GLO - GLO: An Interesting Speculation

2024-01-21 03:34:04 ET

Summary

- Clough Global Opportunities Fund is a closed-end fund trading at a deep discount; the fund invests in equity and fixed-income securities globally.

- The fund has a lackluster historical performance but offers a managed distribution policy that can attract yield investors.

- GLO has reduced its leverage substantially, and while it appears it was done at the wrong time, the more mild leverage I would view as a positive.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Clough Global Opportunities Fund ( GLO ) remains a deeply discounted closed-end fund that takes a hybrid investment approach. They'll invest primarily in equity securities but also can include fixed-income exposure. In addition, they aren't constrained to any specific region around the globe. Finally, they take the flexibility even further and will also include short positions.

This has all culminated in a really lackluster, mediocre historical fund performance, and that might be too high a praise. The fund has barely performed positively in the last decade and has produced losses in other annualized standard timeframes.

However, the 10% managed distribution policy can often garner yield investors' attention, and that has tended to be able to get the discount to the net asset value per share to narrow on occasion. That's especially true from where it is currently. Right now, it is at an attractive discount on an absolute and relative basis. That's what prompted me to take a position early last year initially, and I remain in the position.

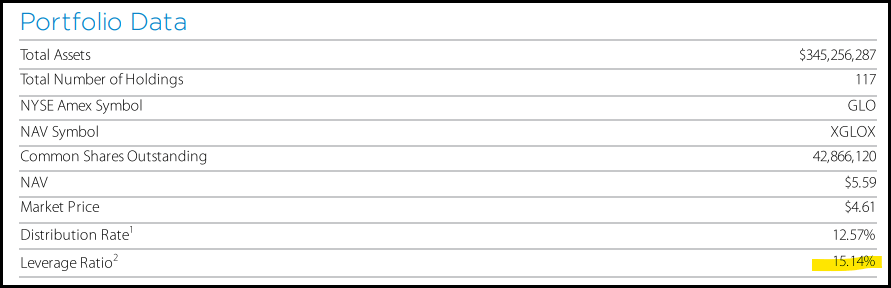

GLO Basics

- 1-Year Z-score: -0.94.

- Discount: -18.28%.

- Distribution Yield: 12.46%.

- Expense Ratio: 2.36%.

- Leverage: 15.14%.

- Managed Assets: $403.7 million.

- Structure: Perpetual.

GLO's investment objective is "to provide a high level of total return." The fund attempts to achieve this by "applying a fundamental research-driven investment process and will invest in equity and equity-related securities as well as fixed-income securities, including both corporate and sovereign debt." They also include that the fund will "invest in both U.S. and non-U.S. markets."

Leverage And Performance

In 2022, when everything was collapsing in terms of asset classes across the board, GLO was doing atrociously. That caused the fund's leverage ratio to skyrocket, and that's when I initially noted that it would become even more difficult for the fund to come back. Deleveraging then did end up happening, as expected, and today, they even took leverage down more aggressively.

As of their last annual report for the period ended October 31, 2023, the fund had $52 million in borrowings. That's down from the fiscal year-end of the 2021 year when it came in at $245.5 million, and from the 2022 FY, when it was at $204 million. However, through most of this period, the fund still was carrying a higher level of leverage, and that pushed the fund's total expense ratio to 5.71%.

As of their last fact sheet, which shows data as of the end of November 30, 2023, it would appear they remain only lightly leveraged due to a leverage ratio of 15.14%.

{kind=link}

In a higher rate environment, I view this as a positive, as the cost of borrowings really ramped up when the Fed was aggressively raising rates. GLO pays at a rate of OBFR plus 0.90%. It remains elevated today. Going forward, rates are expected to come down. In this case, GLO is in a position where they can always add more leverage later.

With all that being said, with a year-end of October 31, 2023, it would appear they once again took the wrong step and deleveraged nearly at the wrong time. It was just in time to miss the massive rebound that we had through November and December 2023 across the board. Though this was a process, as we noted previously, they were taking down leverage; in their last N-PORT for the period ended July 31, 2023 , they had borrowings down to $112 million. So it was a work in progress to get there, and the leverage wasn't all taken down right in October.

That was the reverse of heading into 2022 when they were highly leveraged, and that negatively impacted them. Not being leveraged or overly leveraged in the wrong periods so far is where we come up with the types of annualized performance we can see listed for this fund.

{kind=link}

2022 was the worst year for the fund in the last decade, and that certainly did a lot of heavy lifting for the fund to push these results to where they are today. Prior to that, we would have seen vastly different annualized performance results, but that's really all it takes: one really bad year.

