GIC - Global Industrial Company Lacks Momentum But Rides On Acquisition Benefits

2024-01-09 10:47:39 ET

Summary

- GIC is focusing on investing in eCommerce channels and traditional one-to-one sales channels to drive growth.

- The company saw impressive volume growth in Q3, but order growth shrank due to lower demand for core commodities and consumables.

- GIC's acquisition of Indoff has strengthened its B2B e-commerce platform and expanded its product portfolio, but pricing pressure and margin contraction remain challenges.

GIC Is On A Steady Path

I have been discussing Global Industrial Company ( GIC ) in the past, and you can read the latest article here from December 2022 . As pointed out earlier, the company keeps investing in the traditional one-to-one sales channel while it increases its focus on the eCommerce channels. I expect the Indoff acquisition to accelerate its strategic moves. While the operating margin, which was under pressure, as discussed in my previous article, contracted again in Q3, sales volume provided a cushion. It saw impressive volume growth in Q3 for the large and SMB (small & medium-sized business) customers. Reversing the cash flow decline is also encouraging for investors.

However, GIC’s order growth shrank in Q3 due to lower demand for core commodities and consumables. I think it will be challenging to raise prices in a competitive industry, which will keep the operating margin under a lid. Nonetheless, its cash flows have improved while a zero-debt balance sheet boosts investors’ confidence. The stock is relatively overvalued compared to its peers. I think investors would do well to “hold” it.

Analyzing Current Strategies

{kind=link}

GIC's Q3 2023 Presentation

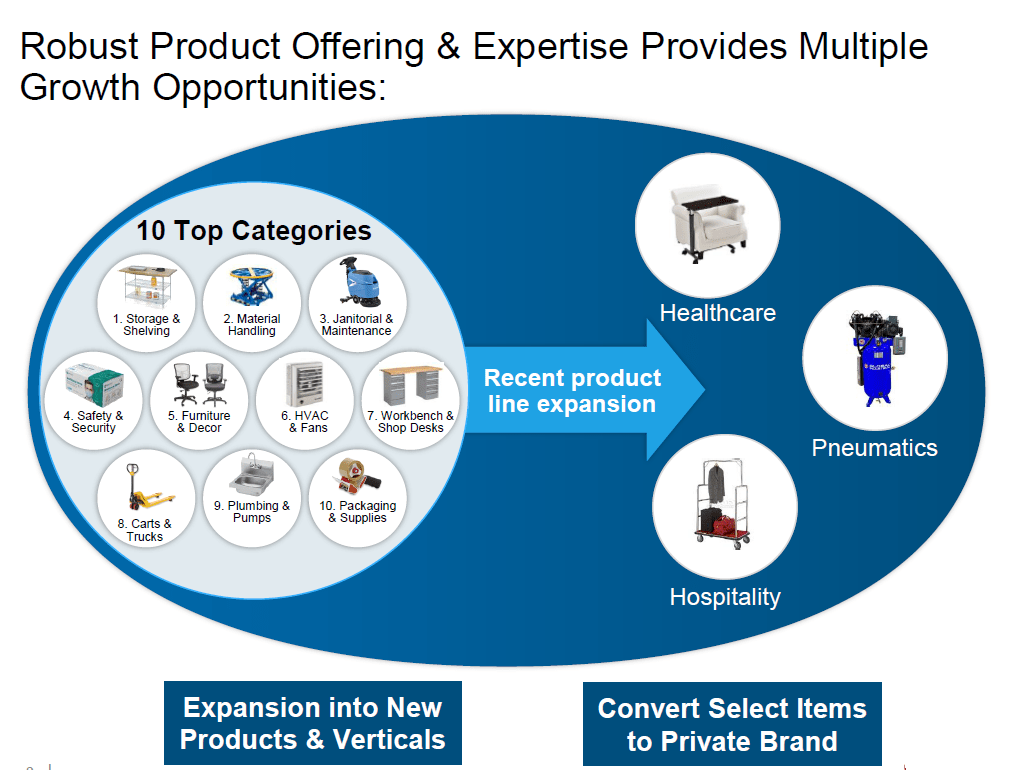

GIC currently invests in its eCommerce channel, and the one-to-one sales channel remains a key focus. It has invested in digital transformation to improve returns. It invests in marketing, price analytics, intelligence, and private brands. It aims to build large accounts and expand into new end markets. So, its sales volume increased in national and public sector accounts. In November, it received a floor cleaning equipment contract from Vizient, one of the largest healthcare performance improvement companies.

