FGLD - GLD: Gold Prices Up 7-Fold So Far This Century And The Best Is Yet To Come

2023-05-11 17:19:03 ET

Summary

- Given the increasingly volatile global economic, geopolitical, fiscal, monetary, and financial situation, few investors are looking to part with their gold positions.

- Net inflows of gold held by central banks, ETFs and other institutions suggest that the market is realizing the need to have a hedge against possible financial disaster.

- If gold prices are to repeat the performance relative to stocks we saw so far this century for the next 23 years, we are looking at a price of about $14,000/ounce.

- While gold's performance in the long term is likely to be bright, it may also be volatile at times, making GLD a convenient tool to play shorter-term volatility.

- Growing talk of new international payment mechanisms, such as stablecoins backed by gold could become a reality within the current geopolitical context, in which case gold prices relative to fiat currencies can potentially explode higher.

Investment thesis

The net inflow of gold into global central bank vaults is reported as having hit a new record in the first quarter of this year. The SPDR Gold Shares ETF ( GLD ) and other funds are also seeing a net inflow , suggesting that investors are getting in on the trend. Ordinarily, this would not necessarily provide for a short-term or long-term gold bull argument. After all, trends may be reversed on certain signals, and net outflows from funds and from central banks always have the potential to throw gold prices into a tailspin. This time it seems different from previous such episodes, because there is arguably no triggering reason to sell gold, and I personally doubt that there will be in the foreseeable future. Gold prices are up over seven-fold since the start of the century, beating out major stock indexes. In the next few years and decades, gold is likely to outshine its performance so far this century relative to other investment assets, with the need to have a major hedge against the fiat-based global financial system becoming more and more obvious.

GLD is a convenient vehicle for short-term gold investment needs

There is a practical potential downside to owning GLD shares, as opposed to having physical gold in one's possession, especially if one intends to hold the shares for a prolonged period.

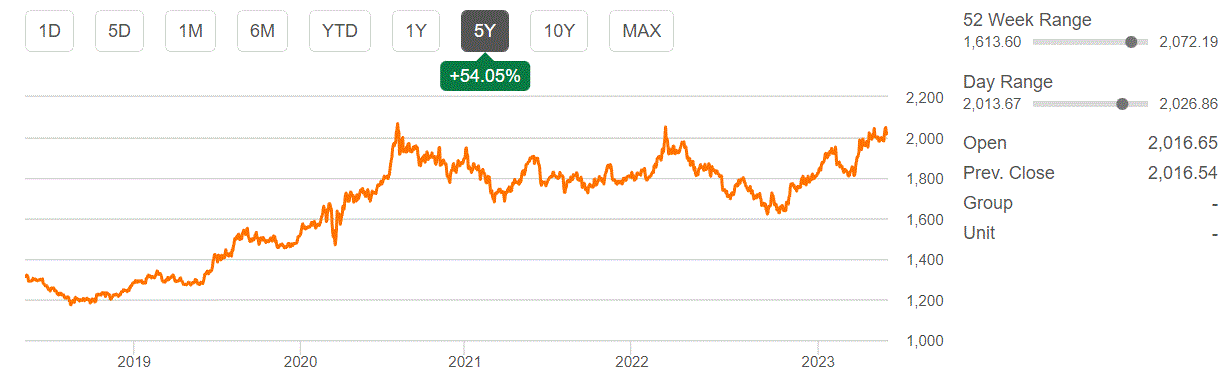

Gold spot price (Seeking Alpha)

{kind=link}

As we can see, in the past five years the gold spot price advanced just over 54%.