2023 looked a bit better in the end, but it wasn't nearly enough to recover from the prior year's missteps.

YCharts

The fund had one blowout year in 2020; it put up results over double what the S&P 500 Index itself provided. That's what really helped significantly boost the distribution at one time. Since then, they haven't been able to capture that magic again.

Still, I believe that the discount on the fund is attractive regardless, and that is why I'm willing to speculate. It's trading well below its long-term historic discount level. This could also be reasonably expected as CEFs across the board are at some of the deepest discounts we've seen going back for decades.

YCharts

On another positive note, the fund noted in the last report that they had begun repurchasing shares. Nearly all CEFs have a repurchase authorization, but actually utilizing it is a whole other thing. In this case, they repurchased 679,602 shares in the last fiscal year. The total shares outstanding at the end of the year were 42.866 million for some perspective. When shares are repurchased at a discount, that is accretive to the NAV.

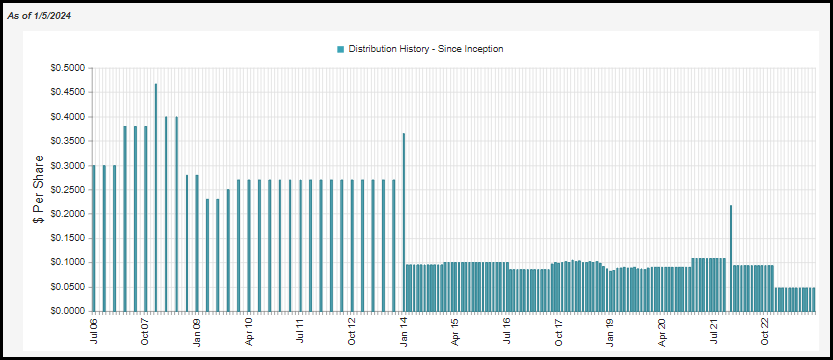

Distribution - Managed 10% Policy

On another potentially positive note, the fund was able to about earn its distribution in 2023 despite the above-mentioned missteps. This can be an important note because the fund has a policy whereby they reset the distribution annually to 10% of NAV.

After that strong 2020 performance, that's when we saw the fund garner more interest after being able to raise the payout substantially based on its distribution policy. It also resulted in the fund being pushed to a premium for a brief period of time, as we saw in the chart above.

{kind=link}

Assuming they go through with this policy once again this year as they have done the prior several years now, that would mean the distribution adjustment should be fairly minor. To be more specific, the fund takes the average NAV of the last 5 trading days of the year and then uses 10% of that divided by 12 for the monthly amount. Therefore, we are looking at a distribution that should be around $0.0479 per month. ( When announced, the distribution ended up being $0.048.)

For coverage of the distribution, the fund actually produces no net investment income; in both FY 2022 and 2023, we saw a net investment loss.

{kind=link}

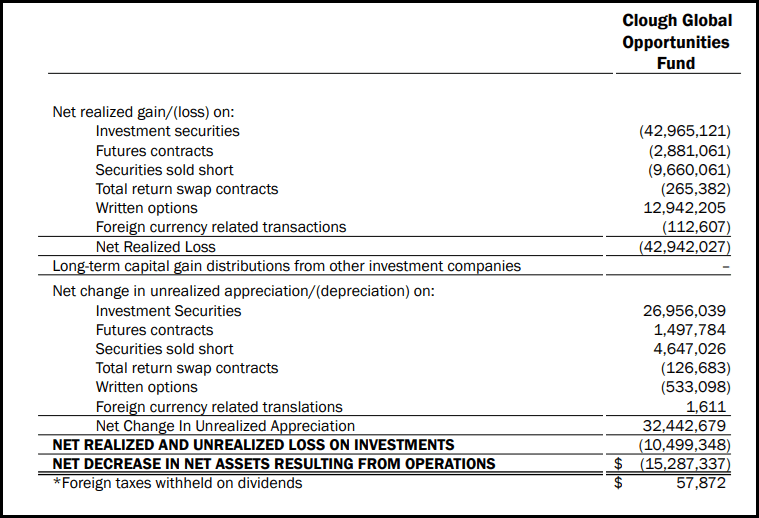

In terms of producing coverage from elsewhere, such as capital gains, the fund didn't see promising results here either. All the flexibility this fund has and the only derivatives to produce a gain were the written options in terms of realized gains.

