KBND - Global Macro Outlook - First Quarter 2024

2024-01-18 04:08:00 ET

Summary

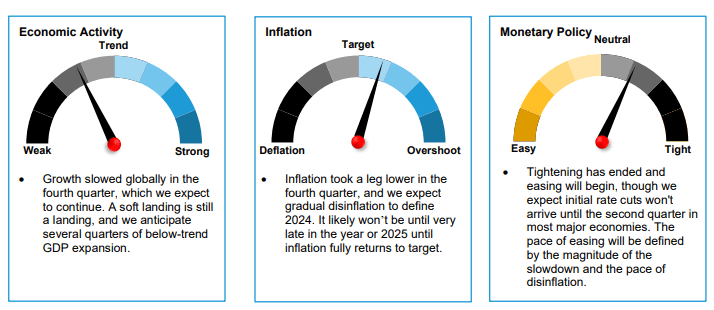

- Growth ran hot for most of 2023; although it’s now slowing, GDP should remain positive for 2024.

- When combined, a soft economic landing and rate cuts would provide the best of both worlds for financial markets.

- Disinflation is further along in the euro area than the US, but core inflation there remains well above target for now.

- China’s policy imperative remains supporting growth and fighting disinflation, and we think they’re equipped to do both.

- Ongoing conflicts in Europe and the Middle East could be disruptive, although markets have largely concluded their economic impacts are likely to be limited.

The Macro Picture

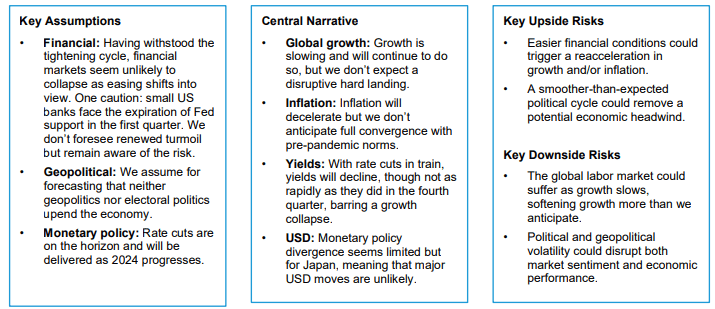

The global economy enters 2024 on the cusp of a transition. After two years of focusing on fighting inflation, central banks appear to have pivoted, with rate cuts more likely than hikes in the coming months.

There are certainly risks from pivoting before it becomes clear that inflation is sustainably headed back to target. But policymakers have been extremely effective the last few quarters. The global economy appears on track for a soft landing, which few expected a year ago. The combination of aggressive rate hikes and multiple shocks—geopolitical and other—had most observers forecasting a recession, potentially severe, in 2023. While a soft landing isn’t guaranteed, we think central bankers deserve the benefit of the doubt for now.

Markets seem more than happy to grant that benefit. Equities, for example, surged and interest rates plunged as policy rhetoric understandably changed in the fourth quarter. A soft economic landing AND rate cuts provide the best of both worlds for financial markets. As in recent quarters, there’s a circularity to the interaction between markets and central banks. The more that markets believe central banks are dovish, the less likely policymakers can deliver what markets expect. In fact, easing of financial conditions associated with December’s pivot could itself limit the magnitude of coming rate cuts. Nonetheless, we believe cuts are coming—which just leaves the questions of how soon, how fast and how far. Any disappointment across these axes could spark market volatility, but the travel direction toward lower policy rates seems clear.

Evidence supporting near-term rate cuts is weakest in the US. Growth ran hot for most of 2023 and, while now slowing, it seems likely to remain positive in 2024. Our forecast is for GDP to expand, albeit at a subdued rate by historical standards, in the coming quarters. Below-trend growth should support gradual disinflation and that combination should allow for the Federal Reserve to cut interest rates. We’re skeptical of the early start and aggressive pace of easing currently priced into financial markets, however, since that path seems more consistent with a hard landing than a soft one. We instead foresee an easing cycle in which the Fed cuts rates to bring the economy back into equilibrium, not to forestall a recession: in other words, a cycle driven by choice rather than out of necessity. The determining variable is likely to be the labor market. If it weakens sharply, aggressive rate cuts are very possible. Our base case for GDP, however, suggests a more modest rebalancing and thus a later start and more gradual pace of easing.

