MT - Global Infrastructure Theme Is Manifested By ArcelorMittal

2023-06-12 20:21:24 ET

Summary

- ArcelorMittal, the second-largest steel manufacturing company globally, has achieved a Q1 EBITDA of $1.82bn and booked ~$1.1bn in net income, driven by its value creation strategy of decarbonization, strategic growth, and capital returns to shareholders.

- Despite underperforming in the steel industry, MT's strong financials and undervaluation make it a 'buy' recommendation, with a fair value of $30.37, according to a discounted cash flow analysis.

- Risks and challenges for MT include input cost volatility, rising interest rates diminishing demand, and logistical or geopolitical risks affecting its international presence.

ArcelorMittal ( MT ) is a Luxembourg-based multinational steel manufacturing company - the second largest in the world - with annual crude steel production of 88mn tonnes in 2022 and annual revenues approaching $79.84bn.

ArcelorMittal Q1'23 Presentation

{kind=link}

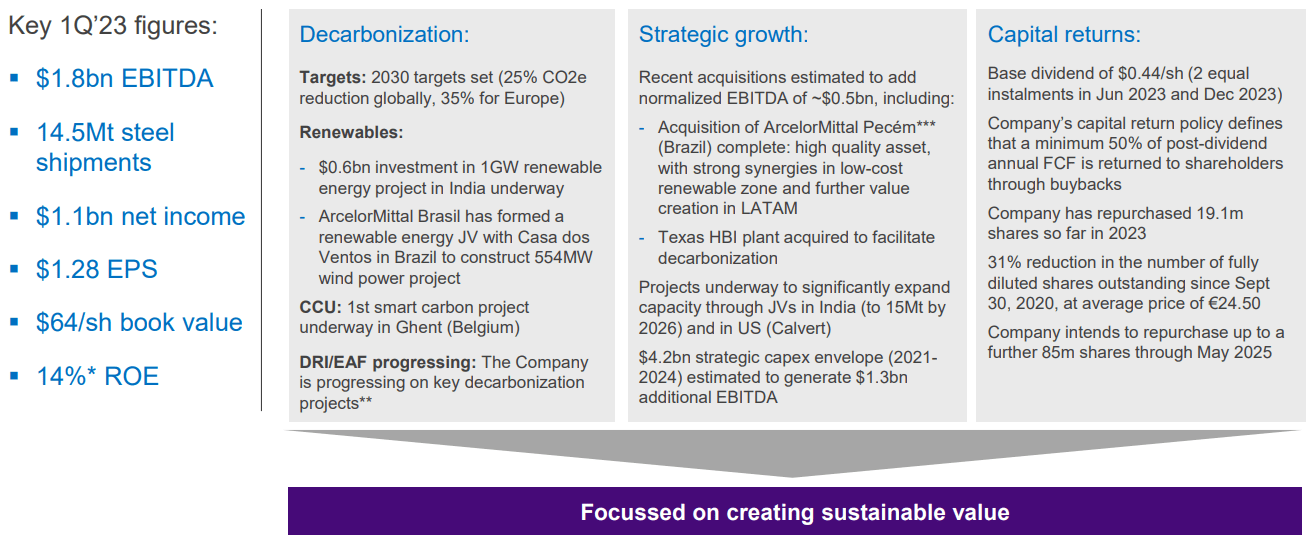

Highly vertically integrated, with operations across the R&D, mining, manufacturing, and distribution of steel products, MT has achieved a Q1 EBITDA of $1.82bn and booked ~$1.1bn in net income in the same period.

This comes on the back of MT's trifold value creation strategy of decarbonization- thus enabling participating in carbon markets, reducing opex, and increasing ESG inclusion- strategic growth through geographic and inorganic means, and capital returns to shareholders, via a combination of dividends and share repurchases.