The volume growth in Q3 was impressive despite the relatively low order growth. Many of the orders originated from large and SMB customers. Given the economic environment, I do not think the large customers will be confident enough to increase their order sizes soon. Also, the pricing competition will remain.

Order Growth And Industry Concerns

One of the key challenges for the past several quarters has been pricing pressure and low order growth. The company sees the pricing contraction mostly happening in core commodities and consumables. However, investors should also keep in mind that the higher prices also accentuate the year-over-year drop in prices in the prior year. This is because the increase in price in the previous year was in response to the costs associated with inbound ocean freight. As the year draws in, prices should normalize and stabilize in Q4.

{kind=link}

tradingeconomics.com

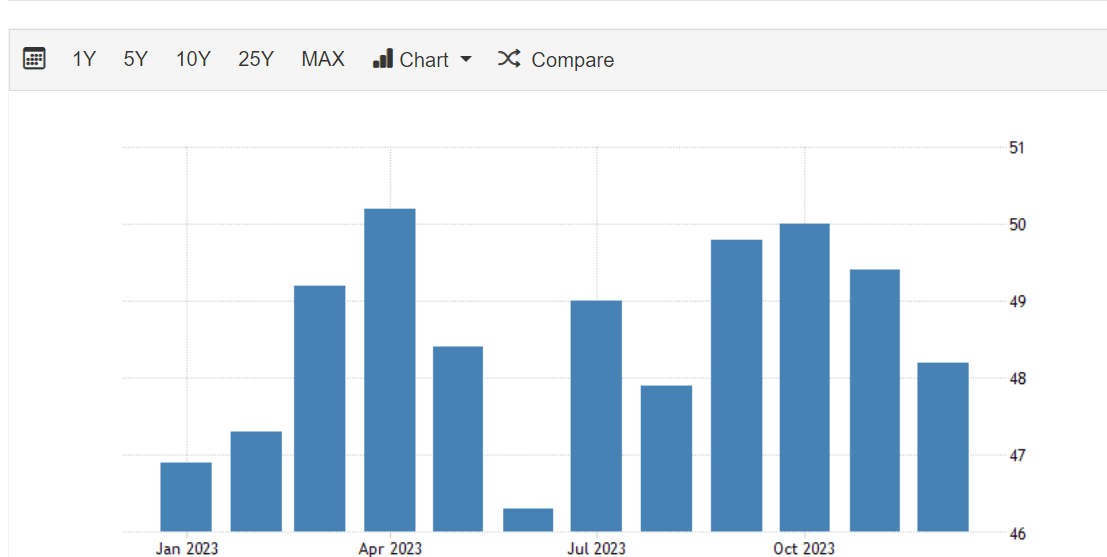

In December, the ISM Manufacturing PMI clocked 48.2, which indicated contractions in output, new orders, employment, and purchase stocks. However, supplier delivery times improved over the past few months as material availability eased. Many manufacturers have cut costs and continued working through stocks to fulfill new order requirements. So, the supply side is still under some duress, although it appears to be manageable now.

