FGLD - GLD: Why Gold Should Be Your First Portfolio Pick In A Recession

2023-04-26 00:16:34 ET

Summary

- Gold is well known as a safe-haven asset, but when recessions require quantitative easing and negative real interest rates, gold can provide much more than stability.

- From 2007 to 2011 during the global financial crisis, the price of gold increased over 150% - the impending recession might demand a similar response from central banks.

- The US Federal Reserve may be forced into financial easing considering elevated debt levels and financial stress, strengthening the case for gold in portfolios.

In times of economic uncertainty and recession, investors often turn to safe-haven assets like gold to protect their portfolios. While protection is an admirable goal, with the right conditions, gold can do far more than simply safeguard a portfolio. Not all recessions are created equal, and the one we are rapidly approaching will be a devious combination of economic weakness piled on mountains of debt with naggingly high inflation and a backdrop of geopolitical stress, not to mention tension in the banking industry. In these types of recessions, central banks have little choice but to preserve financial stability and government solvency with accommodative interest rates and abundant quantitative easing.

We only have to look fifteen years back to the global financial crisis and the US Federal Reserve's (Fed) response to see gold's impressive reaction in an eerily similar recessionary environment. The global financial crisis shattered equity and real estate values while gold climbed precipitously. Gold didn't just provide stability but rather impressive gains for those with material allocations. Sly investors then used gold as funding to pick up quality assets at bargain prices. Currently, the Fed is raising interest rates while simultaneously warning of an impending recession. All the while, bank balance sheets and federal budgets are buckling under the pressure of higher interest rates. Economic weakness will make the situation overwhelmingly unsustainable. It's not clear in which direction it will crack exactly, but the odds look increasingly advantageous that gold will once again be one of the few big winners as the predicted recession unfolds.

Gold may provide far more than stability in the possible upcoming recession

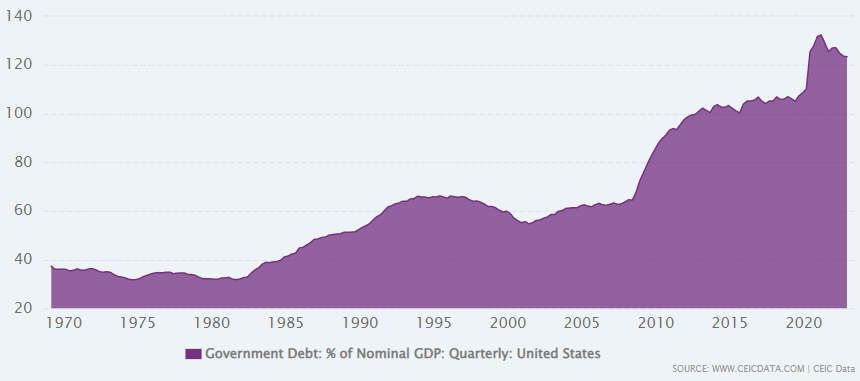

Let's rewind to October 9th, 2007, when the S&P 500 peaked before the onset of the global financial crisis. At the time, US government debt to GDP was around 63%, and the US government budget deficit was about $161 billion, or 1.2% of GDP. The Fed gradually raised interest rates in an effort to cool off the economy and combat inflation (which sat close to 2.5%) until September 2007 when rates hit 5.25%, the highest level seen in many years.

It's unlikely any investor would be relatively concerned about those metrics today with US government debt to GDP essentially double at over 120%, coming out of 2022 with a deficit of $1.4 trillion or 5.5% of GDP while the Fed rapidly raises rates to 4.75% - 5.00% to fight inflation that is essentially twice as high as in 2007.

{kind=link}

According to these metrics, it appears that there was significantly less financial stress back in 2007 than exists today, and yet investors likely have clear memories of what unfolded in the years to come. The global financial crisis was one of the most significant economic events of the 21st century. The crisis led to a severe recession that affected the global economy, with many countries experiencing high levels of unemployment, falling asset prices, and bank failures.