The euro area appears further along its disinflationary path than the US, though core inflation remains well above target for now. The European Central Bank’s (ECB’s) single mandate to maintain price stability suggests that it will need to be cautious rather than aggressive in the near term. But relatively weaker economic performance should give the ECB confidence that inflation will decline to its target in the coming quarters. The UK has borne the worst of both worlds this cycle: the highest inflation and the weakest growth of the G3. Recent progress on inflation is welcome news, but there’s still a long way to go and we anticipate the Bank of England (BoE) will be last of the G3 to cut.

The largest Asian economies remain off-cycle with their western peers. While the Fed, the ECB and the BoE seek signs that inflation is headed sustainably lower, the Bank of Japan (BoJ) wants evidence that inflation’s recent move higher is sustainable. Once it’s confident that this is the case, which we expect later this year, we anticipate an end to yield curve control and an exit from the central bank’s negative policy-rate regime. This means that the BOJ will be tightening while other central banks are easing, which we expect to boost the yen after its significant weakening this cycle.

In China, the policy imperative remains both supporting growth and fighting disinflation. We’re still confident that policymakers have the tools to do it. As in recent quarters, however, investors should limit their expectations, since policy objective is more about managing a long-term, structural slowdown than producing near-term acceleration.

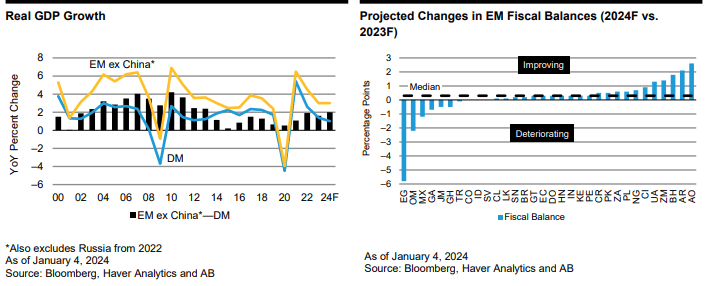

Other emerging-market ((EM)) economies have been challenged by high global interest rates, a strong US dollar, geopolitical instability and sluggish growth in China, but have still managed to grow in line with historical norms. We expect EM growth to remain relatively steady in 2024 (amid softer developed-market ((DM)) growth) as EM monetary easing takes effect and global financial conditions ease.

Looming over any economic forecast for 2024 is massive political uncertainty. US elections are the main event, and the legal issues around them this cycle make the calendar alone an unreliable predictor of when risk events could occur. For instance, disfunction in Washington, DC, well before the election means that the federal government shutdown avoided last quarter could resurface. Elsewhere, more than 60 countries will hold potentially meaningful elections this year. And, of course, conflicts in Europe and the Middle East could be disruptive, even though markets have so far largely concluded that their economic impacts are likely to be limited.

Financial markets enter 2024 on firm footing, buoyed by the idea that central banks will be cutting rates even as growth remains positive. We generally share that optimism. Nonetheless, there are many reasons to remain watchful, both known and unknown. It’s obviously good to start a year with a relatively upbeat outlook, but one need not look very far to the past for a reminder that things can, and often do, change quickly.

Global Macro Outlook: The Next Six Months

{kind=link}

Global Forecast

Forecast Overview

{kind=link}

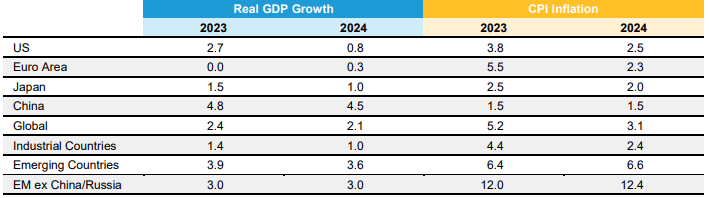

AB Growth and Inflation Forecasts (Percent)

{kind=link}

*US GDP forecasts presented as 4Q/4Q; others YoY; US CPI reflects core inflation; others are headline. As of January 2, 2024

Source: AllianceBernstein ((AB))

