ASHR - Global Macro Outlook - Third Quarter 2023

2023-07-05 01:20:00 ET

Summary

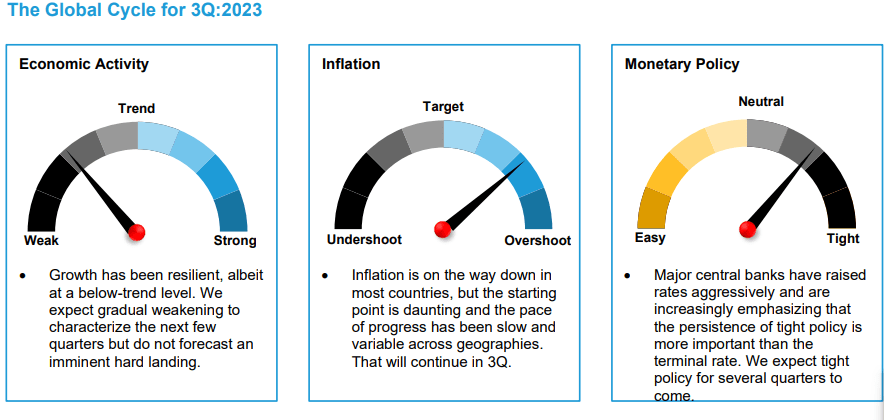

- The US economy has remained remarkably resilient in the face of repeated shocks, most recently the regional bank turmoil in March.

- China’s economy disappointed our, and the market’s, expectations in 2Q. In contrast to other major economies, the growth boost from reopening after the pandemic faded quite quickly, leaving the economy looking wobbly.

- Europe’s economy is weathering the storm of the Russia–Ukraine war quite well, though the marginally negative growth rate of GDP over recent quarters makes clear that it wasn’t entirely smooth sailing.

The Macro Picture

Regional banking turbulence in the US and the failure of Credit Suisse ( CS ) in March did not put an end to the economic expansion, nor did it signal the beginning of a systemic crisis. Likewise, the global economy didn’t fall into recession when confronted with Russia’s invasion of Ukraine, China’s prolonged adherence to its zero-COVID policy, or the rapid rise in policy rates across the US and Europe.

Indeed, the continued resilience of the global economy is the most noteworthy development of the second quarter. There’s little reason to believe that the outlook has meaningfully improved, but downside risks around the sluggish growth trajectory that remains our strongly-held base case have clearly diminished. In fact, the risk of an imminent hard landing is lower today than it was three months ago.

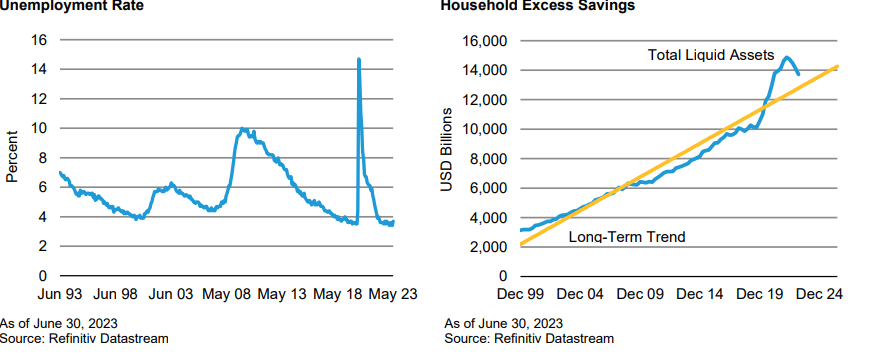

Why has the system proven so resilient? The key variable in developed economies is the labor market. Employment growth remains strong, unemployment remains low and wage growth has kept pace with inflation in most major economies - with the UK being a notable exception. This has allowed households to manage their way through challenging times and smoothed out the bumps in the business cycle.

We still expect growth to slow in time - rate hikes are already weighing on activity in many sectors, and households have begun to deplete savings cushions accumulated during the pandemic.

