GB - Global Blue: This Forgotten Market Leader Could Be Set To Double

2023-12-24 11:44:38 ET

Summary

- Global Blue is a market leader in tax-free shopping refunds, with a 70% market share and long-standing relationships with retailers.

- The company has experienced strong business recovery and momentum, with revenue and operating margin surpassing pre-COVID levels.

- The rebound of Chinese tourism could further boost Global Blue's figures, although reduced spending by Chinese tourists is a potential concern.

- The stock is very attractively valued if the company can deliver lower end of its financial guidance in three years, and the stock could be set to double.

Global Blue ( GB ) is a company indirectly exposed to international travel and luxury goods. It is a clear market leader in its two primary businesses and has a new growth vertical. Global Blue is partly still in recovery from the rough years of pandemic. However, its revenue and operating margin have already reached beyond pre-covid levels and the rebound of Chinese tourism could propel the figures even higher. This appears to have gone unnoticed by the market.

The company has an attractive business model, experienced management team and concentrated ownership with names that can enable it to thrive. The business is performing strong and the company is turning back to profit on an adjusted basis. Meanwhile the stock trades at an attractive forward based multiples, at a lower valuation than the largest owners have paid for their stakes.

A trusted intermediary between three parties

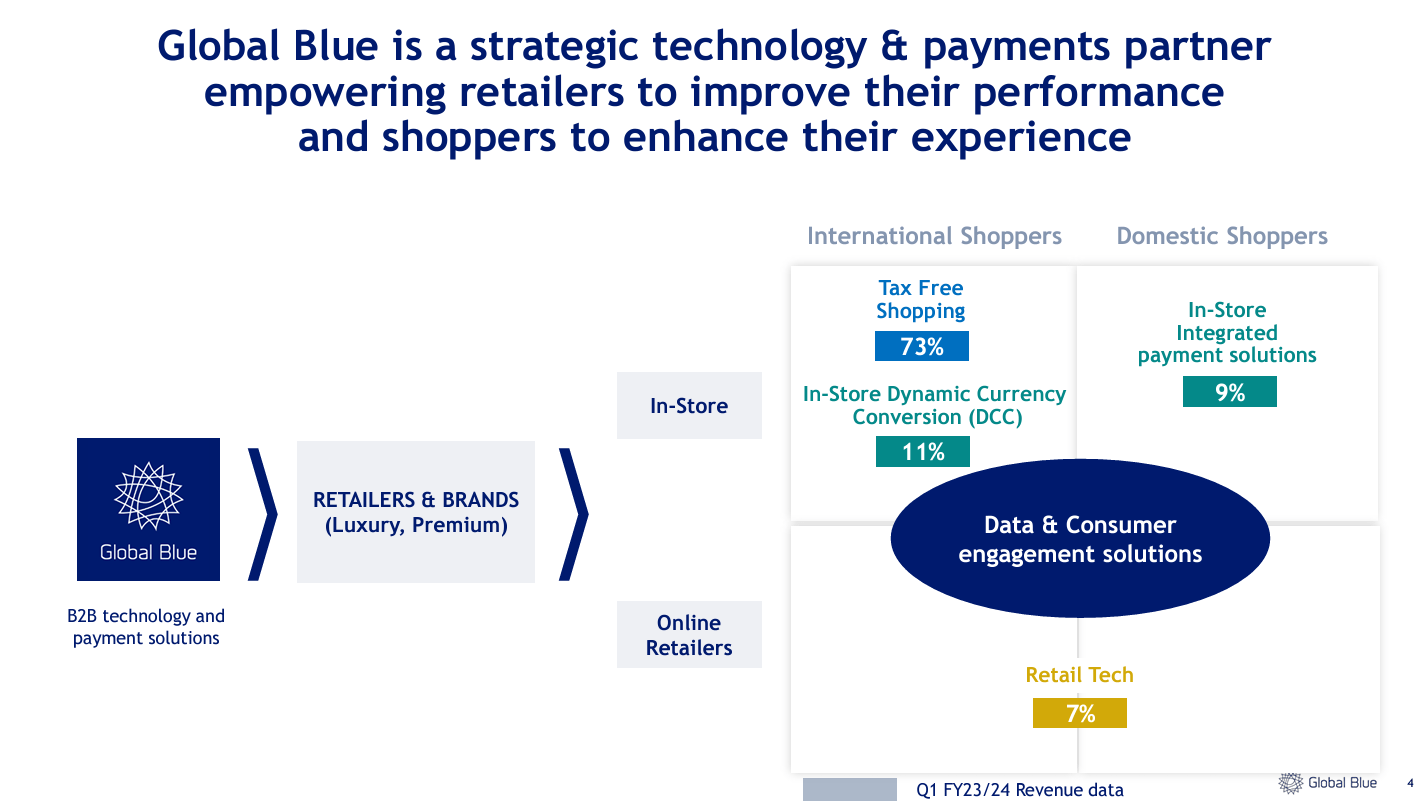

Global Blue, or Global Refund by its former name, is known for enabling international travelers to do tax-free shopping. The company was founded in 1980. Its service is available at over 300 000 points of sale in over 40 countries. Global Blue is a link of convenience and trust between three parties: consumers, retailers and customs and tax authorities. Global Blue enables consumers to save and retailers to earn more.

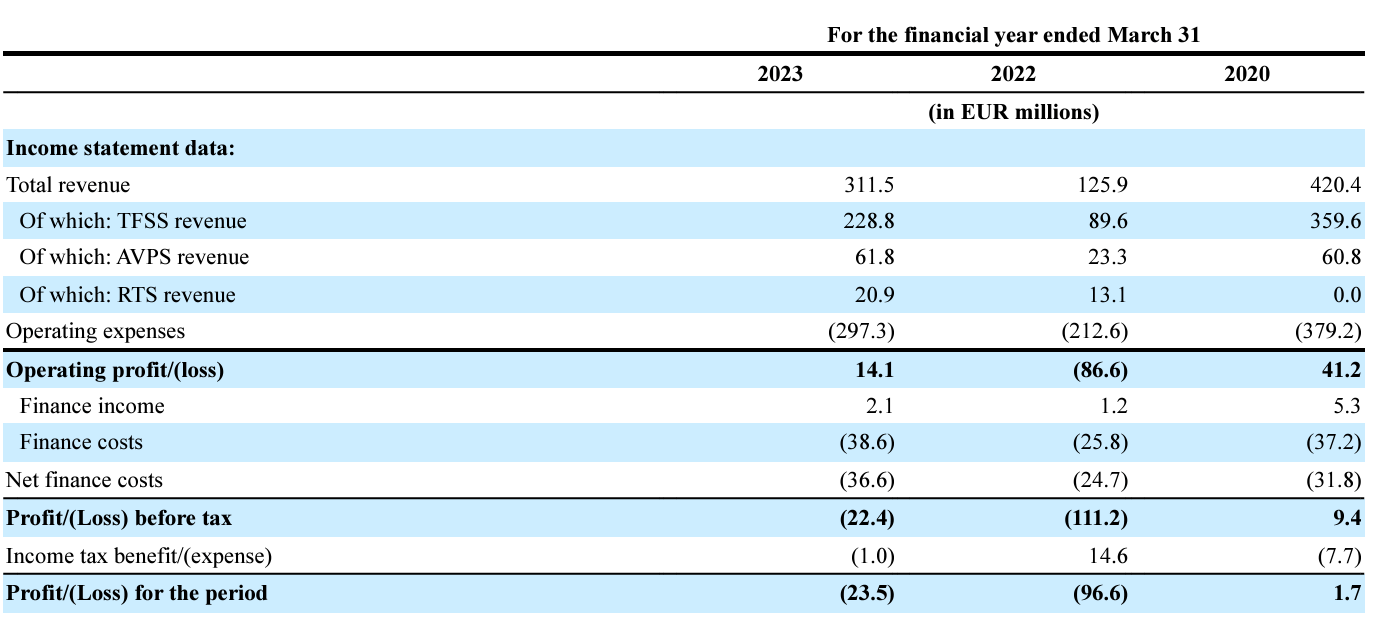

In 2022 Global Blue had revenues of €311 million and 1800 employees, a majority (85%) in the EMEA region. Its largest countries by sales were Australia, France and Italy. The company is headquartered in Switzerland. The shares of Global Blue have been listed since August 2020. Its market cap is approximately one billion and enterprise value 1.5 billion dollars.