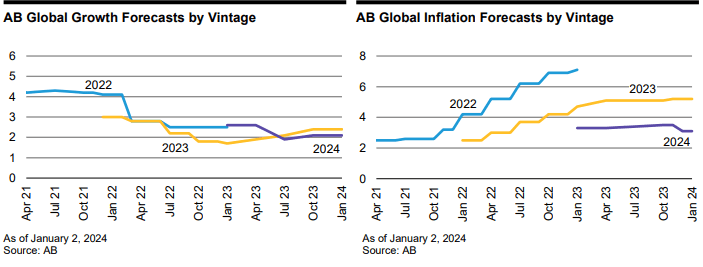

Forecasts Through Time

{kind=link}

US

{kind=link}

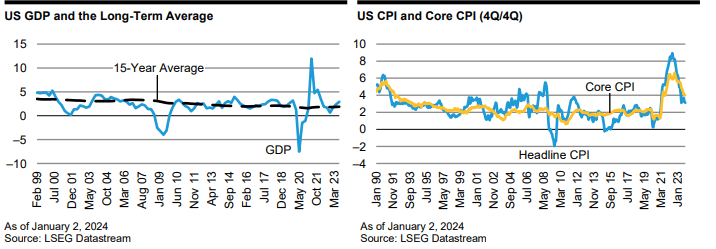

- The US economy exceeded all but the most optimistic expectations in 2023, thriving even as the Fed raised rates. We believe a slowdown is imminent, driven in large part by the lagged impact of past interest-rate increases. But we expect a slowdown to be fairly mild by historical standards, and even unlikely to be recessionary. This looks like a very soft landing indeed.

- The key variable from a growth perspective is the labor market. Solid real income growth has supported consumption and thus economic activity more broadly. We expect this to continue in the coming months, albeit to a lesser degree. The labor market has not yet fully rebalanced, but the process is underway.

- Despite decent growth, we expect inflation to continue its downward trajectory. Goods prices are basically flat year over year (YoY), and the ongoing rebalancing of the labor market should allow for services inflation to decelerate as well. It will take time before inflation falls all the way to the Fed’s 2% YoY target, but the worst of the inflation shock is clearly behind us.

- If last year was all about how fast and how far rates would rise, this year should be the opposite. We expect the Fed to start cutting rates in either the second or third quarter and proceed at a steady but gradual pace as it strives to bring the economy into balance.

Risk Factors

- It’s impossible to look ahead in 2024 without acknowledging looming political risk. It starts with the possibility of a government shutdown, followed by an electoral cycle that has the potential to be extremely disruptive across multiple dimensions. Therefore, it’s possible—even likely—that politics will drive markets more than economics in 2024. This would be a break from the usual pattern of how markets look through politics to focus on the underlying economic path. Then again, the path forward this time may hinge on politics much more than in the past.

Overview

The economic outlook didn’t change significantly over the last three months, despite significant market volatility. The most likely way forward is a moderate slowdown accompanied by gradual disinflation. What did change was the policy setting. The Fed has pivoted from an all-hands battle with inflation to a more balanced approach, signaling that they’re increasingly comfortable that inflation is sustainably headed back to target. Whether they’re right depends on how patient one is willing to be. We agree that inflation is headed back to target but expect it to take several quarters to get there. Given the progress already made on inflation and the elevated level of the policy rate, the Fed’s pivot makes sense even given that protracted timetable, though there’s still some risk. The lesson of the 1970s is that prematurely easing conditions can trigger a reacceleration in inflation. The risk of this outcome seems much lower today, largely because long-term inflation expectations have remained well anchored throughout the cycle. That’s an important variable, and one that we’ll continue to monitor.

Of more proximate importance is the state of the labor market, which we believe will be the determining variable in setting the timing and pace of rate cuts. The gradual rebalancing of the workforce that we envision suggests a similarly gradual and modest economic slowdown that should lead to rate cuts starting in the second quarter. The market is pricing a more aggressive path that seems to suggest a harder economic landing than we envision. Time, and the data, will tell.

Of course, no forward-looking analysis can ignore anticipated risks, of which politics are foremost. We have no ability to forecast the upcoming election nor any inclination to try. But we can say that the risk of an outcome that disrupts markets and even the economy is uncomfortably high—much higher than in a typical election cycle.

{kind=link}

China

{kind=link}

Outlook

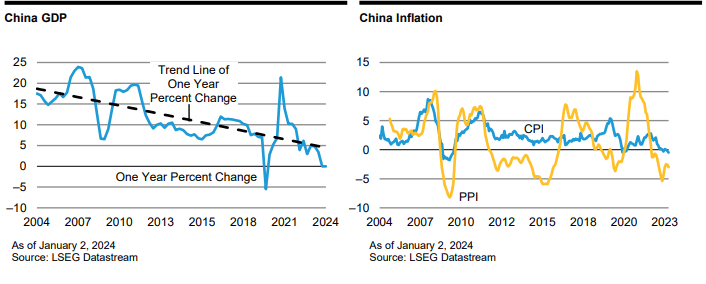

- China’s economy is undergoing a structural slowdown. There will be short-term vacillations around this trend, but the long-term trajectory is clearly toward slower growth.

