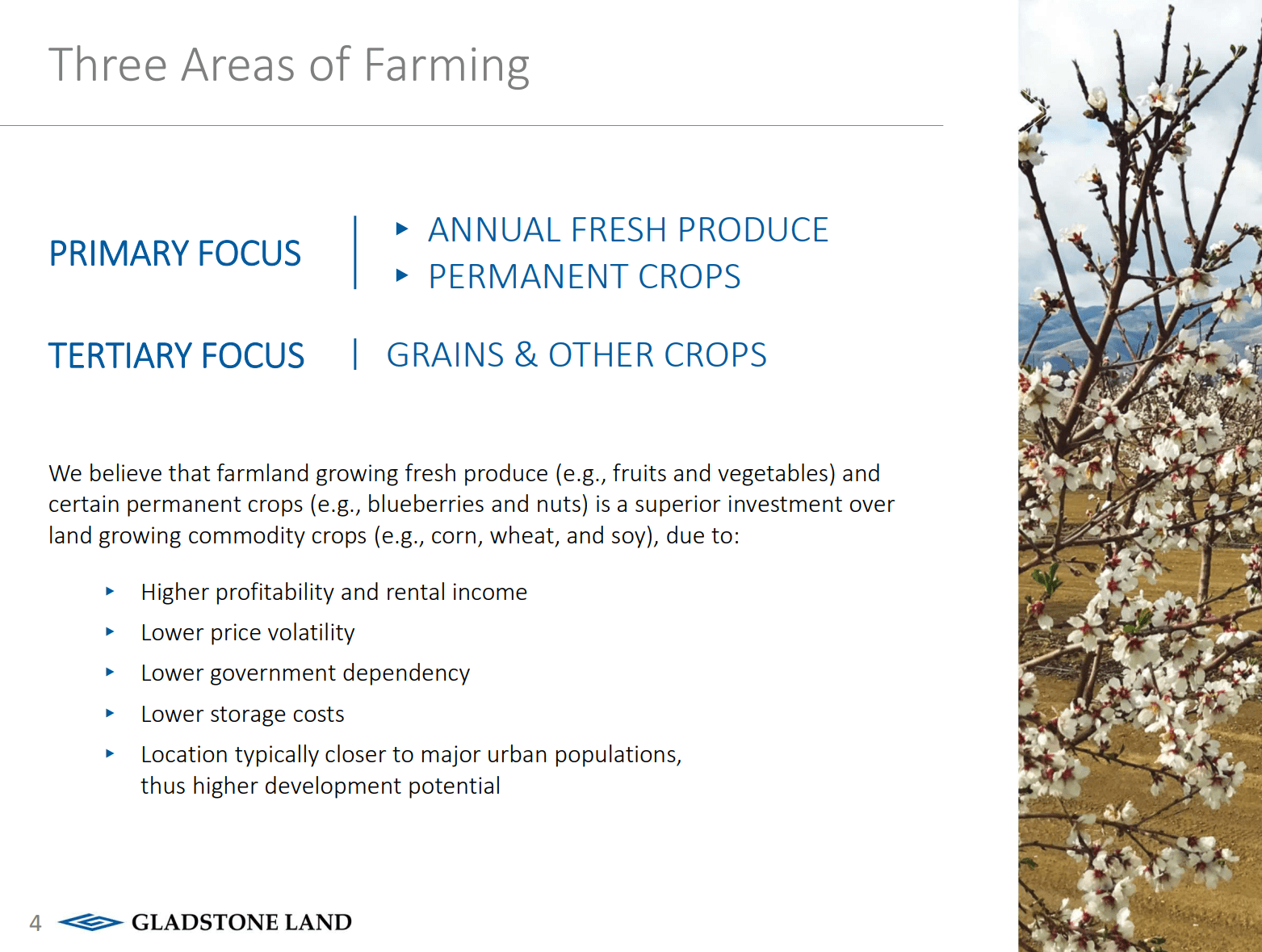

Gladstone Land Corporation is a real estate investment trust ("REIT") specializing in acquiring and owning farmland across the United States. Gladstone is primarily focused on acquiring annual fresh produce (i.e. fruits and vegetables) and permanent crop (i.e. blueberries and nuts) farms, as these have historically been superior investments compared to commodity crops (i.e. corn and wheat) (Figure 1).

Figure 1 - Gladstone Land is focused on fresh produce and permanent crops (LAND investor presentation)

{kind=link}

Fresh produce and permanent crops typically enjoy higher profitability and rental incomes and lower price volatility. In addition, these crops have lower storage costs and these farms are typically closer to major urban centers, which leads to higher development potential for the land.

Gladstone currently owns 169 farms with 116,000 total acres of farmland, in addition to 45,000 acre-feet of banked water in California. Gladstone usually leases its farms to farmers on a triple-net basis (meaning the farmer pays rent, insurance, maintenance, and taxes).