The businesses of Global Blue. (Company presentation)

{kind=link}

By using Global Blue service the consumer can redeem the value added tax in an easy and convenient manner instead of going through the bureaucracy with the customs. In return Global Blue charges a commission which it splits with the merchant. Typically the commission is 30% of the VAT amount.

Global Blue is a clear market leader with a 70% market share in the tax-free shopping segment. The company has long customer relationships with the merchants spanning over 20 years on average. Its customers are retail names such as Bottega Veneta, Audemars Piguet, Lacoste, which are all its latest new customers.

In addition to Tax Free Shopping Solutions (TFSS) has two other operating segments: Added Value Payments Solutions (AVPS), including Dynamic Currency Conversion (DCC), and Retail Tech Solutions (RTS), which comprises many of the recent acquisitions. A consumer faces a DCC solution for example at an international airport, where the payment terminal asks if the buyer wishes to pay in his or her home currency. Here, Global Blue claims leading market position too.

Global Blue’s RTS segment offers new technology solutions to retailers, including digital receipts, eCommerce returns, and an exclusive delivery experience, that can be easily integrated with their core systems and allow them to optimize and digitalize their processes throughout the omni-channel customer journey, both in-store and online. -Global Blue, 20-F

Financial development over three fiscal years. (20-F)

{kind=link}

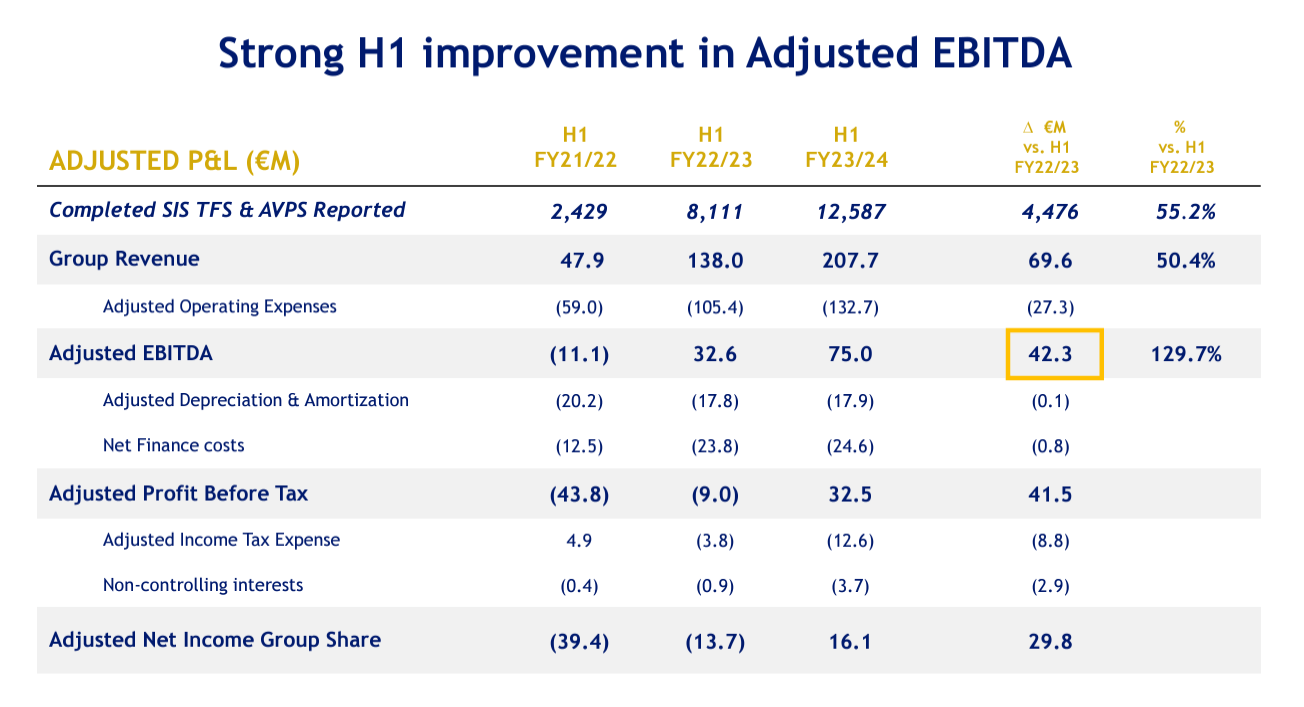

Strong business recovery and momentum

In the H1 of the current fiscal year its revenue increased by 50% and adjusted EBITDA by 130%. In the latest quarter the speed slowed down with growth rates of 38% and 83%. The growth is a result of primarily TFSS segment (76% of revenue) but supported by all other segments.

Financial development in H1. (Company presentation)

{kind=link}

As a result Global Blue’s business has already recovered beyond pre-covid levels despite the significantly lower number of Chinese and Russian tourists in Europe.

Quarterly financial development (Tikr)