During the global financial crisis, the Fed took a number of actions to address the economic challenges facing the country, including lowering interest rates to near zero percent while implementing several rounds of quantitative easing. In total, the Fed's quantitative easing programs during the global financial crisis amounted to over $3.5 trillion in asset purchases, making it one of the most aggressive monetary policy responses in US history.

Gold can be a multi-bagger

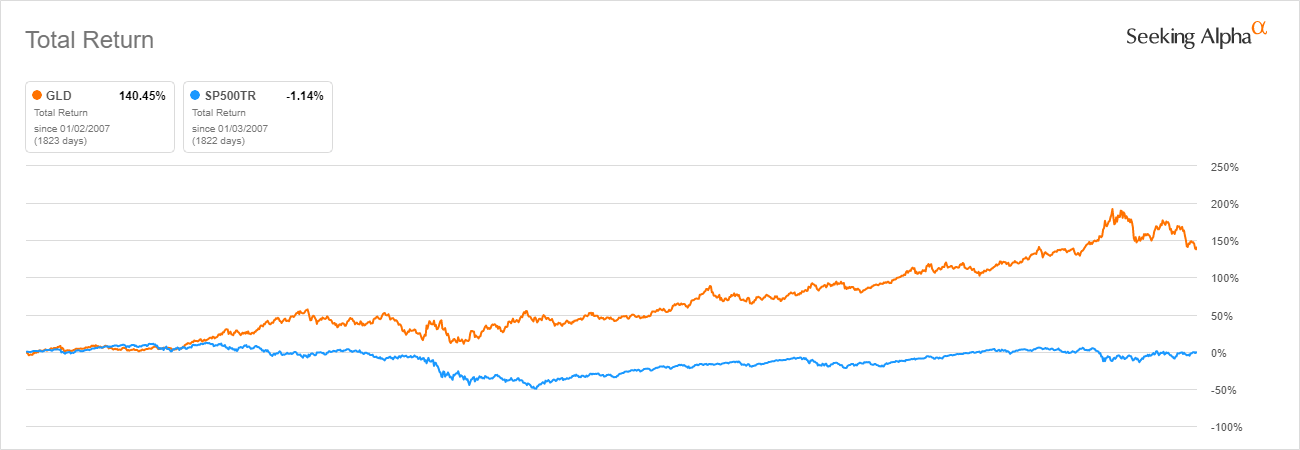

But this article is not about the Fed, it's about why gold may provide impressive returns in the forecasted recession. During the global financial crisis, gold performed exceptionally well as a safe-haven asset. From early 2007 to late 2011, the price of gold increased from around $940 per ounce to over $2,400 per ounce, representing an increase of over 150%. Investors looking for a safe harbor in the storm ended up with a multi-bagger which is even more impressive given the dismal returns of other assets such as stocks during the same period. The chart below uses the SPDR® Gold Shares ETF ( GLD ) as a proxy for gold compared to the S&P 500 from January, 2007, to December, 2011. During the period, there were plenty of opportunities for savvy investors to sell gold at elevated prices to buy equities at a bargain prices.

Gold outperformed equities through the global financial crisis. (Seeking Alpha)

{kind=link}

The Fed itself is now predicting a recession. It might not be another global financial crisis, but it likely won't be a run of the mill recession either. Considering financial metrics and debt levels seem far worse than in late 2007, it's reasonable to assume that the Fed's reaction as well as gold's will be directionally the same as back then, if not even more dramatic. It's admirable that the Fed wants to dampen inflation, but 5% interest rates are untenable for a federal government with over $31 trillion in debt, 13-digit budget deficits, and cracking confidence in the financial system.

Can the Fed really stop gold from rising?

