GMRE - Global Medical REIT: A Hold Despite Improving Performance

2023-11-20 21:33:09 ET

Summary

- In Q3, 2023, GMRE delivered an improved performance with the underlying FFO finally breaking the momentum of a constant decline.

- The key reasons for the growth in FFO per share relative to Q2, 2023 lay in the embedded rent escalators and reduced interest costs stemming from successful property sales.

- GMRE sold an additional property at a cap rate of 5.3%, which is clearly an indicator of high quality portfolio, where the correct value is not reflected in the books.

- As a result of successful divestitures and improving property performance, GMRE's leverage profile has significantly strengthened.

- Yet, the risks still remain on the debt refinancing front, where GMRE is subject to higher interest costs from gradual debt rollovers over the next 3-year period.

On November 6th, Global Medical REIT ( GMRE ) circulated its Q3, 2023 results , which were more or less in line with the market expectations on the FFO and revenue front.

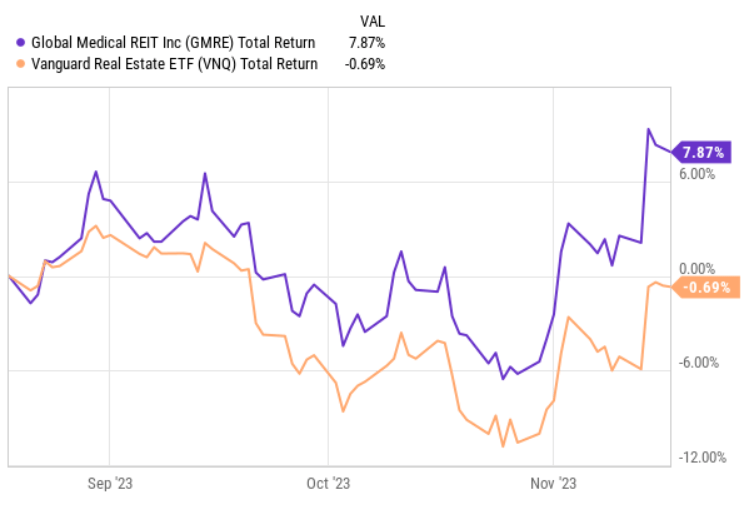

After the earnings were published, GMRE experienced a favourable upward movement in its share price, which came on top of the registered gains (or rather alpha versus REIT market) during the post Q2, 2023 period.

{kind=link}

Ycharts

Over the Q3 period, GMRE managed to outperform the broader REIT market by ~8% on a total return basis.

On September 10th, right after GMRE published Q2 results, I issued an article elaborating on why my previous stance on GMRE's ability to service its dividend (and thus being an attractive investment) was not anymore relevant.

The key reasons for this were the following:

- GMRE devised a successful hedging transaction (i.e., swap agreement), which capped the floating rate debt at ~4% over the next couple of years.

- It also made several divestitures at rather attractive cap rates that helped further de-risk the balance sheet by bringing down the floating rate debt.

- The business or operational metrics remained resilient with growing same store NOI and almost unchanged occupancy ratio.

The bottom line in my previous article was that based on the successful (aforementioned) results, GMRE has become a more predictable dividend-paying stock despite its AFFO payout revolving around 100%.

The essence is that GMRE's FFO generation is linked to periodic rent escalators, which coupled with juicy divestitures at cap rates well below what is recorded in the books helps fully mitigate the risk of higher interest costs destroying the ability to service quarterly dividends.

For example, each divestiture at a cap rate that is below the one that is reflected in the books, allows GMRE to recognize additional gains that could be used to either further reduce the debt component or channel towards fresh acquisitions.

Q3 in a nutshell

Let's now take a look at the most recent results to understand the stock market's motivation to reprice GMRE higher and whether GMRE should remain a hold.

At the FFO level, the third quarter resulted in a decrease of $0.01 per share compared to third quarter of last year. On the AFFO front, the decrease was $0.02 per share over a comparable period. The key reason for this is higher interest costs that are associated with GMRE's floating rate debt.

With that being said, we have to appreciate the rate of change effects relative to the Q2, 2023. If we measure the FFO and AFFO results against the most recent comparables, the picture looks far better. Q3, 2023 was the first quarter in a while when GMRE managed to register a positive growth in its FFO per share figure. On a quarter-to-quarter basis, AFFO remained flat.

The fact that the underlying cash flows have finally stabilized and, in fact, assumed a slightly positive momentum, has provided the market a reason to reprice the stock accordingly.

From the operations perspective, the portfolio remained solid as well.

The overall occupancy landed at a strong 96.7% with the weighted average lease term of 5.7 years that is subject to 2.1% annual rent escalators.