Though, to be fair, they did have unrealized gains that had offset some of these realized losses. Additionally, this was again quite near the depths of the overall market correction in October 2023. Since then, more of these numbers would have turned positive.

{kind=link}

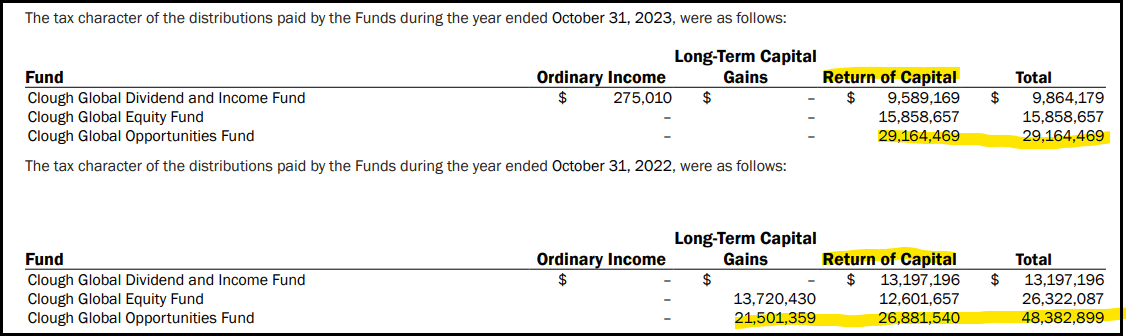

Optimistically, this has meant that the fund's distribution has been primarily a return of capital for both of the prior years. For FY 2023, the entire distribution was classified as ROC.

GLO Distribution Tax Classifications (Clough (highlights from author))

{kind=link}

This is one of those scenarios where there were losses in the FY that generated what could be considered non-destructive ROC since, for the calendar year 2023, the fund really did just about earn its payout. The fund is also sitting on a massive pile of short and long-term non-expiring carryforward losses. That can mean that ROC distributions can continue, at least in some portion of the payout, for a number of years even if the fund 'earns' its 10%.

This can be a positive as investors aren't paying taxes on these distributions in the year received but can defer them essentially. This is because ROC distributions reduce an investor's cost basis. So, at the time of selling, assuming you sell them above your cost basis, only then would taxes be due.

GLO Tax Loss Carryforwards (Clough (highlights from author))

{kind=link}

GLO's Portfolio

With a high amount of flexibility, it seems the managers really take advantage of this and trade their portfolios like madmen. Albeit it never really worked out to benefit positively, as we saw above, but they certainly are staying busy. The average turnover rate for the last five years comes to 220.6%. That said, this latest year, they took it way down to only 115% - which is still far above most funds. The other outlier was FY 2019, with its high 306% turnover.

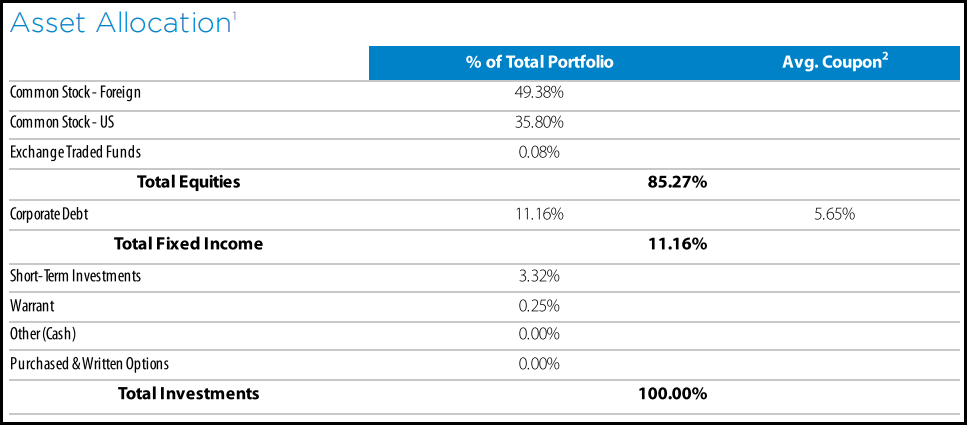

Overall, the portfolio primarily consists of long equity positions in U.S. and foreign companies. With global investments looking relatively cheaper, this isn't a terrible way to invest with some global exposure.