Farmland Delivers Strong Long-Term Returns

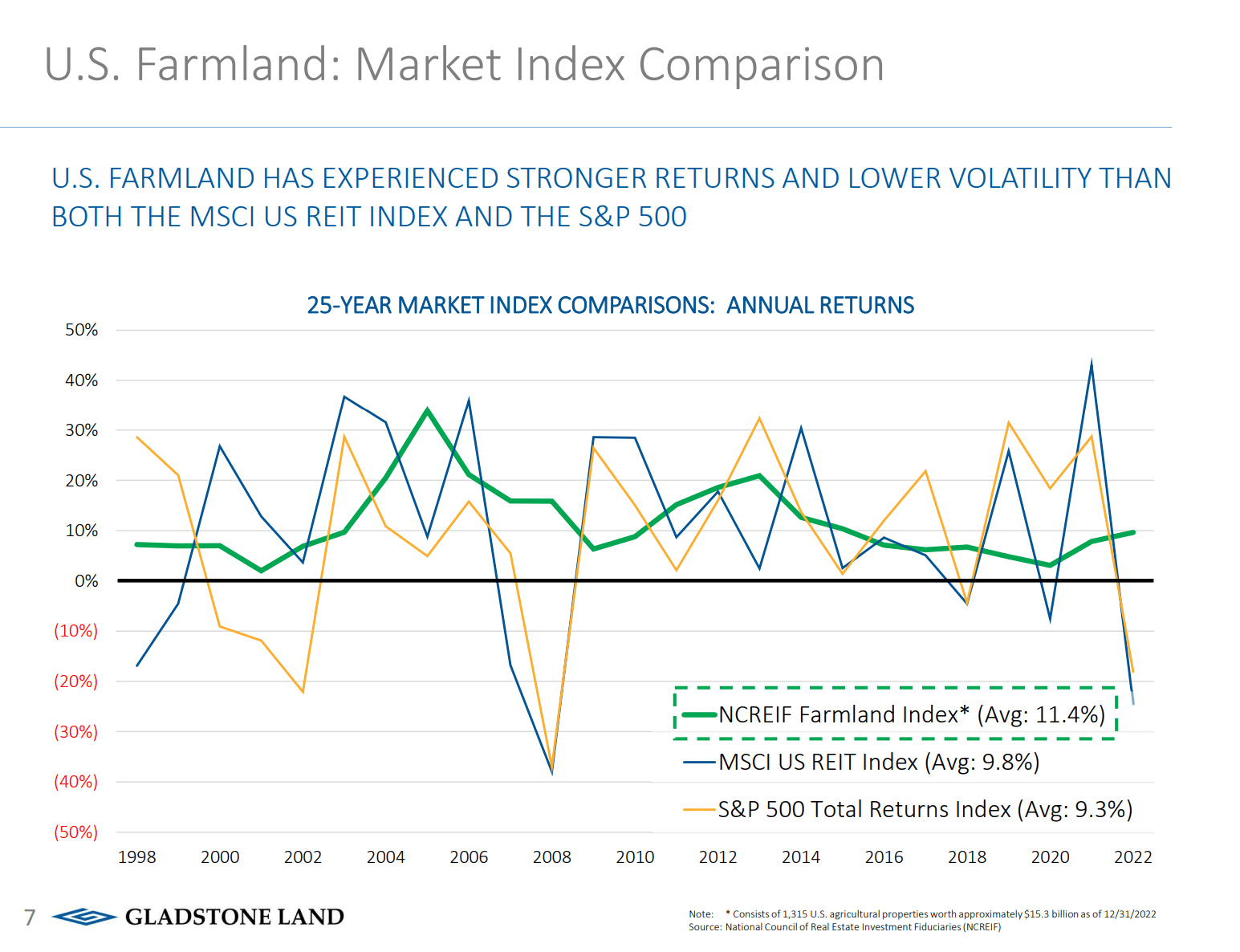

Over the long-run, farmland has been a better investment than the broader REIT universe and the S&P 500 Index (Figure 2).

Figure 2 - Farmland has delivered better returns than S&P 500 (LAND investor presentation)