Whether or not this eventually leads to a recession is a close call. But the evidence in hand suggests that if a downturn occurs, it is likely to be mild by recent historical standards. Rather than a sharp contraction, our forecasts reflect a protracted period of below-trend growth lasting through 2024.

Why such a long period of slow growth? In large part, the cause is the same economic resilience that has characterized 2023. Resilient growth, especially across labor markets, means that global inflation is likely to fall only slowly. Sticky inflation implies that central bankers are likely to raise rates farther than expected and to keep policy rates in restrictive territory for a while. Higher for longer is the new policy regime, and it played out in the second quarter.

Central banks in several countries, notably Australia and Canada, were forced to resume rate hikes after signaling an end to tightening with the expectation that inflation risks had faded. The Fed and the European Central Bank (ECB) have both indicated that the terminal rate is likely to be higher than they expected. Moreover, the Bank of England (BoE) faced renewed acceleration in inflation, resulting in a much higher rate profile than initially thought.

Higher-than-expected rate peaks may be front of mind today, but we believe the more important variable over time will be how long rates stay elevated. Given the resilience of labor markets and, thus, the economy, we take seriously the possibility that rates could stay high for several quarters to come.

Until central banks are confident that inflation will fall back to target, they’ll likely be cautious about cutting rates to support growth - even once economies weaken. We believe that the impact of persistently tight policy will be persistently soft growth. The consequence of a soft landing will be a tepid rebound, and as a result we anticipate that growth will remain weak across the forecast horizon.

There are, of course, risks that surround our base case. While the ongoing tightening cycle has not yet caused durable disorder in financial markets, history suggests that we need to remain wary - tightening cycles often end in financial turbulence. China, too, remains a downside risk. Growth briefly picked up when its zero-COVID-19 policy was lifted.

But recent data suggest that additional policy stimulus will be required to keep the economy on track. Should that stimulus be too little or too late, a hard landing in China could prove disruptive. And, of course, the disinflation we expect throughout the western world remains more forecast than reality: inflation has yet to come down. If it doesn’t, policymakers may have to emphasize “higher” before focusing on “longer.”

From a market perspective, as we have observed in past quarters, a sustained period of below-trend growth argues for caution but not panic. Absent a hard landing, markets may struggle to sustain momentum in either direction, rewarding those willing to be patient through the inevitable bumps along the way.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

- The US economy has remained remarkably resilient in the face of repeated shocks, most recently the regional bank turmoil in March. Strong labor markets have supported real incomes and savings accumulated during the pandemic have provided enough of a cushion for households to keep consumption solid.

- There is increasingly clear evidence that inflation is likely to fall in the coming months as the lagged impact of past house price increases works its way through the system. With goods prices already back to the pre-pandemic norm, the key variable will be services inflation.

- In contrast to goods prices, which were elevated largely due to supply-chain disruptions, services prices resonate with the labor market. As a result, the Fed will not be convinced that inflation is moving sustainably lower until the labor market weakens.

- In the absence of labor market weakening, the Fed’s monetary policy stance is “higher for longer.” We have added a third quarter (3Q) rate hike to our forecast and an additional hike in the fourth quarter (4Q) is a realistic possibility, if not yet our base case. Economic resilience and a strong labor market mean both that the Fed can afford to raise rates farther and that it may need to do so to ensure that inflation converges to target within a reasonable time horizon.

Risk Factors

- As in all tightening cycles, the primary risk is that higher rates cause a non-linearity in the financial system, in which something systemic breaks and causes a sudden stop in the economy. The regional bank turbulence didn’t do this, but the possibility of a disruptive event remains, even if the nature of that event is unknowable ahead of time.

- If the labor market doesn’t weaken in the coming months, interest rates could move meaningfully higher. Periods in which the market has had to adjust its pricing for more aggressive tightening have generally not been good for risk assets.

