GIC - Global Industrial: Traits Of A High Quality Stock

2023-05-16 02:12:27 ET

Summary

- Global Industrial is an industrial distributor with a differentiated approach. Its performance during the past 5 years could be overshadowed by its history and name changes.

- Disappointing Q1 results punished the stock and the weakness could provide a buying opportunity, if the challenges are temporary.

- The company has an excellent capital return profile, concentrated family ownership and no debt. The stock trades below its historical averages and the peer group.

- Global Industrial pays an attractive 3.4% dividend yield and has been growing the dividend for 6 years supplemented by occasional special dividends.

Global Industrial Company ( GIC ) is an industrial distributor whose history shadows its performance in the past few years. Formerly the company was known as Systemax which was a collection of dying businesses. Today, Global Industrial has a simple focus and business model generating high returns on capital. The company has been growing its revenues and margins at a steady pace since 2017.

GIC stock is valued significantly below its peers and historical averages, and lower than what the track record and profitability could justify. In addition, the company pays an attractive dividend sometimes supplemented by special dividends. The company also has a robust balance sheet with no debt.

Industrial distributor with a differentiated approach

Global Industrial is a one billion dollar market cap company focusing today on distribution of industrial, maintenance, repair and operational products. The company has seven distribution centers spread across the United States and Canada offering a selection of 1.7 million products. In 2022 the revenues were $1.2 billion and employed 1650 people. The company has a long history which is filled by name changes.

The company was founded in 1949 as Global Equipment Company, a material handler. It first entered direct marketing in 1972 and began marketing computer equipment in 1981. The company changed its name to Global Direct-mail in 1995 and to Systemax in 1999 and Global Industrial Company in 2021.

Unlike many of its competitors Global Industrial doesn't have any physical branches or outlets. The company relies on the field sales force and e-commerce in its sales efforts. This reduces the reach of the company, but reduces costs, complexity and capital requirements. Among its peers Global Industrial has the highest share of private label revenue which generates half of its sales. Private labels provide higher gross margin but could hurt the relationship with brand manufacturers.