Introduction

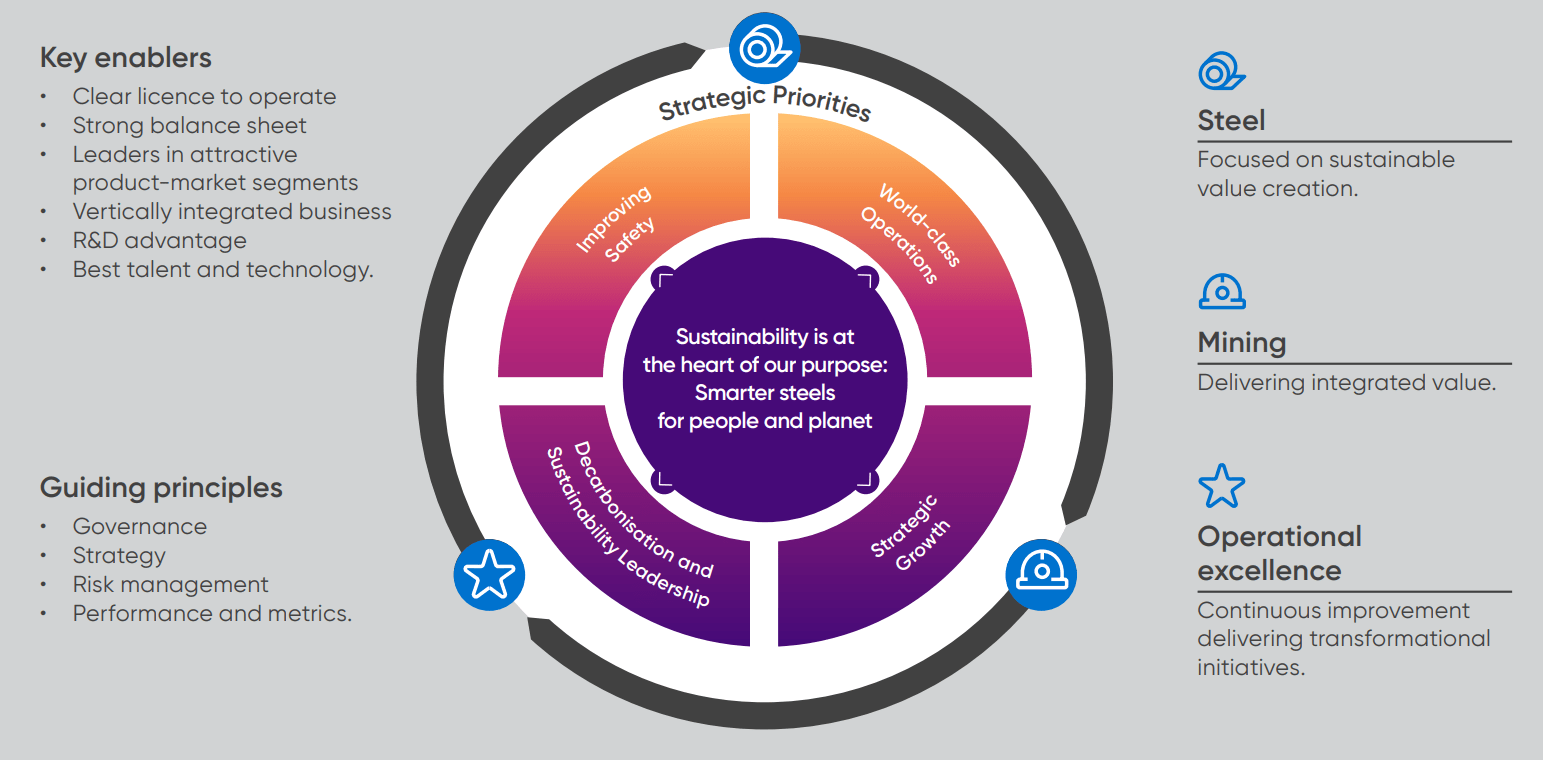

MT outlines four strategic priorities for operational and sustainable success, including continued leadership in decarbonization activities, improved worker safety- proven to promote productivity and retention, strategic growth, and sustained functional strength across its production and mining verticals mix.

ArcelorMittal Q1'23 Presentation

{kind=link}

The company continues to deliver on these priorities with efficacy. For instance, in 2022, MT sold the first batches of its XCarb Recycled flat steel, simultaneously environmentally beneficial sale and profitable, enabling tax support from the EU.