{kind=link}

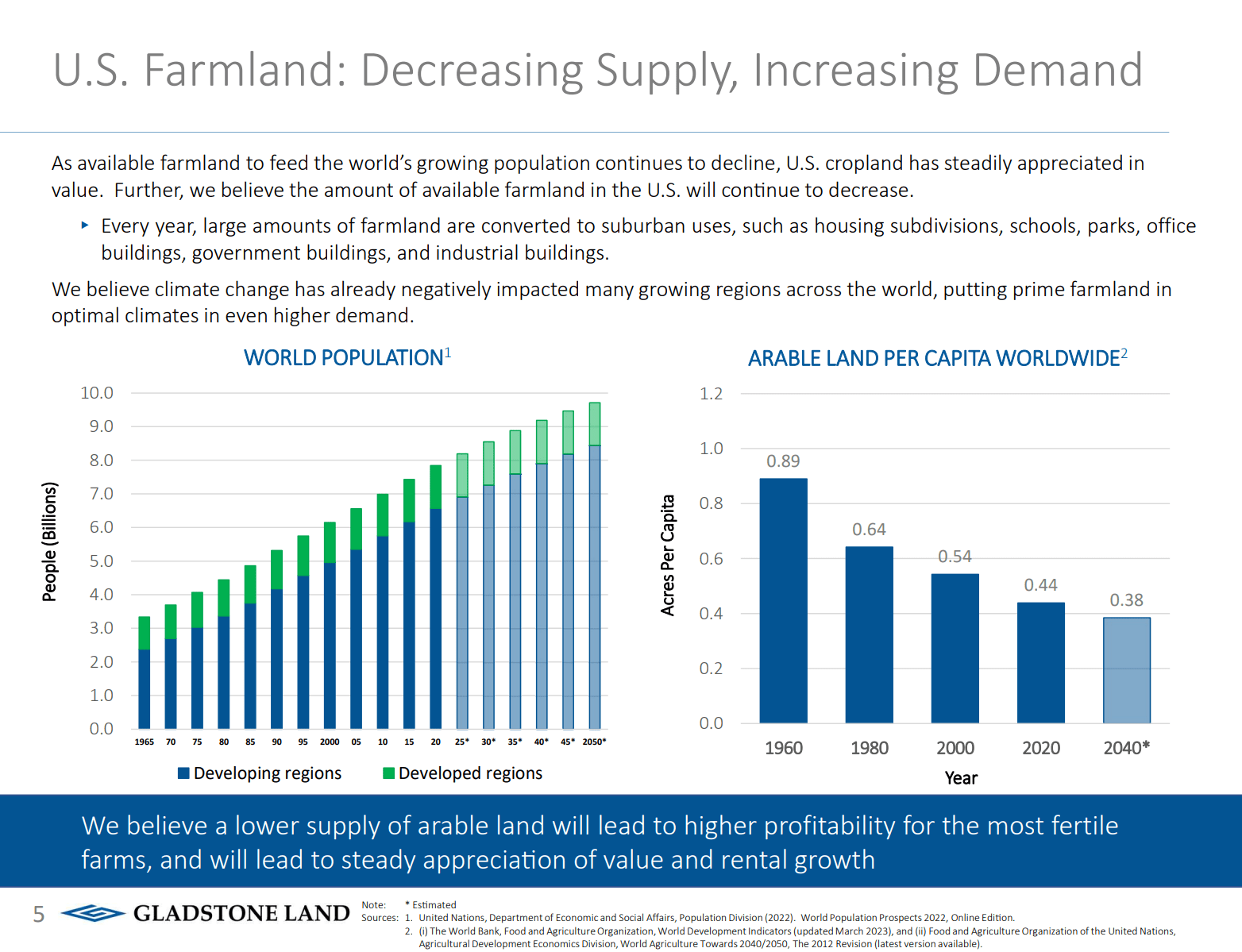

The main reason is because there is only a limited supply of arable land while the world's population continues to climb, which puts upwards pressure on the value of farmland (Figure 3).

Figure 3 - Supply/demand behind the increase in farmland values (LAND investor presentation)

{kind=link}

Gladstone Has Enjoyed Consistent Rental Growth

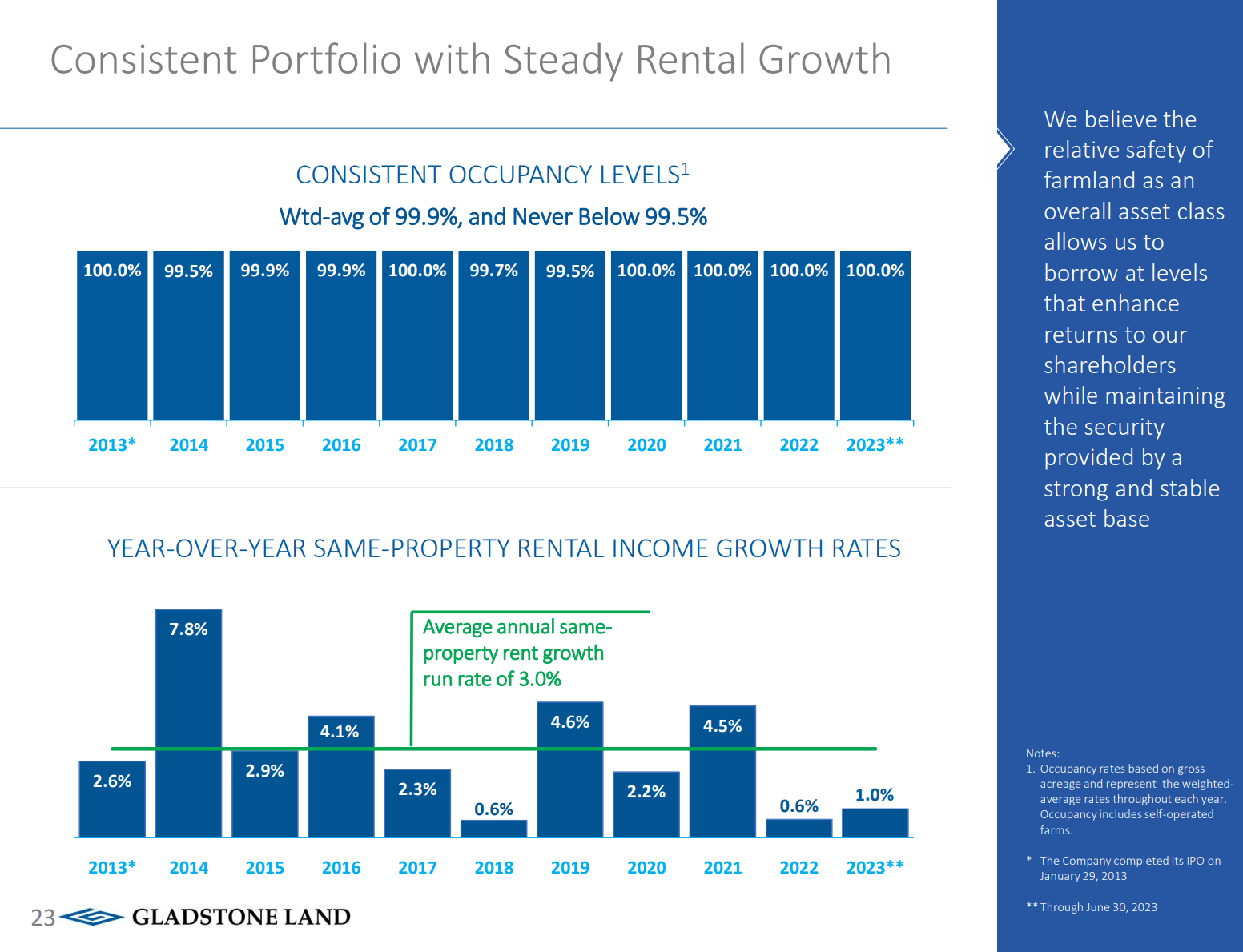

For Gladstone, this dynamic has translated into steady rental growth, with average annual same property rent growth of 3.0% over the past decade and near full occupancy (Figure 4).