If the US government has to pay 5% interest on $31 trillion or more of debt, interest payments would surpass $1 trillion, overwhelm the budget and dent confidence in financial stability. It might get even worse with debt set to continue its steep rise following a budget deficit of over $1 trillion in just the first six months of this fiscal year. Interest rates must come down quickly or the government will have to search far and wide for new financiers to cover its growing interest expense, not to mention its sizable deficits. But comfort in owning US government debt is certainly waning following the immobilization of Russia's USD reserves and the inherent threat to other entities holding US bonds. Foreign governments and central banks were long a reliable buyer of US government debt, but times are changing as reserves, at least incrementally, are shifting to other options such as gold. Just last year, central banks purchased 1,136 tonnes of gold , the highest amount since 1967. The US government is at risk of asking for the check and finding it has no way to pay it. Unless, of course, the Fed comes to the rescue once again.

The government seems to need a long period of time with negative real interest rates (with interest rates below the rate of inflation) to inflate its way out of the debt issue, a backdrop that generally favors gold. The last time the US government and the Fed experienced a similar situation of elevated debt levels and troubling inflation of such magnitude was in the 1940s and 1950s following World War II, and they tackled the issue through yield curve control and letting inflation run hot for many years. Interest rates were held down by the Fed through asset purchases, while the purchasing power of cash and bonds withered away. It's unlikely that it will play out the same this time around, but Fed actions continue to indicate more easing is the most likely outcome. After slashing interest rates and buying trillions of dollars' worth of government-backed bonds during the pandemic, which coincided with the government running large deficits and sending stimulus checks to citizens, the Fed started talking tough about controlling inflation and attempted to shrink its balance sheet. It seemed to be going smoothly until Silicon Valley Bank decided to crash the party, and the Fed quickly reverted to growing its balance sheet.

The message is rather clear. At the first sign of financial instability, the Fed will likely be there to inject confidence. Afterall, someone will need to foot the bill for a desperately indebted government staring a recession in the face.

Inflation is notoriously difficult to predict, but it's clear that risks are high for continued financial stress, money printing and the debasement of fiat currencies. Should central banks' balance sheets resume their long-term upward trajectory, there is little doubt this would push the nominal price of gold to new all-time highs.

Gold is money, but it's not without risk

Essentially all currencies lose value relative to gold over time. Even the mighty US dollar has lost roughly 90% of its purchasing power since Nixon severed its link to gold in 1971. In that sense, gold is the obvious long-term winner in the currency race. In fact, gold is often considered the only true money. As J.P. Morgan stated in his testimony before Congress in 1912, "Gold is money. Everything else is credit." The physical properties which make gold a suitable store of value are well known. It is an element that is chemically inert, and thus endures the passing of time. It has few economic applications, giving it independence. And most importantly, it is adequately scarce. As Henry Hazlitt wrote , "The great merit of gold is precisely that it is scarce; that its quantity is limited by nature; that it is costly to discover, to mine, and to process; and that it cannot be created by political fiat or caprice." Thus, over time, the quantity of gold above-ground has increased at approximately the same rate as the world's population. And as a result, it represents a constant, which enables it to be a store of value and to price everything around it in terms of that constant.