Overview

Three months ago, it appeared that regional banking stress could upend the economy. It didn’t happen. We’ve instead seen a modest credit contraction as regional bank deposits stabilized at lower levels, but that is better described as a headwind to growth than the early stages of a crisis. Indeed, slowing growth remains the primary challenge for policymakers, and in that respect slower credit extension may prove helpful in the process of economic rebalancing.

This is likely to play out over several quarters, however, and inflation is too high right now. To be sure, there is good reason to expect inflation to come down. The lagged impact of housing prices and the health of the global supply chain both argue that inflation will slow. But the labor market remains robust, which best explains the increase in services prices across the economy.

Until the labor market weakens appreciably, it will be foolhardy to have confidence that inflation will return to target over a reasonable time horizon. As a result, the Fed, like other central banks, has added rate hikes to its expectations and extended the period over which it expects to maintain restrictive policy. Rates will be higher for longer - until the labor market weakens and growth slows, increasing confidence in inflation convergence.

We expect higher rates to slow growth in the coming quarters, even while acknowledging that growth has exceeded our expectations so far in 2023. For now, it looks very much like a soft landing, however. If there is a recession in the coming quarters, it looks likely to be quite mild by historical standards.

{kind=link}

{kind=link}

Outlook

- China’s economy disappointed our, and the market’s, expectations in 2Q. In contrast to other major economies, the growth boost from reopening after the pandemic faded quite quickly, leaving the economy looking wobbly.

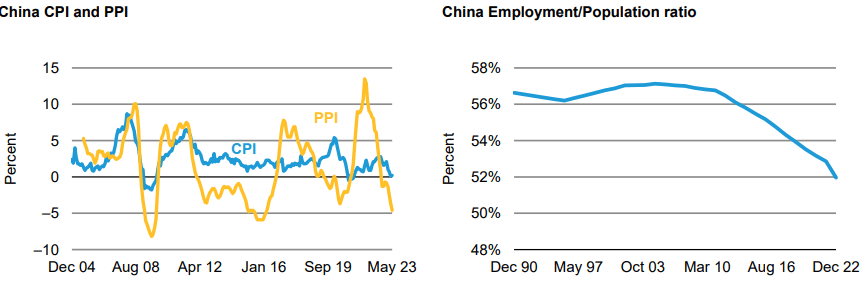

- There are many explanations for disappointing performance, but the common factor is that China is in the midst of a secular, multi-year slowdown. Demographic realities and challenged relations with major trading partners mean that potential growth is lower and that even cyclical upturns will bump up against those constraints.

- Weaker-than-expected growth does not mean that a crisis, or a hard landing, is imminent. We continue to expect policymakers to support the economy in the name of preserving the social contract: the government will provide economic stability in exchange for unquestioned control.

- In the meantime, we note the easing of monetary policy in 2Q and anticipate fiscal easing in the second half of 2023 to keep top-line growth more or less in line with the official 5% to 5.5% GDP growth target for the year.

Risk Factors

- If policymakers provide too little stimulus, or are too late, the downside risks evident in the current environment could persist.

- While domestic politics seem unlikely to be disruptive, China’s efforts to play a larger role in world events are raising tensions with other countries. To the extent that tensions spill into economic policy, it will be a headwind to future growth.

Overview

China’s economy is stuck. The aging of the population and a desired (and desirable) transition from a heavy investment, export-oriented growth model both mean slower growth in the next few years. Demographics are destiny, after all, and no major economic transition comes without friction.

The challenge for policymakers is that slower growth is unacceptable. The social contract in China, in essence, is that the government will provide economic stability in exchange for unquestioned authority. If the government cannot provide the former, it risks the latter. Thus, we anticipate stimulus measures to support growth in the coming months.

What will those measures look like? The major challenge for authorities is a shortfall in demand. We believe that monetary policy will not be sufficient to boost demand. Over the long term, the creation of a social safety net that would allow workers to spend rather than save to care for their aging parents, would be the best policy.