- As the global economy cools, it’s likely that China’s economy will require additional domestic support in the form of both monetary and fiscal stimulus in the coming months. What form that support takes is an open question; policymakers’ objective is to stabilize growth while minimizing the imbalances that stimulus can create, particularly in the property sector.

- Fortunately, inflation is not a near-term concern in China; if anything, inflation is too low, which gives authorities space to ease conditions as needed.

Risk Factors

- It will take considerable skill to provide the necessary support to the economy without exacerbating existing imbalances. Too much stimulus, or misdirected policy, could pile more bad debt on top of the large amount already there or reinflate a property bubble. Both might help growth in the near term but at the cost of future instability.

- China’s financial market is opaque, and it’s unclear how much it reflects the underlying economy. The risk of a disruptive market event, especially in the credit sector, is elevated and could prove problematic for authorities and investors alike.

Overview

So far, so good for policymakers in China. Easing measures up to this point have stabilized growth and avoided the worst sorts of economic and market outcomes. The risk that the system spirals out of control is ever-present and there’s no guarantee it won’t, but we don’t expect that outcome across a reasonable forecast horizon. Slow growth and low inflation provide policymakers with ample room to do what it takes to keep growth stable.

Stable, of course, is not what China investors may be looking for. After years of very strong growth, humbler targets are a tough adjustment for many investors, domestic and external. But it’s an adjustment they’ll have to make, as we see it. It’s neither sustainable nor desirable for authorities to do what it would take to push the world’s second-largest economy onto a more rapid growth trajectory. We believe that it’s better by far to just manage the downside around the growth path rather than trying to inject more upside. We’re confident that Chinese authorities agree with that assessment and thus are comfortable forecasting steadily decelerating—but not collapsing—growth into 2024 and beyond.

{kind=link}

Euro Area

{kind=link}

Outlook

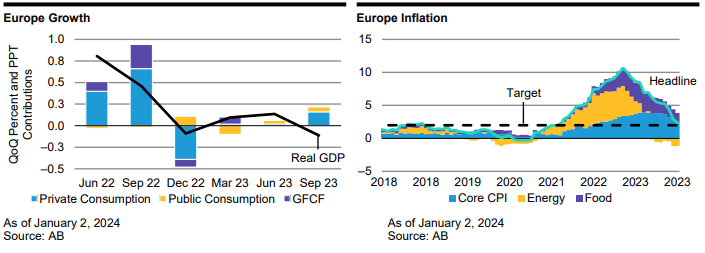

- Euro area inflation is easing more rapidly than anticipated. While the drag from energy prices should wane, indicators of underlying inflationary pressures signal faster convergence towards the inflation target.

- As inflation falls, real incomes should turn positive, allowing consumption to rebound more substantially in 2024. In addition, labor markets remain resilient, which should also continue to provide support to consumers.

- However, headwinds persist. Weakness evident at the end of 2023 will carry into 2024. Monetary policy remains restrictive and its lagged impact on private demand should continue to bite. Meanwhile, fiscal policy will turn increasingly restrictive as governments withdraw energy-related support.

- Overall, activity in 2024 should modestly rebound but remain subdued after a weak start for the year. In that context, the ECB will remain on hold for now, waiting for further evidence that inflation consistently converges to its target.

Risk factors

- Ongoing Middle East tensions have thus far not provoked an increase in energy prices. However, uncertainty remains on the evolution of the conflict. Another energy shock could slow or even reverse disinflation in the euro area, given its dependence on imported energy. Likewise, core goods inflation could increase again if supply chains are significantly disrupted by blockades in the Red Sea.

Overview

Inflation’s steady decline highlighted the fourth quarter in the euro area. Falling energy prices have been a strong driver of disinflation so far, but now food and core inflation have also contributed substantially. Easing pressure from core inflation, services specifically, is more than welcome and will likely be a growing component of disinflation in the months ahead. Indeed, while negative base effects from energy prices should reverse at the beginning of the year, core inflation will continue to diminish amid subdued growth.