{kind=link}

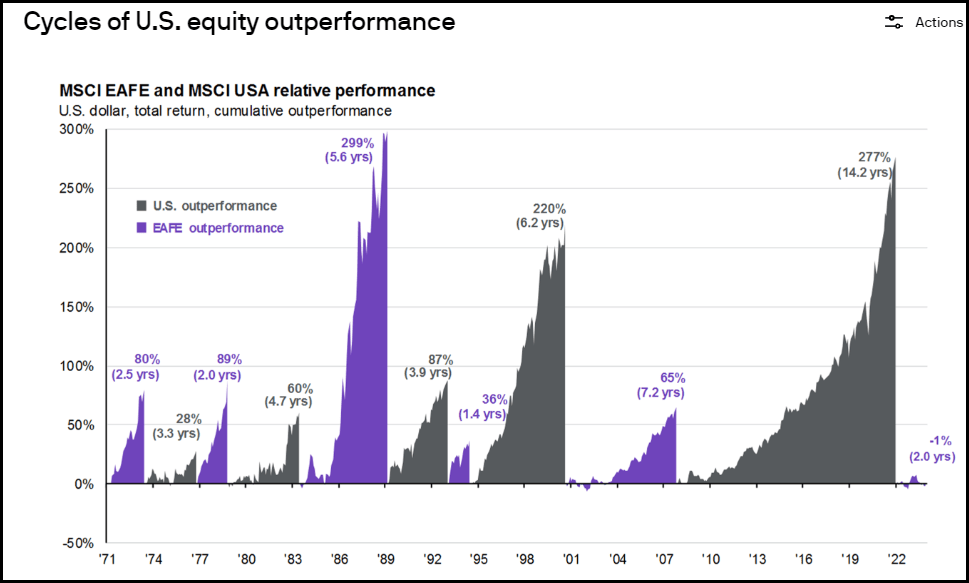

However, global investments have been underperforming U.S. securities for most of the last decade-plus, and that likely contributed to the lackluster historical results of the fund.

{kind=link}

The heavy equity portfolio is also a big change from where they were in our update last year when we saw that the fund had over 51% in fixed-income positions. It was primarily U.S. Treasury notes. Seeing such a dramatic shift probably isn't too surprising, given the fund's incredibly high turnover.

In looking at the geographic exposure a bit closer, we can see that they are shorting primarily U.S. positions, and that, on a net basis, takes some of the exposure down. They also list U.S. multinationals, which are defined as those companies that are located in the U.S. but actually earn over half of their revenue outside of the country.

GLO Geographic Exposure (Clough)

To look at the fund's latest allocation in terms of sector, we can see that they are long on consumer discretionary and information technology. However, on the flip side of this, they are also shorting the consumer discretionary sector the most.

GLO Long/Short Sector Exposure (Clough)

In looking at the fund's top equity holdings, we have several of the Magnificent 7, which proved to be valuable throughout 2023. It probably no doubt helped contribute to the fund's positive performance for the year.

Despite the high flexibility of the portfolio, it should also be noted that the fund is running a fairly concentrated portfolio at the same time, with these top ten positions comprising almost 40% of the fund. CEFConnect lists the number of total holdings at 100.

GLO Top Ten Holdings (Clough)

Although similar to overall portfolio construction, these positions have been quite different in prior updates. The high turnover generally means that the portfolio is relatively more opaque than other CEFs. CEFs don't often have the most updated information in terms of their holdings that ETFs do, which can have daily updates. Instead, we are generally lucky when a fund provides monthly updates. So when a fund like GLO can turn over its portfolio entirely once, twice, or three times in a year, some drastic changes can take place in a month or a quarter's time.

Conclusion

The fund has made all the wrong moves at all the wrong times and runs a highly flexible portfolio of investments that haven't amounted to much aside from one really strong year. I'm not sure the outlook looks different going forward due to continuing their long/short approach. I have never been a fan of long/short funds because the management has to be right more than they are wrong consistently, as one side of the portfolio is often losing if the other is winning. A rising tide lifts all boats, and that's why shorting can be extremely tricky to do regularly.

Short seller Jim Chanos himself capitulated last year, closing down his hedge fund that continually underperformed because the market always wants to go higher.

That said, the higher distribution rate can still have some appeal to drive income investors into the fund. Along with the deep discount, I remain invested in this as a speculative position. Even if the portfolio continues with a mediocre underlying portfolio performance, if we can just get a bit of discount narrowing, we'd see some fairly reasonable results anyway.

Finally, if we go down with this sinking ship, the manager himself, Charles Clough JR, will be going with us. He owns over 260k shares and has made purchases 5 times throughout 2023 - as well as other insiders buying.

For further details see:

GLO: An Interesting Speculation