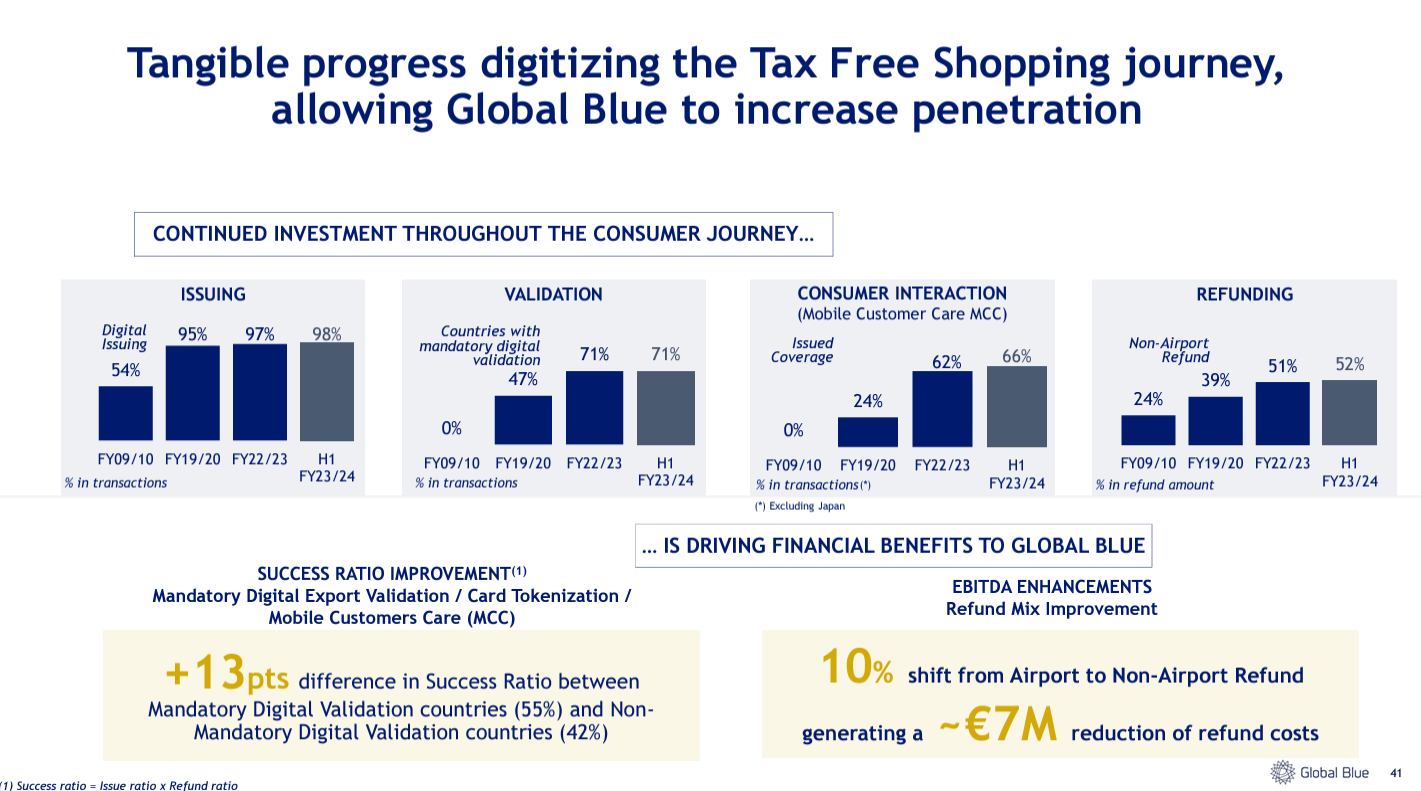

During and after the pandemic Global Blue has invested in its digital capabilities. The investments are partly intended to increase the penetration rate of tax-refunds, since only around 60% of eligible shoppers issue tax-refund forms. Smooth digital processes help to increase its revenues, as more consumers apply for tax-refunds, and decrease costs by streamlined back-end and lower cost of refunding. This trend appears to be persistent, supporting higher margins.

Digital transformation is driving efficiency and increasing sales. (Company presentation)

{kind=link}

An interesting setup with a few shadows

Opportunity to acquire shares cheaper than the largest owners

The ownership structure of Global Blue is relatively confusing and concentrated, it can present both an opportunity and threat to an individual shareholder. Although the picture below, from the company’s latest 20-F, is already outdated, it illustrates the nature of the ownership structure.

Ownership structure of the company in March 2023. (20-F)

Global Blue became a public company as a SPAC by a merger with Far Point Acquisition Corporation sponsored by Third Point Capital and former NYSE President Thomas W. Farley (with 1.4% of the ordinary shares today) at a valuation of $2.6 billion. Being a former SPAC, having no analyst following, small free float and thin trading volumes it is unlikely that the stock receives big interest from institutional investors.

At the time of the de-SPAC, Ant Group, an affiliate of Alibaba (BABA), became a significant owner (6.3%) of the company. The original owners, for example Silverlake Partners and Partners Group remained shareholders and today own approximately 63% and 1.4% of the shares. Silverlake acquired Global Blue for $1.3 billion in 2012.

According to Reuters , Silverlake was looking for a buyer for the company in August 2023. However, in November Global Blue got a new large owner from Tencent who bought a little over 18 million shares or 7.6% share at a price of $5.5 for nearly $100 million.

Half of the shares were sold by Silverlake (approximately 7% of its total holdings) and a few other parties and half of the shares were newly issued. Global Blue intends to use the proceeds to pay down its debt. From this perspective, it appears less likely that Silverlake would find a buyer for the whole company, if not to Tencent itself.

Now, an investor has an opportunity to purchase shares at a lower valuation than the largest owner and a dollar lower than Tencent. Global Blue is soon to produce over two times higher EBITDA compared to 2012, when Silverlake bought the company. Furthermore, in 2021 a private equity investor Advent International acquired Global Blue’s competitor, Planet Payment, with a valuation of €1.8 billion and revenues of $50 million in 2019 according to Fintech Magazine.

Chinese tourism might have changed

The investment case around Global Blue is in a large part dependent on the increasing number of Chinese tourists traveling to Europe and purchasing luxury goods. Global Blue is already missing the Russian tourists left behind the new iron curtain. Although slower than expected by most, due to availability of international flights and constrained availability of visas, the outflow of Chinese tourism has been picking up.