Figure 4 - LAND has enjoyed near full occupancy and steady rental growth (LAND investor presentation)

{kind=link}

Recent Quarters Marred By Tenant Issues

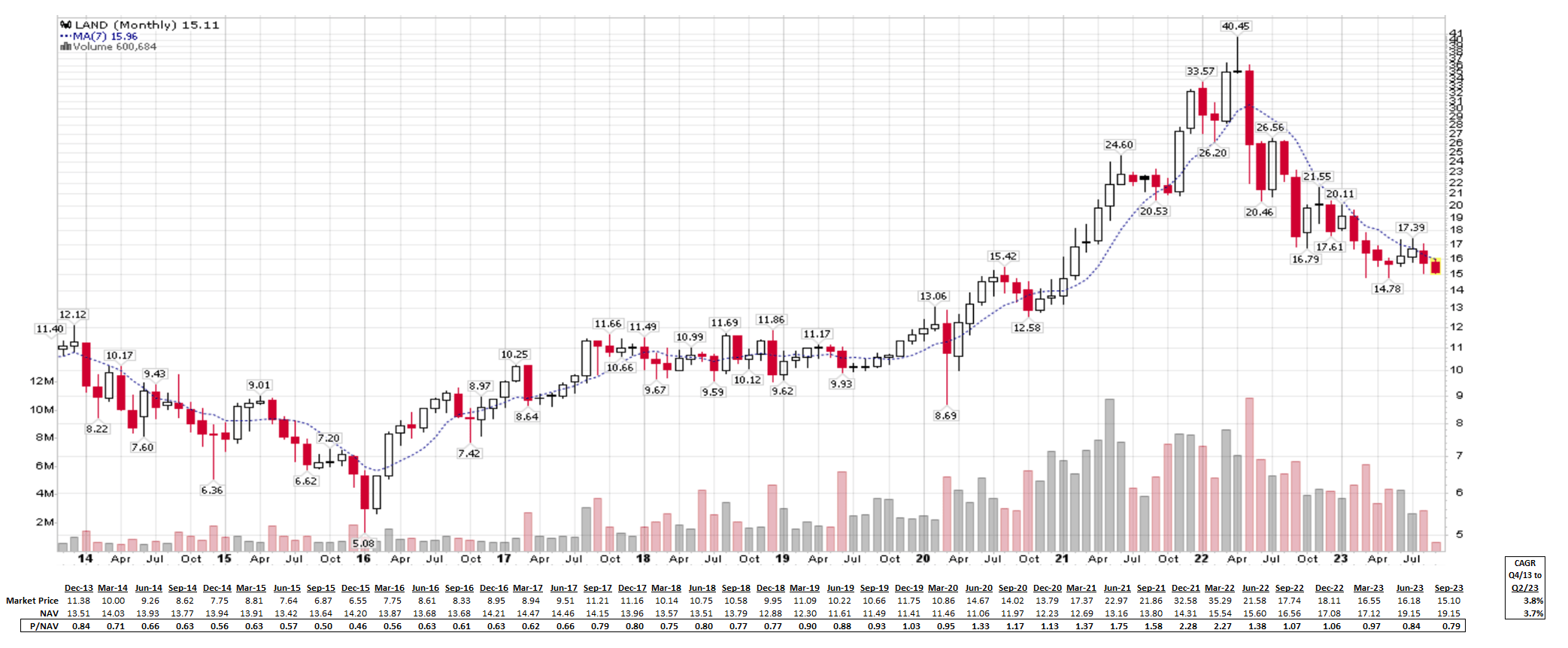

Despite steady operating performance, the stock price of the Gladstone Land itself has been quite volatile. First, immediately following the COVID-pandemic, there was a perceived shortage of food supplies, which caused a literal 'land grab' as investors snapped up shares of Gladstone, pushing valuation to over 2x NAV (Figure 5).

Figure 5 - LAND stock price vs. P/NAV (Author created with data from company reports and stockcharts.com)

{kind=link}

However, in recent quarters, LAND's stock price has come back to earth due to higher interest rates and tenant issues. Gladstone is now trading at only 0.79x P/NAV, based on the most recent published NAV of $19.15 / share.