MT's continued operational strength, which allows the company to participate in the COVID-19 recovery and in infrastructure spending programs, as well as its ESG inclusionary strategy and general undervaluation lead me to rate the company a 'buy'.

Valuation & Financials

General Overview

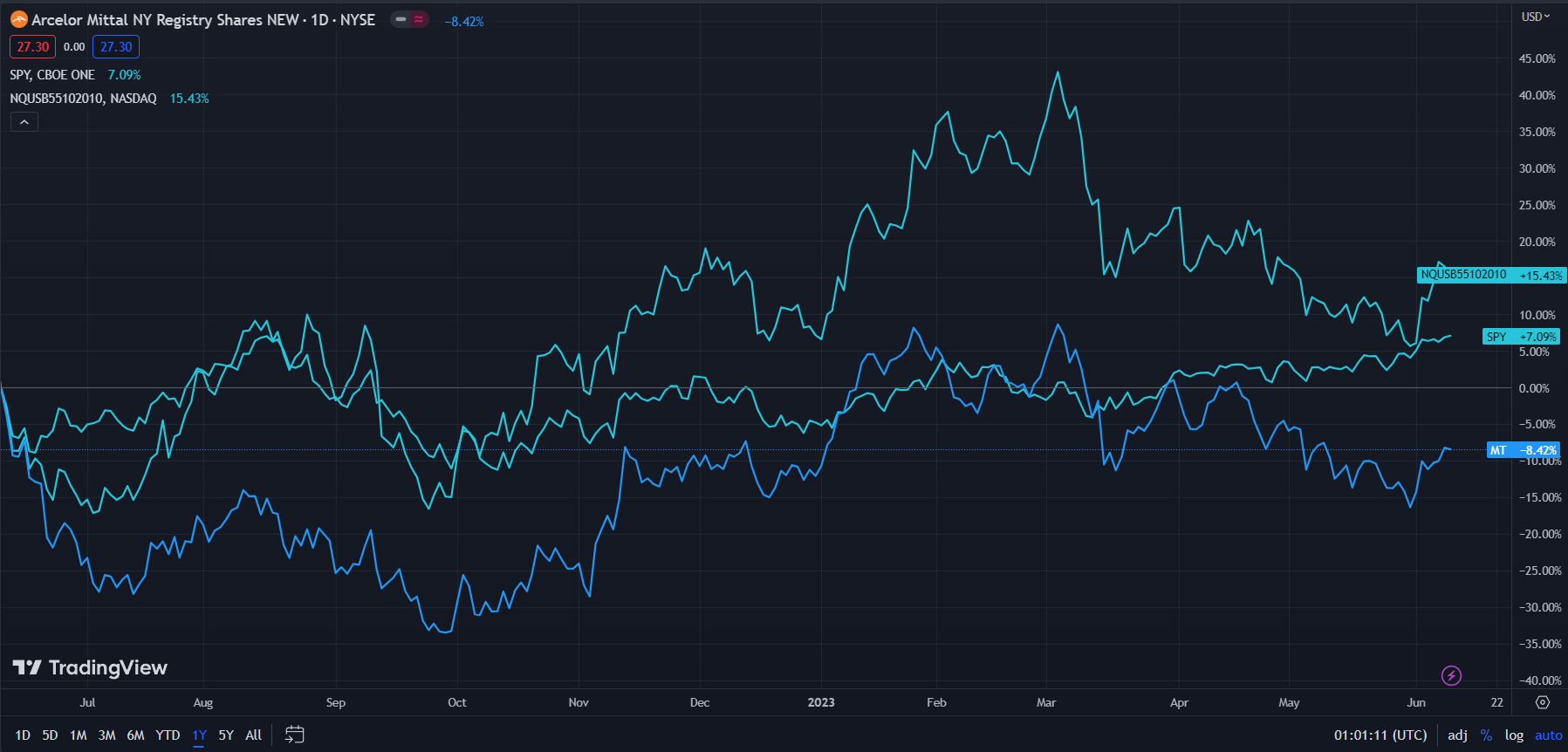

In the TTM period, MT- down 8.42%- has experienced poorer growth relative to both TradingView's iron and steel index- up 15.43%- and the broader market, represented by the S&P500 ( SPY )- up 7.09%.