Acquisition Impact

{kind=link}

GIC's Q3 2023 Presentation

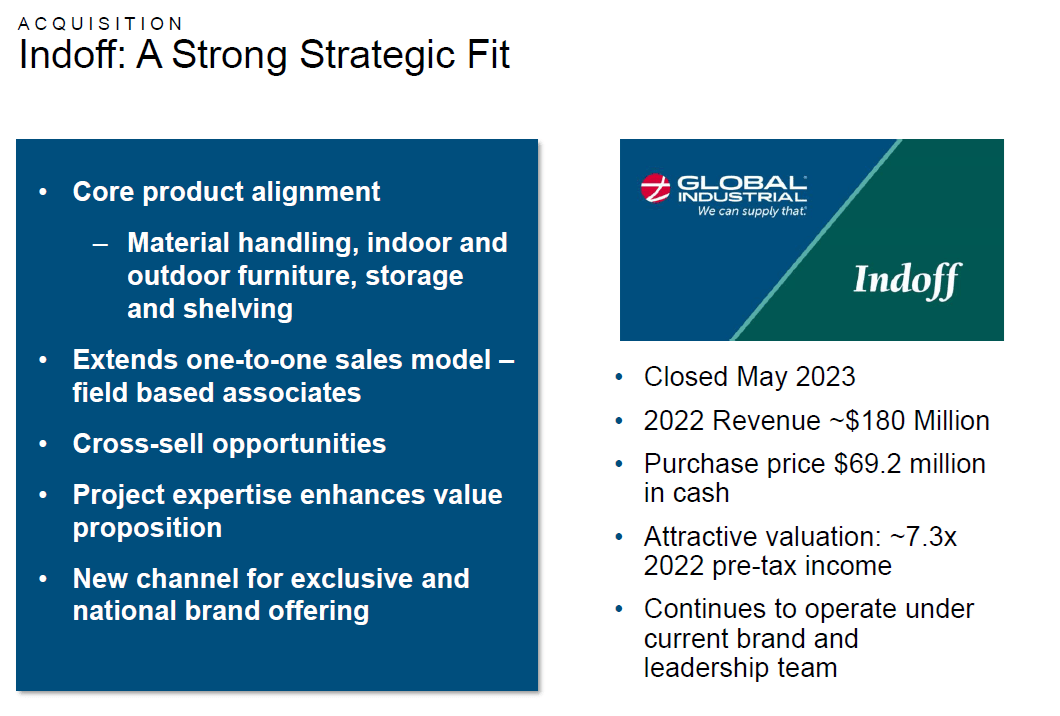

GIC acquired Indoff in May 2023 for ~$69.2 million in cash. Indoff had a network of 350 sales partners. It deals in the sales & distribution of material handling, furniture, storage and shelving, and appliances. The acquisition also strengthened the company’s utilization of the B2B e-commerce platform.

I think this acquisition is a good fit for GIC at this cost. It retained Indoff’s brand and leadership following the acquisition. The acquisition will allow the opening of new channels to promote GIC’s brand and better utilize its B2B e-commerce platforms. The addition of new capabilities should strengthen its value proposition in the market.

Margin Outlook

{kind=link}

Seeking Alpha

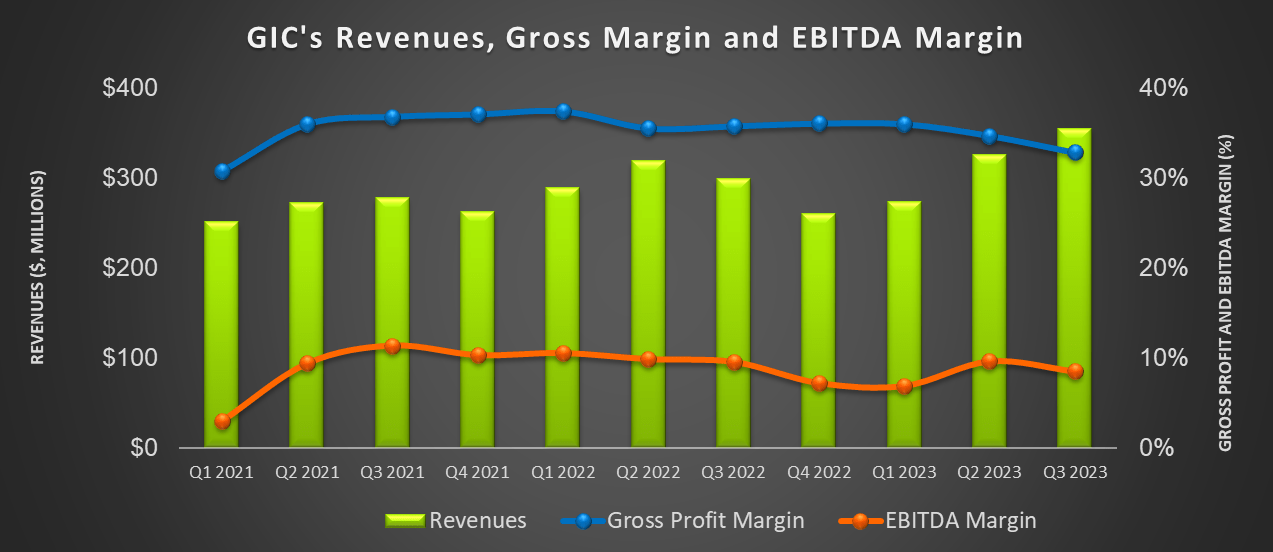

Year-over-year, GIC’s adjusted gross margin contracted by 290 basis points in Q3. However, the organic growth margin was more resilient in Q3. Increased expenses on promotion and selling through high-cost inventory in the cooling category pushed costs higher, resulting in margin contraction. Therefore, maintaining the margin profile remains a key area of focus.

In a stiffly competitive environment, pricing traction remains difficult. I think this will lead to modest sequential organic margin growth in Q4. Although inventory costs will likely be reduced, Indoff’s higher cost structure can hurt GIC’s margin.