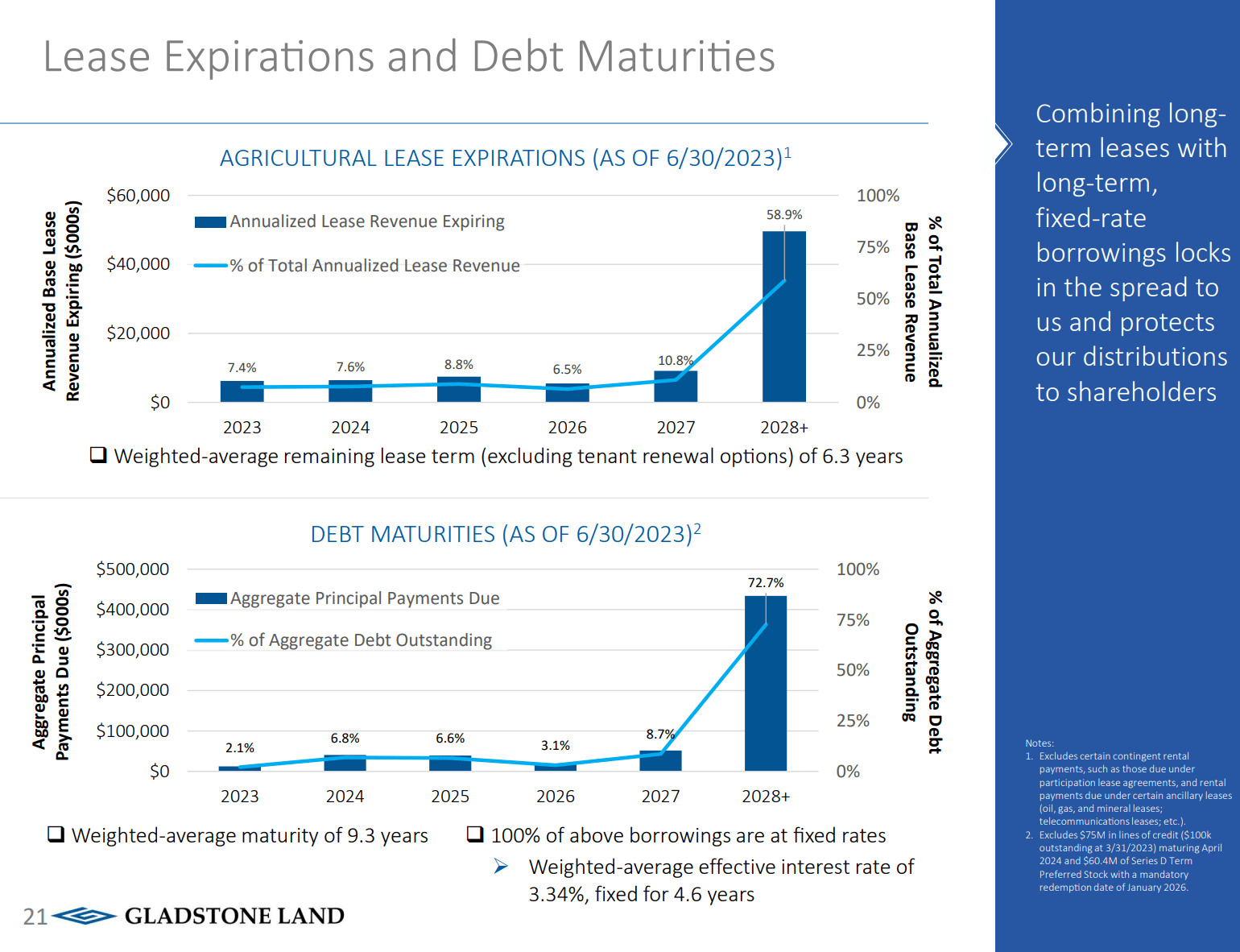

Gladstone is susceptible to higher interest rates as the REIT is heavily indebted, with almost $600 million in fixed-rate debt outstanding. However, Gladstone's debts are generally maturity matched against its lease maturities, giving investors some protection from higher interest rates (Figure 6).

Figure 6 - LAND debt maturities matched against leases (LAND investor presentation)

{kind=link}

The more pertinent problem appears to be delinquent tenants, as Gladstone reported having credit issues with 3 tenants covering 7 leases in total (4 in Michigan and 3 in California).

For the 4 farms in Michigan, Gladstone has terminated the lease agreements with the prior tenant and have entered into short-term leases with new tenants. For 2 of the farms in California, the tenant is current on rental payments and the farms may be placed back into good standing if certain conditions are met. Finally, for the remaining farm in California, Gladstone is currently trying to renegotiate with the current tenant.

Regardless of the outcome of the negotiations with the 3 tenants, management believes its high quality farms can be re-leased on market terms within 1 to 12 months if necessary.