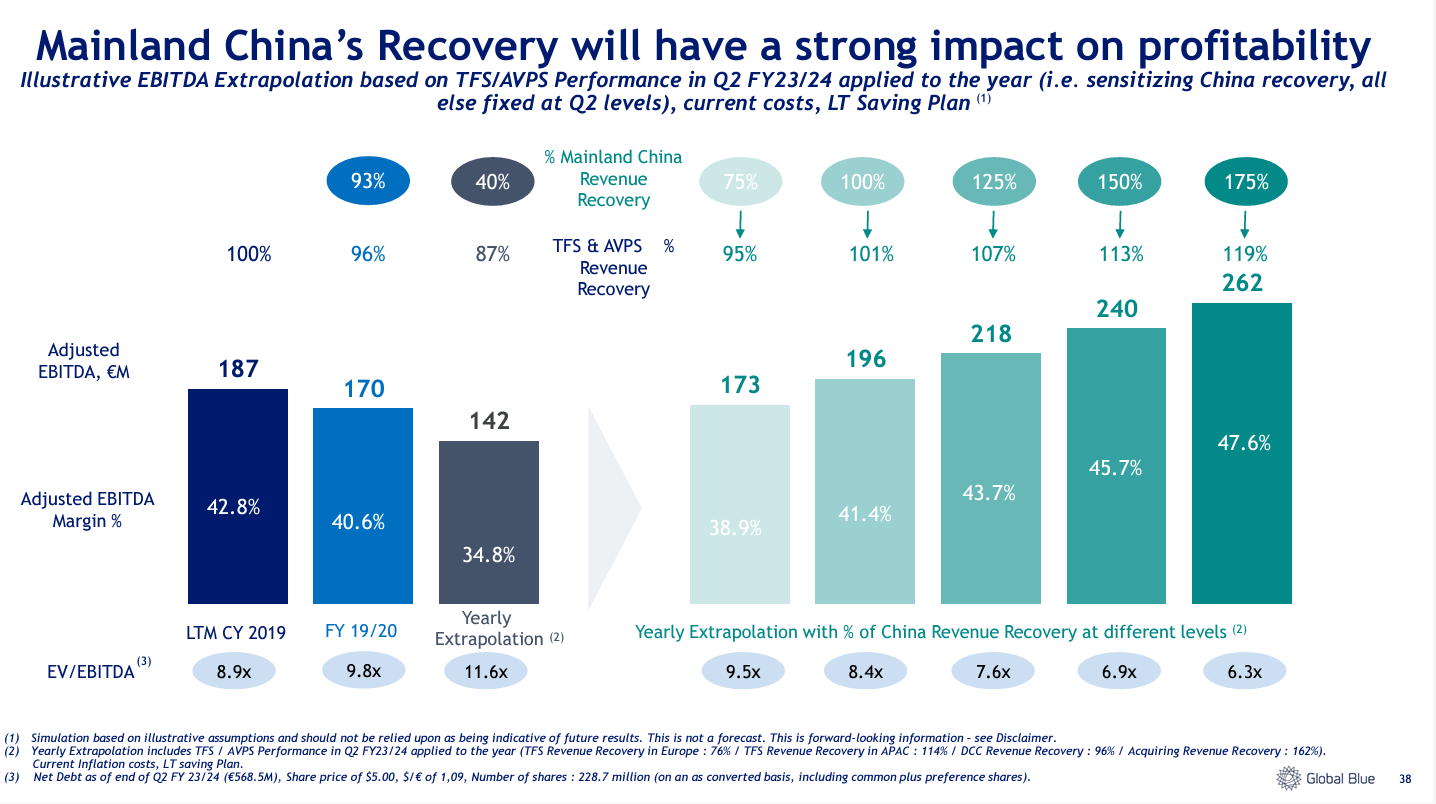

Chinese outbound tourism is important for Global Blue since they are high in numbers and historically also highest spending nationality, twice higher compared to Americans in absolute terms. It appears that the amount of Chinese tourism is generally expected to recover by the end of 2024. The company itself believes in the recovery of Chinese tourism presenting an illustrative impact on its EBITDA generation.

Illustrative impact of Chinese tourism recovery on the EBITDA. (Company presentation)

{kind=link}

However, as featured in recent articles by Wall Street Journal , Reuters and Deutsche Welle , Chinese are traveling but not spending on shopping as much as before. There are competing shopping destinations in China, the outbound travelers are spending more on experiences and cutting back on luxury goods and hotels.

