GLO - GLO: Disappointing Leveraged CEF

2023-07-30 04:22:10 ET

Summary

- Clough Global Opportunities (GLO) has underperformed in an up-market, with only a 7% return compared to the 16% and 19% returns of VT and SPY.

- GLO holds mostly U.S. equities and has a high turnover ratio, indicating a trading-focused strategy rather than buy-and-hold.

- The CEF's high leverage ratio and high cost of funding are contributing to its underperformance, and it is trading at a large discount to NAV.

- The fund will not outperform until Fed Funds come down, and the manager moves towards a buy and hold strategy.

Thesis

Clough Global Opportunities ( GLO ) is a global equities-focused closed-end fund with a high leverage ratio. With the markets up significantly this year, we wanted to re-visit GLO and see how it fared. Leverage amplifies performance, and usually in an up-market a high leverage ratio results in a high octane performance. Not here:

With the Vanguard Total World Stock ETF ( VT ) up 16%, and the S&P 500 ETF ( SPY ) up 19%, we would have expected GLO to post a return in the 20s. It has not been the case. In this article we are going to look at GLO's build, its detractors and its future estimates.

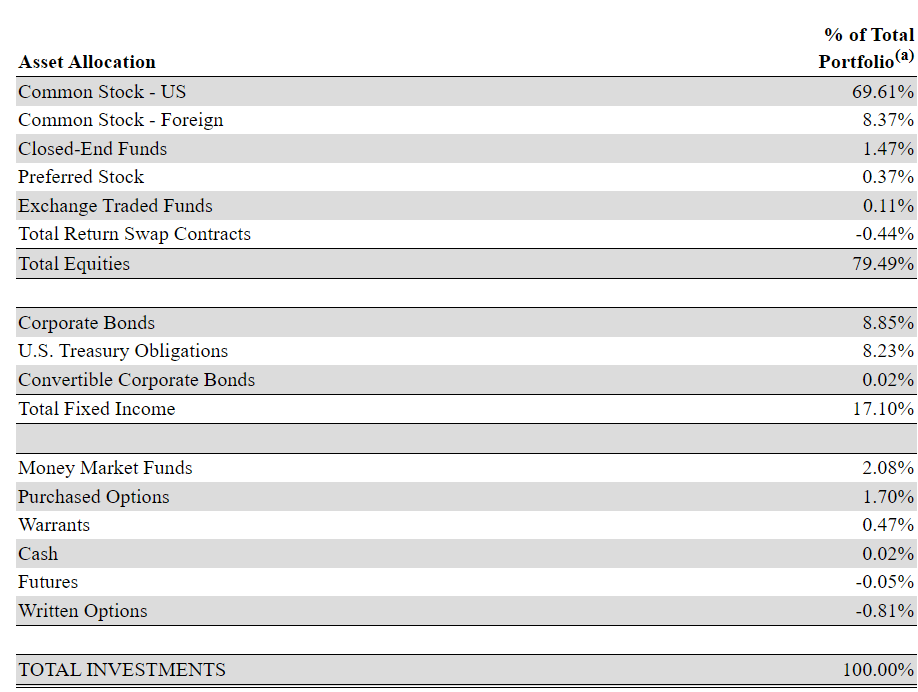

GLO Holdings

The CEF holds mostly U.S. equities:

{kind=link}

We can see the CEF having 2 distinct sleeves:

- An Equity Sleeve - composed of both U.S. and Foreign Equities

- A Fixed Income Sleeve - composed of Treasuries and Corporate Bonds

The fixed income sleeve is used to generate cash-flows and is fairly conservative, with half of the sleeve allocated to treasuries. On the equity side, the main risk factor is constituted by U.S. equities. When we look into detail, we notice the following top holdings:

Top Holdings (Morningstar)

Many of the top holdings in the fund are large, tech mega-caps that have posted an outstanding performance this year. So what happened?