Yet, in my opinion, the most important takeaway from the recent quarter lied in the disposal (or property sale) activity segment.

During the quarter, GMRE sold medical office at a 5.3% cap rate , receiving gross proceeds of $10.1 million and resulting in a gain of $2.3 million. With this sale, the Company marked its sixth YTD divestiture at a weighted average cap rate of 6.3%. The gain component from these divestitures has resulted in $15.6 million or, approximately, one quarter of GMRE's FFO generation.

In the context of the prevailing interest rate environment, capturing so low cap rates is very challenging. Even before the FED started hiking interest rates, ~6% cap rates were deemed quite attractive (to say the least). So, considering where the interest rates are now and that GMRE operates its properties in tertiary markets, the recent property sale transactions could be deemed as highly successful. In my view, this speaks of GMRE's ability to find properties with great prospects and enhance them via targeted investments to bring down the tertiary market discounts.

As a result of this, GMRE has managed to further de-risk its balance sheet by retiring a portion of its floating rate debt. As of Q3, 2023, GMRE had 89% of its debt fixed and the overall leverage ratio at 44.2%, which is clearly below the sector average . Plus, due to the reduction of leverage profile, GMRE's credit facility pricing has now improved by 15 basis points.

GMRE Investor Relations

While GMRE's aggregate leverage ratio is solid, the underlying debt composition is still skewed towards a higher risk spectrum.

Namely, the most significant concern is the short weighted average maturity term of GMRE's debt. Based on the current debt maturity profile, we can easily imply that GMRE will have to assume a notable refinancing risk over the foreseeable future. The risk here is not so much on the access to financing, but rather on the effects from the higher interest rate costs. Considering the interest rate level on GMRE' floating rate debt, we can estimate that there should be additional 200 - 300 basis points coming on top of the existing financing when new debt rollovers take place.

Against the backdrop of ~100% FFO payout ratio, this does not look promising for dividend-seeking investors as any incremental headwind on the cash flows could place the Company in an unsustainable position to accommodate the existing dividend payments.

Nevertheless, according to Jeffery Busch - Chairman, President & CEO as per Q3, earnings call:

We feel safe with the dividend. We think we sort of hit a bottom here. We sold out a bunch of properties brought down our variables in debt we still get our increases every year and our increases every year are now exceeding what the additional debt costs could possibly be unless something gets too wild. But we think we're okay with the dividend. And I totally expect so there's no move to do anything with it.

The main point here is that the annual lease income of ~$144 million (LTM basis) is subject to ~2% rent escalators, which provide additional cash flows that, in turn, are sufficient to offset the pressures stemming from the gradual repricing of GMRE's ~$626 debt portfolio (or $557 million if adjusted for the floater that already now is based on the market level financing costs).

I am, however, a bit more skeptical about CEO's assumption that the rent escalators will be totally sufficient to offset higher financing costs. This is pure mathematics - i.e., annual lease income having both smaller base and lower rate of change effects relative to the outstanding debt stack that is potentially subject to doubling of financing costs over the next ~3 years.

There are three elements that could help GMRE keep the dividend safe, at a sustainable level:

- Further divestitures at similar cap rates that have been registered in the most recent quarters that would unleash additional gains from which to repay portions of maturing debt, while keeping the cash flow and dividend payment level in check.

- Debt refinancing at more attractive levels than currently the floater is priced. This is fully possible given that the Company has a lot of flexibility to attract secured (based on mortgage) financing and tap into the longer end of the maturity profile, thereby decreasing the risk premiums.

- Dropping Fed Fund's rate.

The bottom line

GMRE has delivered sound Q3 results with finally improving quarterly FFO momentum and still resilient underlying portfolio performance. An additional property sale at 5.3% cap rate provided not only a benefit to GMRE's balance sheet, but also sent a direct signal to the market of its high quality portfolio, where the right value is not fully reflected in the books.

As a result of the resilient performance and realized gains from the property sales, GMRE has managed to optimize its balance sheet bringing the leverage ratio down to ~44% that is below the sector average.

Nevertheless, the relatively short debt maturity profile of ~3 years imposes a significant risk factor to the dividend seeking investors, especially against the backdrop of close to 100% FFO payout. If all of the currently fixed debt maturities were to reprice to interest rates, which are more in line with the prevailing market levels, GMRE's FFO payout level would clearly exceed 100%.

Yet, for this, there are a couple of mitigants such as the embedded rent escalators, potential to make further divestitures and attracting encumbered debt proceeds.

In my humble opinion, GMRE is still a hold. I would prefer to see first major refinancing and how GMRE deals with higher interest costs before deciding on a buy rating.

For further details see:

Global Medical REIT: A Hold Despite Improving Performance