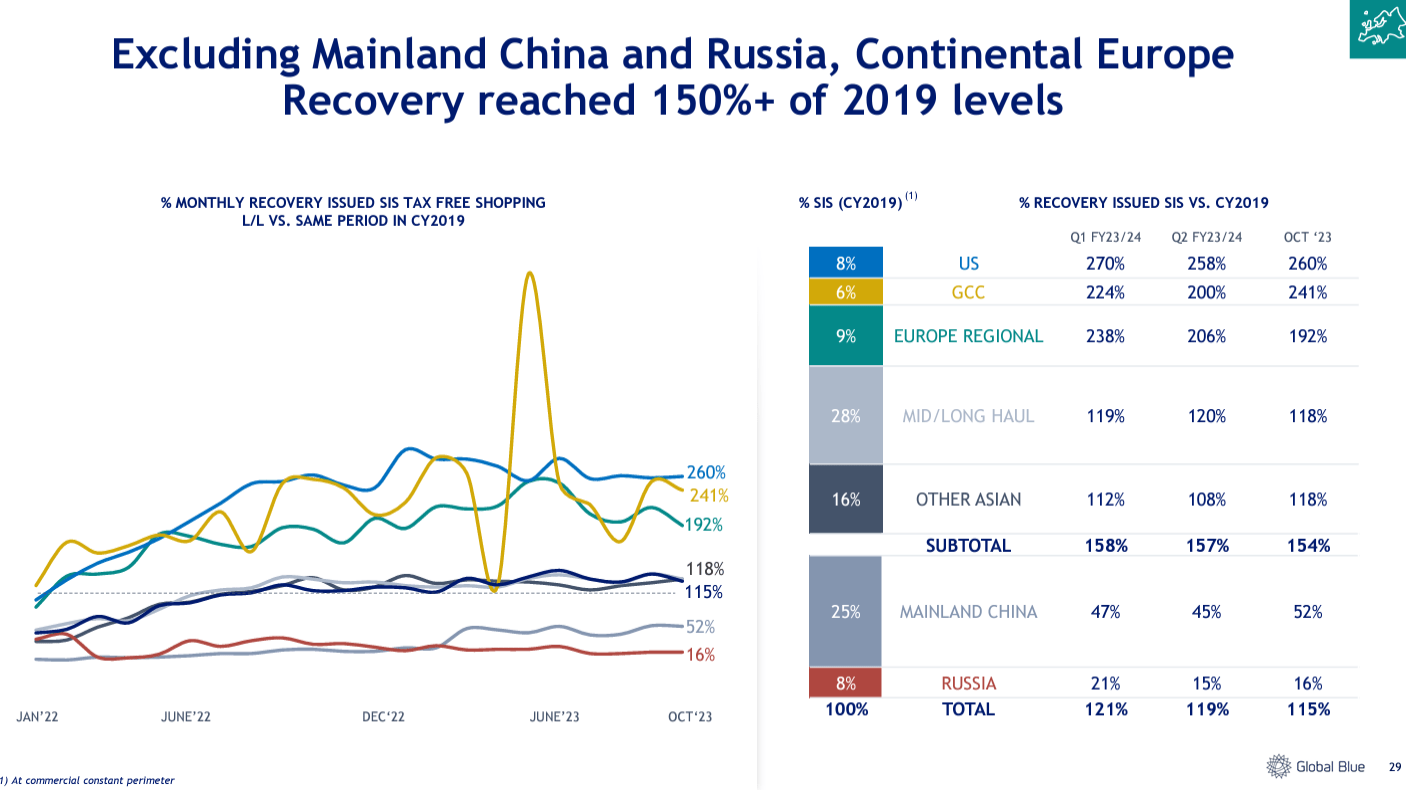

According to DW the reduced spending is a result of the real estate crisis and high youth unemployment. These are probable reasons for why the recovery of Chinese spending is significantly below the average. However, Global Blue's recent business update points to rapid change. In support of company’s expectations, last month the worldwide recovery of Chinese shoppers reached 82%.

In November, the worldwide Sales in Store like-for-like recovery of Mainland China shoppers reached 82% in November vs. 74% in October and 54% in Q2’23. -Monthy tax free business update, Global Blue

Recovery rates compared to pre-covid until October 2023. (Company presentation)

{kind=link}

Debt and inflation could be potential headwinds

Rising prices of international travel and luxury goods represent both a threat and opportunity. The luxury goods inflation has been higher than inflation on average. If the volumes remain unchanged, the revenue of Global Blue will increase as it takes its share of the VAT. However, combined with the overall inflation it’s possible that the volumes could fall. According to Global Blue, in the last recession in 2007-2008, the tax-free shopping remained flat, while international travel and luxury goods sales declined by 16 and 8 per cent.