But that’s not a short-term fix. Instead, it will likely come down to government spending to boost demand. This is consistent with the broader contours of economic policy under Premier Xi, in which the state is playing an ever-increasing role in economic life. As a result, that is what we anticipate: government and quasi-government spending will go up to keep growth on a stable trajectory. Whether that spending is efficient is a question for a later day.

{kind=link}

{kind=link}

Overview

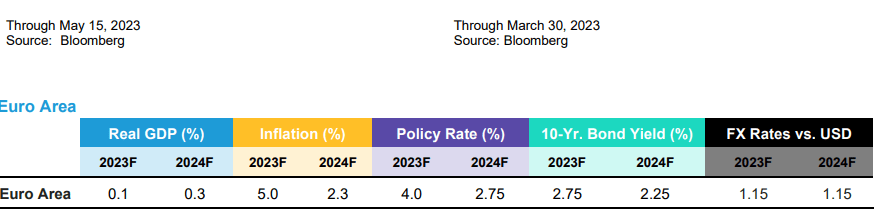

Europe’s economy is weathering the storm of the Russia–Ukraine war quite well, though the marginally negative growth rate of GDP over recent quarters makes it clear that it wasn’t entirely smooth sailing. Still, with the labor market strong and other indicators of economic performance stable, we view recent economic performance favorably relative to expectations.

The consequence of economic stability has been higher inflation. The euro area may have seen the peak in core inflation late in 2Q, but it’s not yet a sure thing, nor is it clear how quickly inflation will decelerate once it has definitively peaked.

As a result, the ECB remains on high alert, and we expect additional rate hikes in 3Q and potentially beyond. Remember that, in contrast to the Fed, the ECB does not have a dual mandate: their sole focus is inflation. As a result, we expect that the ECB has more ground to cover than does the Federal Open Market Committee ((FOMC)) before concluding its tightening cycle.

{kind=link}

Overview

The UK economy remains in very difficult circumstances. Inflation, which had appeared to be heading lower, instead reaccelerated sharply in 2Q. That forced the BoE into reaccelerating its rate-hiking cycle and signaling that the peak in rates is not yet in sight.

To be sure, there are reasons to think that the idiosyncrasies that have pushed UK inflation higher will fade. Food prices have started to decelerate, along with those of core goods.

Producer prices, which measure pressure in the economic pipeline, have decelerated sharply and we expect this to pass through to consumer-facing inflation in the coming months. Still, there’s a very long way to go.

The persistence of inflation means that UK household income is falling in inflation-adjusted terms, in contrast to the US and Eurozone experience. As a result, we anticipate a recession in the UK, likely starting later this year and lasting into 2024.

{kind=link}

Overview

After tweaking its yield-curve control policy a few months ago, the Bank of Japan ((BOJ)) has since maintained its “as-is” stance. We believe this is the right call - inflation in their economy still hasn’t decisively moved into an acceptable range.

With the new BOJ leadership appearing inclined to be patient, there’s hope that might happen. In the meantime, the most obvious consequence of the BOJ remaining accommodative, while other central banks move ever further into restrictive territory, is that the yen is likely to remain weak.

{kind=link}

Outlook

- By leading the interest-rate hiking cycle, EM central banks built a credible interest-rate cushion that provided some protection for EM currencies. Leading the easing cycle is riskier.

- We think growth and trade dynamics might become increasingly important for EM currencies over the next 12 months.

Risk Factors

- World trade volumes have been losing momentum, the US Treasury curve continues to signal recession, and China’s economic recovery does not, in our view, have the strength or the structure to propel EM growth.

- We think cyclical headwinds continue to argue against meaningful exposure to EM high-yield debt, but there are idiosyncratic green shoots which could spread quickly once the global economic trough is in the rearview mirror.