Activity in the third quarter of 2023 mildly contracted, driven by falling inventories, but private consumption and investment held up better. However, we expect growth to have pulled back again in the fourth quarter, depending on final data, and therefore should carry weak momentum further into 2024. While consumption should rebound and support growth in 2024, the extent of that recovery seems to be on the weaker side for the first half of the year. In that context, improving but nevertheless weak growth seems the most likely scenario for the euro area.

There are several implications for monetary policy. A rebound in growth, even if mild, will enable the ECB to remain patient while building confidence that inflation is indeed falling back to target. Secondly, rate cut discussions will eventually materialize in the face of rapidly easing inflationary pressures and underperforming activity. We believe that inflation and a wide range of data, together with new projections, will eventually open the door to rate cuts.

{kind=link}

UK

{kind=link}

Overview

As in the euro area, inflation in the UK accelerated its downward march. Energy prices fell much more dramatically in the fourth quarter, stripping off a significant contribution to inflation. Encouragingly, disinflation was not solely confined to the energy component: food inflation remains high but is trending down and core inflation has also cooled. On the latter, further signs of easing will be required for the Bank of England to abandon its hawkish bias. Compared with the euro area, second-round effects from the energy shock were much more forceful in the UK—leading to strong and simultaneous wage and service inflation—and are taking longer to unwind. Looking ahead, we expect these inflationary factors to weaken: the labor market, including wage growth, is progressively easing, while economic fundamentals remain weak.

Meanwhile, the impact of monetary tightening on activity seems to have intensified in the second half of 2023. Interest-rate-sensitive drivers of growth, consumption and business investment, contracted in the third quarter and are expected to remain weak. Like elsewhere, falling inflation should allow consumption to rebound but only mildly and not in the very near term. At the same time, some evidence suggests that labor market strength is diminishing and will be less supportive for consumers in 2024. Overall, a subdued rebound in growth and faster disinflation best characterize the outlook in the UK.

Japan

{kind=link}

Overview

Japan’s economy continues to progress toward sustainably higher inflation, and the Bank of Japan continues to accommodate that process. The nature of policymaking in Japan means that changes to monetary policy are less predictable than elsewhere: almost alone among major central banks, the BOJ believes that surprising the market is valuable. That makes it very difficult to know when precisely the turn will come, including for us. We do expect, however, that over the course of the next few quarters, the BOJ will exit yield curve control and begin to move away from negative policy rates. This should help the yen regain some of the ground it has lost over the past few quarters.

Emerging Markets

{kind=link}

Outlook

- We expect EM growth to remain steady in 2024 as monetary easing takes effect and global financial conditions ease.

- The projected stability in EM growth is noteworthy because it defies the projected cyclical slowdown in DM and the structural slowdown in China. In fact, moderating growth in China appears to have created opportunities for other large EM countries to fill some of the void, while there are several idiosyncratic bright spots, too.

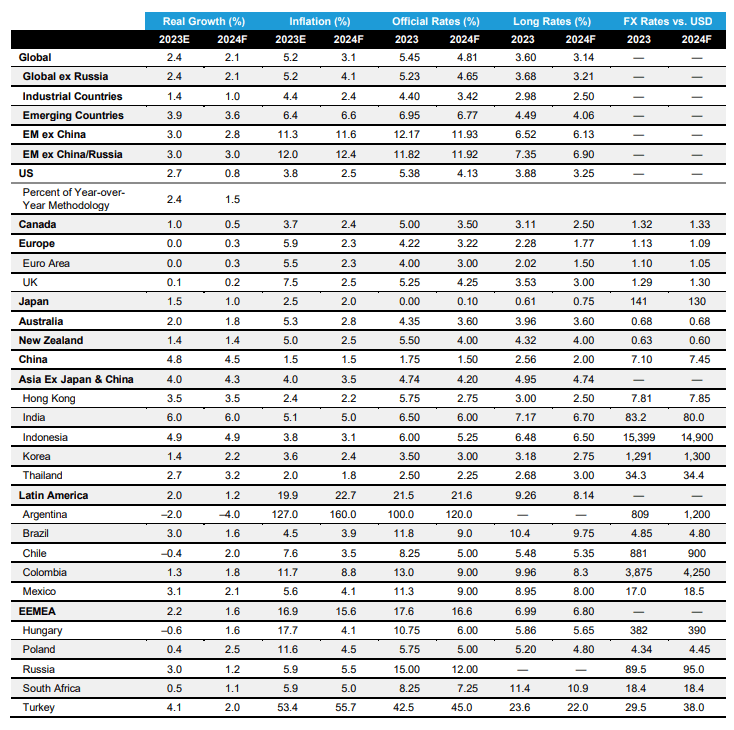

- We think EM regions that effectively drive fiscal stability/consolidation to complement monetary policy easing could outperform in 2024.