ArcelorMittal (Dark Blue) vs Industry & Market (TradingView)

{kind=link}

I believe the steel industry's positive price performance is a product of increased government and automaker appetite for industrial goods, while MT's underperformance reflects a market overreaction to headwinds across the company's South African production and subsequent profit hits.

Comparable Companies

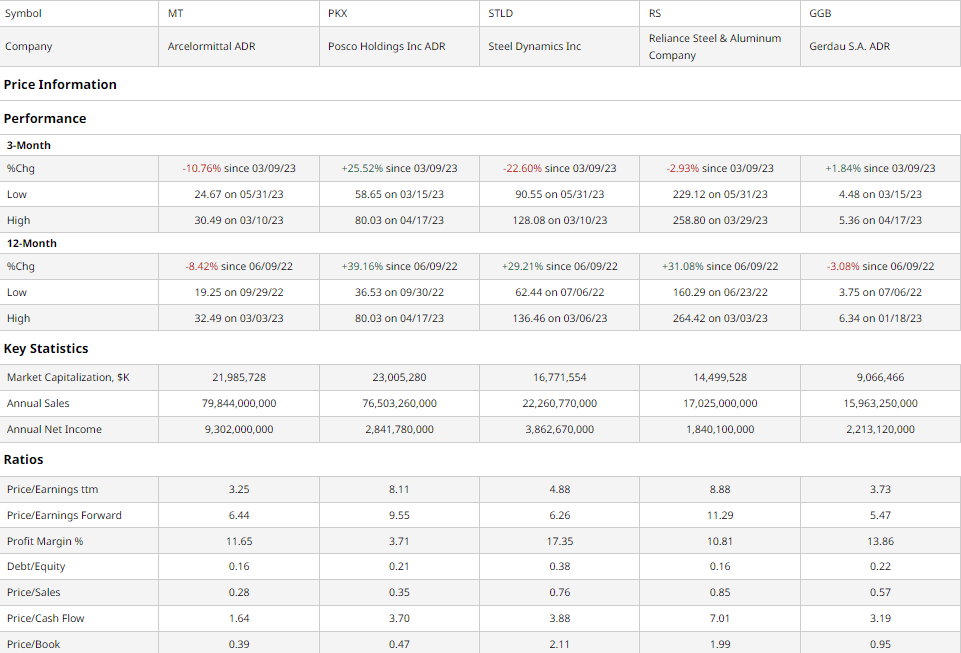

The relative homogeneity of the steel industry lends itself to greater competitive intensity, depressed profit margins, and emphasis on operational capability and efficiency. As such, it makes the most sense to compare MT, although it is the second largest steel producer after state-owned China Baowu Steel Group, to the other largest, publicly traded steel producers. This includes POSCO Holdings ( PKX ), Steel Dynamics ( STLD ), Reliance Steel and Aluminum ( RS ), and Gerdau ( GGB ).

{kind=link}

As demonstrated above, MT continues to underperform relative to peers, experiencing the poorest yearly price action and second-poorest quarterly price action in spite of strong multiples-based value metrics. Though MT's scale proves advantageous during bullish commodity supercycles, I believe the company's global presence lead to its poorer performance, being more sensitive to supply chain issues and pandemic-related closures.

For instance, with a trailing P/E of 3.25, P/S of 0.28, P/CF of 1.64, and P/B of 0.39, MT records the best value on a multiples basis, demonstrating financial strength across the balance sheet, income statement, and cash flow statement.

Moreover, with the joint-lowest debt/equity, MT is poised for superior capital expenditure and investor returns capabilities.

Valuation

According to my discounted cash flow analysis, at its base case, the fair value of MT is $30.37 with an 11% upside from the stock's current price of $27.30.