Series C Prefs Could Be An Interesting Investment Opportunity

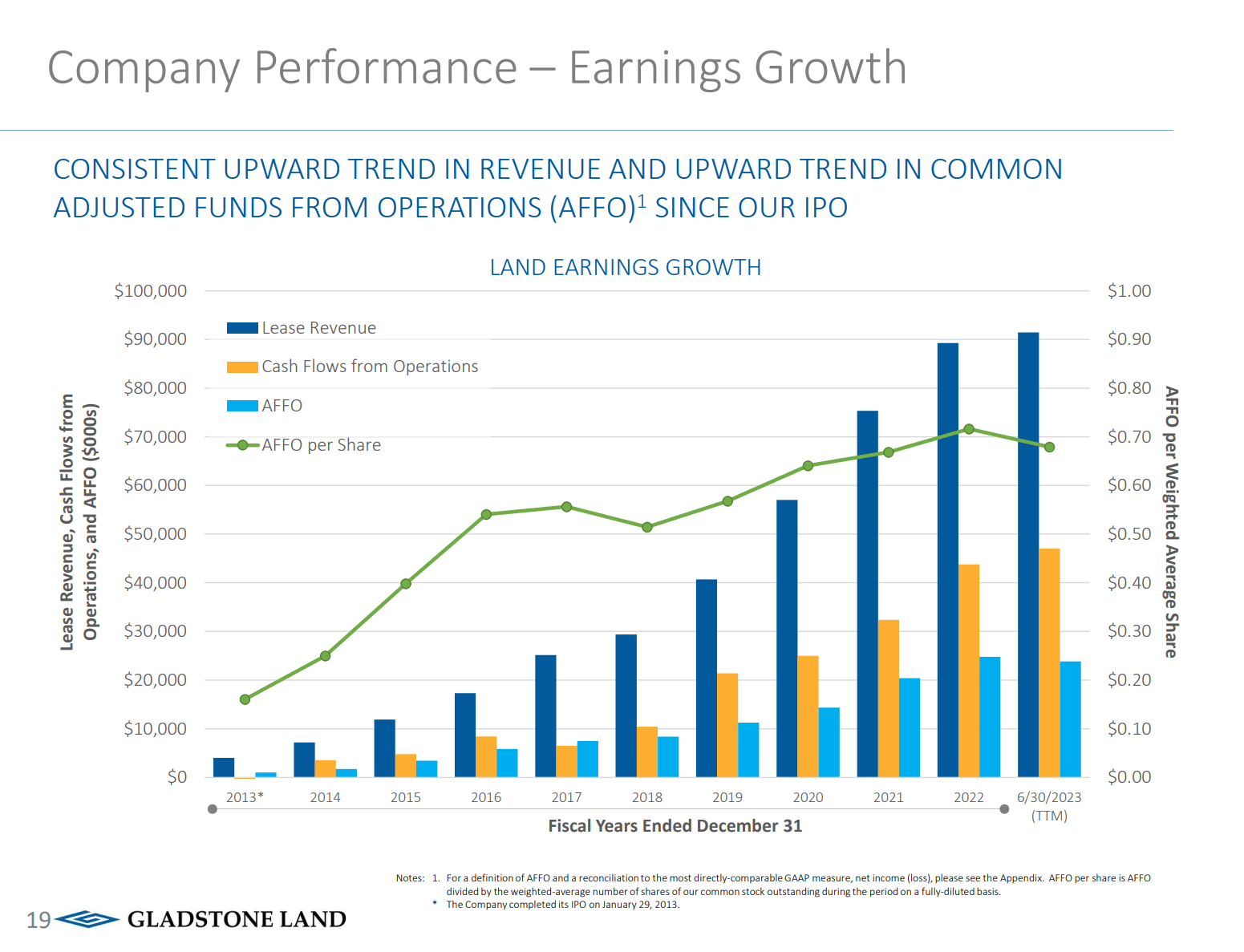

Given the defensive nature of farmland, I believe Gladstone's cash flows are generally fairly safe. In fact, Gladstone has recorded a consistent upward trend in lease revenues and cash flow from operations since IPO (Figure 7).

Figure 7 - LAND has seen steady growth in revenues and cash flows (LAND investor presentation)

{kind=link}

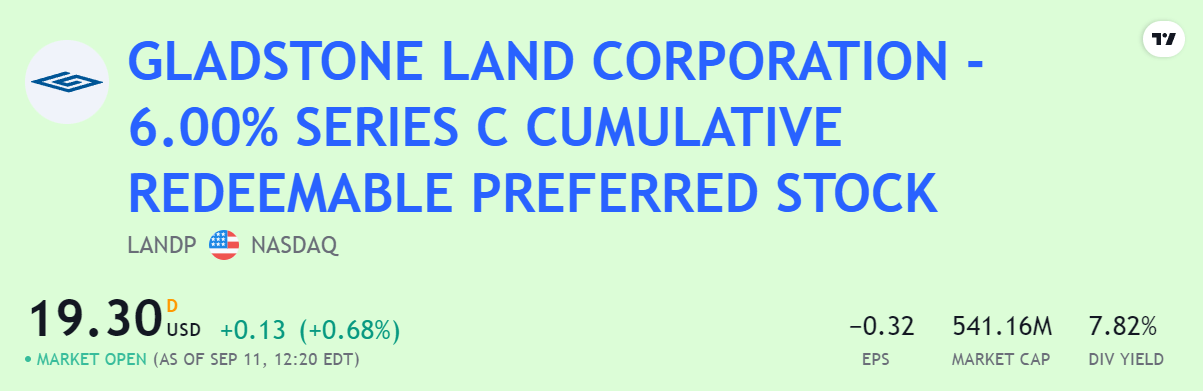

Recently, Gladstone listed its Series C Preferred Shares on the Nasdaq, under the symbol "LANDP". The Series C preferred shares were issued from 2020 to 2022 and pay a 6.0% coupon on its $25 face value. However, given the rise in interest rates, the Series C prefs are now yielding 7.8% currently (Figure 8).

Figure 8 - Series C prefs yielding 7.8% (quantumonline.com)