Risk Factors

- The projected slowdown in DM growth is a risk, but it might only be disruptive to the EM outlook if inflation is stickier than expected.

- US elections will likely shift to the center of investors’ radars as the year progresses, but numerous national and local elections across EM could also shape financial markets.

Overview

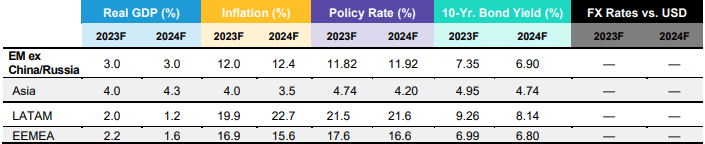

Emerging-market ((EM)) economies have been challenged by high interest rates, a relatively strong US dollar, geopolitical instability and sluggish growth in China over the past year, but still managed to grow in line with historical norms (c.3% for EM excluding China and Russia). EM assets performed relatively well in this environment, with total returns surpassing the annual averages for the past decade. We expect EM growth to remain steady in 2024 as monetary easing takes effect and global financial conditions ease. The projected slowdown in DM growth is a risk, but it might only be disruptive to the EM outlook if DM inflation is stickier than expected, such as a stagflationary scenario that binds central banks’ hands.

We expect disinflation to continue, but we are now in the slower part of the disinflationary process, with risks to the outlook evenly balanced. The duration-friendly global backdrop should, however, continue to support EM duration.

The projected stability in EM growth is noteworthy because it defies the projected cyclical slowdown in DM and the structural slowdown in China. In fact, moderating growth in China appears to have created opportunities elsewhere in EM, like India and Indonesia, to fill some of the void. But there are several idiosyncratic bright spots too, with growth in Pakistan, Senegal and Sri Lanka expected to accelerate meaningfully in 2024. Our expectation of relatively robust economic growth and fiscal improvement— particularly in lower-rated sovereigns—sets the stage for solid returns in 2024. But as the global economy appears to be in transition, and as geopolitical risks rise (potentially fueled by the heavy election calendar), risks to the outlook remain elevated.

Geopolitical dislocations are difficult to predict or position for, but they could be an important driver of this year’s trajectory. The outbreak of the Israel-Hamas war in October 2023 presents geopolitical challenges that pose potential global macroeconomic risks requiring careful monitoring. The war has remained largely contained in the Gaza Strip, and a direct military confrontation between Israel and Iran has been avoided, easing fears of energy supply disruptions in the Strait of Hormuz. That said, Iran's proxies—in particular Houthi rebels—have threatened international trade flows in the Red Sea and forced several cargo ships to reroute via the Cape of Good Hope. This has elevated concerns about rising shipping costs, renewed supply chain disruptions and subsequent price pressures. The spillover to global inflation dynamics still remains unclear and will largely depend on the duration of these and other disruptions.

US elections will likely shift to the center of investors’ radars as the year progresses, but numerous national and local elections in EM could be important too. Some of the key elections include Indonesia (February), South Africa (around May) and Mexico (June). But local elections in Turkey and Brazil will be closely watched too. Fiscal policy choices that precede and/or follow these elections could be important factors in staying with the duration-friendly backdrop.

Indonesia’s elections might go to two rounds, which shouldn’t be destabilizing; in fact, policy continuity could be the most likely outcome. In contrast, South Africa’s elections entail more fiscal and market risks, with social spending pressures mounting as the ruling ANC might struggle to cross the 50% threshold that allows them to govern without forming potentially fractious coalitions. Mexico’s elections are not expected to create concerns around sharp policy changes. But fiscal prospects could be questioned by market participants as tax reform and financing of Pemex will resurface as focal points for policy making. We think emerging markets that effectively drive fiscal stability/consolidation to complement monetary policy easing could outperform this year.