MT Revenue & COGS Growth, Largely In Line w/Crude Steel Prices (TradingView)

{kind=link}

My model, calculated over 5 years without perpetual growth, assumes a discount rate of 10%, capturing the high implied beta of the company and its cash flows. In line with this thinking, revenue growth is estimated at ~4%, to smooth out the volatile revenues in the steel industry, as well as general recessionary pressures.

Alpha Spread

Alpha Spread's multiples-based relative valuation tool more than supports my thesis on MT's undervaluation, estimating a 58% undervaluation, with a fair price of $64.94.

However, Alpha Spread fails to capture the reality of MT's volatility and fiscal instability and therefore, in my opinion, overprices the company.

Dual Capital Deployment & Megatrend Growth Capture Capabilities Support Baked-In Growth

To capture maximal growth, MT has followed a strategy of broadening the firm's geographic footprint, serving the multifaceted purpose of diversification, adaptability, and megatrend momentum coverage. For instance, as demand across the Commonwealth of Independent States dwindles due to the Russian Invasion of Ukraine and consequent economic ramifications, the company remains positioned to capture significant infrastructure investment in the Americas and European Union. MT has most recently invested in facilities in Brazil and Texas.

ArcelorMittal Q1'23 Presentation

{kind=link}

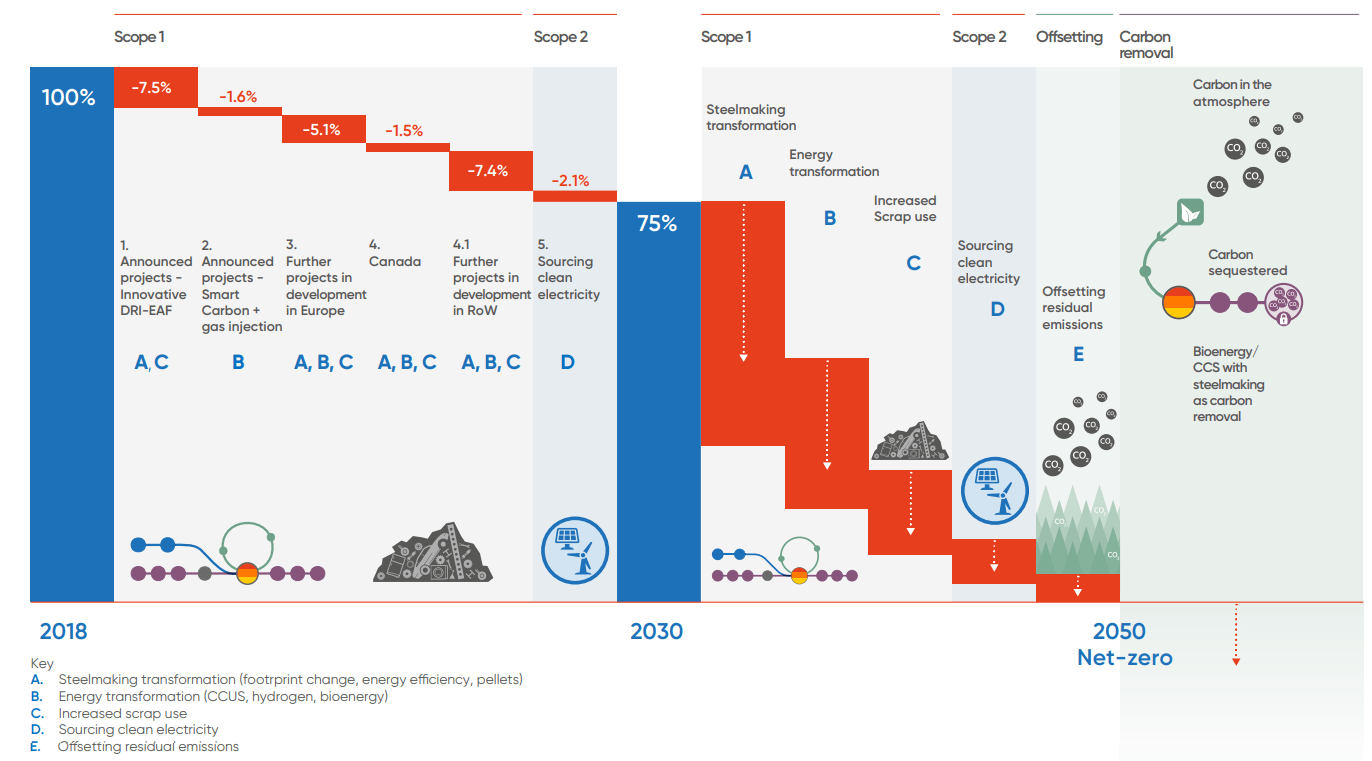

Additionally, supporting the company's sustainability efforts, MT has laid out a roadmap for decarbonization and waste reduction, with residual reductions across different geographies and verticals in conjunction with what best works financially. For investors, this may support index inclusion into ESG funds and increase MT's access to capital whilst reducing the overall cost of capital.

ArcelorMittal Q1'23 Presentation

{kind=link}

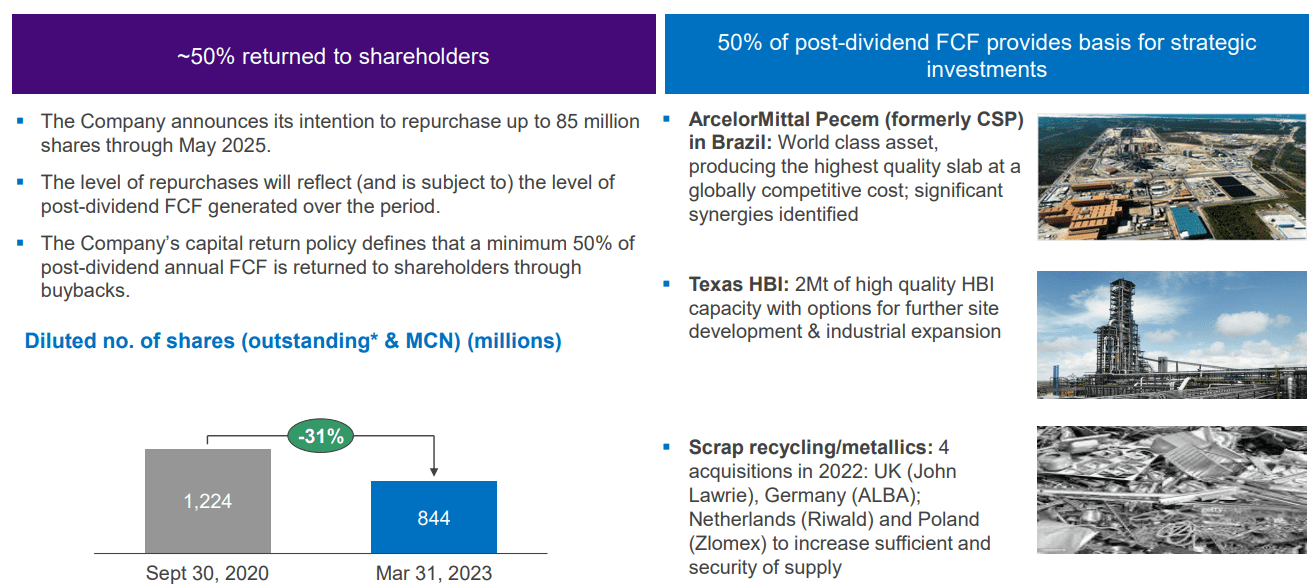

Ultimately, the company will achieve these objectives through reinvestment and M&A activities as outlined by its disciplined capital allocation strategy; as a general rule, the company seeks to return 50% of cash flows to investors, via a combination of opportunistic share repurchases and, to a smaller extent, the company's 0.81% dividend. To promote organic growth, the firm has invested in value-adding facilities, such as mining locations in Brazil and recycling acquisitions across Europe, further emphasizing the company's margin expanding vertical integration.