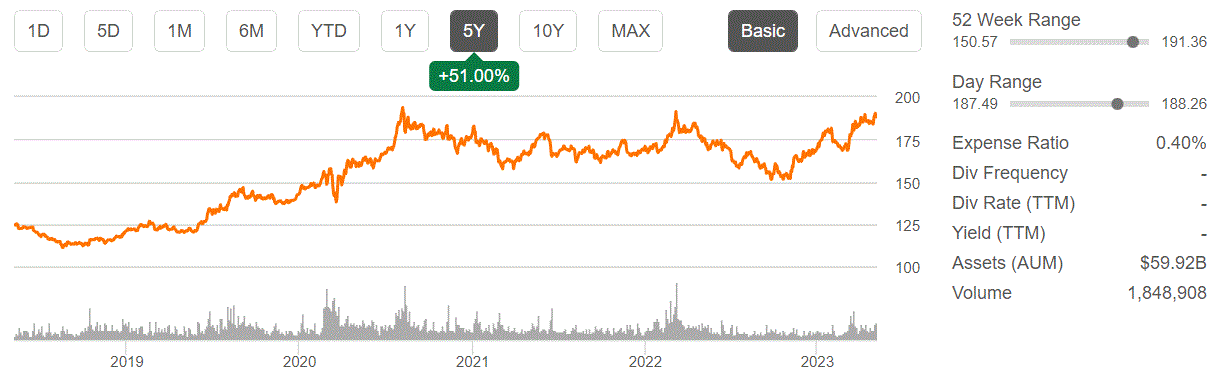

GLD share price (Seeking Alpha)

{kind=link}

The GLD share price increased by a slightly smaller percentage for the same period, with the discrepancy owed mostly to the effect of the yearly expense fees currently sitting at .4%. There are of course fees associated with trading in physical gold, but in time GLD fees may surpass physical gold trading fees.

There is also the issue of not having direct access to physical gold on request, which has been an issue raised over the years, along with suspicions of shares not being covered with physical gold assets. I personally never dwelt too deeply into the issue of whether the gold is actually there to cover 100% of the shares, because it is simply beyond my investigative abilities. As far as the conversion issue, the way I see it, one can always sell GLD shares and use the proceeds to buy physical gold. I see physical gold as something to buy & hold for a prolonged period, while GLD is a more convenient avenue to buy & sell, adjusting to shorter-term market moves.

Hard to think of a viable investment thesis in favor of the sale of gold investment assets within the current global economic and geopolitical context

With gold prices close to all-time highs, the typical investment strategy would dictate for investors who bought at a significantly lower price to start considering exit strategies meant to take profits. It is certainly the strategy that I tend to employ most of the time, with most investment positions, where I tend to sell at least a part of an investment position when new all-time highs are reached, in order to lock in some of the profits, and in the process reduce the likelihood of a net loss on any investment. Once in a while, it is worth considering being flexible and adjusting to any particular circumstances accordingly, rather than following general strategies. If there is ever such an exceptional situation, this is arguably it.

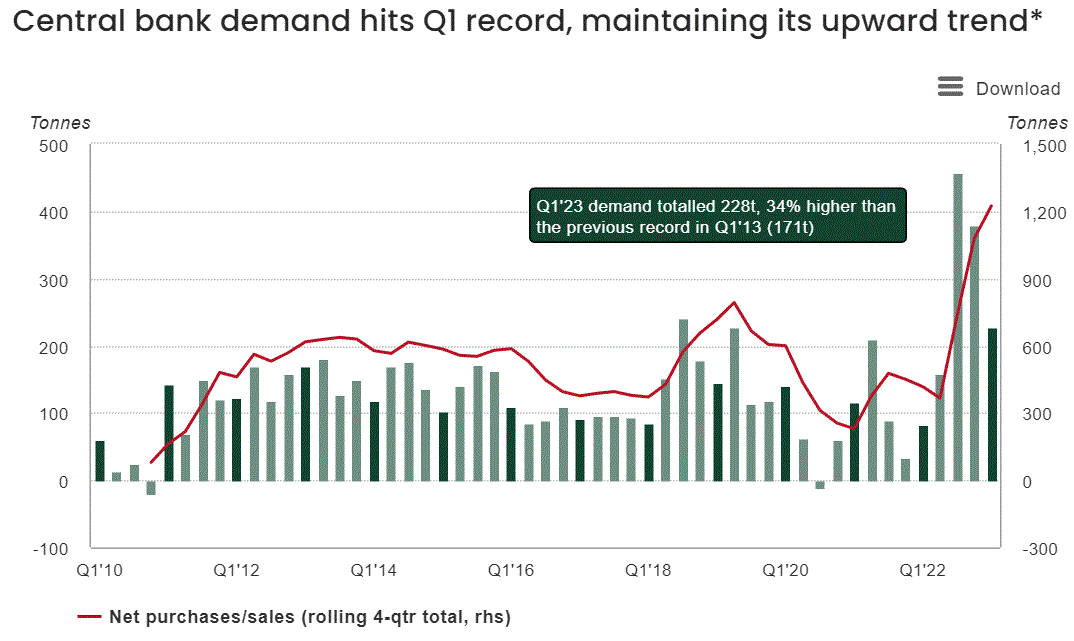

It seems that I am not the only one with this point of view. Central banks in particular seem to be piling into gold, despite gold prices having averaged higher in Q1 of this year compared with previous quarters in 2022.

