GLAPF - Glanbia: Fairly Valued For Current Performance

2023-08-31 07:11:38 ET

Summary

- Glanbia has seen a 47% increase in value since August 2020, with its US nutrition business continuing to perform well.

- Profitability has been less impressive, with a net profit margin of 3.5% and post-tax profits of €200m in 2020.

- The company plans to boost its EBITA margin, reduce net debt, and grow its dividend, but the author remains skeptical about its ability to significantly improve profitability.

Irish based nutrition firm Glanbia (GLAPF) has the makings of a strong business, but I continue to see it as solid rather than exciting.

I last covered the company in August 2020, when I have it a "hold" rating. Since then it has moved up in value by 47%. I maintain my "hold" rating.

Ongoing Business Strength

In my previous piece I outlined why I liked Glanbia's U.S. nutrition business and that continues to be the case.

According to data provider Euromonitor, last year Glanbia was the number one global sports nutrition brand. With currency effects stripped out, revenue was €1.6bn.

The company assesses its total addressable market to be $25bn. In my view, it remains a highly fragmented market. I also expect it to show long-term growth and one of the things I like about sports nutrition is that demand is fairly resilient. Even if the economy slows down, many recreational athletes will continue with their supplements programme. So Glanbia has a strong position and room for growth in a market with attractive long-term drivers.

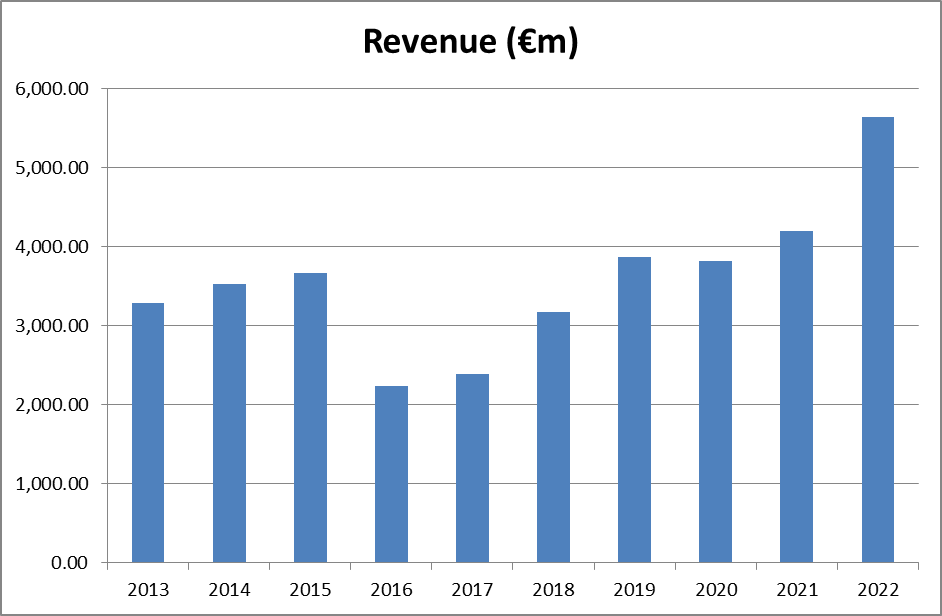

The company has changed shape over the years, but overall, the long-term trajectory for revenue has been upwards. Last year showed a notable jump, which I think can be sustained.

{kind=link}

Compiled by author using data from company reports

Profitability has been less impressive. Last year, post-tax profits came in at around €200m, lower than they were in 2018 even on much higher revenue. That is a net profit margin of 3.5%, which for an ingredients supplier I would not say is bad but also not great (U.K.-listed sweeteners maker Treatt ( TTTRF ) has net margins above 9% last year) but given that a large part of Glanbia's business is selling branded end products, I would hope for higher margins. So while a return on capital employed of 11.1% seems reasonable to me, I think Glanbia needs to work on improving its profitability.

Last month, the company announced its half-year results. Revenues fell 10.3% and post-tax profits grew 38%. (One significant difference is that the company has now switched from reporting in euros to reporting in U.S. dollars). It upgraded its full year guidance to between 12% and 15% growth in adjusted EPS.

While that jump in profits is welcome, the declining revenues are a concern. A positive analysis is that this reflects Glanbia's reshaping of its portfolio, whereby it is focussing on higher margin products and is willing to sacrifice some revenues elsewhere. Time will tell whether this is indeed the case.

Room for Growth

How might such profitability growth be delivered?

Glanbia's answer is displayed in the diagram below.

{kind=link}

But a lot of that consists simply of riding a wave. That could be good for revenue but not necessarily for profitability. Business optimisation and disciplined financial management could help on that score. But that would have been true at any point in the firm's history.

The company is targeting a 12% EBITA margin over the 2023-25 period. I see that as a junk measure: interest and tax are real business expenses. By my calculation, last year the EBITA margin was 6.2% (€347m EBITA on to €5.6bn revenue). Doubling the EBITA margin within three years seems over ambitious to me in the absence of largescale change, which is not planned as far as I am aware. Even if the target is improved, post-tax earnings last year were only 76% of post-tax profits. Nonetheless, boosting EBITA margin should also boost the post-tax profit margin. I am simply not persuaded on current evidence that the company can hit such an ambitious jump in its average profitability.

Improving Balance Sheet

Last year, net debt was reduced to €459m, from €603m.

That improvement in the balance sheet is welcome. The current net debt is around 11% of market cap, which I regard as fine.

Free cash flows last year were €84m, which coincidentally was also the cost of dividends. For now I think that free cash flow looks adequate for the company's financial health.

Room for Dividend Growth

The company targets a dividend payout ratio of 25%-35%, which I regard as conservative. Last year it raised the dividend by 10% and the current yield is 2.4%, which is fine but not particularly attractive given the current level of yields seen more broadly in the London market though it is broadly in line with sectoral names like Associated British Foods ( ASBFY ) and Cranswick (CRWKF).

Despite the jump last year, the dividend is still markedly below where it stood in 2018. In the long term, for the dividend to keep growing strongly within the current dividend policy, earnings will need to grow significantly. I think this is well within the realm of possibility but it may also not happen. Fairly tight profit margins can make it tricky to keep growing earnings strongly, after all. So I expect annual dividend growth but likely at a lower level than we saw last year.

Free cash flow last year came in at €268.6m. Dividends cost the company €84.4m so were amply covered by free cash flow. If the company can maintain roughly that level of free cash flows, I see ample room for ongoing dividend growth while keeping the payout comfortably covered by free cash flows.

Valuation

Currently, Glanbia trades on a price-to-earnings (P/E) ratio of around 20. If the company can continue to grow revenues strongly and improve profitability, I think the prospective P/E ratio could be more attractive than that figure suggests. It is markedly higher than the 15 seen at Cranswick, for example, which has a superb track record in growth and dividend increases.

For a company with a strong position in a large addressable market, I see that as a reasonable valuation. It does not jump out at me as outstanding, however. So, for now, I maintain my "hold" rating.

For further details see:

Glanbia: Fairly Valued For Current Performance