ArcelorMittal Q1'23 Presentation

{kind=link}

Wall Street Consensus

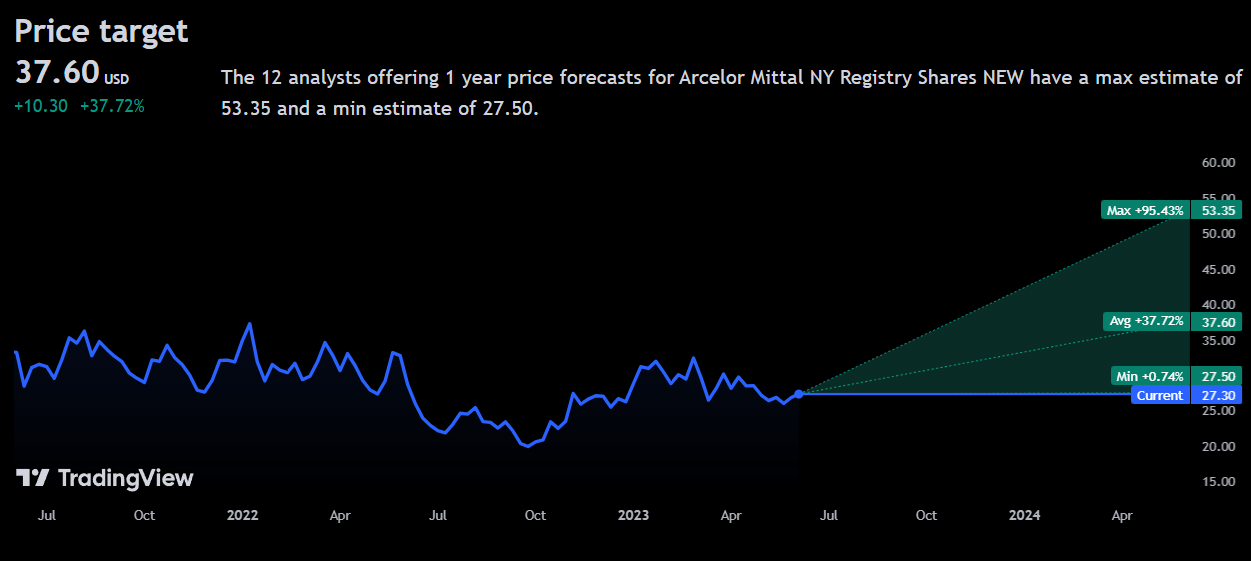

Analysts echo my positive opinion on MT, projecting an average 1Y price increase of 37.72%, to a price of $37.60.

{kind=link}

Even at the minimum projected price increase of 0.74% to a price of $27.50, MT, despite the high level of volatility it faces, experiences positive price growth, demonstrating the sheer level of market overreaction to MT's temporary poor financial results.

Risks & Challenges

Input Cost Volatility

The inherent nature of the steelmaking industry makes MT privy to shifts in commodity prices and inflationary pressures. Such supply volatility is matched only by the demand volatility in the steel industry. Although MT focuses on vertical integration, thus insulating it from the worst of input cost volatility, the company's cash flows remain contingent upon its ability to navigate and pass on increased operational expenses.

Rising Interest Rates May Diminish Demand

MT's relatively low debt/equity levels shield it from experiencing increased large and increased debt expenses. However, the steel industry relies on government and corporate demand for its products, often contingent upon spending capabilities financed through debt. Higher interest rates may lead to recessionary pressures, which compress demand for MT's products and materially reduce the company's scale.

Logistical or Geopolitical Risk

With MT's presence wholly international, the company is exposed to global risks, particularly when concerned with demand. For instance, the war in Ukraine has led to reduced sales to the EAEU and Eastern Europe. And the COVID-driven supply chain crisis led to automakers requiring significantly less steel. Any additional extraneous pressures may reduce MT's ability to generate cash flows and retain clients.

Conclusion

In spite of price volatility associated with crude steel demand factors, I believe investors can expect intrinsic growth, as a result of the company reverting to its fair value, potential ESG index inclusion, and MT's ability to leverage megatrends.

For further details see:

Global Infrastructure Theme Is Manifested By ArcelorMittal