{kind=link}

I think it is worth taking a step back and pondering what might be the reasons behind central banks around the world being so eager to shore up their net gold holdings. To me, it seems like a very clear response to the growing geopolitical, economic, and financial instability of the world. The current decade seems to be the one where the post-WW2 is set to disintegrate, as it no longer fits the realities of the world today. In a worst-case scenario, things could unravel more spectacularly and potentially more violently than most might expect.

The sources of this unraveling are becoming more numerous than we can reasonably examine for the purpose of this article. If I were to have to try to pinpoint the main two roots of the events we see unfolding before us, I would pick two that in my view drive the events, with the problems we are focused on being mostly resulting symptoms.

The commodities price spike that may have ushered in a new prolonged era of global scarcity

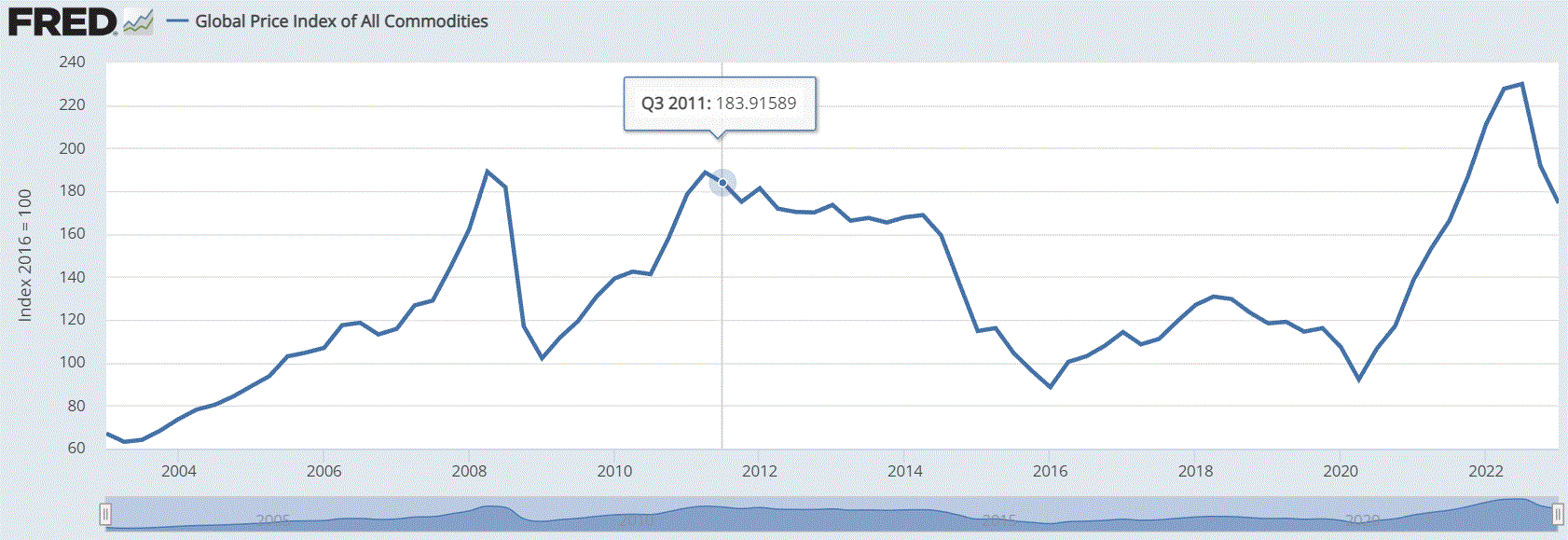

The first-root cause is what I perceive to be a new era we seem to have entered in terms of the availability of crucial commodities. We see this being manifested in record-high commodities prices last year.