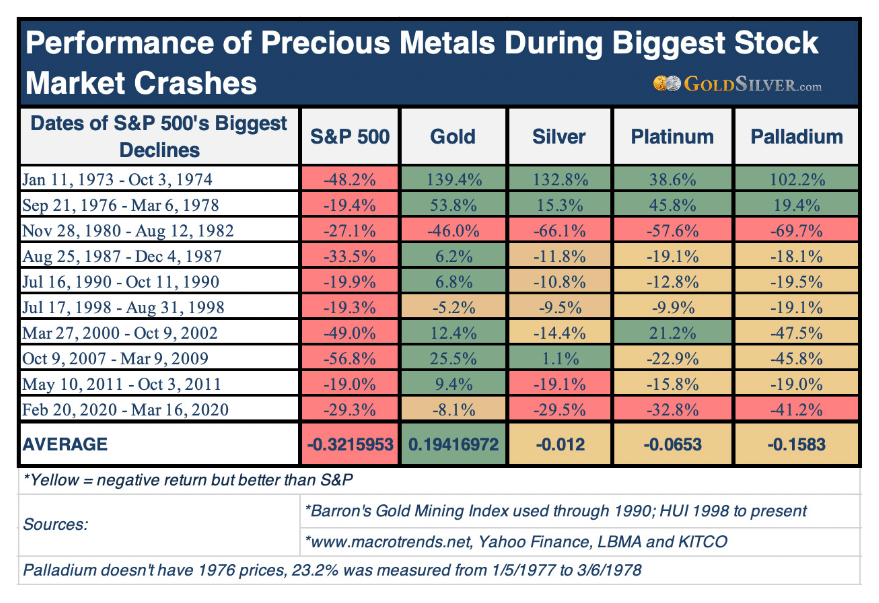

Gold's resume as a store of value also rhymes with its habit of outperforming just when equity investors need stability. Gold's relative performance and its ability to hedge portfolios during stock market crashes should not be ignored, as demonstrated by the chart below displaying the performance of gold (and other precious metals) during the S&P 500's largest declines since the 1970s:

Performance of precious metals during the biggest stock market crashes. (Strategic Wealth Preservation)

{kind=link}

History shows that gold typically does very well during stock market crashes, both in absolute and relative terms. And of the three times gold fell, for two of them the magnitude of the drawdown was much less pronounced than the S&P 500, and the only one greater was just after gold's biggest price rise in history.

Gold's qualities as a store of value and hedge in difficult equity markets should be argument enough for investors to hold a material position in the metal, even if the possibility of substantially greater outcomes in the predicted recession does not materialize. But asset allocators seem to have forgotten about gold's attractive attributes after many decades of disinflation and declining interest rates. As precious metals expert Rick Rule often points out, the market share of Gold currently represents only about 0.5% of total savings and investment assets in the US versus a four decade median between 2.5% and 3%. A simple return to the mean would essentially quintuple the demand for a resource that is rather limited in supply. We all know what happens when rampant demand meets limited supply.