Looking Through Q3 Drivers

In Q3 2023 reported in October, GIC’s revenues increased by 19% compared to a year ago. However, much of the increase is attributed to the Indoff acquisition. Excluding that, its core sales grew by 3.2% in Q3. Quarter-over-quarter, too, its sales volume improved, despite the pricing pressure. Valued in local currency, its revenue growth in Canada exceeded the US. An uncertain demand scenario hampered buying decisions in the US in Q3. In Q4, the pricing factor is expected to be more lenient compared to Q3.

Cash Flows And Debt Level

In 9M 2023, GIC's cash flow from operations (or CFO) increased steeply (3.4x) compared to a year ago. Although revenues remained relatively unchanged, positive changes in working capital related to lower inventory and accounts payable led to cash flow growth. Free cash flow (or FCF) more than doubled in 9M 2023.

GIC has no debt. So, its balance sheet is superior to some of its peers (DSGR and FAST). Its liquidity totaled $138 million as of September 30, 2023. During Q3, it repaid the $40.3 million balance on the credit facility. The company pays an annual dividend of $0.80 per share with a dividend yield of 2.05%. The management is confident in managing its strategic plan and funding its quarterly dividend through its liquidity.

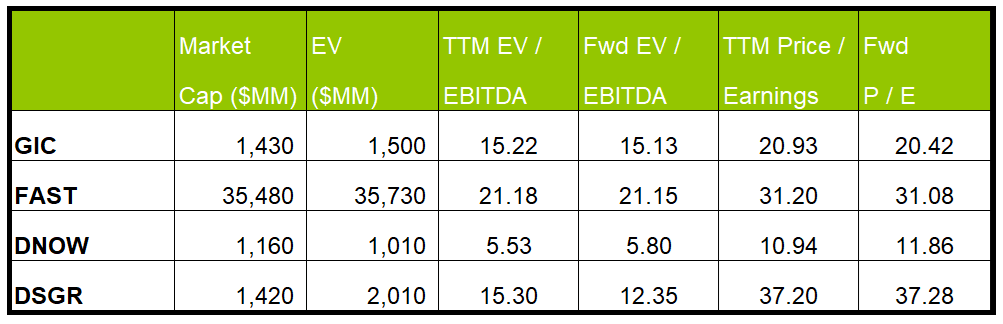

Relative valuation

{kind=link}

Author Created and Seeking Alpha

GIC's forward EV/EBITDA multiple contraction versus the current EV/EBITDA is less steep because its EBITDA is expected to increase less sharply than its peers in the next year. This typically reflects in a lower EV/EBITDA multiple than peers.

However, its TTM EV/EBITDA multiple (15.2x) is higher than its peers' (FAST, DNOW, and DSGR) average of 10x. So, the stock is relatively overvalued. It is also trading at a premium to its past five-year average. If it trades at the past average in the medium term, it can decline by 7% from the current level. So, its return outlook has not changed much since my last stock analysis. However, as its strategic positioning improves, the stock should recover and yield positive returns in the medium term.

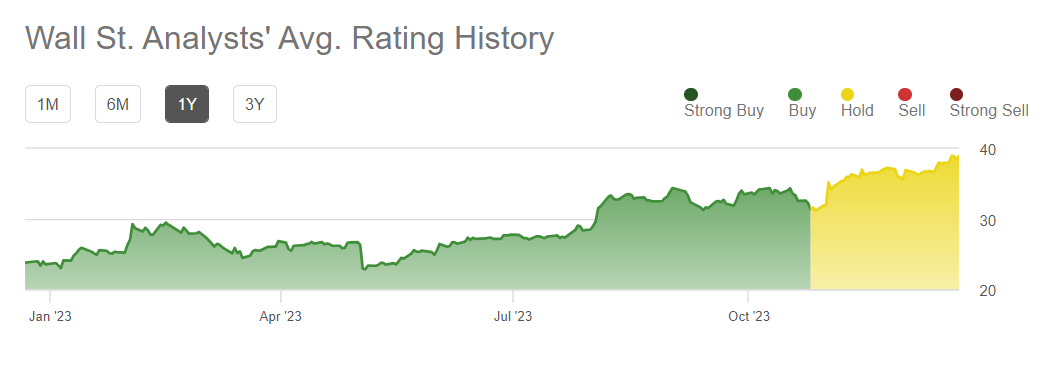

Wall Street Rating

{kind=link}

Seeking Alpha

One analyst rated GIC a "hold" in the past 90 days. None rated it a "sell" or a “buy.” The consensus target price is $36.5, suggesting a 2% upside at the current price. I think, given the current value drivers, the Wall Street analysts are overestimating its returns.