Federal Reserve Bank of St. Louis

{kind=link}

As we can see, after last year's record-high commodities prices, this year we are seeing a moderating trend in commodities prices. It is not what it seems, however, because it is mostly the result of a dramatic decline in economic growth taking place in the developed world.

{kind=link}

Even with the slowing global economic growth forecasts in place, we may still be looking at a return to high commodities price inflation as soon as the second half of this year, or next year at the latest. For instance, Goldman Sachs sees a possibility of $100/barrel oil by the end of this year. Higher oil and other energy input prices can affect the price of other key commodities that need high levels of energy input for extraction.

There are other sources of commodities price inflation, such as food prices, and certain metals such as copper that are actually up in price compared with the last quarter of 2022. Many crucial global commodities seem to be poised for a reversal of the temporary price reprieve we are seeing, as soon as there is any slight demand pickup. The fact that we are still near all-time high commodities prices, even as the global economy has clearly stalled out, should be a reason to worry.

We did get a reprieve of about a decade, courtesy of the shale boom , which added about 10% to the global crude oil & gas supply, but that card has now been played. At best, we can expect small incremental growth, mostly when higher oil & gas prices will stimulate some extra drilling. The inflationary spike we have seen lately is in large part connected to resource scarcity issues, that are not likely to go away. We will probably bump up against high commodity prices every time the global economy will attempt to accelerate, which will bring with it issues such as inflationary pressures. With inflationary pressures, we will see financial, economic, social, and probably geopolitical fallout all intensify.