Overview

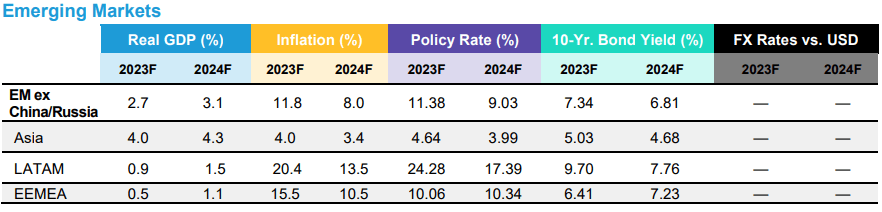

Emerging markets ((EM)) are at a crossroads. They have generally reached the end of their interest-rate hiking cycles and stand ready to commence easing. But the direction of monetary policy in developed markets ((DM)) is not as clear, and that means there’s a risk of being wrong-footed if the DM hiking cycle gets extended.

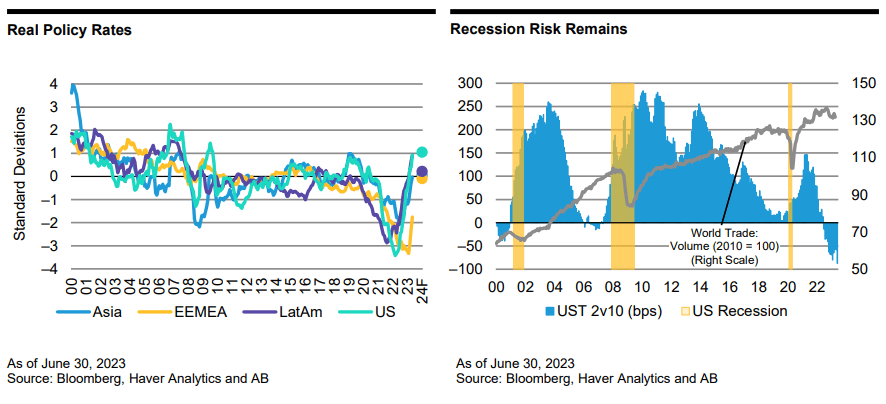

By leading the interest-rate hiking cycle, EM central banks built a credible rate cushion that provided some protection for EM currencies. Leading the easing cycle is riskier and could put pressure on EM currencies. Our forecasts through 2024 point to a normalization in EM real policy rates versus a relatively restrictive US real policy rate (see Figure 1).

While these projected interest-rate trends could indeed weigh on EM currencies, we think growth and trade dynamics might become increasingly important for EM currencies over the next 12 months.

There are red flags on this front too: world trade volumes have been losing momentum, the US Treasury yield curve continues to signal recession, and China’s economic recovery does not, in our view, have the strength or the structure to propel EM growth (see Figure 2).

There are, however, pockets of economic strength in Latin America and Asia, which could be bolstered if EMs start cutting rates in the second half of the year. We project only a mild acceleration in EM growth (excluding China and Russia) through 2024, but that looks somewhat better than the projected path for DM.

That’s not the optimal growth balance for EM asset prices, and as long as the risk of a deep and disruptive recession lingers, upside potential for EM asset prices will likely be capped. Diverging monetary policy and growth dynamics (in EM’s favor), and relatively stretched US dollar valuations, might, however, be net positive for EM asset prices over the next 12 months.

The high-yield external debt space remains littered with credits in distress, with varying degrees of progress made to quell concerns about default (Ecuador, Egypt and Pakistan, for example) and varying degrees of progress to resolve defaults (Ghana, Sri Lanka and Zambia, for example). In Ecuador, political risk remains elevated with regime change on the cards - snap elections are scheduled in the second half of the year.

In Egypt, there’s been limited progress on asset sales and FX rigidity remains a point of contention, with a low probability of resolution in the near term. Default and restructuring of debt seemed almost inevitable in Pakistan, but the eleventh-hour agreement between IMF staff and the Pakistani authorities on policies supported by a Stand-By Arrangement provided a lifeline.

Of the countries that have already defaulted, Ghana has made swift progress with its debt restructuring. The country’s domestic debt exchange program was concluded in February 2023 and the external debt creditor committee recently provided the necessary financing assurances to allow fund disbursement from the IMF.