Disappointing Q1 results punished the stock

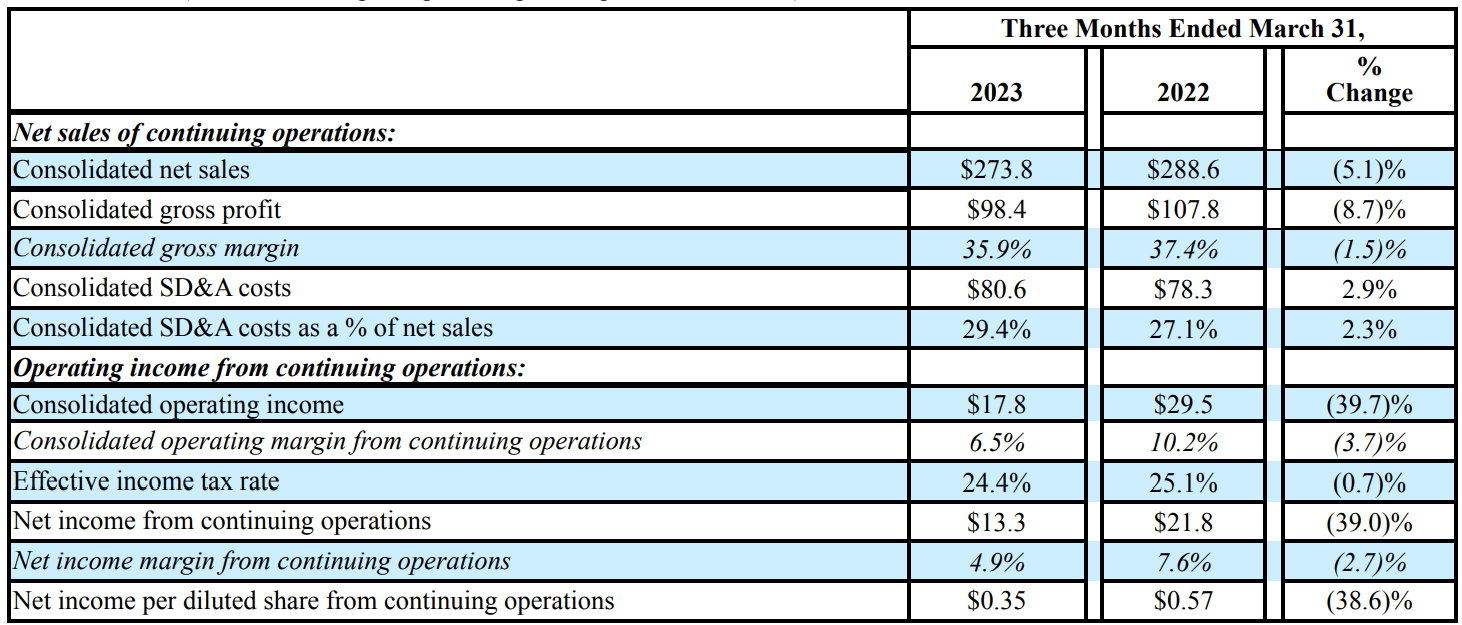

The first quarter results were a disappointment to the market and the stock got punished with a 13% decline. The company's performance was unsatisfactory on all fronts. The revenue declined by 5.1%, gross margin declined to 35.9% from 37.4% previous year. Due to the decreasing sales and margins, net income per share shrunk by 38.6% down to $0.35 compared to $0.57 previous year.

There are some acceptable reasons for the sales decline of $14.8 million. If we adjust the number with two factors, equivalent amount of selling days ($4.3 million) and currency effects and one-time sales that occurred last year in Canada ($3.4 million) the sales decline is approximately $7.1 million.

There were also additional costs that aren't necessarily recurring. The company spent $1.1 million on the ramp-up of a distribution center in Canada and an additional $1.2 million on marketing. If we exclude all these four elements, the decline of net income would be 20% instead of 39% reported by the company. Not too good either, but giving a better picture of the underlying performance and showcasing how small relatively small absolute differentials can have a large impact on a medium sized business and its profitability.

First quarter 2023 results of GIC. (10-Q.)

{kind=link}

According to the management, the accounts of small and mid-sized businesses were not performing as well as large accounts. Since Global Industrial is focusing on the SMB-segment this could be a reason explaining worse performance than the peers in the quarter. According to the latest earnings call, the management expects the weakness among SMBs to continue. However, the short term weakness could create a buying opportunity for a patient dividend investor.

Breaking down the investment thesis

High returns on capital

When looking at the current valuation multiples, it seems like investors might be missing the fact how high capital returns the company has been producing since 2017 after the transformation to a pure industrial distributor.