{kind=link}

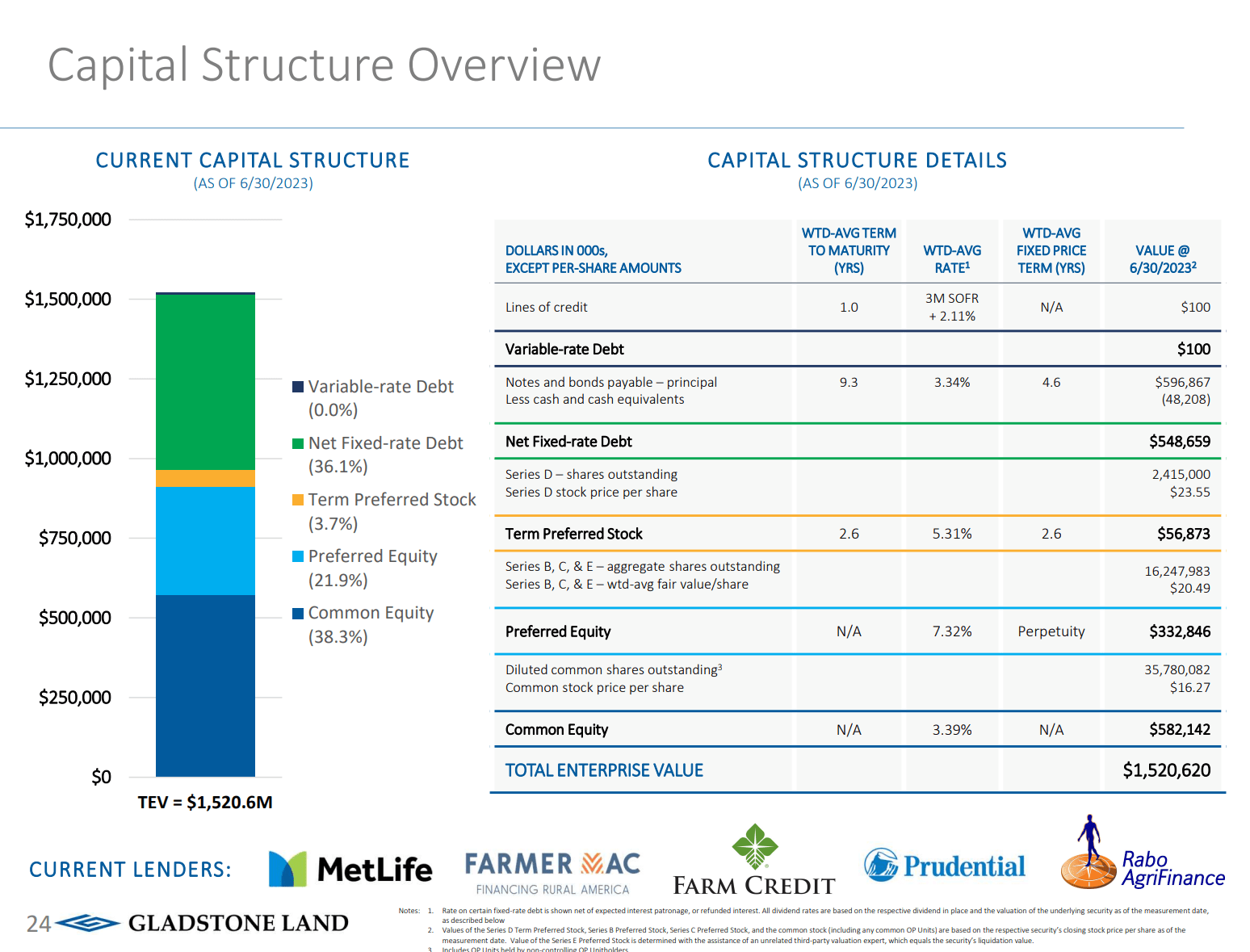

Looking at Gladstone's capital structure, Gladstone's preferred shares are protected by over $580 million in equity capital. Furthermore, given that preferred shares rank ahead of common equity, Gladstone will have to cut its common equity dividends to zero before preferred share dividends are cut.

Figure 9 - LAND capital structure (LAND investor presentation)

{kind=link}

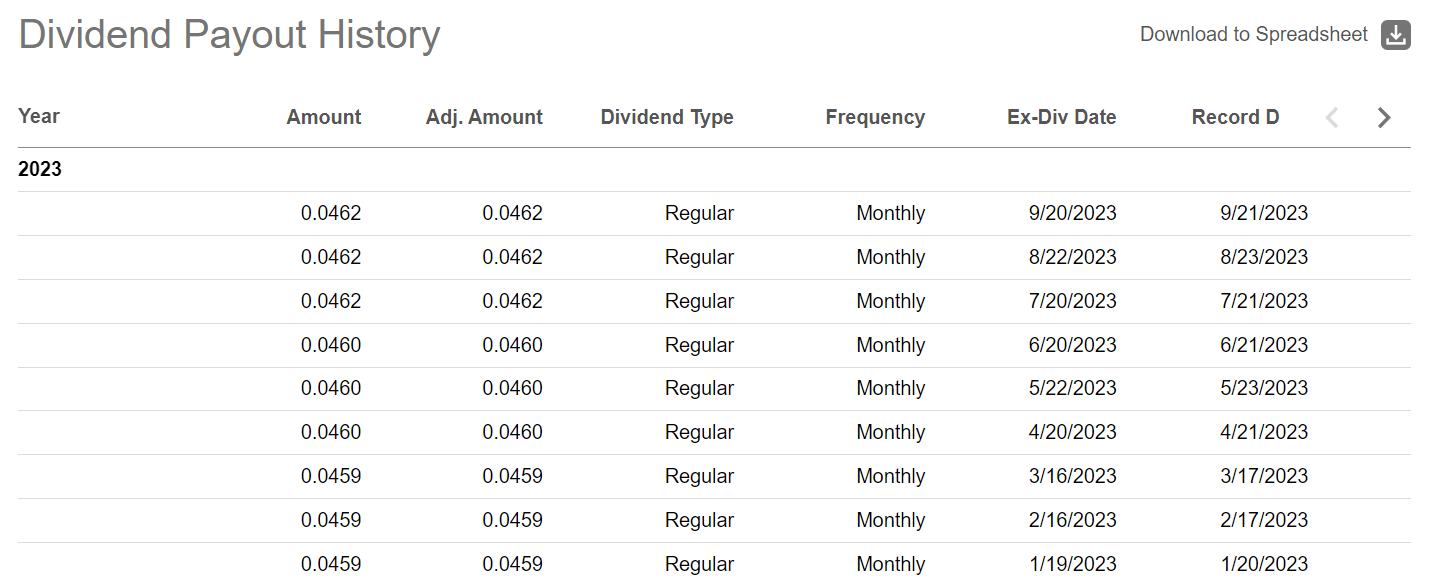

There are currently no indications that a common share dividend cut is in the cards for Gladstone. In fact, Gladstone recently increased its monthly common equity dividend from $0.046 to $0.0462 / share, suggesting management remains comfortable with business operations (Figure 10)