In Sri Lanka, there is uncertainty about the government’s commitment to local debt restructuring and the extent to which China will participate in the restructuring process. Zambia’s agreement with official creditors on debt treatment under the G20 Common Framework is noteworthy because it’s generally been seen as a test case of the efficacy of the Common Framework amid meaningful debt obligations to China. Zambia’s progress might thus be a positive signal for Sri Lanka too.

The aggregate EM high-yield debt space is certainly not out of the woods - the global economic slowdown and lack of market access will remain challenging for many frontier countries. We think cyclical headwinds continue to argue against meaningful exposure to this section of the EM universe, but there are idiosyncratic green shoots which could spread quickly once the global economic trough is behind us.

{kind=link}

{kind=link}

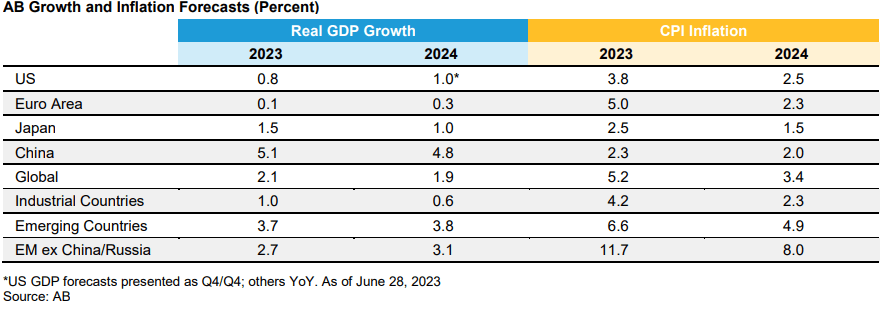

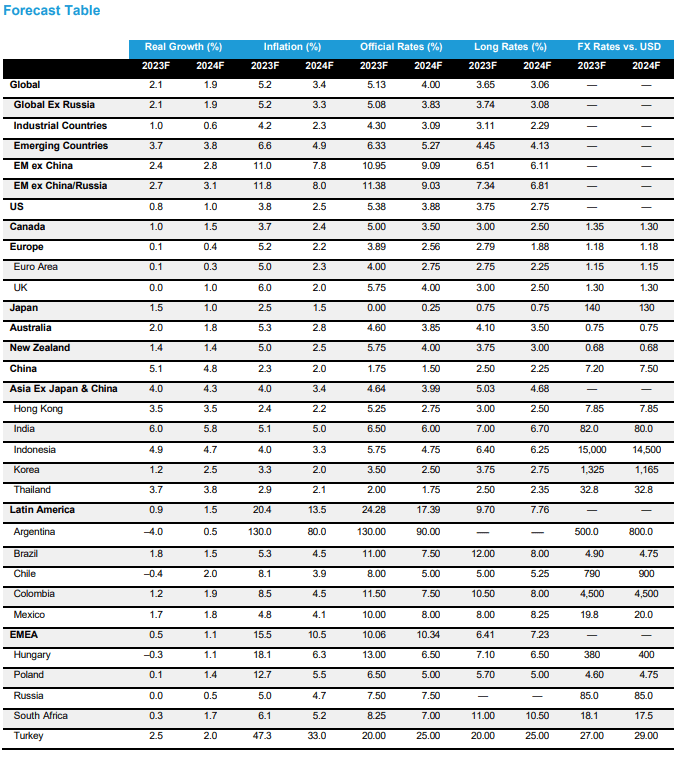

Growth and inflation forecasts are calendar year averages except US GDP, which is forecast as 4Q/4Q. Interest-rate and FX rates are year-end forecasts.

Long rates are 10-year yields unless otherwise indicated.

The long rates aggregate excludes Argentina and Russia; Argentina is not forecast due to distortions in the local financial market; Russia is not forecast because the local market is inaccessible to foreign investors.