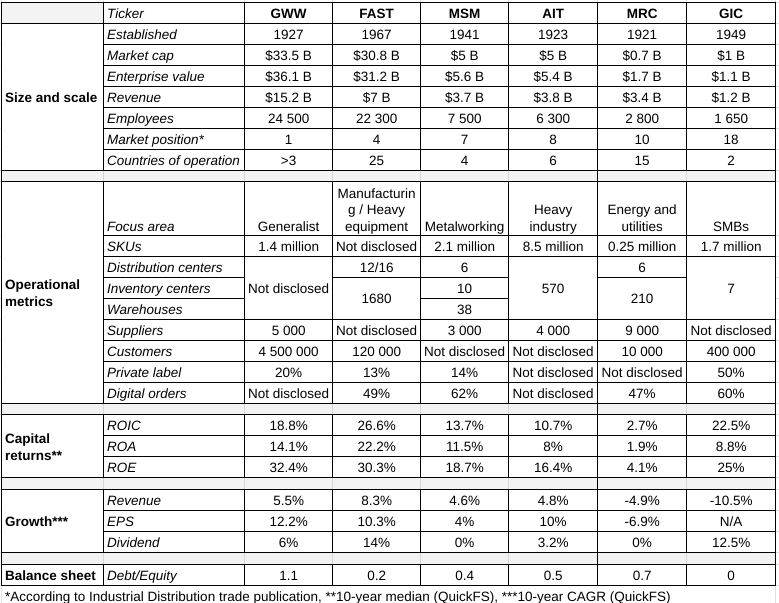

Both ROIC and ROE are higher than the 10-year averages for Fastenal (FAST) and W.W. Grainger (GWW), which are the blue chips in the industry. Even if we exclude the exceptionally high numbers in 208 the average ROIC is 27.9% and ROE is 42.5%, which are higher than the ones for the two peers. Despite this, Global Industrial trades at much lower multiples, as we will see.

ROIC and ROE of GIC. (Author, data source roic.ai.)

The annual revenue growth has been 6.8% from 2018. Since 2017 Global Industrial has realized a strong and steady margin profile. Gross margins have fluctuated between a tight range of 34-36% and EBIT margin between 7-9%. Here, Global Industrial lags the two blue chip peers.

Concentrated ownership

Global Industrial is controlled by Leeds family which controls 66.4% of the voting power. The fifth largest owner is the first outsider, Mawer Investment Management, with a 4.7% ownership. After transforming and downsizing Systemax into Global Industrial it's difficult to see a reason for Leeds family to let go of the company. However, if there's an increased interest in the stock, there's not plenty of free float to cover that demand.

Richard Leeds serves as the chairman of the company and the current CEO, Barry Litwin, has been in his role since 2019. Litwin introduced an "accelerating customer experience" strategy to create the best buying experience and achieve customer loyalty.

Potential for organic sales growth and acquisitions

The company aims to grow its revenues 5 %-points faster than the market which is estimated to grow slowly, at 2.5% annual growth rate until 2030. Global Industrial is in the process of establishing its presence in the hospitality and healthcare verticals, but currently these verticals don't have a meaningful contribution to the growth and likely need several quarters of leg work from the field sales to achieve results.

The company also seems to have potential to take market share in Canada, which importance at the moment is relatively low. In November 2022 the company opened a new distribution center in Canada and increased the capacity three-fold. The new distribution center is said to increase the service level and shorten lead times. Although being a small part of total revenue, an investor should pay attention to the development of Canadian sales, if the management is able to execute on this growth avenue.

Financial goals of GIC. (Global Industrial.)

Global Industrial prioritizes strategic acquisitions. In the fragmented industry this should be possible to do without destroying value for the shareholders. According to MSC Industrial, the fifty largest distributors only have a total market share of 33%. According to the Industrial Distribution trade publication , Global Industrial holds the market position of 18th, up from 19th in 2020 but down from 16th position in 2021.

Unknown name on the Street

The fairly recent name change , from Systemax to Global Industrial, in June 2021 could be one reason for a low level of awareness among investors. Global Industrial Company is not a name to be remembered, it's vague and unoriginal. The name is also misleading as the company operates solely on one continent.

Second, the spotty history of Systemax could repel some investors with a better than average memory. Last but not least, the former Systemax has done quite a significant transformation from electronics and IT-equipment reseller to the current form. Systemax can be recalled from names such as CircuitCity, CompUSA and TigerDirect from over a decade ago. These mediocre businesses are now long left behind.

Robust balance sheet

In the current market environment it's also a great benefit that at the end of the first quarter the company had $48 million of cash and no debt. The cash position increased from $28.5 million from a year ago. Out of the total assets of $461.6 million only $8.3 million were goodwill and other intangibles at the end first quarter.

The stock could be trading below its fair value

The investment thesis on Global Industrial does not necessarily build on the superior quality of the company. There are many better companies in the same business such as W.W. Grainger and Fastenal. Global Industrial definitely faces tough competition. It's one of the smallest publicly listed industrial distributors as can be seen in the comparison table below. A little bit deeper discussion of the industry can be found in my analysis about MSC Industrial (MSM).

Competitive landscape. (Author.)