{kind=link}

Forecast Table

{kind=link}

Growth and inflation forecasts are calendar year averages except US GDP, which is forecast as 4Q/4Q. Interest-rate and FX rates are year-end forecasts.

Long rates are 10-year yields unless otherwise indicated.

The long rates aggregate excludes Argentina and Russia; Argentina is not forecast due to distortions in the local financial market; Russia is not forecast because the local market is inaccessible to foreign investors.

Real growth aggregates represent 29 country forecasts, not all of which are shown.

Investment Risks to Consider

The value of an investment can go down as well as up and investors may not get back the full amount they invested. Past performance does not guarantee future results.

Important Information

Note to All Readers: The information contained here reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion in this material will be realized. Past performance does not guarantee future results. The views expressed here may change at any time after the date of this publication. This document is for informational purposes only and does not constitute investment advice. AllianceBernstein L.P. does not provide tax, legal or accounting advice. It does not take an investor's personal investment objectives or financial situation into account; investors should discuss their individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer or solicitation for the purchase or sale of any financial instrument, product or service sponsored by AB or its affiliates. Note to Canadian Readers: This publication has been provided by AB Canada, Inc. or Sanford C. Bernstein & Co., LLC and is for general information purposes only. It should not be construed as advice as to the investing in or the buying or selling of securities, or as an activity in furtherance of a trade in securities. Neither AB Institutional Investments nor AB L.P. provides investment advice or deals in securities in Canada. Note to European Readers: This information is issued by AllianceBernstein Limited, a company registered in England under company number 2551144. AllianceBernstein Limited is authorized and regulated in the UK by the Financial Conduct Authority (FCA -Reference Number 147956). Note to Readers in Japan: This document has been provided by AllianceBernstein Japan Ltd. AllianceBernstein Japan Ltd. is a registered investment-management company (registration number: Kanto Local Financial Bureau no. 303). It is also a member of the Japan Investment Advisers Association; the Investment Trusts Association, Japan; the Japan Securities Dealers Association; and the Type II Financial Instruments Firms Association. The product/service may not be offered or sold in Japan; this document is not made to solicit investment. Note to Australian Readers: This document has been issued by AllianceBernstein Australia Limited (ABN 53 095 022 718 and AFSL 230698). Information in this document is intended only for persons who qualify as "wholesale clients," as defined in the Corporations Act 2001 (Cth of Australia) and should not be construed as advice. Note to Singapore Readers: This document has been issued by AllianceBernstein (Singapore) Ltd. (“ABSL”, Company Registration No. 199703364C). AllianceBernstein (Luxembourg) S.à r.l. is the management company of the portfolio and has appointed ABSL as its agent for service of process and as its Singapore representative. AllianceBernstein (Singapore) Ltd. is regulated by the Monetary Authority of Singapore. This advertisement has not been reviewed by the Monetary Authority of Singapore. Note to Hong Kong Readers: This document is issued in Hong Kong by AllianceBernstein Hong Kong Limited, a licensed entity regulated by the Hong Kong Securities and Futures Commission. This document has not been reviewed by the Hong Kong Securities and Futures Commission. Note to Readers in Vietnam, the Philippines, Brunei, Thailand, Indonesia, China, Taiwan and India: This document is provided solely for the informational purposes of institutional investors and is not investment advice, nor is it intended to be an offer or solicitation, and does not pertain to the specific investment objectives, financial situation or particular needs of any person to whom it is sent. This document is not an advertisement and is not intended for public use or additional distribution. AB is not licensed to, and does not purport to, conduct any business or offer any services in any of the above countries. Note to Readers in Malaysia: Nothing in this document should be construed as an invitation or offer to subscribe to or purchase any securities, nor is it an offering of fund-management services, advice, analysis or a report concerning securities. AB is not licensed to, and does not purport to, conduct any business or offer any services in Malaysia. Without prejudice to the generality of the foregoing, AB does not hold a capital-markets services license under the Capital Markets & Services Act 2007 of Malaysia, and does not, nor does it purport to, deal in securities, trade in futures contracts, manage funds, offer corporate finance or investment advice, or provide financial-planning services in Malaysia. Important Note for UK and EU Readers: For Professional Client or Investment Professional use only. Not for inspection by distribution or quotation to, the general public.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

www.alliancebernstein.com

© 2024 AllianceBernstein L.P.

UMF-479351-2024-01-11

ICN20240085

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Global Macro Outlook - First Quarter 2024