Real growth aggregates represent 29 country forecasts not all of which are shown.

Investment Risks to Consider

The value of an investment can go down as well as up and investors may not get back the full amount they invested. Past performance does not guarantee future results.

Important Information

Note to All Readers: The information contained here reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion in this material will be realized. Past performance does not guarantee future results. The views expressed here may change at any time after the date of this publication. This document is for informational purposes only and does not constitute investment advice. AllianceBernstein L.P. does not provide tax, legal or accounting advice. It does not take an investor's personal investment objectives or financial situation into account; investors should discuss their individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer or solicitation for the purchase or sale of any financial instrument, product or service sponsored by AB or its affiliates. Note to Canadian Readers: This publication has been provided by AB Canada, Inc. or Sanford C. Bernstein & Co., LLC and is for general information purposes only. It should not be construed as advice as to the investing in or the buying or selling of securities, or as an activity in furtherance of a trade in securities. Neither AB Institutional Investments nor AB

L.P. provides investment advice or deals in securities in Canada. Note to European Readers: This information is issued by AllianceBernstein Limited, a company registered in England under company number 2551144. AllianceBernstein Limited is authorized and regulated in the UK by the Financial Conduct Authority (FCA -Reference Number 147956). Note to Readers in Japan: This document has been provided by AllianceBernstein Japan Ltd. AllianceBernstein Japan Ltd. is a registered investment-management company (registration number: Kanto Local Financial Bureau no. 303). It is also a member of the Japan Investment Advisers Association; the Investment Trusts Association, Japan; the Japan Securities Dealers Association; and the Type II Financial Instruments Firms Association. The product/service may not be offered or sold in Japan; this document is not made to solicit investment. Note to Australian Readers: This document has been issued by AllianceBernstein Australia Limited (ABN 53 095 022 718 and AFSL 230698). Information in this document is intended only for persons who qualify as "wholesale clients," as defined in the Corporations Act 2001 (Cth of Australia) and should not be construed as advice. Note to Singapore Readers: This document has been issued by AllianceBernstein (Singapore) Ltd. (“ABSL”, Company Registration No. 199703364C). AllianceBernstein (Luxembourg) S.à r.l. is the management company of the portfolio and has appointed ABSL as its agent for service of process and as its Singapore representative. AllianceBernstein (Singapore) Ltd. is regulated by the Monetary Authority of Singapore. This advertisement has not been reviewed by the Monetary Authority of Singapore. Note to Hong Kong Readers: This document is issued in Hong Kong by AllianceBernstein Hong Kong Limited (????????), a licensed entity regulated by the Hong Kong Securities and Futures Commission. This document has not been reviewed by the Hong Kong Securities and Futures Commission. Note to Readers in Vietnam, the Philippines, Brunei, Thailand, Indonesia, China, Taiwan and India: This document is provided solely for the informational purposes of institutional investors and is not investment advice, nor is it intended to be an offer or solicitation, and does not pertain to the specific investment objectives, financial situation or particular needs of any person to whom it is sent. This document is not an advertisement and is not intended for public use or additional distribution. AB is not licensed to, and does not purport to, conduct any business or offer any services in any of the above countries. Note to Readers in Malaysia: Nothing in this document should be construed as an invitation or offer to subscribe to or purchase any securities, nor is it an offering of fund-management services, advice, analysis or a report concerning securities. AB is not licensed to, and does not purport to, conduct any business or offer any services in Malaysia. Without prejudice to the generality of the foregoing, AB does not hold a capital-markets services license under the Capital Markets & Services Act 2007 of Malaysia, and does not, nor does it purport to, deal in securities, trade in futures contracts, manage funds, offer corporate finance or investment advice, or provide financial-planning services in Malaysia. Important Note for UK and EU Readers : For Professional Client or Investment Professional use only. Not for inspection by distribution or quotation to, the general public.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

www.AllianceBernstein.com

© 2023 AllianceBernstein L.P.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Global Macro Outlook - Third Quarter 2023