{kind=link}

Instead of the economic moat, the investment thesis is based on lower relative and absolute valuation, comparable capital returns and profitability during the past five years and low indebtedness. In the light of these variables, the stock seems undervalued. The market appears to give a good discount on the smaller sized distributor.

Valuation multiples. (Data source: Seeking Alpha.)

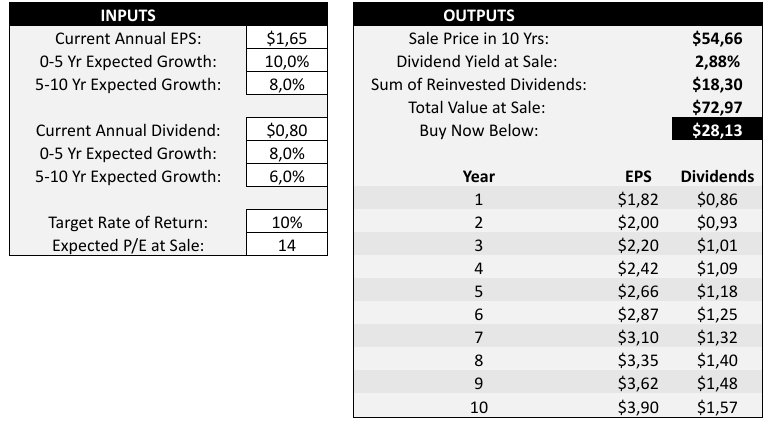

Out of the two in total, the lowest analyst EPS estimate for the current year is $1.65 ($2.04 in 2022). For the sake of safety margin, let's use this figure as a starting point to see if Global Industrial is a buy or not. Let's assume 10% EPS growth for the next five years and 8% after that. The historical growth rate has been for the past three years 13% and the company is aiming for 10-15% annual EPS growth.

Let's also assume that the company grows its dividend 2 %-points slower. Although a company growing this fast would deserve a higher multiple, let's assume a terminal P/E of 14 and apply a 10% discount rate. With these assumptions Global Industrial would be a buy under $28 per share. If we drop all the growth rates by 1 %-point lower, the fair value would be $26.

Fair value calculation based on earnings and dividend. (Author, model by Lyn Alden Schwartzer)

{kind=link}

There are only two Wall Street analysts following the company with an average target price of $48, which is probably a stretch but indicating upside potential.

Rewarding the shareholders

The company aims to return capital to shareholders by growing dividends, special dividends and share repurchases.

Global Industrial currently pays an annual dividend of $0.8 per share translating to a dividend yield of 3.4%. The payout ratio stands comfortably at 35%. The company pays out less than half of its average operating cash flow as dividends. The average dividend growth rate for the past five years is 12.5%. The average dividend yield is around 1.9%, which is another indication of undervaluation of the shares. Global Industrial has increased its dividend for six consecutive years.

Dividend record. (Global Industrial.)

The occasional special dividends have been rather substantial. Last time the company paid a special dividend was in 2021. The year end installment was $1 per share, which would solely by today's share price mean an additional yield of 3.7%. At the time the special dividend was worth $38 million and after the payment the company's cash position was $15 million and it had $4.5 million of debt.

In order to grow the earnings per share at a pace of 10-15% the company likely needs to do share repurchases. Currently, the company has 1.5 million shares left in the existing buyback program.

Conclusion

Global Industrial is a family-owned company with a robust balance sheet. It has a differentiated approach to a slowly growing industry and has a track record and ambition to gain market share. The company has achieved excellent capital returns and stable margins after its focus on industrial distribution. This might have gone unnoticed from the larger investment community.

The multiples are low compared to its peers and historical averages. Based on earnings and the dividend the stock is trading below its fair value. In addition, Global Industrial is offering a solid and growing dividend. As a last remark, an investor should stay alert on the following quarterly earnings, if industrial demand weakens and if the company is able to keep up its performance against the peers.

For further details see:

Global Industrial: Traits Of A High Quality Stock