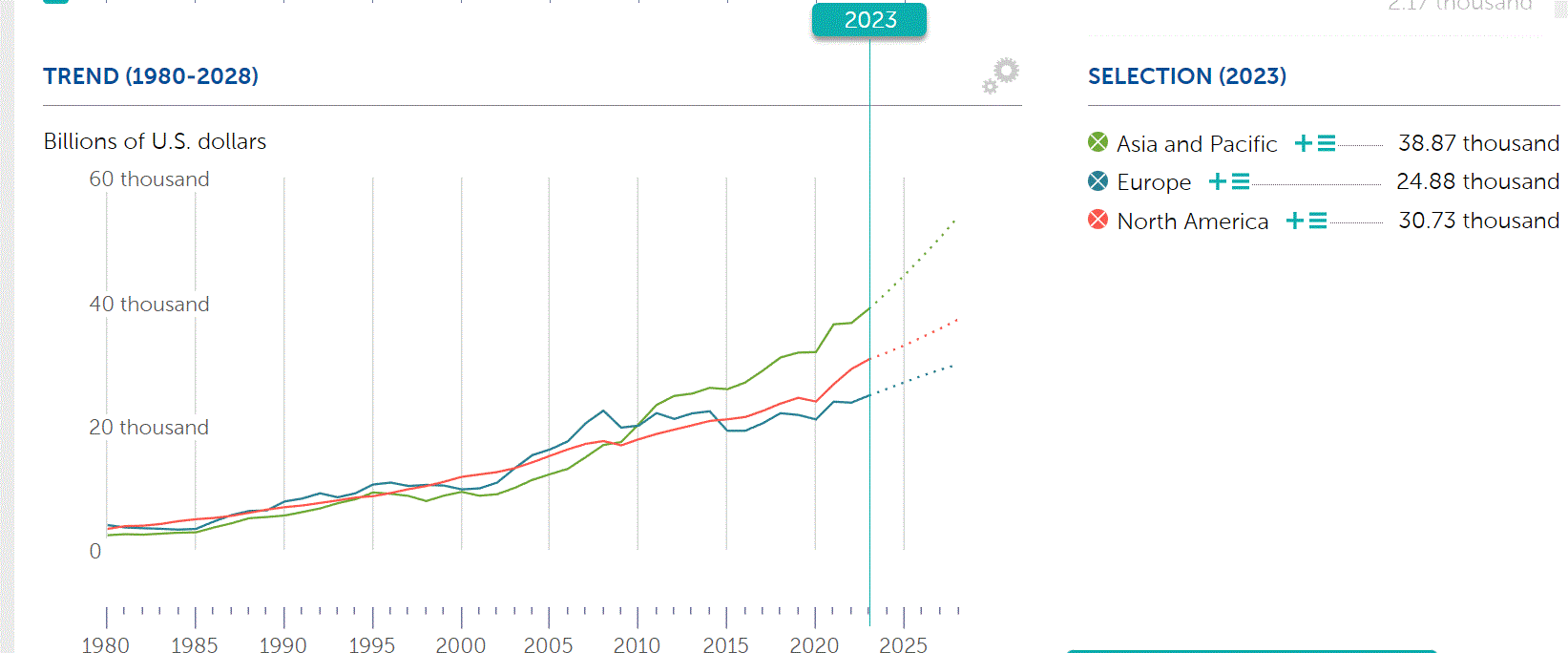

The great shift of the global economic weight to Asia

Another major factor that has been shaping the global economic landscape is the shifting of the global economic weight away from the post-WW2 dominant Western Hemisphere, to Asia.

{kind=link}

As we can see, in the past decade or so, Asia's economy seems to be outpacing North America and Europe, with the gap growing exponentially. The post-WW2 global order however is based on Western institutions and leadership.

Instability for the foreseeable future

Having identified the two main root causes of global economic, geopolitical, and financial instability, as I personally perceive them, and looking at the symptoms we experienced as a result of the past two decades, my view is that we will not only continue to see instability but it will intensify in frequency and in terms of impact. The symptoms we saw, like inflationary pressures, after over a decade of deflation and resulting low-interest rates are likely to spawn new symptoms. The recent collapse of a few US banks as a result of a spike in interest rates is just an example of what to expect going forward.

The geopolitical fallout from the changing world we live in gave rise to increasingly frantic efforts around the world to reduce reliance on Western financial institutions and currencies in global trade. Russia & China are of course prime examples of this, but India , Brazil , and many others have been equally as eager in the past year to move away from our still very dominant global financial infrastructural and institutional dominance. The implications for our financial, fiscal, and monetary situation are quite obvious. High deficit spending, low-interest rate policies are likely to become a thing of the past, making the economic environment more difficult.

Of particular interest to gold investors should be the prospect of a return of gold as a facilitating mechanism in global trade & finance. The stablecoin concept, with gold-backed crypto, seems to be of growing interest to a number of countries around the world that are looking for alternatives to the fiat, dollar & euro-dominated global financial system. Russia in particular seems eager to explore the creation of such a mechanism as a way to bypass our financial infrastructure for trade with its partners. If such cryptocurrencies will start to be launched by central banks around the world, gold demand could skyrocket.

Investment implications

Since the beginning of the century, The Dow Jones & S&P are up about 220%, the Nasdaq is up about 200% as well. Gold prices are up about seven-fold, from about $280/ounce to about $2,000 currently. Ordinarily, this would be the point where one might argue that it is time to take profits on gold and pile into stocks that provided some decent, but by no means spectacular returns so far this century.

While I do not want to venture and guess any future price points that may be reached in the coming years, I do believe that gold prices will outperform stocks to a greater degree than they did in the past two decades. It outperformed in the run-up to the current decade of crisis. Logic dictates that in the midst of the crisis itself and the potentially endless symptoms we will experience going forward, it should do even better relative to other investment assets. In other words, if the Dow will reach about 100,000 about two decades from now, then gold prices will likely be at about $14,000/ounce or higher by then, assuming that gold will continue to outperform stocks, at a stronger pace than it did in the past two decades.

While the performance of gold should be spectacular in the long term, it should also see a lot more volatility, along with most of the rest of the market. Perhaps it will be somewhat less volatile, comparatively speaking, when looking at other investment assets, but we should still expect a great deal of it going forward, with wild swings in price along the way. GLD is a convenient way to navigate through that potential volatility going forward. It is much easier to buy and sell than physical gold, making it easier to react to shorter-term market moves. While I prefer to keep most of my gold positions in physical gold as well as in gold mining stocks, GLD remains an important component of my overall gold investment strategy.

For further details see:

GLD: Gold Prices Up 7-Fold So Far This Century And The Best Is Yet To Come