Risk Factors

One of the key risks for GIC is the uncertainty in economic conditions and the lack of visibility relating to future orders. In this connection, international geopolitical instability can affect its operations, including its ability to manage freight & shipping costs and prices. This can adversely affect its margin, as seen in the past. In the past, the tariff war between the US and China created supply chain constraints, pushing costs higher. Such instances can recur if the geopolitical condition deteriorates.

Why Do I Keep My Rating Unchanged?

In my last iteration on GIC, I discussed how the company’s focus on the digital e-commerce platform could enhance its digital footprint. It also looked to gain market share in hospitality and large healthcare markets. The company kept its inventory level high, adversely impacting its cost structure. Its free cash flow declined. I wrote :

GIC is building a long-term competitive position through investment in private branding, digital marketing, pricing analytics, and distribution. Healthcare is one such market that holds significant potential because GIC has had low penetration in this market.

After Q3, it focuses on building eCommerce channels, large accounts, and expanding into new end markets. The Indoff acquisition helped strengthen its product portfolio, although it pushed its cost structure higher. The competition in the market will likely hold back any potential operating margin growth. Cash flows, however, improved significantly. Considering all aspects, I reiterate my “hold” call on the stock.

What’s The Take On GIC?

{kind=link}

Seeking Alpha

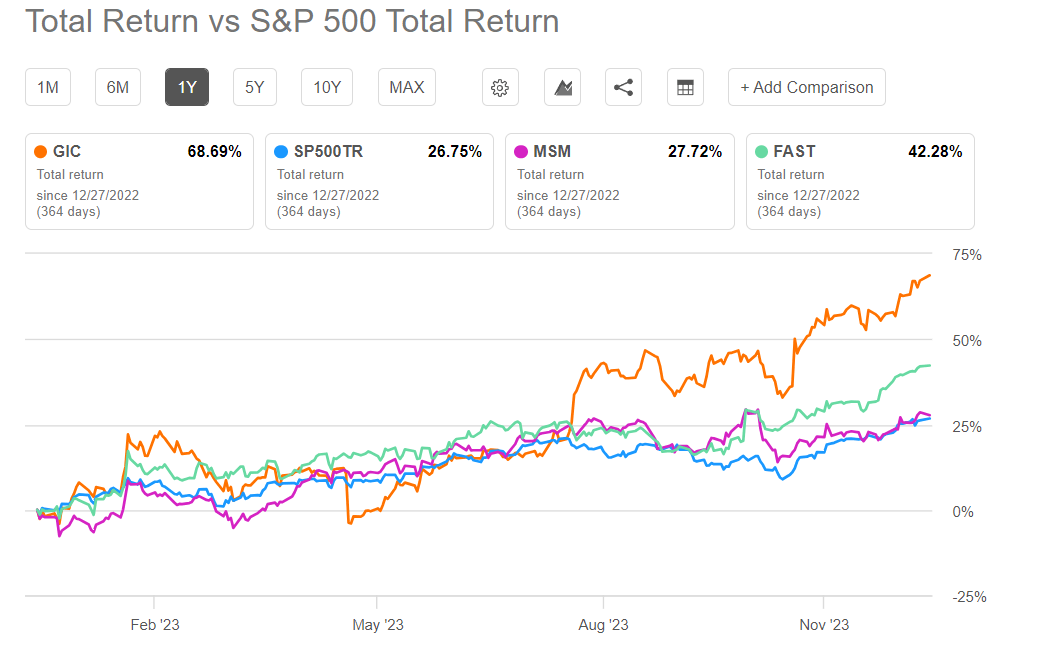

GIC invests in digital transformation to improve returns, which helped expand its national and public sector accounts. Its recent award for floor cleaning equipment contract from Vizient is the latest addition in this direction. The other growth factor is the impact of the Indoff acquisition, which distributes many products and a vast sales partner network. Plus, its B2B e-commerce platform utilization also strengthened following the acquisition. So, the stock outperformed the SPDR S&P 500 ETF ( SPY ) in the past year.

The main challenge facing GIC is the difficulty of raising prices in a competitive industry and the margin pressure due to cost hikes from promotional campaigns. Despite that, its cash flows improved substantially in 2023. Plus, it has a zero-debt balance sheet. Given the relative valuation, I consider the stock apt for a “hold.”

For further details see:

Global Industrial Company Lacks Momentum But Rides On Acquisition Benefits