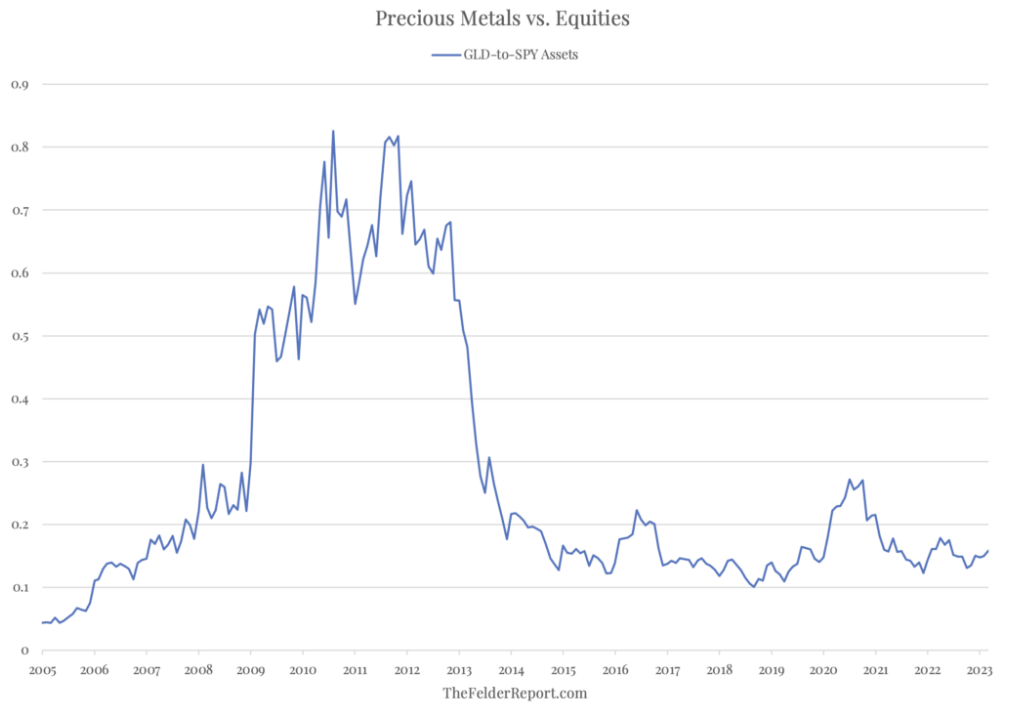

Gold itself doesn't have cash flows, but there are ways to contextualize valuation. Again, using the SPDR Gold Shares ETF as a gold proxy and comparing it to the S&P 500, it is clear that gold is likely reasonably valued when compared with equities.

{kind=link}

So why is there such resistance to owning gold at a time when a recession seems inevitably on the horizon, and it looks under owned and potentially undervalued? There are risks involved with owning gold. The price of gold can be volatile, and there are no guarantees that it will perform well in any given situation. Some will point to nominal yields on bonds as a relative argument for the asset class, even if real yields remain negative. Perhaps asset allocators have been stretching for yield in other places due to low interest rates? The price of gold can easily be affected by factors that are notoriously hard to predict, such as inflation and interest rates or changes in the value of the US dollar.

Investing directly in gold can also be tricky. Physical gold must be stored securely, which often comes at a cost. The risk of theft or confiscation is hard to eliminate completely. Despite the challenges, we invest in precious metals predominantly through physical holdings stored in our home country of Switzerland. For many, financial instruments such as exchange-traded funds (ETFs), such as the SPDR Gold Shares ETF mentioned in this article, are an easier option even if they have some disadvantages to physical gold. ETFs have counterparty risk. This means that investors are relying on the financial institution backing the ETF to fulfill their obligations. Some investors, including ourselves, get exposure to gold through gold miners or gold mining focused ETFs such as the VanEck Gold Miners ETF ( GDX ) and the VanEck Junior Gold Miners ETF ( GDXJ ), but these products can be hyper volatile and contain company level risks that are difficult to understand.

Despite the risks and challenges, gold may be the best place to allocate capital considering a possible recession that might include substantial quantitative easing and negative real interest rates.

Beat the coming recession with gold

Gold might be a multi-bagger, a stabilizer or simply a portfolio diversifier and source of funds during the impending recession, but any way the economic difficulty unfolds, investors may be well-advised to hold a material percentage of gold in their portfolios. Gold has a solid track record of being a useful reserve asset that adequately acts as a store of value, as well as a suitable hedge against large drawdowns in the price of risk assets. And during the global financial crisis, it proved it can achieve impressive financial returns in recessions driven by financial stress and treated with lower interest rates and quantitative easing. A 2-5% allocation is better than no allocation at all and would already have a noticeable impact on the risk / return profile of any portfolio, but investors convinced of gold's potential in the current economic backdrop, as we are, go well beyond that with allocations in excess of 20% of assets.

Our preferred way to own gold is to own the physical metal, but we recognize that this is not always practical for many investors. Instead, many chose to gain exposure to gold via ETFs such as the SPDR Gold Shares ETF, which is the world's largest gold ETF. Other gold ETFs exist, and interested investors should research their relative strengths and weaknesses (including liquidity, counterparty risk, certification of gold ownership to match the fund's assets, geographic location of storage and others). As a much smaller complement to owning physical gold, we also own gold royalty companies such as Franco-Nevada ( FNV ) and a diversified collection of miners via the VanEck Gold Miners ETF ( GDX ) and the VanEck Junior Gold Miners ETF ( GDXJ ).

With central banks and government finances under pressure and cracks emerging in the financial system, we view the skew of risk regarding gold to be heavily to the upside. Even if a dramatic rise in the price of gold fails to materialize through the next recession, we feel confident in its ability to improve portfolio performance and to provide liquidity to buy assets at bargain prices. Do you own gold?

Editor's Note: This article was submitted as part of Seeking Alpha's Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

GLD: Why Gold Should Be Your First Portfolio Pick In A Recession