Figure 10 - LAND common dividends recently raised (Seeking Alpha)

{kind=link}

Risks Of Owning Gladstone Preferred Shares

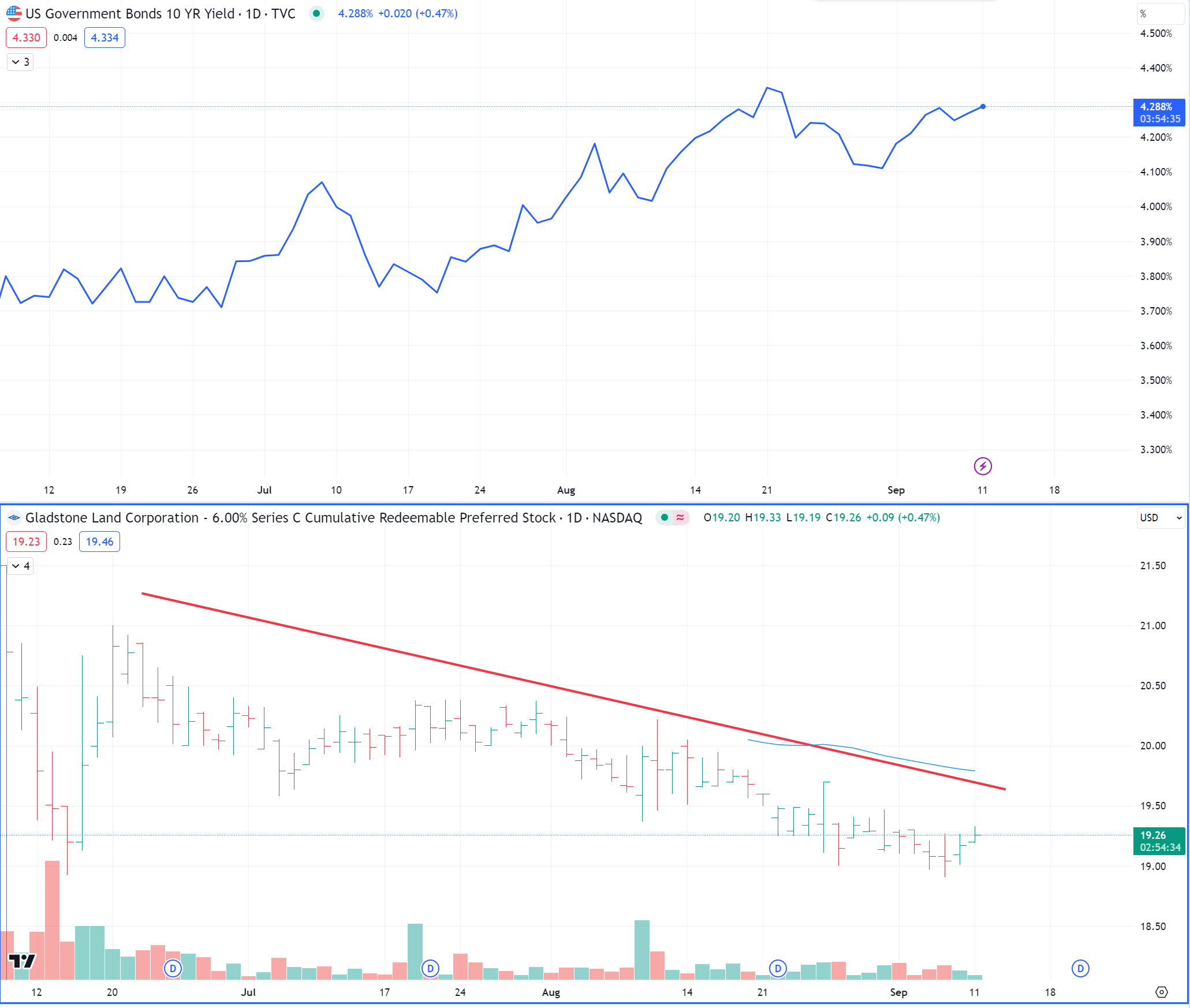

The biggest risk to owning Gladstone Series C Preferred Shares remain long-term interest rates. Given the perpetual nature of these preferred shares, investors can think of them as similar to long-term bonds on Gladstone Land. As treasury yields have risen in the past few weeks, the share price of the Series C prefs have declined (Figure 11).

Figure 11 - LANDP vs. 10Yr yields (Author created with tradingview)

{kind=link}

If long-term interest rates continue to rise, chances are, the price of the Series C will continue to decline. However, locking 7.8% yields from defensive farmland appears to be an attractive proposition in the long-run.

Conclusion

I believe the Series C preferred shares of Gladstone Land could be an interesting investment opportunity, with the shares currently yielding 7.8%. Gladstone owns over 110k acres of valuable farmland with steady occupancy and reliable growth in rents that generate steady income to pay dividends on its preferred and common shares. I rate LANDP a buy .

For further details see:

Gladstone Land Series C Preferreds: 7.8% Yield From Farmlands