Turnover (Morningstar)

If we look at the available data for the portfolio turnover, we can see an extremely high turnover ratio. That translates into a strategy that is more geared towards trading, rather than buy-and-hold. To that end, even if the fund contains Microsoft right now, and Microsoft has had a stellar performance in 2023, we do not know when it was purchased. It is highly likely the fund did not have a full 4.4% allocation to the name at the beginning of the year. CEFs with extremely high turnover ratios are more of 'mini hedge-fund' type of instruments rather than proper value creators.

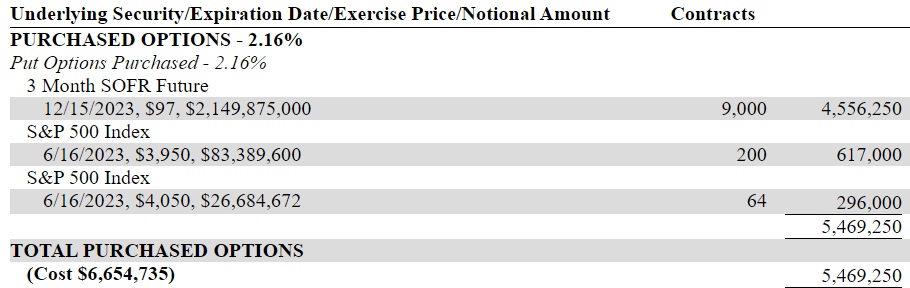

The fund also engages in options trading, owning some SOFR and SPY positions as of its latest Semi-Annual Report :

{kind=link}

The SOFR futures position can be used speculatively or for hedging (for its fixed income sleeve), whereas the SPY put options look more of a hedging play for the equity portfolio.

Reasons Behind the CEF Underperformance

1. High Cost of Funding

This CEF has a 37% leverage ratio, entirely achieved via debt (either revolving bank facility or TRS). The cheapest way of securing funding is via preferred equity for CEFs. This allows a fund to lock in attractive term rates during low interest rate environments. Even if rates subsequently rise, the preferred equity maintains the same cost of funds. Unfortunately, GLO did not issue any preferred equity. With Fed Funds now above 5%, the fund is paying away a significant amount for its leverage

2. High Turnover Strategy

When looking at this CEF's portfolio, at the first glance all seems well. The top names are tech mega-caps, and these names have done tremendously well this year. Unfortunately, when digging into the details it becomes clear this name does not buy-and-hold, but trades extremely frequently. Market timing is impossible, and more importantly, this type of strategy is not readily quantifiable. When a fund trades alot of its portfolio, an investor ends up relying more and more on the trading acumen of the portfolio manager rather than standardized risk factors.

Premium / Discount to NAV

The CEF is trading at a large discount to NAV:

Historically, the fund has traded at discounts to NAV in excess of 10%. The only time when the CEF was flat to its actual net asset value was during the zero rates environment of 2020/2021. We expect the current discount to persist as long as the fund is highly leveraged and the cost of funds is high.

Fund Forward

As long as rates stay high, this CEF will incur very significant leverage costs, which will drag it down. Furthermore, unless the portfolio manager changes his modus operandi, we are going to have to rely on moments of trading brilliance to make up for a high churn strategy:

While the S&P 500 is close to recouping most of its 2022 drawdown, GLO is still far off from breaking even on a three year look-back. For GLO to do well, rates have to come down, and the market needs a constant upwards trajectory. We fail to see those two factors occurring together in the next twelve months. Rates will stay higher for longer in our opinion, especially in light of the strong economic data as of late, and the 'soft landing' narrative.

Conclusion

GLO is an equity closed-end fund. The vehicle focuses on global equities, but also contains a small fixed income sleeve. This CEF is an extremely leveraged vehicle, with a 37% leverage ratio. Buying equities with debt results in an amplification of returns, both on the upside and on the downside. This CEF had a very difficult 2022, being down -44%. Despite the substantial run-up in equities this year, GLO is severely lagging, being up only 7%. The factors behind this poor performance are represented by the high cost of debt for the fund and its high churn ratio (the portfolio turnover here is extremely high). This CEF will not be able to outperform until rates will come down substantially, and the manager moves back towards a more value creating buy-and-hold strategy. At the current juncture, a retail investor is best served to Sell this name.

For further details see:

GLO: Disappointing Leveraged CEF