Additionally, an investor should pay attention to the phenomenon of revenge-spending. For example, the so-called recovery rate, compared to pre-covid, in Europe decreased in the last quarter, which could potentially be a sign of slow down of consumer consumption.

Global Blue carries a significant amount of debt. At the end of its previous fiscal year it had a long-term debt position of €731.6 million. At the end of Q2 of fiscal 23/24 the company had a debt position of €610 million on a pro forma basis and a net debt of €562 million. Along with increased interest rates Global Blue’s interest expenses doubled from €12 million to €24 million. In the latest quarter the company refinanced its debt with a maturity till 2030 and a 5% margin on top of the euribor.

The long-term target of the company, in a couple of years time, is to have leverage below 2.5x on net debt to EBITDA basis. By next year’s EBITDA guidance of €245 million and pro forma net debt, the leverage would be below its target.

New businesses and markets supporting growth

Global Blue has recently made exclusive contracts in Peru and Colombia for Tax Free Shopping Solutions. These countries are unlikely to move a needle for Global Blue, but they are examples of the company's market position and power of its brand and technology. In the past, new markets enabling tax-free shopping have contributed to the growth significantly and the ones who have given up on tax-free shopping, for example the UK, are having talks about returning back to the scheme.

In 2020 the company decided to diversify and grow along with e-commerce and leverage its relationships with its retail clientele. The new segment is called Retail Tech Solutions (RTS). Although its share of total revenue was only 6%, in the latest quarter the RTS segment increased its revenue by 65% and 39% organically. The segment is a collection of majority stakes in several different companies. Initially, these acquisitions were funded by an investment of $250 million by CK Opportunities in Global Blue.

Global Blue's RTS businesses. (20-F)

Significant upside if the company meets its guidance

The stock has traded significantly down since the company became public through the SPAC.

For the current fiscal year, ending in March, Global Blue is guiding for €145-165 million EBITDA. For the following fiscal year the guidance is €245-265 million. With an enterprise value of €1.56 billion and using lower end figures, this would translate to EV/EBITDA multiples of 10.7x and 6.3x. These multiples don’t appear high for a company recovering as fast as it has been. Although the growth comes from extremely depressed levels and will ultimately slow down, it appears that the market has not discovered its recovery.

Quarterly growth rates. (Tikr)

Global Blue aims to grow revenue 8-12% with over 50% EBITDA drop-through. Let’s assume that Global Blue reaches €245 million EBITDA next fiscal year and then see what the stock could be worth with different EBITDA growth rates and EV/EBITDA-multiples in approximately three years.

In a bear case we assume that the revenue grows 4% and EBITDA 2% annually. In a base and bull case the EBITDA grows 4% and 6%, meaning that in a bull case the company reaches its revenue growth target. The table assumes no significant multiple expansion, expecting them to stay at around current levels. In base and bull scenarios the assumption is that the net debt to EBITDA goes 2% and 3% below the 2.5x target. Here no further dilution is assumed and the exchange rate between EUR/USD is assumed to remain at current level.

Estimation of stock price based on EV/EBITDA and EBITDA in 3 years. Figures in EUR, millions, except the share price (USD). (Author)

What the table tells is that there’s not too high expectations built in the stock from an EBITDA generation perspective. Surely, the market might give much more value to real earnings. The largest question mark is at what kind of multiple should be applied to the stock. There’s no direct peers. For example, Paypal ( PYPL ) is currently trading at around EV/EBITDA 10x, while Global Blue is producing a higher EBITDA margin.

Conclusion

Global Blue is a market leader in two of its main businesses with a rapidly growing e-commerce services segment. Its businesses are capital light, high-margin and tapped into several megatrends. Its niche is more resilient than one could expect, since Global Blue enables consumers to save and retailers to earn more.

An individual investor now has an opportunity to pay less for a stock that the main shareholder paid for the company over 10 years ago and less than Tencent paid a couple of months ago. If Global Blue is able to grow at an even lower end of its guidance, the stock could be worth twice more than the current price.

Editor's Note : This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!”

For further details see:

Global Blue: This Forgotten Market Leader Could Be Set To Double